After a wreck, the last thing you want is the insurance company offering you pennies on the dollar for your classic car. Unfortunately, it happens all the time. This isn't just a string of bad luck; it's how the system is designed. Standard valuation tools are built for your daily driver, not for a unique piece of automotive history.

This is where a certified independent appraiser becomes your most important ally.

Why Insurance Offers on Classic Cars Fall Short

You’ve poured years of your life and a small fortune into restoring your 1969 Camaro. Then, after an accident, the insurance company's software spits out a number that treats it like any other old, used car. It’s a gut-wrenching, all-too-common scenario for anyone who owns a classic, custom, or restomod vehicle.

The problem is simple: the tools insurers lean on, like KBB or NADA, just don't get what makes a classic car special. They're programmed to see depreciation, but well-maintained classics often appreciate in value. They have no way to factor in rarity, the quality of a restoration, historical importance, or specific modifications. The result? A lowball offer based on completely irrelevant data.

The Flaw in Standard Valuations

Insurance adjusters are often overworked and rely on automated systems built for volume and speed, not for accuracy on one-of-a-kind assets. Your car’s unique story—the numbers-matching engine, the period-correct paint job, the thousands of dollars in receipts—is completely invisible to their software. This creates a huge gap between the insurer’s offer and your car's real-world market value.

This is exactly why professional classic auto appraisers are so crucial. They step in as your expert advocate, armed with deep market knowledge and data from the actual collector car world. They don't just see an old car; they see an investment with a documented history and value.

The stakes have never been higher. The global classic car market is exploding and is projected to reach an incredible $77.8 billion by 2032. This kind of growth makes it clear why a generic, computer-generated number is completely unacceptable when you’re fighting for a fair settlement.

Your Right to a Fair Valuation

The good news is that your auto policy likely contains a powerful but little-known tool: the Appraisal Clause. Invoking this clause is your right, and it allows you to hire your own independent appraiser to formally challenge the insurance company’s figure. It forces them to abandon their flawed algorithms and deal with a valuation based on actual evidence.

By invoking your policy's Appraisal Clause, you completely shift the power dynamic. The negotiation is no longer dictated by the insurer's software; it's grounded in the documented, market-based reality presented by your expert appraiser.

For owners of high-value assets, it's also worth looking into specialized coverage like private client insurance, which is specifically designed to handle the complexities that standard policies ignore. Protecting your investment starts with the right coverage, and you can learn more about the specific classic car insurance requirements in our detailed guide here: https://totallossnw.com/classic-car-insurance-requirements/

How We Decode the True Value of a Classic Car

Figuring out what a classic car is really worth isn't like looking up a price in a book. It’s more like an art historian authenticating a masterpiece. A professional appraiser has to dig deep, peeling back the layers of a car's history, its current condition, and what the market is doing right now to land on a true, defensible number.

This isn't about pulling a figure out of thin air; it’s a methodical process that relies on established valuation techniques. In fact, a seasoned appraiser never hangs their hat on a single method. They blend data from several approaches to build a complete, unshakeable picture of the vehicle’s value. Think of it like a detective building a case—the more evidence you gather from different sources, the stronger your final conclusion.

The Market and Comparable Value Approach

The cornerstone of almost every appraisal is the Market Value approach. This method answers one simple question: what would a willing buyer realistically pay a willing seller for this car in today's market? To get this right, an appraiser has to act like a stock market analyst for classic cars, constantly tracking auction results, private sales, and the subtle shifts in demand for specific makes and models.

Tied directly to this is the Comparable Value method. This is where the real legwork comes in. The appraiser hunts down recently sold vehicles that are as close a match as possible to your car. We're talking about much more than just the same year and model. A true expert finds "comps" with similar mileage, condition ratings (from a flawless #1 concours car to a #4 daily driver), factory options, and even desirable color combinations.

The best evidence comes from a few key places:

- Public Auctions: Results from big names like Barrett-Jackson or Mecum are gold because they provide transparent, verifiable sales data.

- Private Sales: Good appraisers have networks and access to private databases that track sales the public never sees.

- Dealer Listings: While asking prices from specialty dealers are a useful data point, the final sale price is what truly matters.

This intensive research ensures the final number isn't just an estimate, but a value grounded in what real people are paying for similar cars, right now. To go a level deeper, a crucial part of this process is understanding the provenance value of classic cars—the car's unique story.

A car’s story—its documented ownership history, a past racing career, or unique factory paperwork—can add a staggering amount of value that a simple lookup would miss. A great appraiser knows how to quantify that narrative and translate it into a dollar figure.

The Cost of Restoration Method

For restored, restomod, or highly customized vehicles, the Cost of Restoration approach is another essential tool in our belt. Think of this method as a detailed financial audit of the car’s journey to its current state. It isn't about what the parts cost back in the day, but what it would cost today to replicate that same level of quality and craftsmanship.

This requires the appraiser to document and value every single component and every hour of expert labor invested in the build. It’s like adding up the receipts for a bespoke suit—it captures the true cost of creating that specific, high-quality final product.

We have to consider things like:

- Labor Costs: What are the current rates for a master painter, a specialized engine builder, or a concours-level upholsterer?

- Parts Sourcing: Were rare New Old Stock (NOS) parts hunted down, or were high-quality modern reproductions used?

- Quality of Work: The value difference between a garage restoration and a professional, frame-off build by a nationally recognized shop is absolutely massive.

Let's break down how these different valuation methods stack up against one another.

Classic Car Appraisal Methods Explained

A breakdown of the primary valuation methods used by certified classic auto appraisers to determine a vehicle's true worth.

| Appraisal Method | What It Measures | Best For |

|---|---|---|

| Market Value | The current price a vehicle would sell for between a willing buyer and seller. | All types of classic cars, establishing a baseline value. |

| Comparable Value | The sale prices of nearly identical vehicles sold recently. | Vehicles with a good number of recent sales to compare against. |

| Cost of Restoration | The total cost to replicate the vehicle's current condition (parts + labor). | Restored, modified, or custom-built cars where the investment is high. |

| Concours Condition | A rating (#1-6) based on the vehicle’s quality relative to a perfect, factory-new example. | Show cars and high-end collectibles where originality and perfection are key. |

Each method provides a different piece of the puzzle. By combining these approaches, a professional classic auto appraiser builds a comprehensive, rock-solid case for your car’s actual worth. This multi-faceted strategy is exactly what you need to counter an insurance company's often simplistic, lowball valuation. If you want to see how we put this into practice, you can find a breakdown of our own expert vehicle appraisal services on our site.

How Appraisals Maximize Your Insurance Payout

This is where the rubber meets the road—the point where a meticulously researched valuation turns from a stack of paper into a check in your hand. A professional appraisal isn't just another document; it’s the leverage you need to get a fair payout from the insurance company. It directly impacts the two most gut-wrenching scenarios a classic car owner can face: Diminished Value and a Total Loss.

In both situations, an appraisal acts as your expert witness. It transforms the conversation from your word against theirs into a data-driven argument that’s incredibly hard for them to ignore. Essentially, it systematically takes their lowball offer apart and rebuilds it based on what’s actually happening in the real-world market.

The Fight for Diminished Value

Think of your classic car like a rare piece of art. If it gets a hairline crack and is flawlessly repaired by a master restorer, it might look perfect, but it will never be worth the same as an identical, undamaged piece. That permanent drop in value is called Diminished Value.

Even with the best repairs money can buy, an accident history attaches a permanent stigma to your vehicle. A knowledgeable buyer simply won't pay top dollar for it anymore. And you can bet the insurance company will almost never volunteer to pay for this loss.

This is exactly why you need a certified classic auto appraiser. They don't just guess; they create a detailed report that quantifies this specific loss in market value. Here's what they'll do:

- Document the vehicle's pre-accident condition and establish its value based on all its unique qualities.

- Analyze the severity of the damage and the extent of the repairs performed.

- Provide concrete market evidence showing how similar cars with accident histories sell for less than their untouched counterparts.

Without this expert analysis, you're leaving thousands of dollars on the table that you are rightfully owed. An appraisal is the tool that proves this loss isn't just a feeling—it's a real, measurable financial hit.

Winning the Total Loss Battle

When an insurance company declares your classic car a total loss, their first offer is almost always a lowball figure spit out by the same flawed software that can't properly value classics in the first place. They are counting on you to be too tired or intimidated to fight back. A professional appraisal is your most powerful counter-punch.

Your appraiser’s report becomes the definitive argument for your car's true Actual Cash Value (ACV). It will present a mountain of evidence—comparable sales, restoration costs, unique features, and provenance—to prove their number is wrong and yours is right.

An independent appraisal isn't just another opinion. It's a meticulously researched, evidence-based argument that forces the insurance company to either justify its low valuation or accept yours. It completely flips the power dynamic of the negotiation in your favor.

The global collector car market is massive. According to Hagerty, there are 43 million collector cars holding a combined $1 trillion in insurable value. In such a high-stakes environment, insurers rely on generic algorithms that often miss the mark, leading to unfair settlements. A classic auto appraiser cuts through the noise, using hard data from recent auctions and sales to build a true, defensible value for your car. You can explore more of the data driving the market with Hagerty's market insights.

Invoking the Appraisal Clause

So, what happens when the insurance company digs in its heels, even after seeing your detailed appraisal? Most auto policies in Oregon, Washington, and across the U.S. contain a contractual right you probably don't know you have: the Appraisal Clause.

This powerful but often overlooked clause gives you the right to force a binding, independent valuation process.

Here’s how it typically unfolds:

- You hire your appraiser, and the insurance company hires theirs.

- The two appraisers get together to negotiate and try to agree on a value for your vehicle.

- If they can’t reach an agreement, they jointly select a neutral third-party expert, known as an umpire.

- A final value agreed upon by any two of the three parties (your appraiser, their appraiser, or the umpire) becomes legally binding.

Invoking this clause effectively takes the insurance adjuster out of the equation and puts the final decision in the hands of qualified, unbiased experts. It is the ultimate tool for ensuring you get a fair settlement based on your classic car’s actual market worth, not a computer's best guess.

Choosing a Certified Classic Auto Appraiser

When your classic car is on the line, the last thing you want is a generic appraiser. You wouldn't ask your family doctor to perform heart surgery, right? By that same token, you shouldn't trust a standard collision appraiser—someone who spends their days looking at late-model sedans—with your unique automotive investment. The classic car world plays by a completely different set of rules, and you need a specialist who lives and breathes that market.

Finding the right expert means looking past a simple business card. You’re not just hiring an appraiser; you're hiring an advocate. You need someone who truly understands the nuances of restoration quality, provenance, and rarity—factors that are often completely lost on standard insurance adjusters.

Credentials That Actually Matter

When you're vetting potential classic auto appraisers, their background and certifications tell you a lot. While credentials from organizations like the Inter-Industry Conference on Auto Collision Repair (I-CAR) or the National Institute for Automotive Service Excellence (ASE) are great for modern collision work, they say nothing about a person's expertise in classic cars.

You need someone whose experience is planted firmly in the collector car world. Look for an appraiser who is an active member of classic car clubs, regularly attends major auctions like Barrett-Jackson or RM Sotheby's, and can talk fluently about the historical details of your car’s make and model. This is the kind of niche knowledge that turns a generic valuation into a meticulously defended appraisal.

An appraiser’s real worth isn't just in their certifications. It's in their ability to build a compelling, evidence-based story about your vehicle's value. Think of them as part historian, part market analyst—not just a damage estimator.

Key Questions to Ask a Potential Appraiser

Before you hire anyone, you need to interview them. Think of it like hiring a lawyer for your car, because in a very real financial sense, that's what you're doing. Their answers to a few key questions will tell you everything you need to know about whether they have the specialized skills to handle your case.

Here’s a quick checklist of must-ask questions for any classic auto appraiser you’re considering:

- Can you show me successful reports for vehicles similar to mine? This proves they have direct, relevant experience and aren't just learning on your dime.

- What specific sources do you use for comparable sales data? A vague answer is a major red flag. They should be able to name specific auction houses, private sale databases, and specialty dealer networks without hesitation.

- How do you challenge an insurance company's low valuation? A confident, experienced appraiser will have a clear process for picking apart an insurer's weak report and building a strong counter-argument.

- Are you an independent appraiser? This is critical. You need to be sure they work for you, not for the insurance companies. A truly independent appraiser has no conflict of interest and is 100% focused on protecting your financial stake.

The classic car market is a powerful economic engine, with annual transactions growing at an average of 10% per year since 2000. This makes precise, unbiased valuations more critical than ever, especially when protecting owners from insurance company lowball tactics. With collector cars averaging 4.6% annual returns between 2018 and 2023, a professional appraisal ensures that a single accident doesn't wipe out your investment's potential. You can find more current trends in the classic car market to see just how much is at stake.

Ultimately, choosing the right professional is the single most important step you can take to get the settlement you truly deserve.

The Anatomy of an Appraisal Report That Wins

What's the real difference between an appraisal that an insurance company dismisses and one that forces them to write a proper check? It’s not just the final number. It's the mountain of solid, undeniable evidence backing that number up. A winning appraisal report is essentially a legal argument, built piece by piece to be so logical and thorough that it leaves the insurer no wiggle room.

Think of it this way: the insurer's typical one-page valuation printout is like a flimsy tent in a storm. A professional appraisal report, on the other hand, is a brick house. It’s built on a foundation of hard data, detailed observations, and expert analysis, with each section reinforcing the others. The result is a structure that can easily withstand the high-pressure tactics of an insurance negotiation.

Beyond a Simple Photo Gallery

High-quality photography is the starting point, but we're talking about much more than a few quick snapshots. A truly compelling report includes dozens of high-resolution images that document the vehicle from every possible angle. The goal isn't just to show the car's general condition; it's to create a complete visual record of its value.

This means getting detailed shots of things like:

- Unique Features: Close-ups of rare factory options, the specific color codes on the VIN tag, or any period-correct modifications that add value.

- Quality of Workmanship: Macro shots that show the depth and quality of the paint, the precision of the panel gaps, or the fine stitching in the upholstery.

- Undercarriage and Mechanicals: A spotless engine bay, clear photos of numbers-matching engine block stamps, and a documented rust-free frame are all huge value points that must be captured visually.

- Flaws and Imperfections: A credible report has to be an honest one. By documenting minor wear and tear, the appraiser proves the inspection was meticulous, which builds trust in the overall assessment.

This kind of detailed photographic evidence tells a story that words alone can't, proving the vehicle’s condition is precisely as described.

The Power of Verified Comparables

This is the absolute heart of any strong appraisal. A list of verified comparable sales—or "comps"—is the definitive proof of your vehicle's real-world market value. A top-tier classic auto appraiser doesn't just do a quick online search; they meticulously curate a list of actual, recently sold vehicles that are as close to a mirror image of yours as possible.

These aren't just random online listings. They are carefully chosen sales from reputable sources, like major auction houses and verified private transactions. Each comparable vehicle is then adjusted—value is added or subtracted for differences in mileage, condition, options, or ownership history—to zero in on a precise, data-backed valuation for your specific car. This methodical process systematically picks apart an insurer's lowball offer, which is usually based on generic book values.

An insurer's report often pulls vague, irrelevant "comparables" from different parts of the country or for cars in vastly different condition. A winning appraisal presents a tight, localized, and highly relevant set of comps that establishes an undeniable benchmark for your vehicle's true worth.

The Valuation Reasoning: A Compelling Narrative

The final, and most critical, element is the Valuation Reasoning. This is where the appraiser connects all the evidence into a clear and persuasive narrative. Think of it as the closing argument, explaining why your vehicle is worth the value being claimed.

This section logically connects the dots for anyone reading the report, from the insurance adjuster to a third-party umpire. It lays out how the vehicle’s specific history, its documented condition, its rare features, and the comparable sales data all lead to one inescapable conclusion about its value. It puts the flimsy, algorithm-based logic of the insurer side-by-side with a robust, evidence-based assessment. This clarity and logical flow turn the report from just a document into a powerful negotiation tool built to win.

Your Step-By-Step Guide for Oregon and Washington Claims

Navigating an insurance claim in the Pacific Northwest can feel like a maze, but a clear game plan is your best defense against a lowball offer. Right after an accident, your instinct is to document everything—and that's a great start. But it's the steps you take in the following days that truly shape the financial outcome for your classic car.

Think of the insurance company's first offer as exactly what it is: an opening bid. It's almost never their final number. Your job is to come to the table prepared with your own hard evidence, starting with a professional appraisal from a firm that knows the Oregon and Washington markets inside and out.

The Initial Steps After an Accident

What you do immediately after an accident sets the tone for the entire claim. It’s all about controlling the narrative from the get-go.

Notify Your Insurer Promptly: Get the accident on record as soon as you can, but stick to the basic facts. Don't admit fault or guess about what happened. Just let them know an accident occurred and that you’ll be sending more information.

Decline Recorded Statements: You are not legally required to give a recorded statement to the other driver's insurance company. You can politely decline, stating that you'll communicate through your representative or provide details in writing. This is a crucial step to prevent your words from being twisted later on.

Get a Professional Appraisal: This is a big one. Before the insurer's lowball offer even hits your inbox, get a certified classic auto appraiser on your side. Walking into a negotiation with an expert valuation already in hand gives you immediate leverage and signals that you're serious about protecting your car's true value.

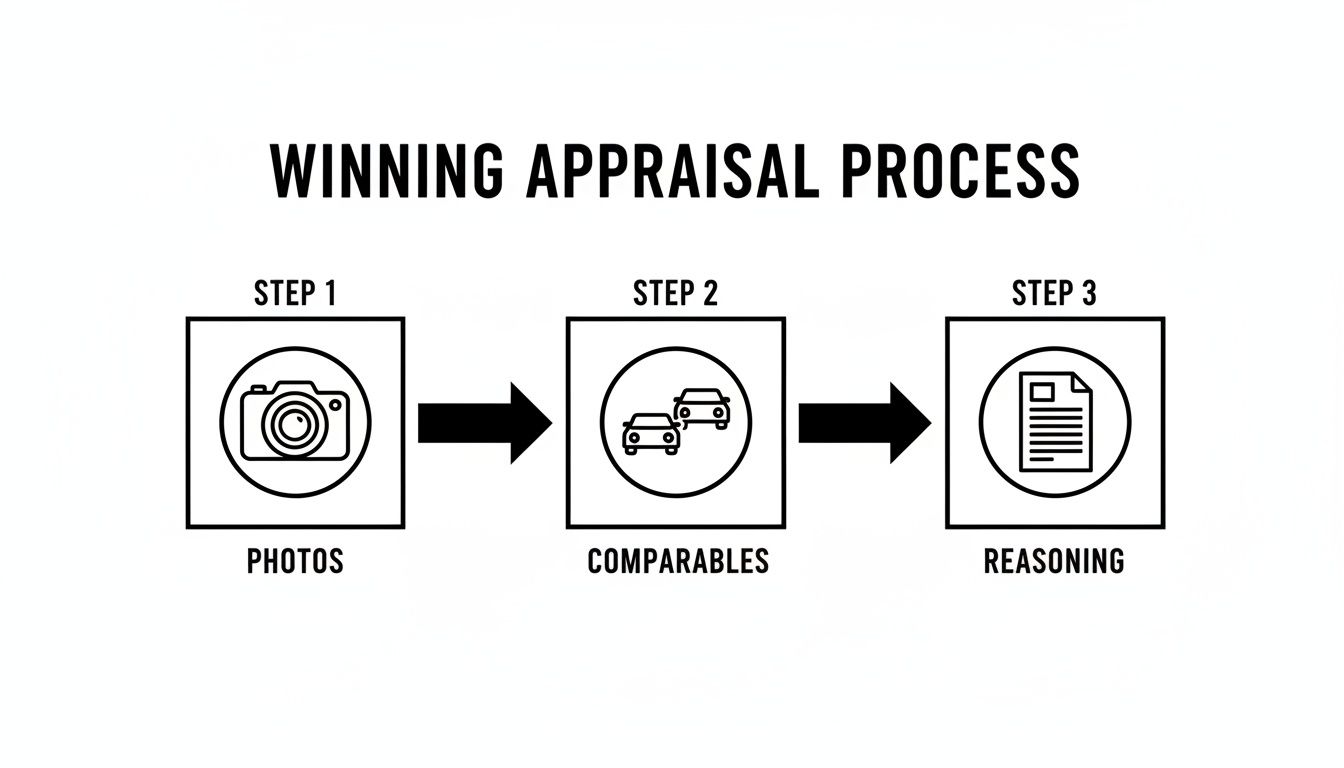

This is what a winning appraisal process looks like—it’s a simple but powerful formula built on solid evidence.

As you can see, a strong appraisal isn't just a number. It's a cohesive argument built on visual proof, real market data, and the clear, logical explanation that connects all the dots.

Invoking the Appraisal Clause in OR and WA

So, what happens when the insurance company just won't budge? It’s time to play your trump card: the Appraisal Clause. This is a contractual right baked into your policy in both Oregon and Washington that forces the issue into a binding, independent valuation process.

Invoking the clause is a formal move. You need to inform the insurer in writing that you are officially disputing their valuation and hiring your own independent appraiser. This single action kicks their biased, computer-generated number to the curb and puts the final decision in the hands of qualified experts.

Invoking the Appraisal Clause isn’t an act of aggression; it’s you exercising your contractual right to a fair shake. It tells the insurer you won’t be settling for a number spit out by a flawed algorithm.

A firm that specializes in this process can handle everything for you, from sending the formal notification to negotiating with the final umpire. This ensures every detail is managed correctly, positioning your claim for the best possible result. If you want to dive deeper into how this works, check out our complete guide to the diminished value claim Oregon process. It's your roadmap for taking control and getting the settlement you deserve.

Common Questions About Classic Auto Appraisals

When you're staring down a tough insurance claim, questions are bound to pop up. Getting straight answers is the first step toward making a smart decision and protecting your investment. Let's tackle some of the most common questions classic car owners have when they find themselves in this situation.

How Much Does a Professional Classic Car Appraisal Cost?

The final number can vary based on your vehicle's complexity and the details of your claim, but it's crucial to see a high-quality appraisal as an investment, not just another bill. A well-researched, professional report often pays for itself many times over, increasing a final settlement by thousands—sometimes tens of thousands—of dollars.

Think of it as your financial defense plan. You're paying to ensure an insurer's lowball offer doesn't become the final word on your classic's value. A small upfront cost is what protects your much larger asset.

Can I Get an Appraisal After Accepting an Insurance Offer?

Unfortunately, the answer is a hard no. The moment you accept a settlement, cash that check, and sign their release forms, the insurance company slams the book shut on your claim. It's a harsh lesson many owners learn when it's already too late.

This is why it's absolutely critical to contact a certified classic auto appraiser the second you get an offer that feels wrong. Acting quickly—before you agree to anything—is the only way to keep your options open, dispute their valuation, and fight for the compensation you truly deserve.

How Long Does the Appraisal and Claim Process Usually Take?

Doing this right takes time. A thorough vehicle inspection and building a detailed, evidence-backed report can easily take several days. Once the Appraisal Clause is officially invoked and your report is in the insurer’s hands, the real negotiation begins.

While some claims wrap up in a few weeks, more complex cases can take longer. A good appraiser’s goal isn't just to get you a fast settlement; it's to get you a fair one that reflects your car's actual market value.

Does My Car Have to Be a Perfect Show Car to Qualify?

Absolutely not. This is one of the biggest myths out there. Expert appraisals are essential for any vehicle that standard book guides simply don't understand.

This covers a huge range of vehicles that you might not expect, including:

- Well-maintained "driver" classics that have significant value because of their excellent condition and the care they've received.

- Custom builds and restomods where thousands of dollars in parts and labor are completely invisible to standard valuation software.

- Rare or historically significant models whose value has nothing to do with their original sticker price.

Bottom line: if your car's real worth is tied to its unique condition, history, or custom features, you need a classic auto appraiser to properly document and defend that value.

Don't let an insurance company's flawed software dictate the value of your classic, custom, or daily driver. At Total Loss Northwest, we fight for the true market value you're owed. If you're facing a total loss or diminished value claim in Oregon or Washington, contact us to get an expert on your side.