You open the claim letter, look at the settlement number, and your first reaction is disbelief. The insurer is treating your classic like a used commuter car with a VIN and four tires. That's the moment most owners realize they're not arguing about damage alone. They're arguing about history, originality, documentation, and a market the average adjuster doesn't work in every day.

A classic auto appraiser exists for exactly this gap. When a collector car is totaled, underpaid, or diminished after a loss, the issue usually isn't whether the vehicle had value. The issue is whether anyone on the insurer's side measured that value the right way.

If you own a vintage Mustang, a numbers-matching Mopar, a carefully restored Porsche, or a survivor car with unusual provenance, you need more than a generic estimate. You need a defensible valuation and, in Oregon and Washington, you also need to understand one of the most overlooked rights in your policy: the Appraisal Clause.

Why Your Insurer's Valuation Is Just a Starting Point

You get the total loss number, compare it to the car in your garage, and the gap is obvious. The carrier valued a collector vehicle with a process built for ordinary transportation.

That does not automatically mean bad faith. It usually means the valuation method was too broad for the car in front of them.

Insurance companies handle claims at scale. Their systems are built around recent sales, standard trim levels, and vehicles that trade often enough to create clean data. Classic cars are different. A numbers-matching drivetrain, a documented restoration, factory color changes, rare options, provenance, and regional collector demand can change value in a way generic software does not capture well.

Why classics get undervalued

The first problem is usually the comp set. A late-model pickup can be compared against dozens of local sales. A 1967 fastback, a split-window Corvette, or a well-kept survivor Mercedes may need sales from specialty dealers, enthusiast auctions, marque-specific listings, and private transactions that never show up in ordinary retail databases.

Condition is another place where claims go sideways. In the collector market, condition grades are not casual opinions. They are part of the valuation framework. Hagerty explains the hobby's 1 through 4 condition scale and how those categories affect value in its car valuation methodology. If the insurer treated your car as an average driver when the market would recognize it as a stronger example, the valuation starts low and stays low.

Then there is verification. The National Automobile Dealers Association's classic and collectible guidance notes that value turns on facts such as authenticity, rarity, provenance, condition, and equipment, not just year, make, and model, in its classic car valuation overview. If no one confirmed tags, driveline numbers, options, restoration records, or prior judging history, the file may be missing the very facts that separate your car from a cheaper example.

What the insurer's number actually is

A settlement offer is the carrier's current position based on the information in its file.

That matters because many owners assume there are only two choices. Accept the number or hire a lawyer. In Oregon and Washington, there is often a more practical first step. Build a better valuation record, then press the claim with evidence. If the carrier still refuses to move, the Appraisal Clause may give you a contract-based path to challenge the amount of loss without filing suit first.

That clause is underused in classic car claims. It should not be. On the right file, it shifts the dispute away from opinion and toward documented market evidence.

Practical rule: If the insurer did not account for originality, documented work, correct options, provenance, or the real collector market for your model, treat the offer as an opening number.

What helps your position

What works

- Questioning the comparable sales: Ask for the exact vehicles used, where they sold, and whether those cars match your car's condition, equipment, and originality.

- Documenting what makes your car different: Restoration invoices, photos, ownership history, judging sheets, build documentation, and prior appraisals give the claim file facts the software did not have.

- Using a qualified independent appraiser: A proper appraisal puts enthusiast details into a format insurers, umpires, attorneys, and courts can evaluate.

What weakens your position

- Arguing from attachment: Sentiment is real, but it does not establish market value.

- Relying on asking prices alone: List prices show ambition. Closed sales and well-supported market analysis carry more weight.

- Assuming the adjuster already knows the niche: Some do. Many handle collector claims only occasionally.

I tell owners this all the time. The insurer's first number may be the start of the process, but it is rarely the last word if the car was not evaluated on its actual merits.

What a Certified Classic Auto Appraiser Does for You

A carrier totals your classic, sends over a valuation, and the number feels light the moment you read it. The disagreement usually is not about whether the car had value. It is about whether anyone on the insurer's side understood the car well enough to measure that value correctly.

That is where a certified classic auto appraiser earns his fee.

The job is to inspect the vehicle, verify what it is, document its condition, trace the quality of any restoration work, and place it in the right collector market. Then the appraiser has to explain that conclusion in a report that can hold up under scrutiny from an adjuster, another appraiser, an umpire, or a judge.

The appraiser's job in the real world

An insurance adjuster handles claims for the carrier. An independent appraiser represents the owner's interest in the value question. That difference matters, especially with collector cars, where originality, provenance, options, and quality of workmanship can change the number in a serious way.

A qualified appraiser does more than inspect sheet metal and paint. The work often includes reviewing service and restoration records, checking tags and numbers, comparing the car to relevant sales, and separating broad price-guide chatter from the actual market for that model and condition level. Professional appraisals are also commonly used for insurance, financing, estate settlement, charitable donation, and other legal or tax matters, as recognized by the Internal Revenue Service appraisal guidance.

That same discipline becomes especially useful if you end up invoking the Appraisal Clause in Oregon or Washington. Once a claim moves into that process, unsupported opinion stops carrying much weight. Documentation does.

Where an appraiser adds real value

Owners often call after a total loss decision, but that is only one part of the work.

- Total loss claims: The appraiser develops a supported pre-loss value based on the actual car, not a generic database match.

- Diminished value claims: A repaired classic may still suffer a market penalty because accident history follows the car.

- Pre-purchase inspections: Buyers need an independent assessment of authenticity, condition, and prior repairs before funds change hands.

- Estate, divorce, and legal disputes: A written appraisal gives the parties something better than guesswork or family folklore.

I tell owners this plainly. A sound appraisal does not exist to confirm a hoped-for number. It exists to prove a defensible one.

Why certification matters

Collector vehicle appraisal is a specialty. General automotive experience helps, but it does not replace training in appraisal standards or deep familiarity with a specific segment of the hobby.

A credible appraiser should understand USPAP, know how to document market support, and have working knowledge of the vehicle type being valued. A split-window Corvette, an early Bronco, and a postwar pickup may all fall under the collector-car umbrella, but the market does not judge them by the same standards. The appraiser needs to know what buyers pay extra for, what they discount, and what details are merely nice to have.

That expertise gives you a practical advantage if the insurer stays dug in. In many Oregon and Washington disputes, the strongest path is not arguing louder. It is presenting a report solid enough to support an Appraisal Clause demand and strong enough to stand on its own if the file gets more formal.

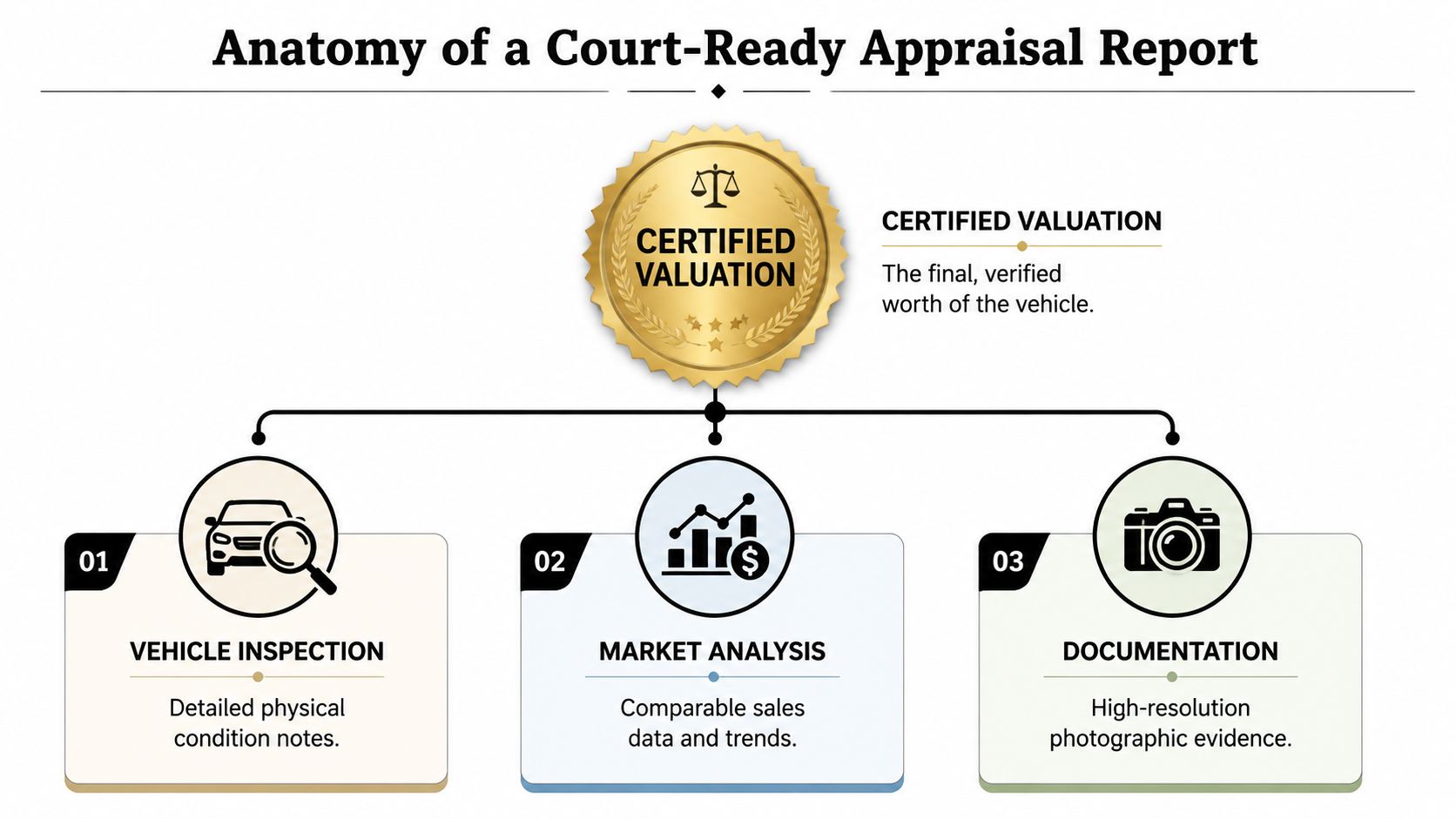

Anatomy of a Court-Ready Appraisal Report

After a loss, the carrier's adjuster may send over a number that looks tidy on paper and light on proof. If you plan to challenge it, especially through the Appraisal Clause in Oregon or Washington, your report has to do more than state an opinion. It has to show exactly how that opinion was reached.

A court-ready appraisal is built like evidence. An insurer, umpire, mediator, or attorney should be able to follow the file from vehicle identification to condition analysis to market support without guessing what the appraiser meant.

The identification section

Every solid report starts by proving what the car is.

That means the year, make, model, VIN, and body style, but it also means the identifiers that separate a genuine example from a tribute, clone, or incorrectly described car. Depending on the vehicle, that can include trim tags, fender tags, cowl tags, engine pad stampings, casting numbers, transmission codes, axle tags, and factory option data.

Those details affect value in real dollars. A matching-numbers drivetrain, a rare factory package, or a period-correct replacement engine can change the result materially. For unusual systems or low-production cars, technical background matters too. A reference point like this Chrysler Imperial EFI system overview can help explain why originality and proper component identification matter on cars that are often misunderstood.

The condition and photo record

Condition language has to be specific. “Nice car” is useless in a dispute. A proper report explains paint quality, panel fit, chrome, glass, interior materials, undercarriage condition, engine bay presentation, evidence of prior repairs, and whether the restoration was driver-grade, show-quality, or somewhere in between.

Photos carry a lot of weight because they let the reader verify the written analysis. A court-ready report should include:

- Identification images: VIN plates, trim tags, stampings, castings, and serial numbers

- Overall views: Front, rear, both sides, three-quarter angles, and roofline

- Condition details: Paint flaws, rust, chips, cracks, upholstery wear, trim damage, and underbody condition

- Mechanical and authenticity details: Engine bay, trunk, chassis, wheels, tires, and factory-specific components

- Document support: Restoration invoices, ownership history, judging sheets, and build records where available

A thin photo set is a warning sign. If the report only shows glossy exterior shots, it is not giving you much support when the carrier questions originality, condition, or prior damage.

The market analysis section

The market analysis is where weak reports usually fail. A credible appraiser identifies comparable sales, explains why those vehicles were selected, and adjusts for differences in condition, originality, provenance, equipment, and regional demand.

That process should track recognized appraisal practice. The Appraisal Foundation's Uniform Standards of Professional Appraisal Practice requires the appraiser to disclose the scope of work and support the conclusions reached. In plain English, the report has to show its math and judgment, not just announce a number.

For collector vehicles, that usually means weighing private-party sales, dealer offerings, major auction results, and current listing data with caution. Asking prices are not closed sales. Auction sales can run hot or soft depending on venue, timing, and bidder mix. If you want a broader explanation of how these inputs fit together, this guide on how to value a classic car accurately lays out the basics.

The certification and compliance page

The final pages matter more than owners often realize. The report should state the intended use, effective date of value, definition of value being applied, limiting conditions, scope of inspection, and the appraiser's certification.

That certification tells the reader the appraiser stands behind the work. It also matters if the claim turns into a formal Appraisal Clause dispute, because the other side will look for gaps in method, qualifications, or documentation.

A polished PDF is nice. A defensible report is what protects you. If the file can survive hard questions from an insurer and still hold together, it is doing its job.

How Appraisers Determine Your Classic Car's True Market Value

Your carrier says your car is worth one number. You know the car that burned, flooded, or got hit was better than the average example in their system. The gap usually comes from how the vehicle is identified, how its condition is judged, and which sales are treated as true comparables.

Authenticity sets the ceiling

An appraiser starts by confirming exactly what the car is. That sounds obvious until a claimed numbers-matching car turns out to have a service block, a replacement transmission, reproduction trim, or a later repaint in a non-original color.

For collector vehicles, small authenticity issues can move value sharply because buyers pay premiums for factory-correct drivetrains, rare option packages, and documented provenance. The National Highway Traffic Safety Administration explains the structure and purpose of the VIN standard, but a classic appraisal usually goes further than modern VIN decoding. It includes body tags, engine stampings, casting dates, trim codes, axle and transmission IDs, and period-correct equipment.

That matters most on specialty cars, low-production trims, and transitional models where originality is easy to overstate. A technical reference such as the Chrysler Imperial EFI system shows why an appraiser needs model-specific knowledge before assigning value.

Condition has to be graded in the right lane

A clean driver, a high-level restoration, and a well-preserved original car can all present well in photos. They do not trade at the same level.

I look at paint quality, bodywork, panel alignment, chrome, glass, interior materials, undercarriage condition, mechanical operation, and how consistent the whole car is. Fresh paint can help. It can also hide poor metal work. Older restoration work can hurt value, or it can support value if the workmanship held up and the car still presents honestly.

Documentation changes the analysis. Restoration invoices, photo records, ownership history, judging sheets, and service files help separate a car with a story from a car with proof. If you want a practical owner-side checklist before an insurance dispute, this guide on how to value a classic car accurately is a solid place to start.

Comparable sales only work if they are actually comparable

The hardest part of the assignment is often comp selection. Same year and same model is not enough.

A bench-seat small-block coupe is not a fair comp for a big-block four-speed car with factory air and documented provenance. Regional demand also matters. So does venue. A televised auction sale during a strong weekend can produce a very different result than a private-party transaction between informed buyers.

Good appraisal work adjusts for those differences instead of averaging them away. Asking prices get little weight unless they help show market direction. Closed sales matter more. Dealer offerings can help define the upper retail range if the car being appraised would reasonably compete in that setting.

This walkthrough adds useful visual context to how vehicle inspection and market analysis fit together:

The real number is the market you can defend

Owners often want credit for every dollar spent. The market rarely pays that way. Modifications may improve drivability and still reduce collector value. Rare equipment may increase value, or it may make the car harder to place if buyers do not want it.

For an insurance claim, the target is not a flattering number. It is a supportable fair market value based on the car you owned on the date that matters. If the insurer still clings to a thin valuation after that work is done, that is often the point where the Appraisal Clause becomes useful in Oregon and Washington.

How to Choose and Hire the Right Classic Auto Appraiser

Your insurer declares the car a total loss. The offer looks tidy on paper, but the number would not buy a comparable car in the current collector market. That is the moment to hire carefully, because the appraiser you choose may end up carrying your side of the value dispute under the policy's Appraisal Clause.

Treat the hire like you would treat a shop selection for a rare driveline rebuild. You want the person with the right lane, the right process, and work that holds up when someone starts asking hard questions.

Start with qualifications that matter

A qualified classic auto appraiser should be able to explain credentials without a sales pitch. Look for professional appraisal training, USPAP familiarity where applicable, and actual experience with collector vehicles, not just late-model daily drivers. The American Society of Appraisers outlines the kind of professional grounding serious appraisers are expected to have in its overview of appraisal discipline and ethics.

Then get specific about your car.

A solid appraiser for a numbers-matching muscle car may be the wrong fit for a vintage Porsche, a brass-era car, or a custom hot rod. Market knowledge is narrower than many owners realize, and honest appraisers will say so. Ask how often they appraise your make, era, and condition tier. Ask whether they work insurance total loss and diminished value files, not just estate planning or agreed value paperwork.

If you want a baseline for what a claim-focused service should cover, review this example of an independent car appraiser. Compare the scope of inspection, the documentation reviewed, and whether post-report support is part of the assignment.

Red flags that should end the call

An appraiser who quotes your target number before inspecting the car, records, and market evidence is selling reassurance, not analysis.

The same goes for contingency pricing tied to your settlement. That fee structure creates an obvious credibility problem if the report is challenged. Be cautious with vague talk about "industry databases" if the appraiser cannot explain how comparable sales are selected and adjusted. Be cautious if there is no sample report, no discussion of file documentation, and no willingness to defend the conclusion with facts.

Methodical beats flashy here.

Questions that separate a real appraiser from a list-maker

| Question Category | What to Ask | Why It Matters |

|---|---|---|

| Credentials | What appraisal training and professional affiliations do you hold? | Shows whether the appraiser follows recognized standards and ethics |

| Vehicle expertise | How many cars like mine have you appraised recently? | Collector values depend heavily on segment-specific market knowledge |

| Report standards | Is the report prepared to stand up in a claim dispute or legal setting? | A usable report needs more than a value conclusion |

| Claim experience | Have you handled total loss or diminished value cases involving classics? | Insurance work requires claim-specific documentation and communication |

| Inspection process | What identifiers, stampings, options, and records do you verify? | Confirms whether the appraiser checks originality, provenance, and condition carefully |

| Comparable sales | How do you choose comps and adjust for differences? | This reveals whether the value opinion is reasoned or just assembled from listings |

| Deliverable | Can I review a sample report? | Lets you judge depth, photos, sources, and clarity before hiring |

| Fees | Do you charge a flat fee, hourly rate, or something else? | Clear pricing helps you compare services and avoid conflicts |

| Follow-through | Will you discuss the report with the insurer if the value is challenged? | Some claims stall because the appraiser disappears after delivery |

Hire for defensibility, not comfort

Owners under claim pressure often want someone who sounds confident. Confidence helps, but discipline wins. The right appraiser inspects carefully, documents thoroughly, and explains the market in plain language. That is the kind of report that can support you if the insurer's number stays low and you decide to invoke the Appraisal Clause in Oregon or Washington.

Choose the person whose process you can trust under scrutiny. In a disputed classic car claim, that is the appraiser who usually does the most good.

Using the Appraisal Clause in Oregon and Washington

Your insurer declares your classic a total loss, sends a valuation that leans on ordinary used-car data, and expects a quick signature. That is the moment many owners in Oregon and Washington realize the actual dispute is not coverage. It is value.

Most policies contain an Appraisal Clause for exactly that kind of fight. If the carrier agrees the loss is covered but assigns a number that does not reflect the collector market, the clause gives both sides a defined method to resolve the valuation dispute. For classic car owners, that matters. Generic valuation systems often miss provenance, documented restoration work, rare options, and regional demand.

Why this clause matters so much

The Appraisal Clause is one of the most underused rights in a classic car policy. Owners often spend weeks arguing with an adjuster, sending more photos, and rebutting weak comparables one by one. That rarely changes the process. Invoking the clause changes the process.

That distinction matters in Oregon and Washington, where collector cars range from restored muscle and vintage pickups to air-cooled European cars and Japanese classics with fast-changing market demand. A software valuation may treat your car like basic transportation. An appraisal clause dispute forces the file into a valuation process where condition, originality, documentation, and true comparables carry more weight.

If you want a practical explanation of how that process works, review this guide to the insurance appraisal clause.

How the process usually unfolds

A common claim goes like this. The carrier issues a total loss offer. The owner reviews the comparables and sees obvious problems: wrong trim level, poorer condition adjustments, missing options, or sales that do not reflect the collector market. The owner objects, but the insurer keeps returning to the same valuation platform and the same number range.

At that point, the policy language matters. If the disagreement is about value, the owner can usually invoke the Appraisal Clause in writing. Each side selects an appraiser. If those appraisers cannot agree on value, they submit the dispute to an umpire. The result usually carries far more weight than another round of internal adjuster review.

This is why I tell owners not to confuse delay with progress. Repeating your position five times is not the same as moving the claim into a procedure the policy already provides.

How to use the clause without weakening your position

A good invocation is focused and documented.

- Read the exact policy language: Confirm that the dispute is about the amount of loss or value, not a separate coverage denial.

- Send written notice: State clearly that you are invoking the appraisal provision in the policy. Keep a copy and document delivery.

- Define the disagreement precisely: Identify where the insurer's valuation fails, such as incorrect comparables, missed options, unsupported condition adjustments, or disregard for collector-market evidence.

- Choose an appraiser who can function in a claim dispute: Classic car knowledge is only part of the job. The appraiser also needs to document the file in a way the opposing appraiser, umpire, or attorney can follow.

- Organize your evidence early: Prior appraisals, restoration invoices, ownership history, photos before the loss, awards, and provenance can all affect the value conclusion.

What helps, and what slows the claim down

The owners who get the best use from the clause usually act once the dispute is clear. They stop treating the claim like an endless negotiation and start treating it like a valuation case that needs proof.

What slows things down is hesitation, vague complaints, and hiring someone who knows collector cars but cannot support a number under scrutiny. I have seen owners with strong cars lose their advantage because they waited too long to invoke the clause or submitted a thin appraisal that could not answer obvious questions. In Oregon and Washington, the Appraisal Clause is not a technical footnote. It is often the cleanest path to a fairer number when the insurer's valuation starts in the wrong place.

Frequently Asked Questions About Classic Car Appraisals

How should I prepare my car before the appraisal?

Start with access and documentation. The appraiser needs to see the car clearly, including flaws, tags, trim, engine numbers if available, and the quality of any repair or restoration work.

Wash the car and empty out loose items, but do not try to hide defects. Have the title, registration, invoices, service records, restoration photos, prior appraisals, and any provenance ready. If the appraisal is tied to an insurance dispute, include photos from before the loss and the insurer's valuation paperwork so the differences can be examined point by point.

What does a classic car appraisal usually cost?

Fees vary with the assignment. A simple insurance value update on a local, well-documented car usually costs less than a claim report involving disputed condition, rare options, travel, or court-ready support.

Ask what you are buying. Some owners only need a market value opinion for coverage planning. Others need a report that can hold up in an Appraisal Clause dispute in Oregon or Washington, where the appraiser may need to defend comparable sales, condition adjustments, and documentation under pressure. The cheapest fee often buys the thinnest report.

What's the difference between total loss and diminished value?

A total loss appraisal answers one question. What was the vehicle worth immediately before the damage occurred?

A diminished value appraisal answers a different one. How much value did the vehicle lose after repair because the market now sees it as a damaged-and-repaired car. On collector vehicles, that stigma can matter even when the repair work is competent, especially on cars with known history, high-level restorations, or strong originality.

Do modifications always increase value?

No. The market pays for modifications it respects, understands, and can verify.

A period-correct performance build with receipts, quality workmanship, and buyer appeal may help value. A poorly documented engine swap, custom interior, or one-off fabrication can narrow the buyer pool and pull value down. The issue is not whether money was spent. The issue is whether the collector market treats that work as an asset.

How are EV-converted classics handled?

EV conversions are harder to value because they sit outside the normal original-versus-restored framework. Some buyers want the usability and engineering. Others discount the car because it no longer fits traditional collector expectations.

That means documentation carries even more weight. Keep the conversion invoice, parts list, battery and motor specifications, installer information, build photos, and any engineering or safety documentation. In a claim, insurers sometimes default to a generic modification adjustment that misses the actual market reaction. If that happens, the dispute needs evidence, not opinions.

If you're dealing with a low total loss offer, a diminished value dispute, or a classic car claim that doesn't reflect what your vehicle is worth, Total Loss Northwest can help you push back with an independent, certified appraisal. They focus on Oregon and Washington claims, including Appraisal Clause disputes, and they also provide diminished value support nationwide.