You've already been through the worst part. The crash. The tow truck. The call from the adjuster. Then the insurance company sends a value for your car, and your stomach drops because it doesn't look anything like what it would cost to replace it.

That reaction is usually right.

When an insurer labels your vehicle a total loss or brushes off the value hit after repairs, they're not handing you some sacred number from on high. They're giving you their number. Sometimes it's reasonable. Sometimes it's built on weak comparables, software shortcuts, or a version of your car that ignores what made yours worth more.

That's where a certified auto appraiser matters. Not as a fancy title. As a practical tool. If the offer is off, you need someone who knows how to document value in a way the insurance company has to take seriously.

I've seen drivers waste days arguing with adjusters over the phone when what they really needed was evidence. Not emotion. Not screenshots from random listings. A proper appraisal. If you're staring at a low settlement or wondering whether it's worth paying for help, this is how to make that decision like an adult and not like someone getting pushed around.

Your Guide to a Certified Auto Appraiser

A lot of people reach out after the same moment. The insurer says, “We've completed our valuation,” and what follows feels detached from reality. Your car was clean, maintained, low-mileage for its age, maybe upgraded, maybe hard to replace locally. None of that seems to show up in the payout.

You're not crazy if it feels off.

A certified auto appraiser is often the first real counterweight a driver has in that situation. Not a body shop. Not your cousin who buys and sells cars. Not an adjuster assigned by the same company writing the check. A valuation professional who can review the facts, inspect the vehicle or records, research the actual market, and put that conclusion into a formal report.

You don't win these disputes by saying the insurer is wrong. You win them by showing where their valuation breaks down.

That distinction matters. Insurance claims are paperwork fights disguised as customer service calls. If you don't bring organized, defensible evidence, the insurer controls the frame of the conversation.

Here's the practical truth. Hiring an appraiser isn't always necessary. If you drive a common vehicle with endless local comparables and the carrier's number is close, you may not need one. But if your car is unusual, especially clean, customized, collector-grade, or affected by a total loss or diminished value dispute, an independent appraisal can change the entire posture of the claim.

What drivers usually need to know fast

- Whether “certified” means anything useful: Sometimes yes, sometimes less than people assume.

- Whether an appraiser helps in your kind of claim: Total loss and diminished value are the big ones.

- Whether the fee is worth it: That depends on the size and type of valuation gap.

- What happens after the report: You submit it, and in some policies you can force a more formal appraisal process.

If you're trying to decide what to do next, start with one rule. Don't focus on the title alone. Focus on whether the appraiser can prove your vehicle's value in the exact kind of dispute you're in.

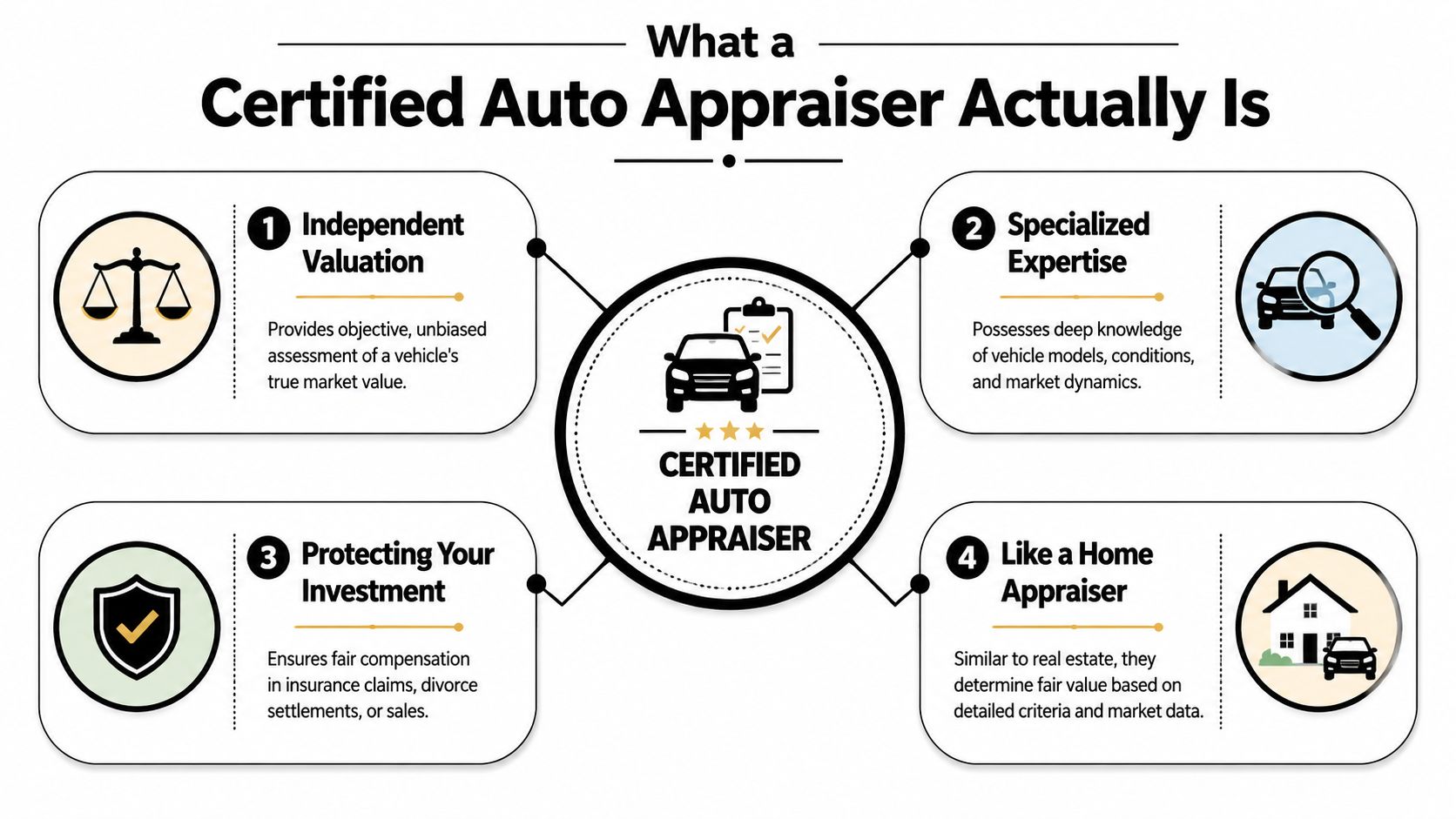

What a Certified Auto Appraiser Actually Is

“Certified auto appraiser” sounds more official than it often is. Drivers hear the label and assume there is one universal standard, one license, and one clear meaning. There isn't.

That does not make the title useless. It means you need to be pickier.

A certified auto appraiser is a vehicle valuation professional who documents what a car is worth for a specific purpose, such as a total loss claim, diminished value claim, divorce matter, estate valuation, or court dispute. The job is not to estimate repair cost. The job is to support a market value conclusion with evidence that can hold up when someone challenges it.

What the appraiser does

A real appraiser studies the vehicle itself, its condition, mileage, options, history, and the market it sells in. Then they match that information to a valuation method and explain the result in a formal report.

That method matters.

If the number is just a guess with a nice cover page, it will not help much in a claim. A useful appraisal shows how the appraiser reached the number, why the comparable vehicles make sense, and where adjustments were made for condition, equipment, prior damage, rarity, or other factors that change value.

What “certified” means, and what it does not

“Certified” can refer to training from a private appraisal organization, a professional designation, or a credential used in a narrow type of valuation work. It does not automatically mean the person is state-licensed for every purpose, accepted by every insurer, or qualified for every dispute.

That is where drivers get tripped up.

The safer question is not, “Are you certified?” Ask, “Have you handled my kind of claim before, and can your report stand up in negotiation, appraisal, or court?” That is the standard that matters. A polished credential means very little if the appraiser has never defended a diminished value report or never worked a total loss dispute involving a specialty vehicle.

As noted in the JurisPro automobile appraisal directory discussion, credentials in this field can vary widely by specialty and use case. That is why fit matters more than the title by itself.

Appraiser versus mechanic

A mechanic deals with damage and repair. An appraiser deals with value.

Those roles overlap at points, but they are not the same job. A mechanic may know what parts need replacement and what labor should cost. An appraiser answers a different set of questions:

- What the vehicle was worth before the loss

- What it is worth after repair, if diminished value is the issue

- Whether the insurer used weak comparables or bad condition adjustments

- Whether this vehicle falls outside the assumptions used by standard insurance software

That last point is a big one. Insurance systems handle common vehicles reasonably well. They often struggle with low-mileage cars, uncommon trims, heavy option packages, collector vehicles, well-kept older vehicles, and customized vehicles. In those cases, a qualified appraiser can save you real money because the standard process misses facts that drive value.

Practical rule: Hire the appraiser whose report fits your dispute, your vehicle, and your financial upside.

Here's the blunt version. “Certified” is a starting point, not a decision. If you drive an ordinary car and the insurer's number is close, the title may not matter much. If your vehicle is unusual or the valuation gap is large, the right appraiser can change the outcome.

Independent Appraiser vs The Insurer's Appraiser

Drivers are often lulled into a false sense of fairness. The insurance company may send someone called an appraiser, estimator, or valuation specialist, and people assume that person is neutral.

Usually, they're not neutral in the way you need.

The insurer's appraiser works inside the insurance claim system. That doesn't automatically make them dishonest. It does mean their role exists within a process designed to resolve claims for the carrier. Your independent appraiser works for one purpose only: documenting your vehicle's value from your side of the dispute.

The difference that actually matters

One is part of the claim machine. The other is your check on that machine.

Insurers often lean heavily on valuation software and standardized workflows because they have to process claims at scale. An independent appraiser is more likely to slow down, inspect the details, and challenge bad comparables or weak assumptions. That's exactly why people hire one.

| Attribute | Your Independent Appraiser | The Insurance Company's Appraiser |

|---|---|---|

| Who they answer to | You | The insurer |

| Main goal | Defend a supportable market value for your claim | Resolve the carrier's valuation within its claim process |

| Typical focus | Vehicle-specific evidence, condition, local comparables, claim context | Standardized workflow, insurer file requirements, consistency across claims |

| How disputes are handled | Pushes back on weak comparables and unsupported adjustments | Defends or revises the insurer's position inside the claim |

| Best use | Total loss disputes, diminished value claims, unusual vehicles | Routine claim handling |

Why common cars and unusual cars get treated differently

If you drive a common car with endless recent sales, the insurer's process may get reasonably close. There are enough comparables that software has less room to drift.

If your vehicle is unusual, the cracks start showing. Maybe it's a classic. Maybe it has meaningful upgrades. Maybe it has exceptionally low mileage or a condition profile that generic data doesn't capture well. In those cases, the insurer's number can miss by a lot because the system was never built for nuance.

Don't confuse speed with accuracy

Drivers often get pressured by tempo. The insurer moves quickly, sends paperwork fast, and sounds certain. That can make their valuation feel more authoritative than it is.

It isn't.

A fast number is still just a number. What matters is whether the underlying support is any good. If the adjuster can't clearly explain the comparables, adjustments, and condition assumptions, you should stop treating the valuation as settled fact.

The insurer's appraiser may be competent. They still aren't your advocate.

That's the key point. A certified independent appraiser is not there to create drama. They're there to create accountability. If the carrier's number is right, the evidence will show it. If it's low, you need someone who knows how to prove that cleanly.

When You Absolutely Need to Hire an Appraiser

This is the question that matters most. Not “What is a certified auto appraiser?” but “Is hiring one worth my money?”

My opinion is simple. Hire one when the value dispute is large enough or the vehicle is unusual enough that insurer software is likely to miss the actual number.

Total loss is the clearest trigger

If the insurer says your car is a total loss and the settlement feels low, that's the most common moment to get an appraiser involved. Once a vehicle is totaled, the fight is no longer about repair strategy. It's about actual cash value or fair market value.

That fight is won or lost on comparables, condition, options, and market relevance.

If the insurer used bad comps from outside your market, ignored major features, or treated a standout vehicle like an average one, a proper appraisal gives you a way to challenge the offer with structure instead of frustration.

Diminished value is the second big trigger

A lot of drivers miss this one. Even after proper repairs, a vehicle with an accident history often isn't worth what it was before. That's diminished value.

Documentation matters even more, because insurers don't usually hand out extra money just because you say resale value dropped. You need a report that explains pre-loss value, post-repair impact, and why the market would discount the vehicle.

The strongest cases are edge cases

Appraisal is most defensible for vehicles where standard insurer valuation software is weakest, meaning high-value, classic, custom, or atypical-condition vehicles. The strongest use cases are often these edge cases, not routine claims on common cars with abundant market comparables, according to Certified Auto Appraisers.

That lines up with what I'd tell any friend. If your car doesn't fit neatly into a software box, don't let software set the number without a fight.

A simple decision checklist

Hire an appraiser faster if any of these apply:

- Your vehicle is hard to replace locally: Collector cars, specialty trims, rare configurations, or unusual condition profiles.

- The insurer's comparables look weak: Wrong trim, wrong mileage band, wrong market, salvage history, or poor condition matches.

- You have a diminished value claim: Especially if the vehicle was in strong condition before the loss.

- Your car has documented upgrades or restoration work: Not every dollar spent adds equal value, but good documentation matters.

- The offer feels detached from the actual market: If replacing your vehicle for that amount seems unrealistic, pay attention.

Skip the appraisal if this sounds like your situation:

- A common car

- Plenty of obvious comparables

- A settlement number that matches the local market

- No meaningful disagreement on condition or trim

You don't hire an appraiser because you're mad. You hire one because the facts suggest value is being flattened.

The Appraisal Process and Report Explained

Most drivers assume an appraisal is just someone eyeballing the car and naming a price. A legitimate report is a lot more disciplined than that.

When done correctly, the process creates a paper trail. That's why it has influence.

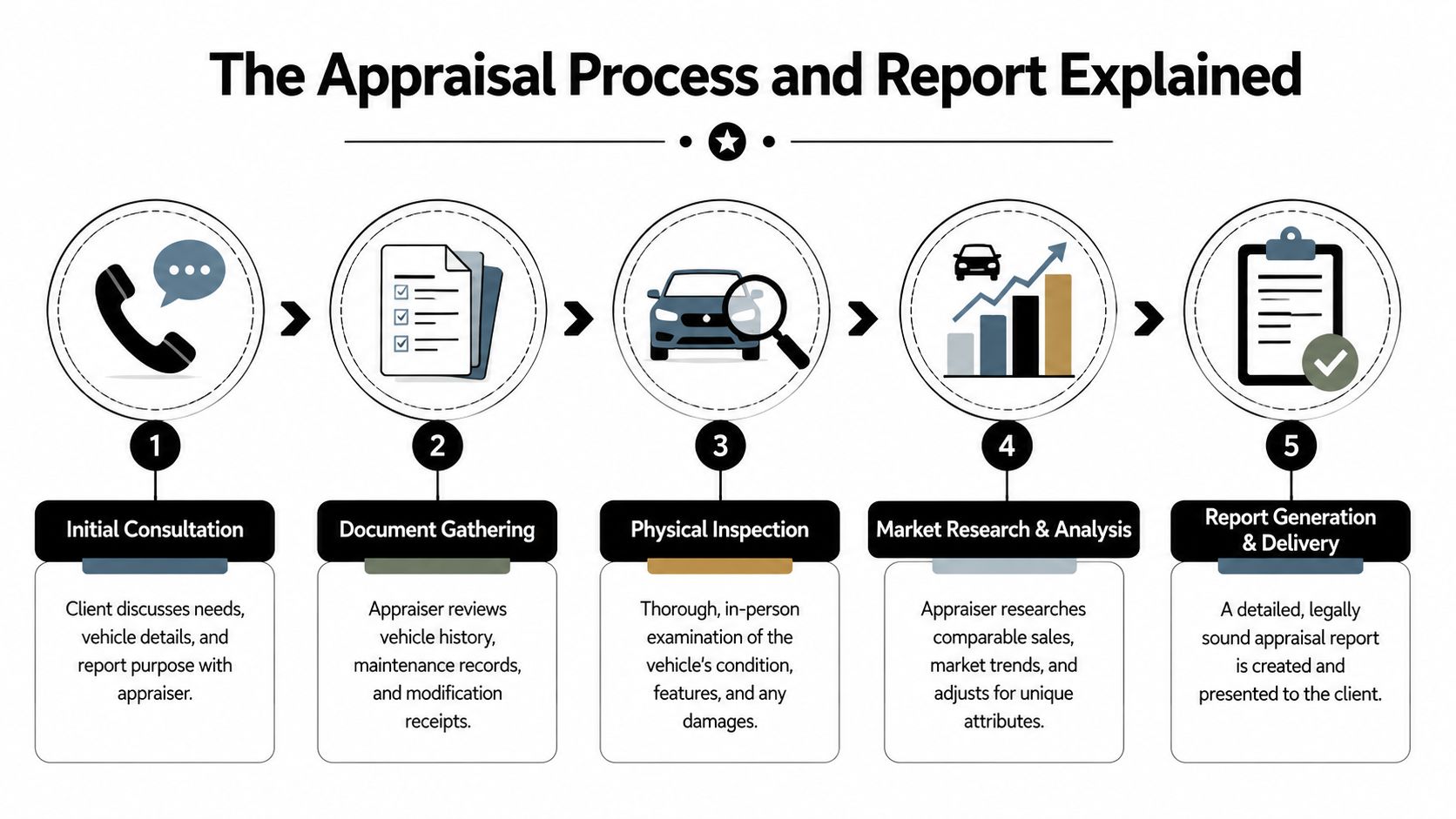

What usually happens first

The appraiser starts by figuring out the assignment. Are you dealing with a total loss, diminished value, pre-purchase dispute, estate issue, or something else? That purpose shapes the inspection, the research, and the report.

Then comes document gathering. Good appraisers ask for what matters: photos, VIN, mileage, condition details, prior repair records, maintenance records, option lists, and receipts for meaningful upgrades or restoration work.

If your policy dispute may turn into a formal valuation fight, it also helps to understand how the insurance appraisal clause process works before the report is finished. That way, the appraisal can be prepared with the likely next step in mind.

Inspection and market analysis

The inspection may be physical or, in some assignments, supported by records and images. Either way, the appraiser needs enough evidence to describe the vehicle accurately.

After that comes the hard part: market analysis. Market analysis distinguishes weak appraisers from strong ones. Anyone can pull listings. A competent appraiser evaluates whether a comparable is a valid comparison. Same model year isn't enough. Trim, drivetrain, mileage, accident history, condition, options, local availability, and buyer demand all matter.

Why the report carries weight

A certified auto appraiser's work is often constrained by jurisdictional rules and standardized methods. For example, some states require damage estimates to be based on visual inspection using new OEM parts only, with prices and labor calculations drawn from published, auditable manuals. That reduces subjectivity and creates a defensible paper trail, as shown in the Massachusetts motor vehicle damage appraiser training standards.

That's the point of a real appraisal report. It should be reviewable. Auditable. Explainable.

What a solid report should include

Look for these elements:

- Vehicle identification and purpose: VIN, year, make, model, mileage, and why the appraisal was prepared.

- Condition analysis: A clear description of pre-loss or post-repair condition, depending on the assignment.

- Comparable market support: Not just a list, but reasoning behind the comp selection.

- Methodology: The report should show how the value was developed.

- Supporting documentation: Photos, records, and calculations that can be followed by someone else.

If a report gives you a number without showing its work, it won't do much when the insurer pushes back.

A good report doesn't just help you understand your position. It helps another appraiser, an adjuster, an umpire, or a lawyer see that the valuation was built on evidence instead of wishful thinking.

How to Find and Vet a Reputable Appraiser

Your insurer says the car is worth less than it should be. You know the number is off, but now you have to decide whether paying an independent appraiser will put money back in your pocket.

That decision starts with one question. Is this a simple car with a straightforward market, or the kind of vehicle insurance software regularly misprices?

If the car is older but clean, low-mileage, modified, rare, high-trim, or has strong local demand, a generic valuation often misses the mark. That is when hiring an appraiser makes financial sense. You are paying for evidence the insurer does not already have.

Where to look first

Start with people who work around disputed values, not generic search listings. Search results are full of appraisers who may be fine for estate paperwork or dealer inventory but weak in an insurance fight.

Better sources usually include:

- Attorneys who handle property damage claims: They know which appraisers write reports that hold up under pushback.

- Collector, enthusiast, and marque-specific communities: These are especially useful for classics, specialty trims, and modified vehicles.

- Claim-focused valuation firms: Some providers concentrate on total loss, diminished value, or appraisal clause disputes. For example, car appraisal services from Total Loss Northwest focus on valuation disputes rather than general vehicle pricing.

- Professional associations and directories: Use them to build a list, not to make the final call.

A credential puts someone in the running. Their actual work gets them hired.

Questions that separate a real appraiser from a title collector

Ask blunt questions. A good appraiser will answer them without dancing around the issue.

- What kind of claims do you handle every week? Match their experience to your problem. Total loss is different from diminished value. Both are different from pre-purchase or classic car appraisals.

- How do you support your number? Listen for market comps, condition adjustments, documentation, and a report that explains the reasoning.

- Have you handled claims like mine in my area? Local market knowledge matters, especially when comparable vehicles are scarce.

- Can I review a sample report? Redacted is fine. You want to see whether the report is detailed enough to survive scrutiny.

- Do you have any ties to insurers, repair shops, or salvage buyers? Independence matters. Conflicts of interest weaken the report before the argument even starts.

- What happens after you deliver the report? Ask whether they will answer insurer objections, revise for factual errors, or participate if the dispute escalates.

One warning sign shows up fast. If the person leads with letters after their name and struggles to explain their method, keep looking.

Later in your search, this video can help you think more critically about the hiring process.

What it may cost

Fees vary by market, vehicle type, and claim complexity. Standard appraisals usually cost less than diminished value work or disputes that require follow-up with the insurer.

Get three answers before you hire anyone. What is the fee? What exactly is included? What support do you get if the insurer pushes back?

Do not hire on price alone. A cheap report that cannot defend its conclusion is just another document in the claim file.

That matters even more when the dispute is part of a larger financial loss after a Texas car accident. In that situation, the appraisal is not paperwork. It is part of your recovery strategy.

Ask for the fee, the scope, and the post-report support in writing.

You are buying judgment, documentation, and someone who can explain the number under pressure.

Putting Your Appraisal Report to Work

Once the report is done, don't just email it to the adjuster with a vague note and hope for the best. Use it deliberately.

The first move is simple. Submit the report formally and ask the insurer to reconsider the valuation based on the evidence. Keep your message short. Attach the report. Ask for a written response.

After that, the path depends on your policy and your state, but many drivers have a second tool available: the appraisal clause. If your policy includes one, that clause can force a more structured valuation dispute process instead of endless back-and-forth with the adjuster.

For drivers trying to understand the number they should be fighting for, a fair place to start is this guide on how to calculate fair market value. It helps frame the issue before you escalate.

What the appraisal clause changes

In plain English, the clause can shift the fight from “the insurer says no” to “each side hires an appraiser and the dispute moves into a formal process.” If the two appraisers can't agree, an umpire may be brought in to break the tie.

That matters because it takes the claim out of pure adjuster discretion.

For many people, this is also when they realize the money at stake isn't just about replacing a car. It's about the broader financial loss after a Texas car accident, including the way accident history can affect value even after repairs.

Use the report as leverage, not decoration

A proper report should help you do one or more of these:

- Challenge weak comparables

- Support a higher total loss value

- Document diminished value after repairs

- Trigger the next step under your policy

This screenshot gives you a sense of the kind of claim-focused service environment drivers often look for when they need valuation help.

If you're overwhelmed, that's normal. Most drivers have never had to turn a valuation report into a claim strategy. The point is not to argue louder. The point is to use the report to force a better process.

Frequently Asked Questions About Auto Appraisals

Will hiring an appraiser raise my insurance rates

An appraisal itself doesn't function like a moving violation or an at-fault loss. You're hiring a professional to assess value and support your side of a property damage dispute. That's not the same thing as creating a new claim.

Your rate questions usually depend more on the underlying accident history and policy details than on whether you challenged a low valuation.

Can a certified auto appraiser help with things besides insurance claims

Yes. Appraisers are also used in legal disputes, resale situations, estates, donations, and other valuation contexts. The important part is hiring someone whose background matches your purpose.

That said, don't assume an appraiser who handles estate or IRS-related work is automatically the right person for a total loss or diminished value fight. Match the expert to the assignment.

What if the insurer ignores my appraisal report

That happens. Don't panic.

Start by asking for a written explanation of what they disagree with. If they reject your comparables, ask why. If they claim your report uses the wrong method, make them say specifically what method they think should apply. Vague pushback is common. Specific pushback is easier to answer.

A report has real value when it forces the insurer to explain its own number in detail.

If your policy gives you an appraisal clause, this is often the point where that option becomes worth serious attention.

Is an appraisal worth it for an ordinary car

Sometimes no. If the vehicle is common, local market data is plentiful, and the insurer's value is in line with real replacement options, paying for an appraisal may not make financial sense.

It becomes more attractive when the car is unusually valuable, unusually clean, difficult to compare, or clearly undervalued by the carrier.

How fast can this process move

It depends on the appraiser, the claim type, and how organized your records are. If you have the title, photos, mileage, maintenance records, and insurer valuation in hand, things move much faster than if everyone is chasing missing documents.

What's the biggest mistake drivers make

They accept the first number because they're tired.

That's understandable. It's also expensive. If your gut says the valuation doesn't reflect your vehicle, stop and test that instinct with evidence before you sign anything.

If the insurance company is lowballing your total loss or diminished value claim, Total Loss Northwest is one option for drivers who need certified independent auto appraisals and help with appraisal clause disputes. If you're stuck between the insurer's number and what your vehicle is worth, getting a professional valuation is often the cleanest way to level the field.