You picked up the car, the repair work looks clean, and everyone around you says the problem is solved. But if you tried to trade that same vehicle tomorrow, the dealer would pull the history report, see the accident, and lower the offer. That's the part most drivers feel immediately, even before anyone names it.

A diminished value claim new jersey is about that leftover loss. Not the repair bill. Not the rental. The value your vehicle gave up because it now carries accident history even after proper repairs. In New Jersey, that loss can be recoverable in the right claim, but only if you handle it like a proof problem and not like a complaint.

Many drivers lose their bargaining power early. They call the insurer too soon, rely on the body shop invoice as if it proves market loss, or accept an adjuster's formula without questioning how it was built. The better approach is simpler and more disciplined. Repair the car fully. Build the file. Get an independent opinion of value loss. Then demand payment with evidence that can survive scrutiny.

Your Repaired Car Isn't Worth the Same and You Know It

The body shop may have restored the panels, paint, and drivability. Buyers still care about history. That's why a repaired vehicle can sell for less than an identical one that has never been in a crash.

That post-repair loss is usually called inherent diminished value. It isn't about unfinished repairs or bad workmanship. It's the market discount tied to the fact that the car now has a damage record. If you're sorting out whether you even have this kind of loss, a plain-language overview of diminished value on a car helps frame the issue before you start arguing with an adjuster.

What drivers get wrong first

The most common mistake is assuming repair cost equals diminished value. It doesn't. A vehicle can have a modest repair bill and still take a meaningful hit in resale appeal. It can also have expensive repairs and a weaker diminished value case if the market doesn't react strongly to that history.

Another mistake is treating this like a customer service issue. It isn't. The insurer isn't evaluating how frustrated you are. The adjuster is asking one question: can you prove the vehicle is worth less now than it was before the loss, even after proper repairs?

Buyers don't pay for how good the repair invoice looks. They pay for the car's current market perception.

What a workable claim looks like

A strong New Jersey claim usually has four ingredients:

- Clear liability: The other driver caused the crash, and that part is documented.

- Completed repairs: The car is done. No open estimate, no pending supplements, no guesswork.

- Good records: Photos, police report, final invoice, and service history are all in one file.

- Independent valuation support: Someone other than the insurer has measured the market loss.

If any one of those pieces is missing, the claim gets easier for the carrier to minimize. If all four are present, the conversation changes. You're no longer asking the insurer to be generous. You're telling them the loss exists and you've documented it.

Understanding Your Rights Under New Jersey Law

New Jersey is one of the better states for pursuing this kind of property damage claim, but the legal advantage only helps if you're making the right kind of claim.

Third-party claims are where New Jersey is strong

In New Jersey, diminished value is generally pursued as a third-party claim against the at-fault driver's insurer. New Jersey practitioners point to a February 28, 2019 Appellate Division decision confirming that compensation can include both repair costs and post-repair loss in market value, and they also note a 6-year statute of limitations under N.J.S.A. 2A:14-1 for property damage claims, including diminished value, as discussed by New Jersey diminished value case law analysis.

That matters because it gives you legal footing to demand both categories of loss when the evidence supports them. The car can be fixed and still be worth less. New Jersey recognizes that point.

Fault still controls the outcome

This is still a fault-based claim. The same New Jersey legal discussion notes that recovery is generally available only if you're less than 50% at fault, and any award is reduced by your share of fault in the accident through the state's modified comparative negligence rule. In practice, that means liability disputes can shrink an otherwise solid diminished value case.

If the police report, statements, and insurer file already place fault clearly on the other driver, your path is cleaner. If fault is disputed, settle that issue early because diminished value negotiations are weak when the liability picture is muddy.

Practical rule: Don't start arguing dollar amount until you've pinned down responsibility for the crash.

Why your own insurer usually isn't the answer

Drivers are often surprised by this. They assume that because their own policy paid for repairs, their own carrier should also pay for the loss in value. Usually, that's not how it works.

Most first-party auto policies focus on repairing or replacing damaged property, not paying for stigma in resale value after the repair is complete. If you're reviewing coverage options or trying to understand how a New Jersey policy is typically structured, Liberty Insurance Associates auto policies give a practical reference point for the kinds of coverages and limits drivers should read, especially before a claim happens.

The legal advantage still has limits

A favorable state doesn't mean automatic payment. It means you have a recognized theory of recovery if you prove it correctly. New Jersey gives claimants a better platform than many states, but insurers still push back on weak files, early demands, and unsupported numbers.

That's the trade-off. The law helps. Your evidence wins.

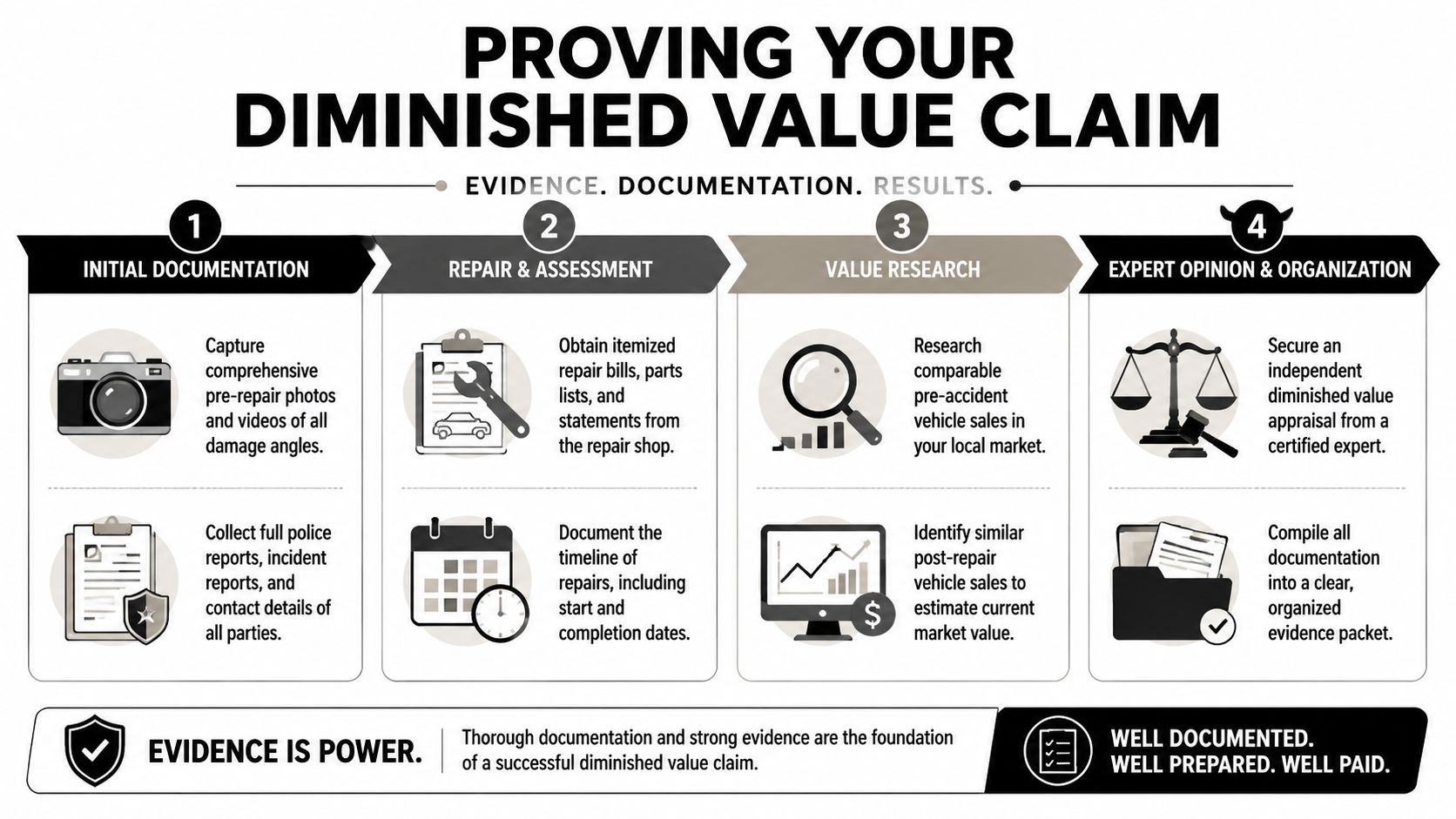

How to Document and Prove Your Diminished Value

Adjusters don't pay diminished value because a driver says, "I know my car is worth less." They pay when the file shows a clean chain from accident, to repair, to remaining market loss.

The New Jersey claim workflow is commonly described this way: complete repairs, assemble documents, get an independent appraisal, then submit a formal demand, and filing before repairs are done or without a credible third-party appraisal weakens negotiating strength because insurers can challenge the loss as speculative, as explained in this New Jersey diminished value process guide.

The order matters

A lot of claims go sideways because the owner skips ahead. They ask for diminished value while the shop is still waiting on parts or while supplements are still changing the scope of repair. That creates an easy defense for the insurer. The carrier can say the final condition of the vehicle isn't even known yet.

Finish the repair first. Get the final invoice, not just the original estimate. Then build the rest of the package around the actual repaired condition of the car.

What belongs in your evidence packet

Don't send a handful of PDFs and hope the adjuster sorts them out. Build one organized file with labels, dates, and a logical sequence.

- Police report and claim details: Include the accident report, claim number, date of loss, names of drivers, and any liability determination already made.

- Final repair invoice: Use the completed itemized bill. If there were supplements, include them too so the insurer sees the full repair path.

- Photos from before and after repair: Pre-loss photos are ideal if you have them. Post-repair photos matter because they document the vehicle's finished condition.

- Service records: A consistent maintenance history supports the argument that the vehicle had solid pre-loss condition.

- Vehicle identification documents: VIN, trim level, mileage at loss, title status, and ownership records all help keep valuation accurate.

Evidence that gives you extra leverage

Some files are adequate. Some files make adjusters cautious. The difference is usually the supporting detail around marketability.

Consider adding:

- Pre-loss condition proof: Recent listing photos, dealership walkaround images, inspection records, or prior appraisal paperwork.

- Parts and repair detail: If the repair involved significant panel replacement, structural work, calibrations, or repainting, the final documentation should reflect that.

- Timeline records: Save messages with the shop, supplement approvals, and completion notices. They help show the claim matured properly before submission.

The cleaner your file looks, the harder it is for the insurer to dismiss your valuation as guesswork.

Build it like a reviewer will challenge every line

I tell drivers to assume the adjuster will look for breaks in logic. Missing dates. Mismatched mileage. Invoices that don't match photos. A demand made before the vehicle was even done. Those aren't minor issues. They're openings.

A simple format works well:

| Document | Why it matters |

|---|---|

| Police report | Supports accident facts and liability |

| Final repair bill | Shows completed repairs and actual scope |

| Photos | Documents damage and final condition |

| Service history | Supports pre-loss condition |

| Independent appraisal | Measures remaining market loss |

If you're making a diminished value claim new jersey, think like you're preparing a file for someone who wasn't there and doesn't care how obvious the loss feels to you. If the documents tell the story without your help, you're in a much better position.

Why an Independent Appraisal Is Your Most Powerful Weapon

The insurer already has a valuation method ready to go. If you don't bring your own evidence, you'll usually be negotiating inside their framework instead of yours.

What the 17c formula does

Insurers often rely on the 17c formula, which starts with the vehicle's pre-loss market value, applies a 10% base-loss cap, and then reduces that amount with damage and mileage multipliers. J.D. Power's guide gives a benchmark example where a $15,000 vehicle has a maximum $1,500 base loss, but the payout may shrink to about $600 after the modifiers, as outlined in J.D. Power's explanation of diminished value calculations.

That formula isn't the used-car market. It's a claims tool. It tends to compress value loss, especially where accident history carries more stigma than the formula acknowledges.

Why that matters in real negotiations

If the carrier uses 17c and you respond with, "That seems too low," you haven't changed anything. You need competing evidence that speaks the language of valuation.

A credible independent appraisal does that. It can analyze local comparable vehicles, account for pre-loss condition, consider the completed repair record, and express an opinion about the remaining market penalty after repair. That's the difference between reacting to the insurer's number and forcing the insurer to deal with yours.

For readers weighing appraisal options, independent car appraisers can include firms that specialize in documenting post-repair market loss for diminished value disputes. Total Loss Northwest is one example of a company that provides certified independent auto appraisals used in these claims.

What a useful appraisal should contain

Not every report helps. Some are little more than a number on letterhead. That won't carry much weight.

A report should be able to answer basic questions:

- What was the vehicle worth before the loss?

- What evidence supports that opinion?

- What is the post-repair market value now?

- What comparable vehicles support the difference?

- How did the appraiser account for trim, mileage, condition, and accident history?

A repair invoice proves what was fixed. An appraisal proves what was still lost.

Here's a short walkthrough that helps many drivers understand how valuation arguments unfold in practice.

When appraisal quality matters most

Some vehicles are hit harder by accident history than others. Late-model vehicles, luxury models, collector vehicles, and clean one-owner cars often need stronger valuation support because buyers in those segments pay close attention to history reports.

That's also where weak insurer formulas tend to feel most disconnected from the actual market. If the vehicle had strong pre-loss desirability, a proper appraisal becomes less of an optional add-on and more of the foundation of the claim.

Drafting Your Demand Letter and Negotiating a Fair Settlement

Once the file is complete, stop talking in fragments. Send one clear demand package. That's the moment the claim becomes organized, reviewable, and harder to brush aside.

If you've never written one before, reviewing a sample insurance demand letter can help you avoid the usual problems, especially vague language and unsupported numbers.

What to put in the letter

Your demand letter doesn't need drama. It needs structure.

Include these elements in plain language:

Accident summary

State the date of loss, location, claim number, and that the other driver was at fault.Vehicle identification

Include year, make, model, VIN, mileage at loss, and ownership information.Repair history

Note that repairs are complete and attach the final itemized invoice.Diminished value position

State that the vehicle suffered post-repair loss in market value and attach the independent appraisal.Settlement demand

Ask for payment in the amount supported by the appraisal and identify a response deadline.

A tone that works better than anger

Adjusters see emotional letters every day. Long narratives about inconvenience, stress, and disappointment usually don't move a property damage file. Clear documentation does.

Use firm wording. Stay professional. Keep every factual statement tied to an attachment. If you say the vehicle was in excellent pre-loss condition, include service records or other supporting proof. If you say the accident history affects resale, let the appraisal explain how the market reflects that loss.

Negotiation note: Written communication protects you. Calls disappear. Letters and emails create a record.

How insurers usually push back

Expect one of three responses.

| Insurer response | What it usually means | Best reply |

|---|---|---|

| Delay | The file isn't a priority yet | Follow up in writing and restate the demand |

| Low offer | They're testing your resolve | Counter with appraisal support, not emotion |

| Denial | They think your proof is weak or your claim is outside coverage | Ask for the denial basis in writing and answer it point by point |

If they offer less than the appraisal amount, don't reject it reflexively. Ask how they calculated their figure. If they used a generic internal formula and ignored your comparable market evidence, say so directly.

What improves leverage

Negotiation gets easier when you remove excuses.

- Send one complete package: Don't drip out records over weeks.

- Reference attachments clearly: Make it easy for the adjuster to find each supporting document.

- Set calendar follow-ups: If they promise review, follow up when that date passes.

- Ask for written reasons: A vague refusal is easier for the insurer. A written explanation pins them down.

There is a point where persistence stops being productive. If the carrier keeps ignoring evidence, refuses to explain its valuation, or leans on blanket denials, it may be time to consult legal counsel. The purpose of mentioning that isn't to threaten. It's to show you're prepared to move the dispute into a more formal process if the insurer won't evaluate the file fairly.

Frequently Asked Questions About NJ Diminished Value Claims

Can I recover diminished value from my own insurance company

Usually no. In New Jersey, the major gap is first-party coverage. You can generally pursue diminished value from the at-fault driver's insurer, while your own policy typically excludes it. Some policies may offer an exception through uninsured or underinsured motorist property damage coverage, but claims are often denied, and New Jersey's minimum required property damage liability is only $5,000, which may not come close to the full loss on a newer vehicle, as discussed in this New Jersey diminished value coverage overview.

What if the at-fault driver has little or no insurance

That is one of the hardest versions of this claim. If the other driver's property damage limits are low, the available insurance may be exhausted by repair costs alone. In that situation, policy language on your own coverage becomes important, especially any uninsured or underinsured property damage provisions. Read the actual policy wording before assuming coverage exists.

Is an older vehicle worth pursuing

Sometimes yes, sometimes no. The central question isn't age by itself. It's market reaction. If the vehicle had strong pre-loss condition, clean history, and a buyer pool that cares about accident records, there may still be a meaningful claim. If it was already carrying prior damage, rough condition, or weak resale demand, the economics may be less favorable.

Do I need a lawyer

Not always. Many diminished value disputes are handled through documentation and negotiation. A lawyer tends to become more relevant when liability is disputed, coverage is limited, or the insurer refuses to address a supported appraisal in good faith.

If you're organizing records, comparing insurer positions, or trying to turn a denial letter into clear next steps, tools like top AI legal assistants can help you sort documents and questions before speaking with counsel. They aren't a substitute for legal advice, but they can help you get organized.

How long should I wait to file

You don't want to rush the valuation before repairs are complete, but you also shouldn't sit on the claim. Delay makes comparable market evidence harder to tie back to the condition and timing of the loss. The strongest claims are mature enough to prove, but still close enough to the accident that the market story is clean.

If your insurer is minimizing post-repair loss or leaning on a formula that doesn't reflect the actual market, Total Loss Northwest provides independent diminished value and total loss appraisal support, including documentation drivers can use in negotiations and claims nationwide.