Your car's been in an accident, and the body shop did an amazing job. It looks brand new. But even with the best repairs, your vehicle has lost value, and that's a hard fact. This is where a diminished value appraiser comes in. They are certified experts who figure out exactly how much your car's market value has dropped, giving you the proof you need to get that money back from the at-fault driver's insurance.

Think of them as your personal advocate, fighting to recover the hidden financial loss you’ve suffered.

Your Car Is Repaired, But Is It Worth Less?

You did everything right after the accident. You filed a claim, took your car to a great shop, and now it drives just like it did before. So, why do you still have that nagging feeling you’ve lost something? It’s because you have. This lingering loss is called diminished value.

It's the automatic hit to your car’s resale price just because it now has an accident on its record.

The Stigma of an Accident History

Let's put you in a potential buyer's shoes for a moment. You're looking at two identical used cars—same make, model, year, and mileage. One has a squeaky-clean vehicle history report. The other shows it was in a collision, even though it was repaired perfectly.

Which one are you buying? If you even consider the one with the accident history, you'd demand a steep discount, right?

That's inherent diminished value in a nutshell. It’s not about the quality of the repair work; it’s about perception. The moment an accident is documented, the vehicle is permanently flagged in the marketplace, and its value takes a hit.

This accident stigma can slash a vehicle's market value by 10% to 30%. If their client was at fault, the insurance company is on the hook for that loss. But without a professional appraisal, it’s money you'll probably never recover.

Why Insurance Companies Overlook It

Insurance adjusters have one primary goal: to minimize how much the company pays out on claims. It's just business. They often use a generic, lowball formula (like the 17c formula) or simply hope you don't even know you can claim diminished value.

They might tell you that since your car is fully repaired, its value is completely restored. Anyone who has ever tried to sell a car with an accident history knows that's just not true. A professional diminished value appraiser cuts through these tactics with an unbiased, data-driven report that proves your actual financial loss and gets you the compensation you're owed.

Why You Need an Independent Appraiser on Your Side

When your car gets wrecked, it's natural to think the insurance adjuster is there to help you. But here’s the hard truth: they work for the insurance company. Their main job isn't to make you whole; it's to protect their company's finances by paying out as little as possible on your claim.

That’s a huge conflict of interest. They aren't on your team. You're heading into a negotiation where they hold all the cards—the data, the experience, the industry knowledge—and you're just expected to take whatever they offer. This is precisely where a diminished value appraiser steps in to flip the script.

Leveling the Playing Field

An independent appraiser works for you. Period. Their only goal is to give you an honest, detailed, and accurate report on how much value your car has actually lost. They're your expert witness, armed with real-world market data and the right methodology to build a rock-solid case for you.

Think of it like this: would you go to court without a lawyer? Hiring an appraiser is the same idea. Instead of just accepting a lowball number from the insurer, you walk in with a professional, evidence-based report that proves what you're owed. If you're wondering how to find a good one, it helps to know what to look for in an independent auto appraiser near you.

An independent appraiser’s report isn't just a number they pulled out of thin air. It’s a professional valuation document built to hold up under pressure. It gives you the concrete proof you need to fight back against the insurer's low assessment and show the real financial hit you've taken.

Without that professional report, you're just arguing your opinion against their questionable formulas. With it, you're presenting hard market facts they can't ignore. That expert backing is often the one thing that separates a frustrating, failed claim from one that gets you the fair compensation you deserve.

How an Appraiser Pinpoints Your Car's True Lost Value

Figuring out a car's "lost value" after a wreck isn't about pulling a number out of thin air. It's a careful, data-driven process. A professional diminished value appraiser doesn't guess what your car has lost; they build an ironclad case based on real-world market evidence, which is a world away from the cookie-cutter formulas insurance companies love to use.

Most insurers default to a calculation known as the 17-c formula. Right off the bat, this method puts a ceiling on your potential loss, capping it at just 10% of your car's pre-accident value, no matter how severe the damage was. Considering that real-world data shows a car's value can easily drop by 10% to 30% after an accident, you can see how this formula is built to protect their bottom line, not yours.

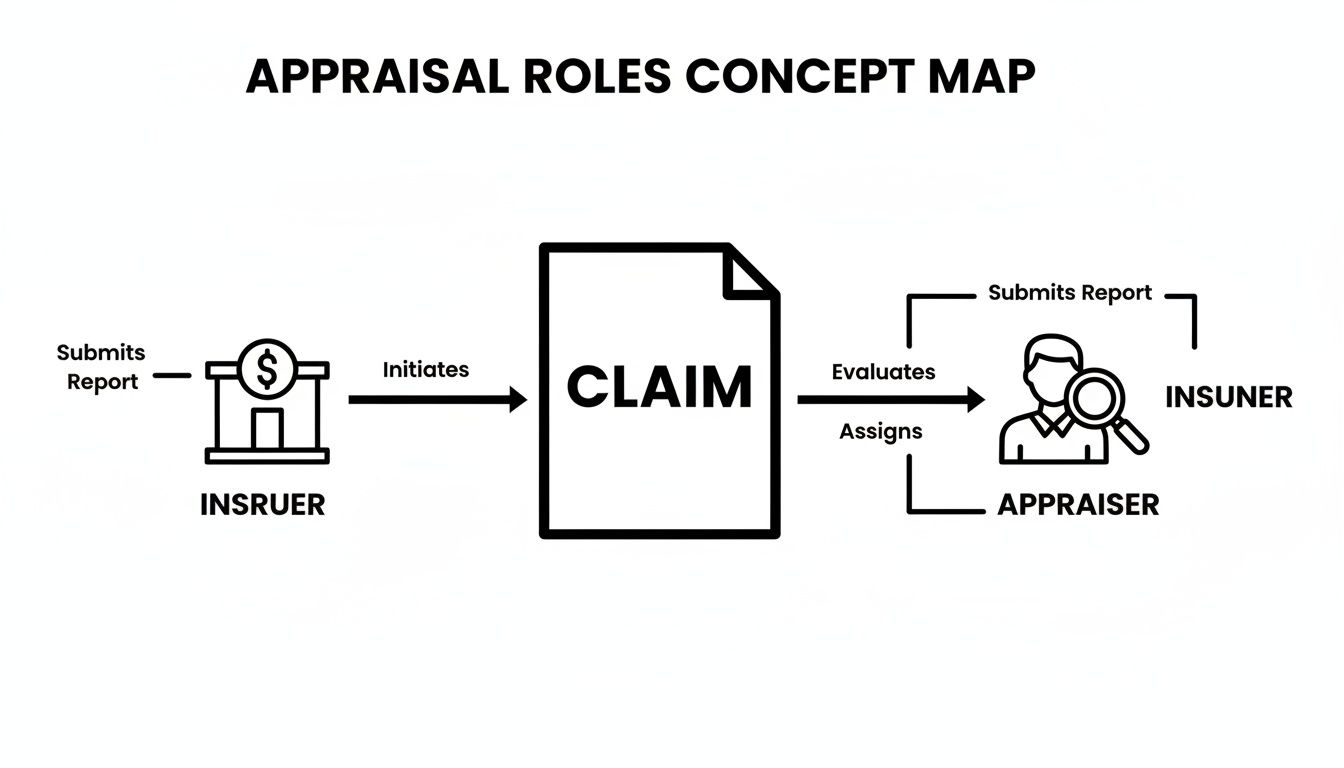

This chart illustrates the different roles your insurance company and an independent appraiser play after you file a claim.

As you can see, the insurer's evaluation is an internal process. The independent appraiser, on the other hand, works for you, providing an objective, external analysis of your actual financial loss.

A Better Way: The Market Analysis Approach

A truly independent appraiser tosses the flawed formulas aside and digs into a full-blown market analysis. This is a much more thorough and, frankly, more honest way to determine your car’s diminished value. Think of it as the difference between a generic, one-size-fits-all estimate and a detailed valuation tailored specifically to your vehicle and your local market.

Here’s a look at how a professional appraiser constructs your claim:

- Comparing "Comps": They dive into real-world sales data, finding vehicles just like yours. They then compare the sale prices of cars with clean histories to those with accident records to establish a clear pattern of loss.

- Getting Dealer Insight: They pick up the phone and talk to sales managers at local dealerships. Getting their expert opinion on what they’d offer for a car like yours—both with and without an accident history—provides powerful, on-the-ground proof.

- Checking Auction Results: Wholesale auto auctions are where the rubber really meets the road. Appraisers review auction data to see exactly how much less dealers are willing to pay for vehicles with a documented accident history.

This is where the difference between an insurer's quick calculation and a real appraisal becomes crystal clear. One is designed for speed and savings (for them), while the other is designed for accuracy.

Comparing Appraisal Methods Insurance vs Independent Appraiser

| Factor | Insurance Co. (17-c Formula) | Independent Appraiser (Market Analysis) |

|---|---|---|

| Basis of Valuation | A predetermined, generic formula with a low cap | Real-world sales data and expert opinions |

| Damage Assessment | Uses arbitrary damage multipliers | Considers the actual severity and type of damage |

| Market Data | Ignores local market conditions and comparable sales | Directly based on your local market and recent sales |

| Outcome | A low, often unfair settlement offer | A well-documented, accurate valuation of your loss |

The table above really sums it up. The 17-c formula is a shortcut that rarely reflects reality, whereas a market analysis is a comprehensive investigation into your specific loss.

By gathering all these data points, an appraiser paints an undeniable picture of your vehicle's true financial hit. They compile all this research into a professional diminished value report, which gives you the hard evidence you need to push back against a lowball offer. It replaces the insurer's opinion with objective proof, making your claim much harder to ignore.

So, how do you know if it's actually worth hiring a diminished value appraiser?

Not every parking lot ding or minor fender-bender is going to justify a formal appraisal. But for more serious accidents, skipping a professional evaluation is like willingly leaving money on the table when negotiating with the insurance company. Knowing when to make that call is the first step to protecting your car's value.

If your car fits any of the descriptions below, getting an appraisal isn't just a smart move—it’s a financial necessity. Use this as a quick mental checklist to see if you have a solid claim.

When an Appraisal Becomes Non-Negotiable

It's time to bring in an expert if your vehicle:

- Is a newer model. Cars that are less than five years old with fairly low mileage take the biggest hit in value after a wreck. Simply put, a newer car has more value to lose.

- Is a luxury or specialty vehicle. The financial sting of diminished value is much sharper for high-end brands, sports cars, or classic models. A 10% loss on a $70,000 vehicle is a lot more painful than a 10% loss on a $15,000 one.

- Had significant damage. If the repairs involved anything structural—like frame work or airbag deployment—the vehicle's history is now permanently scarred. This kind of damage is a massive red flag that sends potential buyers running.

Even if the body shop did an amazing job and the car looks perfect, that accident is now a permanent part of the vehicle's history report. It creates a stigma that will absolutely lower what someone is willing to pay for it later.

A professional appraisal turns your hunch into hard evidence. It shows the insurance company that you've done your homework and are serious about being compensated for the full loss in your car's market value.

Think of it this way: the appraisal fee is a small, strategic investment. It's often a tiny fraction of the thousands of dollars in lost value that a good appraiser can help you recover from the at-fault party's insurance.

How to Choose a Qualified and Credible Appraiser

Not all appraisers are created equal, and honestly, picking the right one can make or break your diminished value claim. You're not just looking for someone to throw a high number on a piece of paper; you need an expert whose report can withstand the intense scrutiny it's bound to get from the insurance company.

Think of it this way: you're hiring an ally. You need someone with the right credentials and a rock-solid, proven methodology to back you up.

The best appraisers almost always come from an auto body or insurance background. This gives them invaluable, firsthand knowledge of what quality repairs look like and how the valuation game is really played. They can provide a data-driven, unbiased assessment that’s hard to argue with.

Core Credentials to Verify

Before you sign on the dotted line, you have to do a little homework and check their qualifications. These certifications aren't just fancy acronyms; they’re your proof that an appraiser is a true professional who sticks to industry standards.

- I-CAR or ASE Certifications: These are huge. They show a deep, technical understanding of modern vehicle construction and repair, which is absolutely critical for judging how severe the damage really was.

- Court Experience: Don't be shy—ask if they've ever testified as an expert witness. An appraiser who is confident enough to defend their findings under oath is exactly the kind of expert you want in your corner.

The single most important standard is compliance with the Uniform Standards of Professional Appraisal Practice (USPAP). This is the undisputed gold standard for all professional appraisers, ensuring their reports are ethical, objective, and built on verifiable facts.

USPAP compliance forces an appraiser to ground their valuation in hard market data, not just their personal opinion. Professionals who follow these standards will typically analyze three to four comparable vehicle sales, adjusting for your car's mileage, regional market trends, and its new accident history to build a valuation that’s truly defensible. You can read more about the importance of appraising diminished value on DailyJournal.com.

Ultimately, choosing a certified, USPAP-compliant appraiser gives you the most powerful tool for your claim. It takes the argument from a subjective "he said, she said" debate and turns it into a professional negotiation backed by solid evidence.

Successfully Navigating Your Diminished Value Claim

Once you have that professional appraisal in hand, everything changes. You're no longer just asking the insurance company for fair compensation; you're demanding it with concrete, undeniable proof. The next move is to formally present this evidence to the at-fault driver's insurance provider.

Your appraiser can walk you through the specifics, but this usually starts with sending a formal demand letter that includes their comprehensive report. This officially puts the insurer on notice. It tells them their initial lowball offer won't fly because you have a documented, market-based valuation of what you’ve truly lost.

Submitting Your Claim with Confidence

This single step completely flips the script. Instead of feeling like you're on the defensive, you're now armed with the most powerful tool you can have in this fight. An adjuster simply can't brush off a detailed, evidence-backed report the same way they can dismiss a car owner's opinion. For a complete walkthrough, our guide on how to file a diminished value claim is a great resource.

Even with solid evidence, some insurance companies will still dig in their heels. If you hit a wall, there’s a powerful but often overlooked tool in the insurance policy itself: the Appraisal Clause.

Invoking this clause can force the insurer into a binding resolution process with a neutral third-party appraiser. It's an incredibly effective way to break a frustrating stalemate and get things moving again.

While court cases for diminution of value have seen a slight decrease, assertions of inherent diminished value persist. For vehicle owners in states like Oregon and Washington, understanding these trends and your rights is essential for a successful claim. You can explore more about these statistical trends on IRMI.com.

At the end of the day, a report from a credible appraiser is your best asset. It gives you the leverage you need to recover the money you are rightfully owed.

Got Questions About Diminished Value? We've Got Answers.

When you're trying to navigate a diminished value claim, questions are bound to pop up. Getting clear, straightforward answers is the best way to move forward with confidence. Let's tackle some of the most common ones we hear.

How Much Does An Appraisal Cost?

It's natural to wonder about the cost, but it’s helpful to think of a professional appraisal as an investment, not just another expense. A solid, well-documented report is the single most powerful tool you have for building a strong case.

Typically, the fee is just a small fraction of the thousands of dollars in lost market value you stand to recover. Without that expert report, you're essentially left arguing your opinion against the insurance company's—and that's a tough spot to be in.

Can I Claim Diminished Value From My Own Insurance Company?

In almost every state, the answer is a firm no. You have to file the diminished value claim against the at-fault driver's insurance company. They're the ones legally responsible for making you whole after the crash.

Trying to claim diminished value against your own policy usually isn't an option, with the exception of a few states that have very specific rules allowing it.

Is A Claim Worth It For An Older Car?

This one really depends on the car itself. It's true that claims tend to have the biggest financial impact on newer cars with low mileage, simply because they have more value to lose in the first place.

But don't count out older vehicles just yet. A high-value classic, a well-kept luxury model, or any older car in exceptional condition can still take a major hit to its value. The only way to know for sure is to have a qualified appraiser run the numbers and see if pursuing a claim makes financial sense for your specific situation.

Quick tip: Don't be surprised if the insurance adjuster initially pushes back on your appraisal report. This is a standard negotiation tactic. A good appraiser can often handle the negotiation for you or help you invoke your policy's Appraisal Clause, which forces the insurer to settle the dispute with a neutral umpire.

If you've been in an accident and are concerned about your car's lost value, don't leave your money on the table. The experts at Total Loss Northwest specialize in certified, data-driven appraisals that get you the fair compensation you deserve. Contact us today to protect your investment at https://totallossnw.com.