Staring down an insurance offer that feels way too low? A car insurance appraisal is your secret weapon. It’s a formal, detailed valuation from an unbiased expert who figures out what your car was really worth before the accident, giving you the hard evidence you need to fight a lowball offer.

What a Car Insurance Appraisal Actually Means

Don't mistake an appraisal for just another repair estimate. Think of it more like getting a second opinion from a specialist on your car's financial health. After a wreck, your insurance company will slide an offer across the table. If that number makes you cringe, an independent appraisal is your official counter-argument—a way to prove your car’s true value and get the payout you deserve.

This step is most critical in two situations: when your car is declared a total loss, and when you're claiming diminished value (the loss in resale value even after perfect repairs). A huge part of this process involves a deep dive into the vehicle's condition, which is why many people turn to reliable vehicle inspection services to get the details right. The entire point is to get a fair, objective valuation that isn't influenced by the insurance company's bottom line.

Why an Independent Opinion Matters

Let's be honest: your insurer's valuation is often spit out by software that doesn't care about your car's pristine condition, the expensive new tires you just bought, or what similar cars are actually selling for in your town.

An independent appraiser, on the other hand, does the hard work. They perform a hands-on, detailed review of your vehicle. They become your advocate, focused on one thing: calculating an accurate Actual Cash Value (ACV) based on real-world facts, not just an algorithm.

This independence completely changes the conversation. It brings an expert report to the negotiating table that the insurance company can't just ignore.

An accurate, independent appraisal is your leverage. It replaces the insurer’s opinion with verifiable facts, forcing a more equitable discussion about your vehicle's true pre-accident worth.

The Modern Appraisal Landscape

The game has changed over the years. With new tech and shifting market dynamics, the appraisal process has gotten more sophisticated. U.S. auto insurers have improved their combined ratios to around 95.1%, which means they're getting smarter about managing claims and assessing damage, even as repair costs soar.

What does that mean for you? It means insurers are more dialed-in than ever, making a truly independent expert crucial for ensuring you don’t get left behind. You need someone in your corner who knows the market just as well as they do.

Navigating Total Loss vs. Diminished Value Claims

After a car accident, the appraisal process heads down one of two very different roads, and it all comes down to a single question: can your car be fixed? The answer determines whether you'll be dealing with a Total Loss or a Diminished Value claim.

Each path requires a unique appraisal strategy to make sure you get the settlement you deserve. It’s the difference between getting a check to replace your wrecked car and getting a check to make up for the value it lost because of the accident history. Knowing where you stand is the first step toward protecting your wallet.

Total Loss Appraisals: The Value Before the Crash

If the repair costs are more than your car is worth—or at least a high percentage of its value, depending on your state's laws—the insurance company will declare it a total loss. This is the point of no return. It simply doesn't make financial sense to fix the vehicle.

In this scenario, the appraisal's entire purpose is to pin down the car's Actual Cash Value (ACV) right before the crash happened. This isn't about what you originally paid for it. It's about what it was worth on the open market a moment before the collision, factoring in its age, mileage, options, and overall condition. Getting the ACV right is everything, as this number is the foundation for your settlement to buy a replacement vehicle.

A total loss appraisal doesn't focus on the damage. It's all about establishing a precise, defensible market value for your car before the accident, so you can buy a comparable vehicle without losing money.

When an insurer’s offer feels low, a strong independent appraisal provides a counter-argument. It's not just a number pulled from a database; it’s a detailed report backed by real-world market data for vehicles just like yours. A professional appraiser can provide a comprehensive total loss estimate that shows what your car was truly worth.

Diminished Value Appraisals: The Loss After Repairs

Now, let's flip the script. Your car was in an accident, but it's completely fixable. Even if the body shop does a perfect job and it looks brand new, your car now has something it can never get rid of: an accident history. This stain on its record permanently lowers its resale value.

That loss in value is called Diminished Value.

A diminished value appraisal is designed to calculate that exact financial hit. It measures the difference between what your car was worth before the accident and what it's worth now with a collision on its record. Just picture two identical used cars on a lot—one with a clean vehicle history report, and one that's been in a wreck. Which one do you think a buyer would pay more for? The answer is obvious.

This type of appraisal is the tool you need to recover that lost equity. Without it, you’re the one who ends up eating that loss when it's time to sell or trade in the car, and that’s not fair when the accident wasn't your fault.

Diminished Value vs. Total Loss Appraisals at a Glance

To make it even clearer, let's break down the key differences between these two appraisal types. This table shows you which process applies to your claim and what each one is meant to accomplish.

| Aspect | Diminished Value Appraisal | Total Loss Appraisal |

|---|---|---|

| Vehicle Status | Your car is repaired after an accident. | Your car is not repairable and is declared a "total loss." |

| Goal of Appraisal | To calculate the loss in market value after repairs. | To determine the vehicle's market value before the accident. |

| Compensation | Pays you for the drop in your car's resale value. | Provides a settlement so you can replace your vehicle. |

| When It's Used | When you keep your repaired car, but its value has now decreased. | When the cost of repairs is more than what the vehicle is actually worth. |

Ultimately, whether you're facing a total loss or a diminished value situation, an independent appraisal is your best bet for ensuring the insurance company's offer is fair and accurate.

Your Step-by-Step Guide to the Appraisal Process

Dealing with a lowball offer from your insurance company can feel like hitting a brick wall. It’s frustrating. But there’s a structured, proven path forward: the appraisal process. Let’s break down exactly what that looks like by following a real-world example. Imagine your car was totaled, and the insurer’s offer is thousands less than you know it’s worth. What now?

This is where you take control. Instead of just accepting the first number they throw at you, you decide to formally challenge it. This single decision to push back is what kicks off the entire car insurance appraisal process. It's the most powerful first step you can take.

Finding and Hiring Your Expert Appraiser

The insurance company has its experts; you need one in your corner, too. This is the time to find a certified, independent appraiser. You're not just looking for a mechanic—you need a specialist who lives and breathes vehicle valuation disputes and knows how to counter the tactics insurers use to undervalue claims.

An appraiser’s job is to build an ironclad, evidence-based case for your vehicle's actual pre-accident value. You’ll want to look for someone with solid credentials, a history of positive client reviews, and specific experience with total loss claims. Once you find the right fit and hire them, you'll need to hand over all your documentation, such as:

- The insurance company's initial valuation report.

- Your vehicle's maintenance history and recent repair records.

- Receipts for any recent upgrades, like new tires or a premium stereo system.

Think of this paperwork as the raw material your appraiser will use to construct a compelling, fact-based counter-offer.

Preparing for the Vehicle Inspection and Report

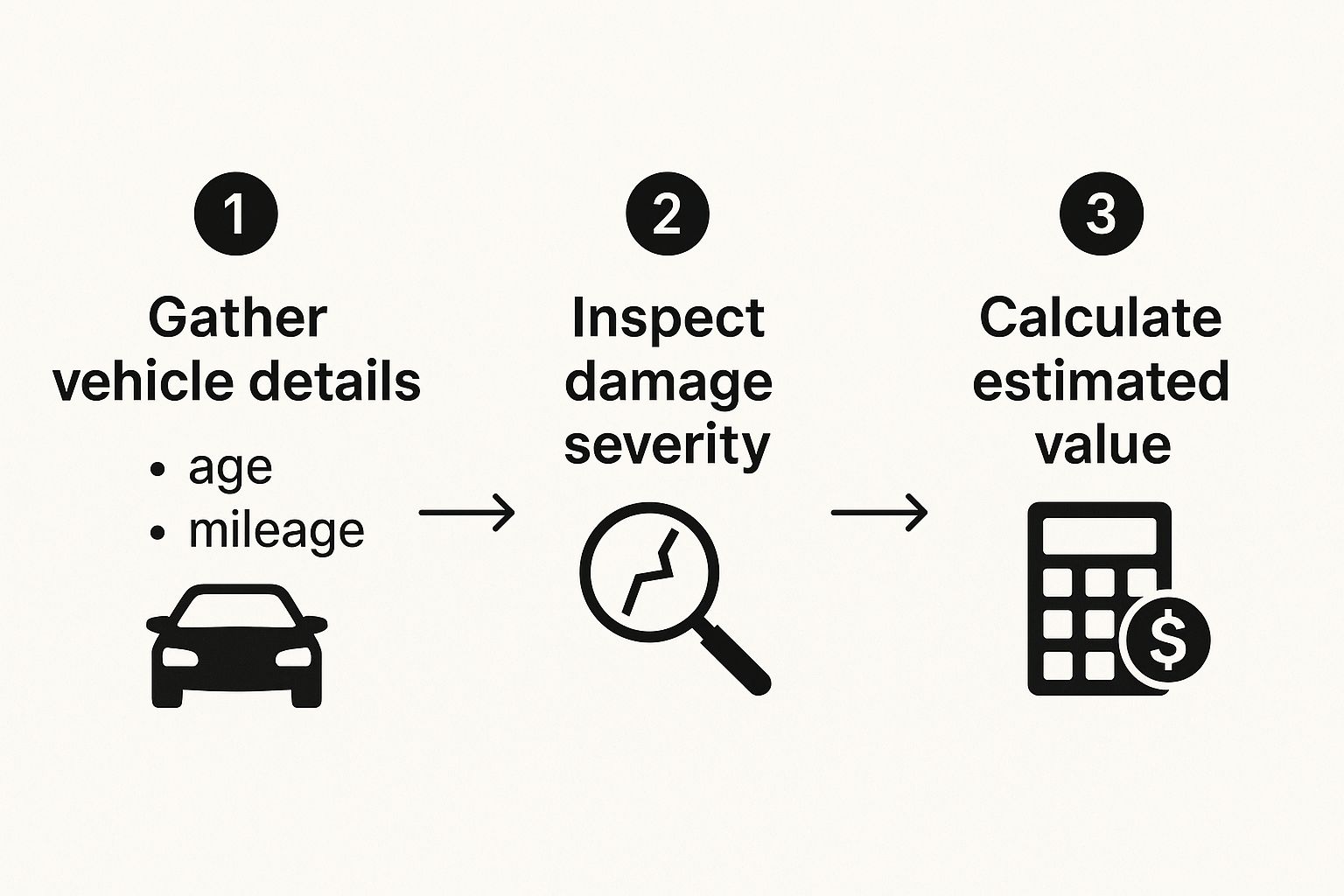

Next up is the hands-on part: the physical inspection. Your appraiser will go over your vehicle with a fine-toothed comb, documenting its exact condition, options, and any unique features that the insurer's automated system almost certainly overlooked. This in-person assessment is absolutely critical for establishing an accurate, real-world value.

This diagram illustrates how a professional appraiser moves from gathering initial data to calculating the final, defensible value.

It’s a methodical approach that ensures every detail, from the low mileage to the local market conditions, is factored into the final number.

A successful appraisal hinges on undeniable proof. The appraiser's final report isn't just an opinion—it's a detailed, market-driven analysis built to stand up to scrutiny from the insurance company.

Once the report is ready, you submit it to your insurer, officially disputing their initial offer. This elevates the claim from a simple back-and-forth negotiation to a formal disagreement backed by expert evidence. This is precisely how professional car insurance appraisals level the playing field. For a closer look at the nuts and bolts, see our comprehensive guide on auto insurance appraisals.

It's true that technology is changing the game. Insurers increasingly use AI and remote inspection apps for their initial estimates to speed things up. But while those tools are efficient for simple claims, nothing replaces an independent, human-led inspection when it comes to getting an accurate valuation in a complex dispute. With your expert's report submitted, you're now set for the final phase: either a new round of negotiations or formally invoking your policy’s appraisal clause.

Using the Appraisal Clause in Your Policy

https://www.youtube.com/embed/qhOwUorcG7Q

Hidden deep within the fine print of your auto insurance policy is a powerful tool most people don't even know exists. It’s called the appraisal clause, and it gives you the contractual right to formally dispute your insurer’s valuation of your vehicle.

Think of it as a built-in tie-breaker. When you and the insurance company are at a complete standstill over the value of your car, this clause provides a structured, fair process to resolve the disagreement. It’s your official way of saying, "I don't accept your offer, and I'm escalating this to a panel of experts."

How to Officially Invoke the Clause

Getting the ball rolling requires more than just a phone call. You need to formally notify your insurer in writing that you’re invoking the appraisal clause to dispute their settlement offer. A clear, direct letter is all it takes.

Once you’ve sent that demand, the process kicks into gear. Here’s how it works:

- You hire an independent appraiser. This is your expert, someone who works for you to determine the true value of your vehicle.

- The insurance company hires their own appraiser. This person will represent the insurer’s position.

- The two appraisers select a neutral umpire. If they can't agree on one, a court will appoint one. This person acts as the impartial third party.

The final settlement amount is locked in as soon as any two of the three parties agree on a value—your appraiser and the umpire, or the insurer's appraiser and the umpire. That decision is almost always final and legally binding on both you and the insurance company.

The appraisal clause is your contractual right to level the playing field. It takes the final decision out of the insurance company's hands and places it into a neutral, three-party system designed for a fair outcome.

Understanding the Costs and Timeline

Invoking the clause does come with some out-of-pocket costs. You’re responsible for paying your appraiser, and you and the insurance company split the cost of the umpire’s fee. While it’s an investment, the potential increase in your settlement often far outweighs the expense.

The whole process can take anywhere from 30 to 90 days, depending on how complex the claim is and how quickly the appraisers and umpire can coordinate. For a more detailed look at the procedure, you can learn more about the insurance appraisal clause and how it really works.

It's no secret that insurers are using more sophisticated data and analytics to come up with their valuations. Having a human expert who understands your car's specific history, condition, and features is your best counter to a lowball offer based on a generic algorithm. An independent appraiser brings that crucial human element to the table.

Actionable Tips to Maximize Your Settlement

Getting a fair settlement isn’t about sitting back and waiting for a check. You have to be your own best advocate, and that means getting actively involved in your claim. When it comes to car insurance appraisals, showing up prepared with rock-solid evidence can completely change the game and put real money back in your pocket.

Think of it this way: you're building a case for what your car was actually worth a moment before the accident. The insurance company's initial offer is often based on a simple algorithm, but your job is to paint a complete picture that their system missed. The more proof you have, the tougher it is for them to stick to a lowball number.

Compile Meticulous Documentation

Long before your appraiser lays eyes on your vehicle, you should be gathering every shred of paper that proves its value. This isn't just paperwork; it's your ammunition. A well-organized file gives your appraiser the facts they need to fight for you. Don't leave anything out.

Your evidence file should be airtight. Start with these:

- Maintenance Records: Every oil change, tire rotation, and tune-up receipt tells a story of a well-maintained vehicle. This directly boosts its pre-accident value.

- Receipts for Recent Upgrades: Did you drop $800 on new tires last month? Find that receipt. The same goes for a new battery, brakes, or an upgraded sound system. These investments count.

- Original Window Sticker: If you happen to have the original Monroney sticker, it’s gold. It lists every single factory option and package, which is critical for establishing an accurate starting value.

Prepare for the Inspection

Believe it or not, first impressions count. Before the appraiser shows up, give your car a thorough cleaning, inside and out. A clean car is easier to inspect and sends a powerful, non-verbal message: "I took excellent care of this vehicle." It helps remove any doubt about its condition before the crash.

An appraiser’s job is to uncover the vehicle's true market value. When you present a clean car with detailed records, you make their job easier and reinforce that you were a meticulous owner. That pride of ownership translates into a stronger valuation.

You should also do a little homework yourself by researching "comps," or comparable vehicles. Find at least three local listings for the exact same make, model, and year with similar mileage. This kind of real-world market data is one of the most powerful tools you have.

Have these examples ready to share with your appraiser. It’s hard to argue with what similar cars are actually selling for right down the street.

Answering Your Questions About Car Insurance Appraisals

When you're trying to settle a claim, the appraisal process can feel a bit confusing. It's only natural to have questions, and getting good answers is the key to making smart decisions and getting the money you deserve.

Let's walk through some of the most common questions people have. My goal here is to give you clear, straightforward answers so you can tackle your claim with confidence.

How Much Does an Independent Car Appraisal Cost?

This is usually the first thing people ask, and for a good reason. You need to know if it's a worthwhile investment.

Generally, you can expect to pay somewhere between $300 and $700 for a high-quality, independent appraisal. That price isn't set in stone, though. A few things can move the needle, especially how complicated your claim is. A straightforward total loss appraisal on a common vehicle will likely be on the lower end, while a complex diminished value claim might cost more.

An appraiser’s experience and location also play a part, as does the type of vehicle. A seasoned pro who's an expert in niche vehicles might charge more, but that expertise often pays for itself many times over by uncovering value the insurance company completely missed.

Can I Get an Appraisal for a Classic or Modified Car?

Not only can you, but you absolutely should. For unique vehicles, an independent appraisal isn't just a good idea—it's essential.

Why? Because the standard software insurance companies use is terrible at valuing anything out of the ordinary. It’s designed for cookie-cutter cars, not your prized possession.

These automated systems have no way of understanding the real value of:

- Custom modifications like a built engine, a professional paint job, or a top-of-the-line suspension.

- The rarity and history that make a classic car so special.

- The quality of a restoration, which is a huge factor in a collector car’s worth.

You need to find an appraiser who specializes in classic, custom, or modified vehicles. They live and breathe this stuff. They know the market, have the right connections, and can properly document every last detail that makes your car valuable. Without one, you're leaving a lot of money on the table.

Using an insurance company's valuation for a classic car is like asking a family doctor to perform brain surgery. You need a specialist who truly understands the intricate details and market realities of what makes your vehicle unique.

Is the Appraisal Clause Available in Every State?

The appraisal clause is your most powerful tool for fighting a lowball offer, but it’s not a given everywhere. While it's included in most auto insurance policies, the rules—and sometimes its very existence—can differ depending on state law and your specific contract.

Some states have laws that dictate exactly how the process works. In others, it comes down to whatever is written in your policy. That’s why you have to do your homework before trying to invoke it.

Your first move should always be to pull out your insurance policy and read it carefully. Look for a section called "Appraisal," "Mediation," or something similar like "Dispute Resolution." If you're struggling to find it or the legal jargon is confusing, it's time to talk to an independent appraiser or an attorney. They can tell you exactly what your rights are where you live. Never just assume you have this option until you've seen it in black and white.

If you're dealing with a lowball offer on your total loss or diminished value claim, you don't have to take it. Total Loss Northwest is here to help you fight for what your vehicle was actually worth. Our certified independent appraisers will invoke the appraisal clause for you, building the expert case needed to get the fair settlement you’re owed. Take control of your claim today by visiting us at https://totallossnw.com.