You've probably got the estimate open on your phone right now. The dealership looked at your crash damage, printed a number that made your stomach drop, and now the insurance adjuster is acting like that number is either outrageous, incomplete, or both.

That's the fight.

A dealership estimate isn't just a repair quote. Inside an insurance claim, it provides influence. The carrier may use it to cut parts, trim labor, steer you to another shop, or push your vehicle toward a total loss if repairing it at dealership rates doesn't fit their math. If you don't understand how they read that estimate, you're negotiating blind.

I've seen this play out every way possible. A clean late-model vehicle gets tagged with expensive calibrations and OEM parts. A borderline total loss gets treated like a repairable car until the supplement stack grows. An owner assumes the dealership number is automatically “approved,” then finds out the insurer only wants to pay what it calls a reasonable local rate. None of that is rare.

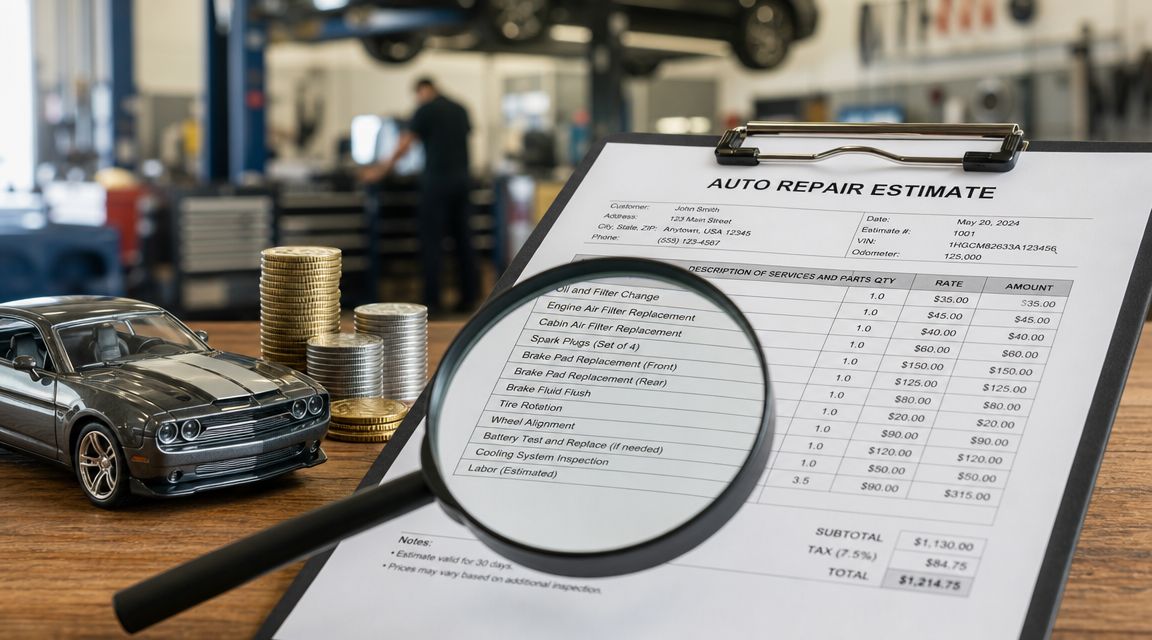

Why Is This Dealership Repair Estimate So High

You pick up your vehicle after the initial inspection, or more often you don't pick it up because it's sitting torn down behind the service lane, and the estimate lands in your inbox. The front bumper cover doesn't look that bad. Maybe a headlamp, a fender, some paint. Then you see the total and wonder if somebody added another car by mistake.

That reaction is normal.

Recent U.S. repair and maintenance data moved sharply higher. The Bureau of Labor Statistics-based measure cited by Cars.com rose 43.6%, from $290.76 in January 2019 to $419.42 in January 2025, which is one reason a modern repair bill now hits harder than drivers expect (Cars.com repair cost data).

What changed in the real world

Vehicles got more complicated. A bumper isn't just painted plastic anymore. It may sit in front of sensors, cameras, brackets, wiring, absorbers, trim pieces, and calibration procedures that don't show up until the shop writes a full blueprint. The dealership also tends to write a more complete estimate on newer vehicles because it knows the brand systems, the repair procedures, and the parts catalog better than most shops.

Then insurance gets involved.

The adjuster doesn't see your shock. The adjuster sees line items. They'll ask whether all those operations are necessary, whether the labor rate is too high, whether OEM parts are required, and whether the repair cost now makes the car a total loss candidate. That's why your estimate feels like one number to you and ten separate arguments to them.

Practical rule: A high dealership estimate doesn't automatically mean the shop is wrong. It usually means the estimate is detailed, brand-specific, and expensive in all the places insurers like to challenge.

Why this matters in a claim

If your car is repairable, the estimate affects what parts get approved and how much delay you'll deal with. If your car is near total loss territory, that same estimate can change the whole direction of the claim. The insurer may decide it doesn't want to pay dealership-level repair costs, supplemental damage, and rental exposure all at once.

That's why you need to read the estimate as a claims document, not just a repair invoice.

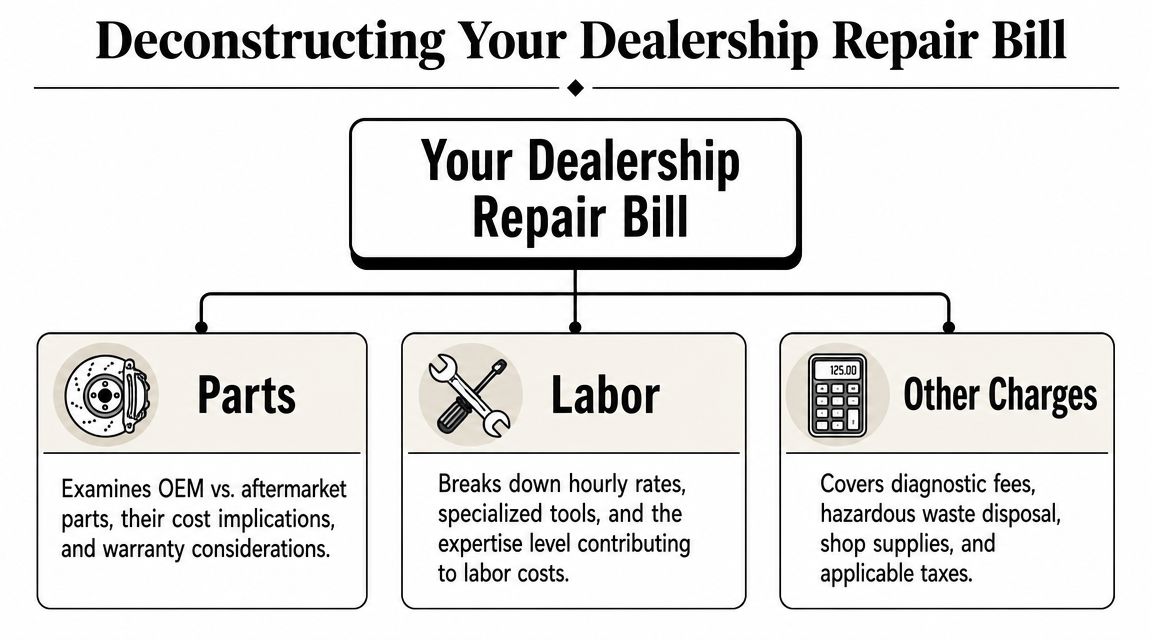

Deconstructing Your Dealership Repair Bill

A dealership repair bill works like a high-end restaurant check. You're not just paying for the steak. You're paying for the kitchen, the staff, the location, the equipment, and the system behind the service. Same idea here. The invoice usually breaks into parts, labor, and other charges.

Labor is where the premium usually lives

AAA reports that dealership shops typically charge 25% or more above independent mechanics because they use factory-trained technicians, brand-specific diagnostic tools, and carry higher overhead such as franchise fees and facility costs (AAA labor rate analysis). That's the core reason many dealership repair costs spike fast on accident claims.

On paper, labor looks simple. It isn't. You'll often see body labor, paint labor, mechanical labor, diagnostic time, calibration time, and scan time. Some of that follows book time. Some of it reflects required procedures. Some of it gets disputed because the insurer thinks a different shop could perform the same operation for less.

Parts are not all equal

The next chunk is parts. Owners often encounter complications due to insurers and repairers frequently using the same words to mean different things. A dealership estimate will often lean toward OEM parts, especially on newer vehicles or vehicles with sensor-heavy assemblies. The insurer may counter with aftermarket, recycled, or alternative-sourcing options if your policy and state rules allow it.

That disagreement matters because a cheap substitute part can affect fit, finish, sensor mounting, and resale arguments later. If your estimate includes OEM parts, don't let the adjuster brush that aside with “a part is a part.” It isn't.

Other charges are where the bill gets sneaky

Many owners stare at labor and parts and miss the smaller categories that add up:

- Diagnostic charges can appear before any wrench turns because the shop has to identify electronic faults.

- Calibration operations may be listed separately from installation work.

- Shop supplies and disposal fees often look minor alone but grow across a full estimate.

- Taxes land at the end and make an already painful number worse.

The line items that insurers call “soft” are often the exact items that modern vehicles actually require.

What to review line by line

When you get the estimate, check these items before you argue price:

- Labor categories: Make sure the shop didn't collapse everything into one vague charge. Specific categories are easier to defend.

- Part descriptions: Look for OEM references, alternative part flags, and whether the parts are new, recycled, or remanufactured.

- Repair versus replace decisions: A dealer may replace where another shop might repair. Sometimes that's justified. Sometimes it's caution.

- Procedures tied to electronics: If a component affects driver assistance or security systems, those operations deserve closer attention.

A clean, itemized estimate gives you a fighting chance. A one-page summary doesn't.

Dealership vs Independent Shop Estimates Compared

People love simple answers. “Dealers cost more” is the easy one. The full picture is messier, and messy matters when you're in a claim dispute.

A widely cited Automotive Aftermarket Industry Association study found repairs cost 34% more at new-car dealerships than at independent repair shops, adding up to $11.7 billion in excess annual costs for consumers (widely cited dealership premium study). But a more recent Cox Automotive service study reported the average dealership service visit in 2023 was $258 versus $249 at non-dealer providers, only a $9 gap (Kelley Blue Book report on dealer and non-dealer service visits).

That doesn't mean both shop types cost the same. It means the gap depends heavily on the job.

The real trade-off

Routine maintenance and straightforward repairs can land surprisingly close. Complex collision-related work, electrical faults, software issues, and brand-specific diagnostic problems often split wider. That's where dealership repair costs become harder for insurers to ignore and harder for owners to justify without documentation.

Here's the side-by-side view that matters.

| Factor | Dealership | Independent Shop |

|---|---|---|

| Labor approach | Usually higher hourly rates tied to brand training and dealer systems | Often more flexible pricing |

| Parts sourcing | More likely to write OEM-focused estimates | More likely to offer options |

| Diagnostics | Better access to manufacturer-specific tools and procedures on many makes | Capability varies widely by shop |

| Estimate style | Often more procedure-heavy and brand-specific | Can be leaner, especially on older vehicles |

| Insurance reaction | More likely to trigger labor-rate and parts disputes | More likely to align with insurer “market rate” arguments |

| Best fit | Newer, complex, software-heavy vehicles | Cost control, older vehicles, second opinions |

When a dealership estimate helps you

If the vehicle is newer, under manufacturer warranty, loaded with driver-assistance systems, or has repair procedures tied to proprietary tools, a dealership estimate can strengthen your position. It may show the insurer that the repair isn't a simple body-shop job. That matters in total-loss negotiations because a complete estimate changes the carrier's numbers.

If you need an outside set of eyes to evaluate whether the estimate is realistic, whether the insurer is lowballing, or whether the claim is drifting toward total loss, a review from independent car appraisers can give you a more defensible position than arguing from frustration alone.

When an independent estimate is the smarter move

A second estimate from a reputable independent shop is often the fastest way to expose padding, inconsistent repair methods, or a dealership premium that won't survive a claims review. It also gives you a benchmark. Without that benchmark, you're relying on whatever number the dealer printed first.

Don't turn this into a loyalty contest between dealer and independent shop. Turn it into a documentation contest. The better-supported estimate wins more arguments.

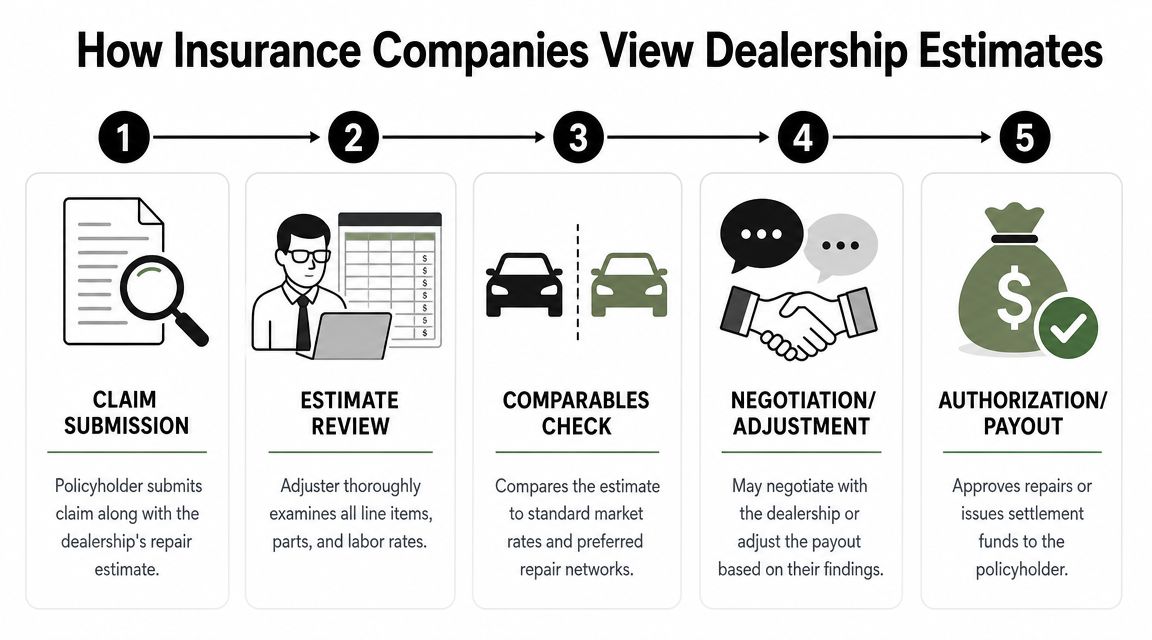

How Insurance Companies View Dealership Estimates

Insurance companies don't look at dealership estimates the way vehicle owners do. You see the bill. They see cost controls, valuation thresholds, and negotiation points.

What the adjuster is actually reviewing

The adjuster usually starts with three questions.

First, is the labor rate above what the carrier considers normal for the area? Second, are the parts choices required, or can they substitute cheaper alternatives? Third, do the repair procedures reflect real manufacturer requirements or a shop's preferred approach?

That's why a dealership estimate can get cut without being fully denied. The insurer may approve the repair but only at what it calls a prevailing rate. It may also challenge calibrations, scans, overlap operations, or replacement choices.

Why a high estimate can push a total loss decision

This is the part drivers miss. A high dealership estimate can hurt and help you at the same time.

If the vehicle sits near the carrier's repairability threshold, the insurer may decide it doesn't want to fight over expensive parts, premium labor, supplements, and added rental time. In that situation, the dealership number becomes support for a total loss decision. That doesn't mean the payout will be fair. It just means the carrier may prefer the certainty of totaling the car over the uncertainty of repairing it.

If you're trying to understand how the insurer arrives at its number, this breakdown of how an insurance company values a car is worth reading before you accept a settlement.

The technology problem insurers don't like to discuss

Modern claims are slower and more technical because the vehicles are. Dealer estimates often reflect that reality better than low-detail estimates from general shops. On the processing side, carriers are pushing digital workflows to move paperwork faster. If you want a look at that back-end trend, this overview on how insurers streamline claims with AI solutions gives useful context for why adjusters rely so heavily on automated review and document handling.

That speed can work against you. Automated systems don't care that your dealer knows the brand better. They compare rates, categories, and parts codes.

What usually gets challenged first

Here are the common pressure points:

- OEM parts use: The adjuster may ask whether non-OEM alternatives are available.

- Labor hours: If the shop wrote a thorough blueprint, the carrier may still trim operations it considers duplicate.

- Diagnostic and calibration lines: These are frequent targets because owners often don't know how to defend them.

- Repair timing: Delays raise rental costs, and insurers pay close attention to anything that stretches the claim.

You don't beat this by saying, “But the dealer said so.” You beat it with documentation, procedure support, and a competing valuation if the claim turns into a total-loss fight.

Real-World Examples of Repair Costs

The average repair is one thing on paper and another in your driveway. Kelley Blue Book and Cox Automotive peg the average repair at $838, but common repairs can jump well above that. A fuel injector replacement can run about $1,127 to $1,251, and a fuel pump replacement can run about $1,125 to $1,247 (Kelley Blue Book average repair and common repair costs).

That matters because owners still walk into claims expecting “a few body panels and some paint” or “just one part under the hood.” Modern repair bills don't stay small for long.

Example one with collision damage

A newer SUV takes a front-corner hit. The visible damage looks limited. The dealer writes for the outer panel parts, associated brackets, paint work, scans, and calibrations because the impact zone involves safety systems. The insurer looks at the same estimate and starts asking whether every operation belongs, whether all parts need to be OEM, and whether a non-dealer shop could do the work for less.

That's a standard conflict, not an unusual one.

If your claim also includes cosmetic items after repairs or owner-paid upgrades, keep your paperwork clean and separate. Small extras muddy negotiations. Even side issues like appearance modifications can create confusion, which is why practical references such as Delaware legal tint limits and pricing are helpful when you're documenting what is accident-related and what is not.

Example two with a mechanical claim after impact

A sedan gets hit, then starts showing drivability issues. The dealership diagnoses a fuel-system problem during post-accident inspection. Suddenly the claim includes a repair category the owner never expected. Using the Kelley Blue Book ranges above, a common component like a fuel injector or fuel pump can already exceed the published average repair amount.

That's where claims get ugly. The insurer may argue the issue is unrelated maintenance. The dealer may say the collision exposed or aggravated the failure. If you don't pin down causation early, the carrier can try to split the claim and leave you paying part of the bill.

A short explainer can help if you want to see how these disputes show up in consumer-facing repair discussions before you go back to the adjuster.

Get the shop to state in writing whether a condition is collision-related, pre-existing, or only discovered during disassembly. Verbal explanations disappear the second the claim gets contentious.

What these examples show

The point isn't that every dealership estimate is inflated. The point is that repair bills escalate fast, and once they escalate, insurers stop treating your claim like a simple repair file. They start managing exposure.

That's when your documentation has to tighten up.

Your Action Plan for High Repair Estimates

You don't need to outtalk the insurance company. You need to out-document them.

Start with the estimate itself

Ask for the full, itemized estimate. Not the summary page. Not the advisor's verbal explanation. You want every labor line, every part number, every note about scans, calibrations, sublet work, and taxes. If it isn't on paper, it's hard to defend.

Then read it like a skeptic. Look for vague entries, bundled labor, or unexplained replacement decisions.

Get a second opinion without delay

Use a reputable independent shop for a comparison estimate, especially if the vehicle is older, the repair seems straightforward, or the insurance carrier is already pushing back. You're not hunting for the cheapest number. You're looking for where the methods differ.

Those differences tell you where the dispute is. Labor rate. Parts choice. Repair versus replace. Diagnostics.

Don't surrender shop choice

The insurer may push its preferred network. That doesn't mean you have to hand your vehicle over. You usually have the right to choose the repair facility, and that choice matters if the car needs brand-specific procedures or if the insurer is trying to normalize everything to a bargain-rate shop.

Escalate when the valuation fight starts

If the carrier uses the dealership estimate to total the vehicle, or refuses to pay enough to repair it properly, stop arguing in circles with the adjuster. Build a record. Save photos. Save the estimate versions. Save the supplements. Save every email.

Then learn how to negotiate with an insurance adjuster without giving away your advantage in the first few calls.

Use the appraisal clause when needed

When the dispute turns into value, not just repairs, the appraisal clause becomes important. That's where an independent appraiser can matter more than another conversation with the claims desk. Total Loss Northwest is one option for owners dealing with total-loss or appraisal-clause disputes in Oregon and Washington, particularly when the insurer's valuation or repair-cost position doesn't match the market.

Bottom line: If the insurer says the dealership estimate is too high, make them prove where it's wrong. If they total the car because of that estimate, make them prove the payout is right.

If you're stuck between a dealership estimate and an insurance company that won't pay fairly, Total Loss Northwest can help you challenge the numbers with an independent appraisal. That's often the difference between accepting the carrier's software-driven figure and getting a settlement based on real market value and actual claim evidence.