You've just been in a bad wreck. The other driver is hurt, a passenger is hurt, two cars are totaled, and someone starts talking about missed work, surgery, and lawyers. That's when people learn the hard way that “full coverage” usually doesn't mean what they think it means.

I'll be blunt. Excess coverage insurance is for catastrophic liability exposure. It protects your savings, home equity, wages, and future income when a serious claim blows past the limit on your auto policy. It is not a fix for every insurance problem. If you're fighting over a low total loss offer or diminished value, more liability insurance won't solve that.

That distinction matters a lot in Oregon and Washington. Drivers here often focus on repairing the car or replacing it, which makes sense right after a crash. But the bigger financial threat can be the liability claim attached to the same accident. One severe injury can turn an ordinary policy limit into a speed bump.

Are Your Auto Insurance Limits High Enough

A serious collision doesn't need to look dramatic to become financially ugly. A left turn goes wrong. A cyclist gets clipped. A second vehicle gets pulled in. The ambulance leaves, then the bills start. Medical treatment, lost income claims, legal defense, and property damage can tear through a standard liability limit fast.

Most drivers don't think about that until they picture what comes next. If your policy limit gets used up and the claim keeps growing, the unpaid amount doesn't disappear. That's the part that can come after your assets.

If you're not sure what your current policy even pays for, start by reviewing what liability insurance covers. A lot of people confuse liability coverage with collision, non-collision, or a total loss payout. They're different buckets, and mixing them up leads to expensive mistakes.

Why more drivers are buying extra limits

The market tells the story clearly. Direct premiums written in U.S. surplus lines, which includes excess liability, grew 19.2% in 2022 to a record $98.5 billion, pushing this market to over 10% of all U.S. property and casualty premiums. More recently, premiums rose 13.2% year-over-year in the first half of 2025, according to Higginbotham citing AM Best.

That doesn't mean every driver needs the same policy. It does mean a lot more people and businesses are deciding their standard limits aren't enough for today's environment.

Practical rule: If a serious accident could put your home equity, savings, or future earnings at risk, your current liability limits deserve a hard review.

My recommendation

Don't treat excess coverage insurance like a luxury product for celebrities or business owners with fleets. If you own a home, have money in retirement accounts, earn a solid income, or want to avoid getting financially wrecked by one bad day, you should at least price it out.

A catastrophic claim is rare. That's true. It's also exactly the kind of event that can undo years of financial progress.

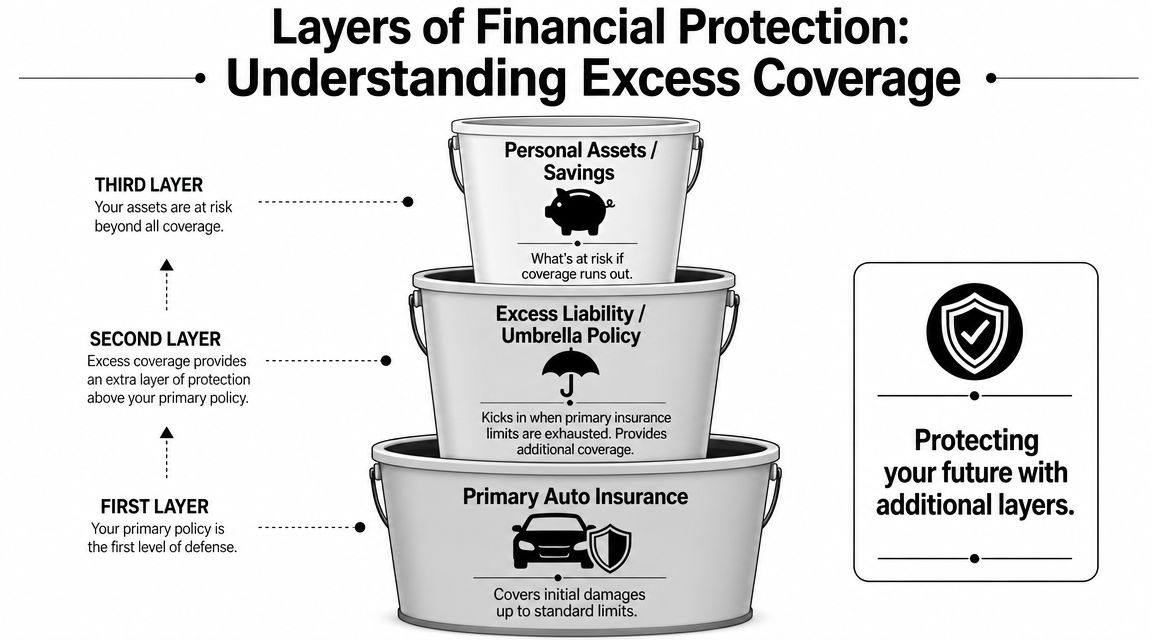

Understanding the Layers of Financial Protection

The easiest way to understand excess coverage insurance is to think in layers.

Your primary auto policy is the first bucket. A covered liability claim hits that bucket first. When that bucket is empty, the next layer matters. That second bucket is the excess policy. If you don't have one, the next bucket is your own money.

What exhaustion actually means

This is the part people skip, and it matters. Excess coverage is structured as a second-loss layer. The primary policy pays first, and the excess insurer only responds after the underlying limits are fully exhausted. The technical details matter because the claim may turn on how the policy defines exhaustion. The CPA Journal also notes that follow-form excess policies typically mirror the underlying policy's coverage triggers and exclusions, which reduces coverage gaps between layers, as explained in this CPA Journal discussion of excess liability structure.

That means the excess carrier usually isn't stepping in early just because the claim looks large. The underlying policy has to be burned through first under the terms of the contract.

Why follow-form matters

“Follow-form” sounds technical, but the concept is simple. A follow-form excess policy usually copies the coverage framework of the policy underneath it.

That's good news if the underlying policy is solid. It's bad news if you thought the excess policy would magically add protections that were never there in the first place.

The concept can be understood clearly as:

- Primary policy pays first. It handles the claim up to its stated limit.

- Excess policy sits above it. It only responds after the underlying limit is exhausted.

- Follow-form usually mirrors the base policy. If the underlying policy excludes something, the excess layer often won't fix that.

- Your assets sit above all of it. If the claim exceeds every available layer, the exposure can land on you.

Excess insurance doesn't rewrite the bottom policy. It usually just adds another layer of money on top of it.

What buyers should check before they rely on it

A lot of bad surprises come from assumptions. Before you count on an excess policy, verify:

- Whether it is follow-form. Don't assume.

- How exhaustion is defined. Payment mechanics can affect when the next layer responds.

- Whether there are added exclusions. A narrower excess form can create a gap right where you expected protection.

- Whether there is any drop-down obligation. If the underlying insurer has a problem, don't guess how the upper layer will react.

This is contract language, not marketing copy. Read it that way.

Excess vs Umbrella vs Primary Insurance Policies

People use these terms like they mean the same thing. They don't.

Your primary policy is the foundation. A true excess policy generally increases the limits of a scheduled underlying policy. An umbrella policy may do more. It can sit over multiple underlying policies and may broaden protection for some losses that the underlying coverage doesn't fully address. That distinction is laid out clearly in this explanation of primary, excess, and umbrella coverage.

The fast comparison

| Feature | Primary Policy | Excess Policy | Umbrella Policy |

|---|---|---|---|

| Main job | Pays first on a covered claim | Adds limits above a scheduled underlying policy | Adds limits above underlying policies and may broaden some protection |

| Coverage scope | Original insuring agreement | Usually follows the underlying form | May be broader than the underlying form |

| Trigger | Starts at the first covered dollar of loss, subject to deductible and policy terms | Starts after underlying limits are exhausted | Starts after required underlying limits are exhausted |

| Typical use | Core auto, home, or liability protection | Higher limits for a specific exposure | Broader personal liability planning across multiple policies |

| Best question to ask | What does it cover and exclude? | Does it truly follow form? | Does it only add limits, or does it also fill gaps? |

Where drivers get tripped up

A lot of households buy what they call “extra insurance” without knowing which kind they purchased. That's risky.

If you want a good outside reference to compare high limit liability policies, use that to frame questions before you talk with your own agent. Don't use it as a substitute for reading your policy language.

Another common mistake is confusing liability protection with physical damage protection. Your auto policy may also include collision and comprehensive auto insurance, but those cover damage to your own vehicle under different rules. They do not replace the need for adequate liability limits.

My opinion on choosing between them

If you have one obvious exposure and want more dollars on top of that exact policy, a true excess policy can make sense.

If you have multiple assets to protect, more than one relevant underlying policy, or you want broader liability planning across your household, umbrella coverage often deserves a closer look.

Buy based on how the policy responds, not what the label on the quote says.

Ask the agent to show you where the policy broadens coverage, where it only extends limits, and what underlying policies it schedules. If they can't explain that cleanly, slow the process down.

Real-World Scenarios for Excess Auto Coverage

The right way to judge excess coverage insurance is to look at what it does in an actual claim, and what it does not do.

Scenario one when excess coverage does its job

You cause a major crash. Multiple people are injured. There's a lawsuit. Your auto policy pays first because that's what primary coverage is supposed to do. Once that limit is exhausted, the excess layer can step in if the claim is still covered under the policy structure above it.

That is the proper use of excess coverage. It is a catastrophic liability tool. It exists to keep a terrible accident from becoming a personal financial wipeout.

If you're trying to understand the claim flow in plain English, this overview helps frame the basics:

Scenario two when excess coverage does nothing for you

Now let's switch to the problem I deal with all the time.

Your vehicle is declared a total loss. The insurer's valuation comes in low. Or your repaired vehicle lost market value after the crash and the carrier pushes back on diminished value. A lot of people assume higher insurance limits somewhere in the household should help.

They usually won't.

Excess liability policies are usually follow-form and only trigger after underlying liability limits are exhausted. They do not create a new valuation process. That's why excess coverage is a poor solution for drivers who are underpaid because of valuation software, disputed comparable vehicles, or diminished value arguments, as explained in this guide on what excess liability does and does not do.

Where appraisal help fits instead

If the dispute is over what your car was worth before the crash, what it's worth after repairs, or whether the insurer's comparable vehicles are garbage, you don't need more liability limits. You need a better valuation process.

That usually means focusing on things like:

- Comparable vehicle quality. Not junk listings, wrong trims, or vehicles from the wrong market.

- Condition adjustments. Mileage, options, prior damage, and maintenance history matter.

- Appraisal rights. Some policies give you a path to challenge the insurer's number.

- Diminished value support. Especially for newer, higher-end, collector, or hard-to-replace vehicles.

If your fight is about the number on the total loss check, excess insurance is the wrong tool. You need valuation evidence.

That's the misconception I want drivers to stop making. More liability insurance protects against being sued for a huge loss. It does not force an insurer to pay more for your own totaled or repaired car.

Is Excess Coverage Right for You Cost and Eligibility

The better question isn't “Am I rich enough for this?” It's “Do I have enough to lose?”

A lot of middle-income households should take excess coverage insurance seriously. If you own a home, have savings, have wages someone could target, or expect your income to keep growing, you already have something worth protecting. Lawsuits don't care whether you think of yourself as wealthy.

Why this market keeps expanding

Research and Markets projects the global excess liability insurance market will grow from $15.89 billion in 2025 to $22.39 billion by 2030, with North America identified as the largest regional market in 2025, according to this excess liability market forecast. That's a projection, not a present fact, but the direction is clear. More buyers want higher limits because severe claims have made old assumptions look thin.

Who should strongly consider it

You should move this up your list if any of these sound like you:

- You have home equity. A severe liability claim can put that at risk.

- You have substantial savings or investments. Cash and non-exempt assets matter.

- You earn good money. Future wages can be part of the exposure picture.

- You drive a lot or transport people often. More road time usually means more liability exposure.

- You have a teen driver or multiple household drivers. More drivers mean more opportunity for a bad claim.

- You own higher-profile assets. Plaintiffs and their lawyers look at collectability, not just fault.

What affects the premium

I'm not going to invent price ranges. What I can tell you is what insurers look at.

They usually care about the limits on your underlying auto and home policies, your driving history, the composition of the household, the nature of the vehicles, and the overall risk profile they see in front of them. They also care whether the policy is being layered over clean, adequate underlying coverage or over a shaky foundation.

My advice is simple. Don't shop excess coverage insurance by price alone. Shop it by fit. A cheap policy with the wrong underlying requirements or tighter exclusions can leave you believing you're protected when you're not.

Special Considerations for Oregon and Washington Drivers

Drivers in Oregon and Washington should pay more attention to liability limits than they usually do.

Why? Because a serious claim here can get complicated fast. Busy corridors, dense urban traffic, bikes, pedestrians, commercial vehicles, weather shifts, and higher repair and medical costs all add pressure to a liability claim. Minimum limits might satisfy the law, but they often don't satisfy reality.

The layered-claim problem most drivers never see coming

Big claims don't always move neatly from one insurer to the next. In layered coverage disputes, the fight often turns on the policy's definition of exhaustion and whether each tier must be fully paid before the next layer responds. That becomes especially important in high-cost states like Oregon and Washington, where a large claim can involve multiple policies and attachment points, as discussed in this analysis of exhaustion requirements in layered excess claims.

That technical issue can affect settlement timing, contribution fights between carriers, and whether an upper layer responds when you expected it to.

Why this matters after a major accident

Here's the practical version:

- One bad injury claim can outgrow basic limits fast.

- Multiple policies can create delay. Each carrier may want proof that the lower layer is fully exhausted.

- Settlement structure matters. If the underlying layer resolves in an unusual way, the next layer may scrutinize whether attachment has actually occurred.

- Property and valuation disputes are separate. If your car is a constructive total loss, that issue still gets decided under the physical damage and valuation side of the policy, not because you bought more liability limits.

Oregon and Washington drivers need to think in two tracks after a crash. One track is liability exposure to others. The other is valuation of their own vehicle. They are not the same fight.

My local advice

If you live in the Portland metro, Seattle metro, or commute heavily on major corridors, review your liability stack before your next renewal. Don't rely on minimums. Don't assume your umbrella or excess policy will behave the way the sales summary suggests. Read the scheduled underlying requirements and the exhaustion language.

That's what protects you when the claim gets messy.

Your Action Plan for Getting the Right Coverage

Start with the loss that could wreck your finances. A serious injury claim can do that. A fight over your own car's value usually cannot.

That distinction matters because people often buy more liability coverage while leaving a different problem unsolved. Excess coverage protects against catastrophic liability exposure. It does not raise a low total loss offer, fix a bad comparable-vehicle report, or resolve a diminished value dispute on your own car.

The checklist I'd use

- Add up what you need to protect. Include savings, home equity, business interests, brokerage accounts, and future income a judgment could reach.

- Pull every declarations page. Review auto, home, rental property, watercraft, and any current umbrella or excess policy together.

- Focus on liability limits first. Premium means nothing if the limits are too low for your risk.

- Confirm what you are buying. Ask whether the policy is true excess, umbrella, or a mix with its own exclusions.

- Get the policy form or specimen. Marketing summaries leave out the language that controls a real claim.

- Verify the required underlying limits. If your primary policies do not meet those requirements, you can end up paying a gap yourself.

- Keep valuation disputes in a separate bucket. If the problem is your insurer's number on a total loss or diminished value claim, use a valuation remedy. Total Loss Northwest handles total-loss and diminished-value appraisal support for qualifying claims.

Questions to ask before you buy

Bring these to your agent or broker and get plain answers in writing.

- Does this policy follow the underlying form, or does it add its own exclusions?

- Which underlying policies are required, and at what limits?

- How does the policy define exhaustion of the lower layer?

- Does it only add more dollars, or does it broaden any coverage?

- What happens if the underlying carrier denies coverage or becomes insolvent?

- What notice do you have to give after a serious crash or likely claim?

- Do any drivers, vehicles, properties, or side businesses in the household create underwriting issues?

Final recommendation

Buy excess coverage for catastrophic liability protection. Set it up carefully, and make sure the underlying limits match what the excess carrier requires.

Use a different tool for property-value disputes. If your fight is over a low total loss settlement or diminished value in Oregon or Washington, handle that as an appraisal or valuation problem, not a liability-limits problem.