Even after the best body shop in town makes your car look brand new, its value has taken a permanent hit. This drop is called diminished value, and it happens because an accident history attaches a permanent stigma to your vehicle. The repairs might fix the dents, but they can't erase the car's past.

The Hidden Financial Cost of a Repaired Vehicle

Let’s put you in the buyer's seat for a moment. You’re looking at two identical used cars—same make, model, year, and mileage. One has a squeaky-clean vehicle history report. The other was in a collision but has been professionally repaired and looks perfect.

Which one do you buy? More importantly, which one would you expect to pay less for?

That right there is the essence of inherent diminished value. It's the automatic, unavoidable loss in resale value that kicks in the second an accident is documented. Even if the repairs were flawless and used only OEM parts, that history is now a permanent part of the car's record.

Why Perfect Repairs Don't Restore Full Value

Think of it like a collectible. A mint-condition comic book is worth a fortune. But one with a repaired tear, no matter how expertly fixed, will never command the same price. The damage, and the story behind it, is now part of its identity. The same principle applies to your car.

This isn't just a feeling; it's a hard market reality driven by vehicle history reports from services like CARFAX and AutoCheck. Today, nearly every savvy buyer and dealership pulls one of these reports. An accident record is a huge red flag that immediately makes them devalue the car.

For example, a 2017 Toyota Camry with a clean slate might be worth $18,000 on trade-in. The exact same car with a documented rear-end collision? You might only be offered $13,500, even if it looks perfect. That’s a 25% loss in value. Research consistently shows that a vehicle with an accident history will fetch 10% to 25% less at trade-in, as detailed in this analysis of post-collision depreciation.

Repair Quality vs Market Reality

This quick comparison shows the disconnect between a car's post-repair condition and its actual market value.

| Factor | Perception After Repairs | Actual Market Value |

|---|---|---|

| Physical Condition | Looks and drives like new. | May be mechanically sound, but still viewed as "damaged goods." |

| Safety | Repaired to manufacturer specs. | Buyers are skeptical about long-term structural integrity. |

| Resale Potential | Owner sees it as fully restored. | The market sees a red flag on the CARFAX report, lowering offers. |

Ultimately, the insurance company pays to fix the visible, physical damage. But they rarely volunteer to pay for this invisible—yet very real—loss in market value.

Your vehicle is now part of a less desirable category: "cars with a story." Buyers will always pay a premium for a car without one, forcing your repaired vehicle to compete at a lower price.

Grasping this fundamental drop in value is the first and most critical step. It helps you understand the full financial impact of the accident and empowers you to pursue the full compensation you're actually owed.

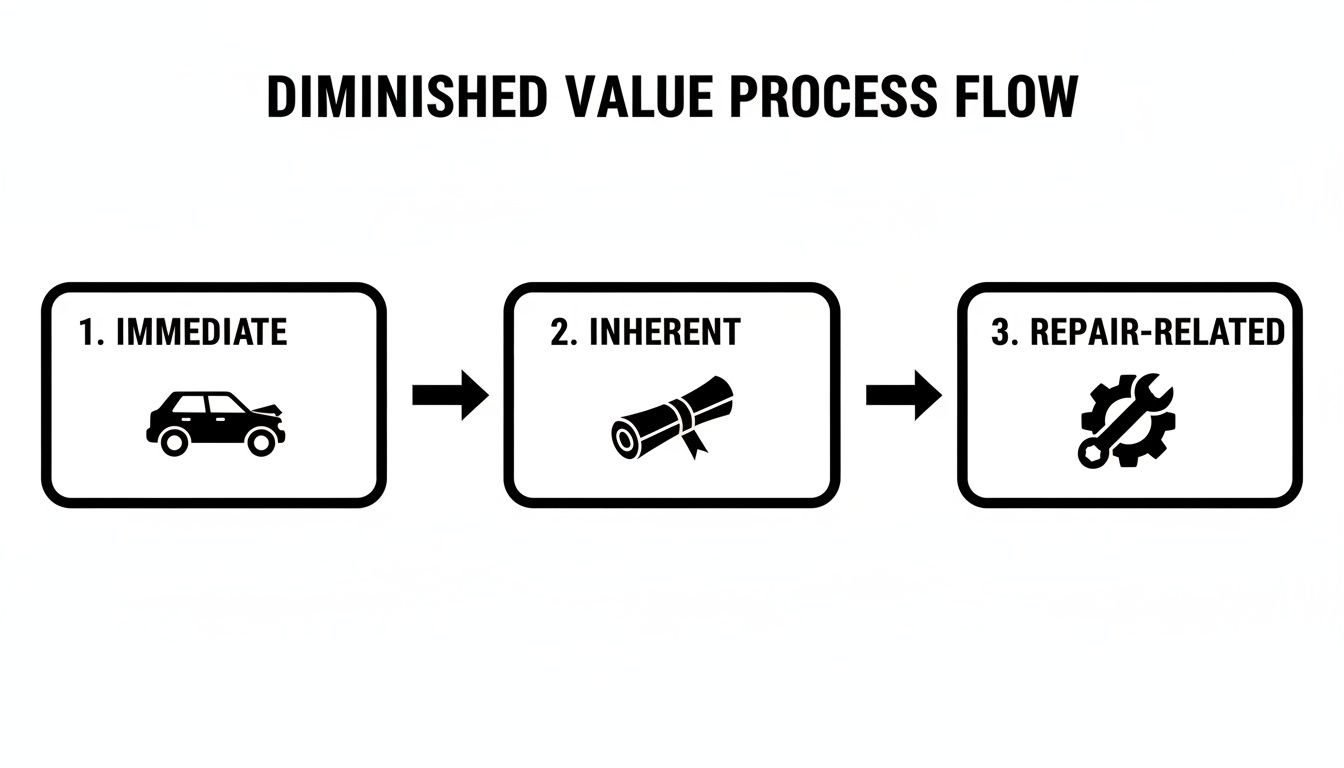

What Are the Three Types of Diminished Value?

When your car is in a wreck, "diminished value" is the financial hit it takes, but it's not a single, one-size-fits-all number. Think of it as a loss that happens in three distinct stages.

Getting a handle on these categories is the key to building a solid claim. Each one represents a real, measurable loss that adds to the total financial damage you’re facing. Let's walk through them one by one.

Immediate Diminished Value

The moment of impact is the moment your car's value tanks. This instant drop is called immediate diminished value. It’s the difference between what your car was worth seconds before the crash and its value as a crumpled wreck, before any repairs have even been considered.

Imagine you own a beautiful antique vase worth $1,000. If it gets knocked over and shatters, its value in that moment is practically zero—maybe just the salvage value of the broken pieces. Even if a master artisan can fix it, right then and there, it's just a pile of fragments. This is the raw, on-the-scene loss.

Inherent Diminished Value

This is the big one—the most common and crucial part of most claims. Inherent diminished value is the permanent loss in market value that follows a car simply because it now has an accident history. Even if the repairs are flawless and it drives like it just rolled off the showroom floor, that stigma is impossible to erase.

Let's go back to that shattered vase. A world-class restorer could meticulously glue every piece back together, making the seams almost invisible. It looks whole again, but it will never be a "mint condition" piece. Any serious buyer would pay far less for the repaired vase than for an identical one that was never damaged.

Your car now has a permanent black mark tied to its Vehicle Identification Number (VIN). When a potential buyer pulls a CARFAX or AutoCheck report, they’ll see the accident. They simply won’t pay the same price as they would for an identical car with a clean record. This loss is baked in and can't be fixed with a new coat of paint.

This is the heart of your diminished value claim. It’s the money you lose at trade-in or resale, no matter how great the body shop's work was. The accident is now part of your car’s story, forever.

Repair-Related Diminished Value

Finally, you might also have repair-related diminished value. This happens when the repairs themselves are shoddy, which drags your car's value down even further than the accident history alone would have.

This loss is a direct result of poor craftsmanship, cost-cutting, or mistakes made by the body shop.

Here are a few common culprits that lead to this kind of value loss:

- Mismatched Paint: The new paint is a slightly different shade or doesn't have the same finish as the factory paint.

- Aftermarket Parts: The shop used cheaper, non-original (non-OEM) parts that don't fit or function as well as the manufacturer's.

- Bad Frame Alignment: The car's frame wasn't straightened back to precise factory specs, which can lead to handling problems or uneven tire wear down the road.

- Visible Flaws: You can spot sanding marks under the paint, see uneven gaps between body panels, or notice other clear signs of a rushed job.

In our vase analogy, this is like the restorer using cheap, yellowing glue or leaving behind sloppy, visible seams. The poor quality of the repair itself has made the vase even less desirable. This loss isn't from the original break, but from the clumsy attempt to fix it, and it stacks right on top of the inherent diminished value your car already has.

How Insurance Companies Calculate Your Car's Worth

When an insurance adjuster hands you a settlement offer, that number can feel like it came out of nowhere. It wasn't a guess, though. It’s the result of a highly standardized process, one that often works in the insurer's favor, not yours.

To come up with a value, they lean on powerful software platforms like CCC ONE and Audatex. These systems are massive databases that pull up "comps"—comparable vehicles that recently sold. The problem is, the adjuster often has a lot of leeway in picking those comps, and it’s not uncommon for them to select vehicles in worse condition or with lower price tags to anchor their offer on the low end.

The Problematic 17c Formula

One of the most infamous tools in their playbook is what’s known as the “17c formula.” It first popped up in a Georgia court case and has since been adopted by insurers everywhere for one simple reason: it almost always spits out a very low number for diminished value.

The formula starts by putting an immediate ceiling on your potential loss, capping it at just 10% of your car's pre-accident value. From there, it uses two "modifiers" to slash that number even further.

- Damage Modifier: This adjusts the value based on how bad the damage was. A small dent might get a low multiplier, while serious structural damage gets a higher one—but it's still just a multiplier on an already-capped number.

- Mileage Modifier: This second hit reduces the value based on your car's odometer reading, effectively penalizing you for having driven your own car.

As this shows, the total loss in value happens in stages—the immediate impact, the permanent stigma of an accident history, and any lingering issues from the repairs. A fair settlement should account for all three.

A Real-World Example of the 17c Formula in Action

Let's walk through a quick example to see just how dramatically this formula can shrink a legitimate claim. Say your car was worth $30,000 before the accident.

- Step 1: The Cap: The 17c formula immediately caps your maximum diminished value at 10%, or $3,000. That's the absolute most you can get, according to their math.

- Step 2: The Damage Modifier: Let's say the accident caused moderate frame damage. The insurer applies a 0.50 damage modifier, instantly cutting your claim in half to $1,500.

- Step 3: The Mileage Modifier: Your car has 60,000 miles on it, so they apply another modifier, this time 0.60. Your claim is now slashed down to just $900.

Just like that, a real loss that started at $3,000 gets whittled down to a $900 settlement offer. It’s a perfect illustration of why knowing their methods is your best defense. If you want a deeper dive into how that initial pre-accident number is determined, you can learn more about how to determine your car's Actual Cash Value in our detailed guide.

Insurers love formulas like 17c because they're predictable, systematic, and easy to defend. But what they conveniently ignore is the real world, where actual buyers will penalize a car with an accident history far more than this formula ever would.

The gap between the insurance company's math and market reality is huge. While their formula might suggest a loss of a few hundred dollars, real-world data shows moderate damage can erase 15-30% of a vehicle's value. Major damage can lead to losses of 50% or more.

This isn't just theory. CARFAX data confirms that simply having an accident on a vehicle's history report can wipe $500-$2,100 off its value on average—and for luxury models, that number is much higher. Understanding this disconnect is where your power to negotiate for a fair settlement truly lies.

Why Luxury and Collector Vehicles Suffer More

Not all cars are created equal, and that’s especially true when it comes to losing value after a wreck. While any accident will ding a car's worth, the financial hit on luxury, exotic, and collector vehicles is often in a different league entirely. The very things that make these cars so special—their prestige, engineering, and flawless condition—are the same things that make them so vulnerable to a massive drop in value.

Think about the different buyers. Someone shopping for a reliable Honda Civic is looking for a practical daily driver. An accident on its record isn't ideal, but if the price is right, they'll often overlook it. But the person in the market for a Porsche 911 or a classic Ford Mustang? They're not just buying transportation. They're buying a piece of automotive art, an investment, an experience. For that buyer, an accident history is almost always a deal-breaker.

The Expectation of a Perfect History

The high-end and collector car market just plays by a different set of rules. Buyers are incredibly discerning and they come with sky-high expectations. They want a car with a perfectly clean, verifiable history, with no hint of damage or major repairs in its past. An accident, no matter how minor, completely shatters that illusion of perfection.

This stigma permanently knocks the car down a few pegs. A collector car with a known damage history will always be the last one picked when a buyer is comparing it to one with a clean record. This forces the owner to slash the price just to get anyone to even consider it.

The heart of the matter is that the value of these vehicles is welded to their story—their provenance and originality. An accident adds a permanent, ugly chapter to that story, and serious collectors will make you pay for it.

On top of that, you have the sheer complexity of modern luxury cars. They are packed with sophisticated electronics, exotic materials like carbon fiber, and intricate safety systems that demand highly specialized (and very expensive) repair work. Buyers are right to be skeptical about whether these complex systems can ever be brought back to their exact pre-accident state. That doubt translates directly into a lower car worth after accident.

The Data Behind the Depreciation

The numbers don't lie, and they paint a pretty grim picture for high-end European brands. Post-accident data shows that German luxury car owners often see the biggest drops in value. For instance, a BMW or Mercedes-Benz that gets into a minor rear-ender in Washington State can easily lose 25-35% of its value. If the damage is major, that number can jump to a staggering 40-50% or more. For comparison, a Toyota with similar minor damage might only see a 10-15% drop. You can dive deeper into the data to see how different car brands are affected by diminished value and see the full scope of the problem.

Unique Challenges for Classic and Collector Cars

For classic and collector cars, the situation is even more precarious. Their value is almost entirely wrapped up in originality and condition.

- Original Parts: Trying to find original, period-correct parts for a repair can be a nightmare. You're often forced to use reproductions, which instantly devalues the car in the eyes of a purist.

- Specialized Labor: The skilled craftspeople who know how to properly repair these vehicles are few and far between, which drives up repair costs and invites intense scrutiny from potential buyers.

- Matching Numbers: For many classics, having "matching numbers" (the original engine, transmission, and other key components) is everything. A serious accident can compromise these parts, causing a catastrophic loss in value.

Because of these unique issues, insuring these cars is a whole different ballgame. Our guide on classic car insurance requirements breaks down how these policies differ from your standard auto insurance. For owners of these incredible machines, an accident isn't just an inconvenience—it's a major financial event that requires an expert's touch to minimize the damage.

Your Step-by-Step Action Plan to Recover Your Loss

Understanding what determines your car worth after accident is one thing. Actually getting a fair settlement from the insurance company is another battle entirely. Insurers aren't in the business of volunteering more money than they have to. It's up to you to build a rock-solid case with clear evidence and a smart strategy.

This is your playbook. Follow these steps to move from being a passive victim of a lowball offer to an active, informed advocate for your own financial recovery.

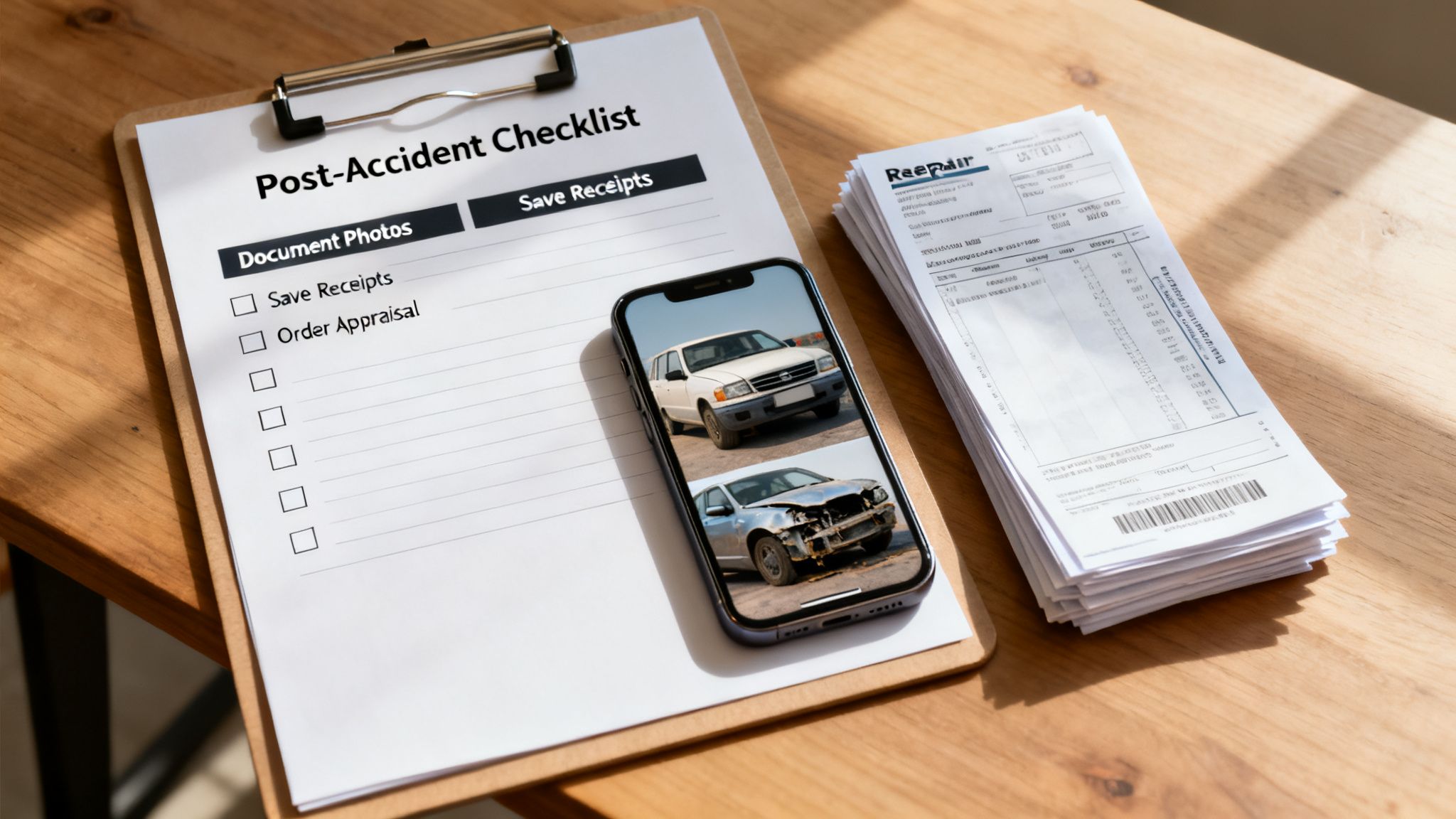

Step 1: Document Everything Immediately

Your claim starts the second the accident happens. The evidence you gather right there on the scene is often the most compelling because it’s raw and undisputed.

Whip out your smartphone and start taking photos and videos immediately. Don't just get a few wide shots of the cars. Get up close. Capture every single dent, scratch, and broken piece from multiple angles. Make sure you also document the other car's damage, the overall scene, road conditions, and any nearby traffic signs.

Think like an investigator building a case file. Every photo, receipt, and note is a piece of evidence that validates your claim and disputes the insurer's lowball tactics.

Your job as a documentarian doesn't stop there. Keep a detailed log of every single conversation you have with insurance adjusters, body shop managers, or anyone else involved. Jot down the date, time, the person's name, and a quick summary of what you talked about. This trail is invaluable.

Step 2: Organize Your Evidence

A messy pile of papers won't do you any good when it's time to negotiate. Create a dedicated folder—a physical one or a digital one on your computer—to house every single document related to your accident and vehicle. This is your official case file.

Arming yourself with organized evidence is the best way to show the insurer you're serious. The table below outlines what you need and why.

Your Essential Evidence Checklist

| Evidence Type | Why It Is Critical | How to Obtain It |

|---|---|---|

| Police Report | Provides an official, unbiased account of the incident, often noting fault. | Request a copy from the law enforcement agency that responded to the scene. |

| Repair Estimates | Shows the initial scope and cost of damages from different professional perspectives. | Get written estimates from at least two reputable body shops you trust. |

| Final Repair Invoice | This is your proof of what was actually done, itemizing parts (OEM vs. aftermarket) and labor. | The body shop provides this once repairs are complete and you've paid. |

| All Correspondence | Creates a paper trail of offers, statements, and promises made by the insurer. | Save every email and letter. Take notes during phone calls. |

| Photos & Videos | Visual proof is undeniable. It captures the severity of the damage before, during, and after repairs. | Use your smartphone. Be thorough and capture multiple angles and close-ups. |

With this file, you can tell the complete story of your loss and the efforts to make it right. It’s your most powerful tool in any negotiation.

Step 3: Order a Post-Repair Inspection

Just because your car looks shiny and new doesn't mean the repairs were done correctly. This is a step most people skip, and it's a huge mistake. A post-repair inspection from an independent, certified mechanic is crucial.

These experts can spot things you'd never notice—mismatched paint shades, poor panel alignment, or cheap aftermarket parts used where original equipment was promised. Their report can identify repair-related diminished value if the work is shoddy. It can also strengthen your claim for inherent diminished value by proving that even with high-quality work, the car is still not what it once was.

For a deeper dive, check out our guide on how to file a diminished value claim.

Step 4: Invoke the Appraisal Clause

So, you’ve done everything right, but the insurance company's offer is still ridiculously low and they won't budge. It's time to pull out the big gun: the Appraisal Clause.

Buried in the fine print of most auto policies, this clause gives you the right to formally dispute the insurer's valuation. When you invoke it, you hire your own certified, independent appraiser. The insurance company has to hire one, too. These two experts then negotiate to agree on a fair value.

If they can't reach an agreement, they bring in a neutral third party (an "umpire") to make a final, binding decision. This brilliant move takes the power away from the insurance company and their biased software and places it in the hands of qualified professionals. It’s the ultimate check and balance to ensure you get paid what you're truly owed.

Navigating Diminished Value Claims in Oregon and Washington

Crossing state lines can completely change the rules of the road for your insurance claim. While the idea of diminished value is the same everywhere, how you actually make a claim—and whether you’ll succeed—often boils down to local laws. If you're in the Pacific Northwest, getting a handle on the specific legal landscape in Oregon and Washington isn't just a good idea; it's critical to getting the fair settlement you deserve.

The core principles might be similar, but how they're applied in the real world can be worlds apart. This is why generic, one-size-fits-all advice you find online often doesn't work. To figure out your car's worth after an accident, your approach has to be built around the laws of the state where the claim is being filed.

Key Differences in Oregon and Washington

Both states are generally consumer-friendly when it comes to diminished value, but they have their own unique legal frameworks you have to work within. Knowing these rules can be the difference between a successful claim and a quick denial.

Here are a few key distinctions to keep in mind:

- Statute of Limitations: This is your legal deadline for filing a lawsuit. In Washington, you have three years from the date of the accident to file a property damage claim. Oregon is much more generous, giving you a six-year window.

- Legal Precedents: Both states have a history of court cases that firmly establish your right to claim diminished value. Washington courts have repeatedly sided with vehicle owners, recognizing that even the best repairs don't erase the financial loss. Oregon law is just as solid, making it clear that the "cost of repairs" is only one piece of the total damages you've suffered.

Your right to be "made whole" isn't just an insurance industry buzzword—it's backed by state law. An insurer can't legally claim that flawless repairs are good enough if your vehicle’s market value has still dropped.

First-Party vs. Third-Party Claims

One of the most important distinctions to understand is whether you're filing a "first-party" claim with your own insurance company or a "third-party" claim against the at-fault driver's policy.

- Third-Party Claims: In both Oregon and Washington, you are on very solid legal ground when pursuing a diminished value claim against the at-fault driver's insurance. Their client caused your financial loss, so their insurance is on the hook to make you whole—and that includes the drop in your car’s resale value.

- First-Party Claims: This is where things get complicated. Trying to claim diminished value from your own insurance company (say, under your collision coverage) is usually a non-starter. Most insurance policies are written with specific language that excludes this kind of loss.

Beyond just knowing the rules for your state, it helps to have a firm grasp of what is a diminished value claim at its core. This foundational knowledge makes you a stronger advocate for yourself, no matter where you live.

Ultimately, your best bet is to work with an appraiser who specializes in the Pacific Northwest. They live and breathe the local precedents, know exactly how insurers in the region operate, and can put together a claim that’s tailor-made to succeed under Oregon or Washington law.

Your Post-Accident Value Questions, Answered

Once you get a handle on the basics of diminished value, the "what if" questions usually start popping up. It's completely normal. The claims process can feel like a maze, and every situation has its own quirks.

Think of this section as a quick chat with an expert to clear up those lingering doubts. We’ll tackle the most common questions we hear from drivers every single day.

Can I File a Claim If I Was at Fault?

This is probably the number one question we get, and the short answer is almost always no. A diminished value claim is a third-party claim. That means you file it against the insurance company of the driver who caused the accident.

The logic is simple: their client's negligence is what caused your car to lose value, so their policy is on the hook to make you financially whole again. Your own collision coverage is there to fix the physical damage, not to compensate you for the hit to your car’s market price. In fact, most insurance policies have specific language that prevents you from claiming diminished value against your own coverage.

Will Filing a Claim Raise My Insurance Rates?

Nope. Filing a diminished value claim against the at-fault driver's insurance should not affect your insurance rates one bit. Your rates are tied to your own driving record and the level of risk you represent to your insurer.

Since you weren't responsible for the crash, your insurance company has no legitimate reason to penalize you. You’re simply holding another driver’s insurer accountable for a loss their policyholder caused.

How Long Does a Diminished Value Claim Take?

This is where it really "depends." The timeline for a diminished value claim can be all over the map, and a few key things will influence how quickly it gets resolved:

- The Insurer: Let's be honest—some insurance companies are just easier to work with than others.

- Your Evidence: A claim that's backed by a professional, well-documented appraisal usually moves much faster.

- The Negotiation: The amount of back-and-forth needed to agree on a fair number is a major factor.

A simple, clear-cut claim might wrap up in just a few weeks. However, a more complicated case, especially one the insurer decides to fight, could easily stretch out for several months. The key is to be patient and persistent.

Key Takeaway: The goal isn't just to get a check quickly; it's to get the right check. Rushing the process often means you're leaving a lot of your money behind.

Is It Worth Filing a Claim for an Older Car?

It can be. While it's true that newer, more expensive cars typically see the biggest drop in dollar value, an older car can still lose a significant chunk of its worth as a percentage. The only way to know for sure is to have an expert take a look.

A skilled appraiser can dig into your vehicle's specific pre-accident condition, its popularity in the used market, and the extent of the damage. They'll run the numbers to see if the diminished value is high enough to make a claim worthwhile. Don't just write it off because of the model year.

At Total Loss Northwest, we specialize in providing certified, independent appraisals that give you the leverage you need to secure a fair settlement. If you believe your vehicle's value has dropped after an accident, don't accept the insurance company's lowball offer. Visit us at https://totallossnw.com to learn how we can help you recover the money you're truly owed.