You opened the claim email, saw the number, and felt it immediately. It doesn't match your car, your repair history, or the market you know. The insurer calls it a fair valuation. You look at the printout and it reads like software decided what your vehicle is worth before any real person studied it.

That reaction is usually justified.

I've seen this pattern over and over. A clean vehicle gets treated like an average vehicle. A repaired luxury car gets valued like its accident history doesn't matter. A custom truck gets priced as if the options and condition are interchangeable with random listings. The insurer's number often looks polished, but polished isn't the same as accurate.

An expert witness for auto damage is not just for courtroom drama or crash reconstruction. In many claims, the key battle is financial proof. You need someone who can inspect the vehicle, document the condition, explain the damage, and defend a value opinion that doesn't depend on the insurer's software. That matters most in total loss and diminished value disputes, where the core issue is simple: what is the car worth, and how do you prove it in a way the other side can't brush off?

Your Insurance Offer Seems Low Now What

Often, the process begins the same way. The carrier sends a settlement figure. You compare it to what similar vehicles sell for, or you look at your repaired car and know it won't bring the same money it did before the crash. Then the adjuster says the number came from their system, as if that ends the conversation.

It doesn't.

A low offer usually means one of two things. Either the insurer used bad comparable vehicles, or they reduced the claim to a software output that ignores the details that drive real market value. Those details include condition, trim, options, prior maintenance, structural damage, repair quality, and how buyers react to an accident history. In a diminished value claim, those details are the claim.

If your repair check also looks short, it helps to understand how insurers frame these disputes. Pacin Levine on repair claims gives a practical overview of what can happen when the payment doesn't line up with actual repair needs. That same mismatch often shows up in valuation disputes too.

You do not have to accept the first number just because it arrived on official letterhead.

Start by treating the insurer's offer as an opening position, not a final answer. Pull together the valuation report, photos, repair records, window sticker if you have it, and any comparable listings you've already found. Then learn the pressure points adjusters respond to. A good primer on that process is this guide on how to negotiate with an insurance adjuster.

What usually goes wrong

- Bad comparables that don't match mileage, condition, trim, or equipment

- Missed options such as packages, wheels, driver-assistance features, or specialty upgrades

- Weak condition grading that drags the number down

- No serious treatment of stigma loss after substantial repairs

If the disagreement is small, negotiation may fix it. If the dispute centers on market value and the insurer keeps hiding behind software, you need stronger proof.

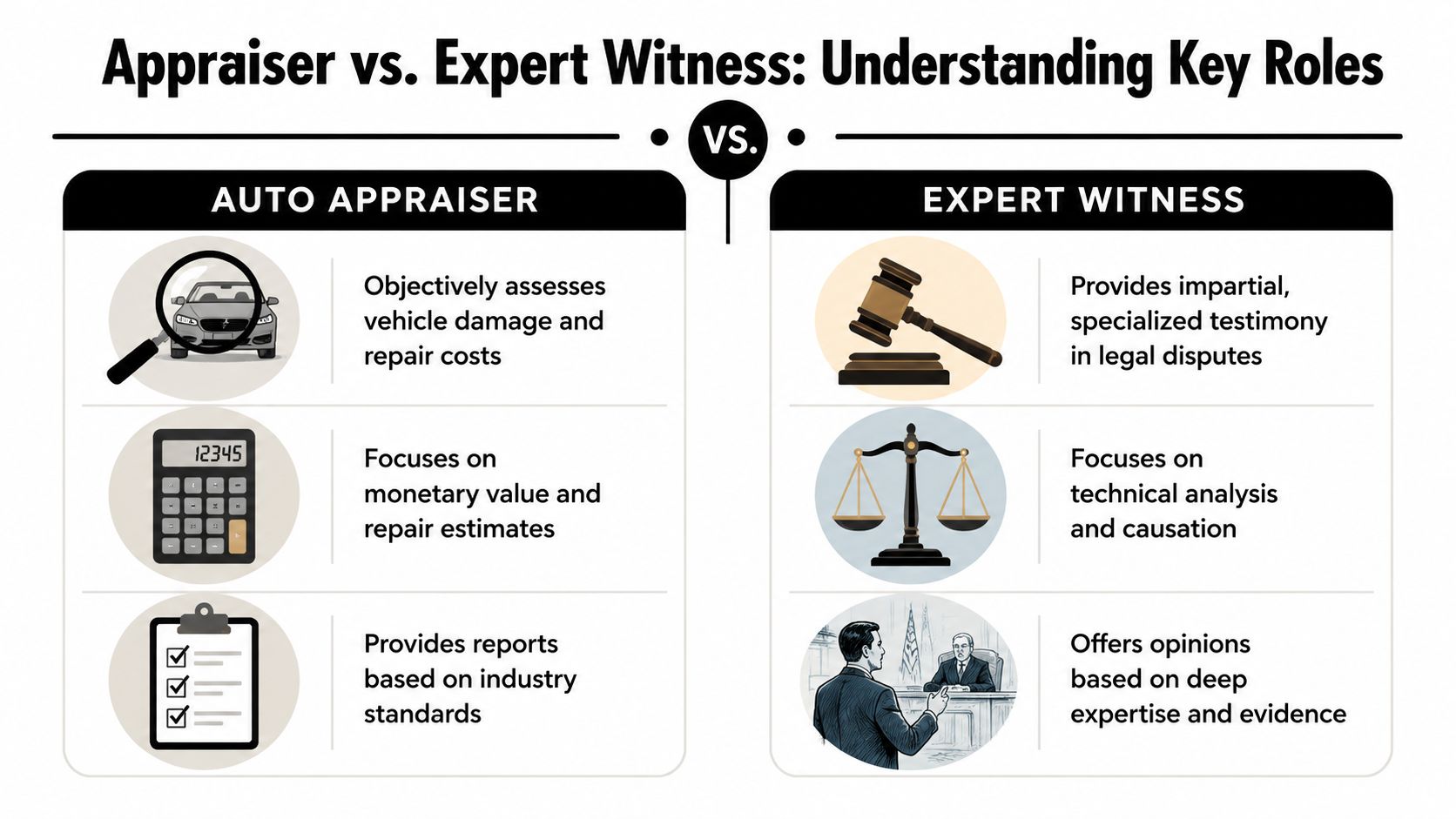

Appraiser vs Expert Witness Understanding the Key Roles

An appraiser and an expert witness are not the same thing, even when one person can serve in both roles.

Think of it this way. A standard appraiser is like a skilled mechanic diagnosing what the vehicle is worth. An expert witness is the professional who can take that opinion into a dispute, explain the method, defend the evidence, and hold up under questioning from lawyers, adjusters, or opposing experts.

Appraiser vs Expert Witness At a Glance

| Factor | Auto Appraiser | Expert Witness |

|---|---|---|

| Primary role | Determines vehicle value or repair-related loss | Defends technical and valuation opinions in a legal dispute |

| Main output | Appraisal report | Court-admissible report, testimony, rebuttal opinions |

| Focus | Market value, condition, comparables, repair impact | Methodology, evidence, credibility, and defending conclusions |

| Typical use | Negotiation, appraisal clause disputes, claim support | Litigation, sworn statements, depositions, trial preparation |

| Scrutiny level | Moderate | High |

| Best fit | Straightforward valuation disagreement | High-conflict claim where the insurer contests causation, value, or both |

When an appraiser is enough

If the issue is a standard total loss dispute and the carrier is still communicating in good faith, an independent appraiser may be all you need. The right appraiser can inspect the vehicle, challenge the comparables, and issue a grounded opinion of value. If you're trying to understand that role better, this page on an insurance appraiser for cars is a useful reference.

When you need the heavier tool

You need an expert witness when the other side is likely to attack the opinion, not just review it.

That happens when:

- The vehicle is high stakes. Luxury, collector, exotic, rare trim, or heavily optioned vehicles invite bigger valuation fights.

- The insurer disputes the basis of loss. They may claim damage was pre-existing, unrelated, cosmetic only, or fully cured by repairs.

- The matter is heading toward lawyers or court. At that point, your report has to survive scrutiny, not just persuade an adjuster.

An appraiser tells you what the vehicle is worth. An expert witness proves why that opinion should be trusted.

If your claim is drifting from negotiation into conflict, hire for defensibility, not just convenience.

When to Engage an Expert Witness for Your Car

You don't bring in an expert witness for every claim. You bring one in when the facts need to be turned into proof that can survive pushback.

Total loss disputes that don't make sense

If the insurer declares the car a total loss and the number is below what it would take to replace your vehicle with a comparable one, that's a trigger. This is especially true when the valuation sheet uses mismatched comps or downplays condition and equipment.

A serious total loss dispute is not about being unhappy with the number. It's about whether the insurer can justify it. If they can't show a credible path from your actual car to their settlement figure, an expert can.

Diminished value claims with real money at stake

This is where drivers get lost, because most public discussion of automotive experts revolves around fault, injuries, or reconstruction. The underserved issue is proving diminished value and total-loss value without relying on insurer valuation software. That gap matters because ordinary drivers need a defensible way to show what the market will pay after a crash, not just what a claims system says. Independent expert resources discuss damage analysis, but they often stop short of explaining the valuation proof needed in these disputes, as noted by Expert Institute's automotive expert overview.

If you drive a newer vehicle, a premium brand, a collector car, or a custom build, diminished value can become the central issue. Even after competent repairs, the market may not treat the vehicle as equivalent to one with a clean history. That's not speculation. That's how buyers act.

Denials based on pre-existing damage or unrelated repairs

This is one of the more aggravating tactics because it shifts the fight from price to credibility. The insurer may say the damage was already there, that the impact couldn't have caused what you're claiming, or that part of the repair bill is unrelated.

In that situation, an expert is useful because the dispute isn't just about value anymore. It's about connecting the physical evidence to the claimed loss.

Three practical triggers

The report is opaque

If the insurer won't clearly explain how it reached the number, don't guess. Get an independent review.The car is not ordinary

Specialty vehicles need specialty analysis. Generic comps won't cut it.The file is hardening

Once communication turns repetitive and the adjuster keeps repeating system output, it's time to escalate.

One practical option in this space is Total Loss Northwest, which provides car expert witness support for total loss and diminished value disputes. The key is not the brand name. The key is finding someone who can inspect, document, value, and defend the result under pressure.

What an Auto Damage Expert Witness Report Includes

A real expert report is not a one-page printout with a bottom-line number. It is a chain of reasoning. If that chain is weak, the opinion is easy to attack. If it's built correctly, the insurer has to engage with the evidence instead of hiding behind software.

For total loss and diminished value disputes, the strongest reports connect the mechanical facts to the financial loss. That means documenting pre-loss condition, addressing repairability versus structural damage, and explaining whether the vehicle's market value remains impaired after repairs, as discussed in Advocate Magazine's analysis of expert roles in motor-vehicle litigation.

The backbone of the report

A useful report usually includes these core parts:

Qualifications and background

The expert's CV matters because the opinion only carries weight if the person behind it can explain their training, experience, and technical basis.Vehicle identification and pre-loss condition

VIN, trim, factory and aftermarket equipment, mileage, maintenance, prior condition, and any prior damage history need to be pinned down.Inspection findings

Photos, measurements, repair records, invoices, and observed structural or cosmetic issues all belong here.Market analysis

This is where the work either becomes credible or falls apart. The expert should use real-world comparable vehicles and explain adjustments, not just recite a software output.Final opinion

The report should state the supported value conclusion clearly, with the reasoning visible on the page.

Why documentation discipline matters

An insurer will often attack the record before attacking the opinion. Missing photos, inconsistent invoices, incomplete repair documents, or uncertain custody of evidence all create openings.

That's why I tell clients to organize evidence like they're already preparing for challenge. If you need a structured way to track files and handoffs, this download evidence documentation form is a practical template.

Practical rule: If a document helps your side, preserve it early. If it hurts your side, disclose it early to your expert so they can account for it.

What separates a strong report from a weak one

A weak report gives conclusions. A strong report shows its work.

Look for these signs of quality:

- Method explained clearly

- Comparable selection justified

- Repair impact tied to market reaction

- Photos and records matched to each conclusion

- No unexplained leaps from damage to dollar figure

If your current paperwork doesn't do that, it's not enough for a serious fight.

The Step by Step Process to Engage an Expert

Hiring an expert sounds intimidating until you break it into actual tasks. The process is straightforward if you move early and stay organized.

Step 1 through Step 3

Start with a case review

Bring the insurer's valuation, photos, repair records, claim correspondence, and any comparable listings you've found. A competent expert can usually tell quickly whether the dispute is about weak valuation, weak causation analysis, or both.Read the engagement letter carefully

This document should spell out scope, fees, deadlines, and whether the work is for negotiation, appraisal, litigation, or testimony.Send every relevant file

Don't curate the file to make it look pretty. Send the bad facts too. Experts do their best work when they know the whole story.

A short explainer may help if you want a visual on how experts fit into accident cases before moving forward:

Step 4 through Step 6

Inspection and technical analysis

In stronger expert-witness auto damage work, the technical foundation comes from integrating vehicle damage patterns, crush profiles, and EDR or black box data with scene evidence such as skid marks, tire tracks, road conditions, and collision photos. That kind of analysis is tied to reliable methodology standards under Rule 702. If litigation is possible, timing matters too. In New Mexico, expert disclosure is typically required 90 days before trial under state rules, as noted in this discussion of expert witnesses used in car accident cases.Review the draft report

This is your chance to correct factual errors. Don't try to steer the opinion. Do verify details like options, mileage, service history, and chronology.Deploy the report strategically

Sometimes the report goes to the adjuster and settlement talks improve. Other times it goes to your attorney, opposing counsel, or into formal litigation.

What you should ask before signing

- Have you handled total loss and diminished value disputes specifically?

- Do you inspect the vehicle yourself or rely only on documents?

- How do you select and adjust comparables?

- Can you defend the report in deposition or trial if needed?

Move fast if court is on the horizon. Delay hurts more than people realize.

The Cost and ROI of an Expert Witness

Let's deal with the obvious concern. Expert witness work costs money, and it's not cheap.

In motor vehicle accident litigation, automotive damage experts typically charge $300 to $800+ per hour, and total case costs often run $3,000 to $15,000 or more per case according to Weatherby Law Firm's guide to expert witnesses in car accident cases. Those figures reflect serious professional work, not a quick opinion. You're paying for inspection, analysis, report writing, file review, rebuttal work, and possibly testimony.

When the cost makes sense

If the disputed amount is modest, the economics may not work. You don't hire a heavy-duty expert to recover a minor gap unless there's a larger legal issue attached.

But when the claim involves a valuable vehicle, a major total loss dispute, or a meaningful diminished value argument, cost needs to be viewed as a strategic advantage. A strong report can change negotiations because it forces the insurer to answer evidence, not just repeat their own numbers.

A simple way to think about ROI

The logic is straightforward:

- Cost of expert work

- Likely improvement in settlement

- Net gain after fees

You don't need a complicated spreadsheet. You need honest math. If the probable increase in claim value comfortably exceeds the professional cost, the hire makes sense. If it doesn't, it may not.

For people trying to budget the valuation side of a claim, this page on diminished value appraisal cost can help frame the discussion.

The cheapest path is often accepting a bad number. It's also the path most likely to leave money on the table.

Questions that prevent wasted spend

Before you hire anyone, ask:

- What exactly is included in the fee?

- Is testimony billed separately?

- Will the expert inspect in person?

- Have they worked on this type of vehicle before?

- Are they being hired to negotiate, testify, or both?

Paying for the wrong scope is a common mistake. Match the level of expert involvement to the level of dispute.

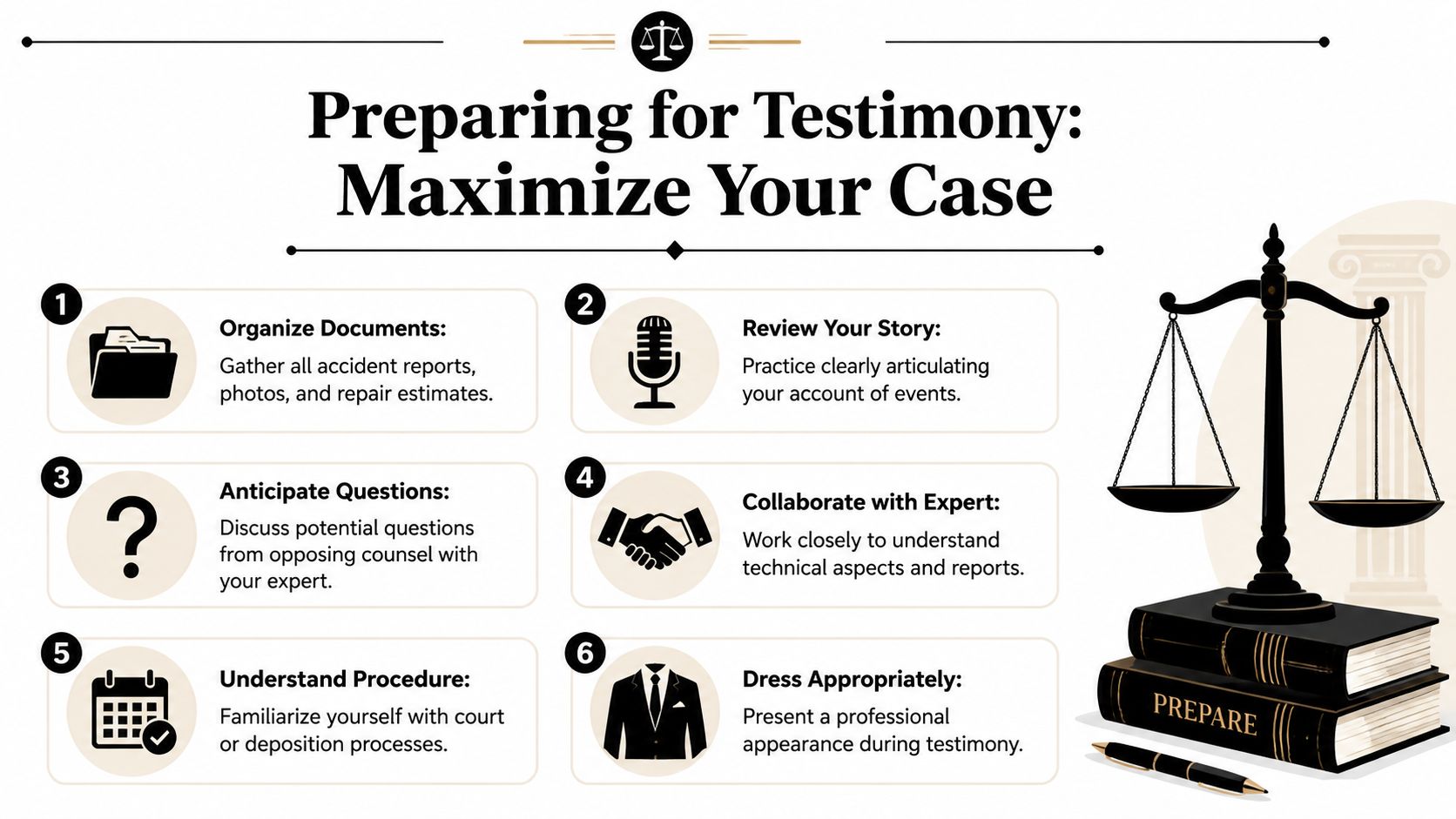

How to Prepare for Testimony with Your Expert

If your case reaches deposition, arbitration, or trial, your job is not to become an expert. Your job is to become a reliable fact witness who supports the expert's work with clean, consistent facts.

Get your own facts straight

Start with your timeline. Know when the collision happened, where the car went, who inspected it, what repairs were made, and what the insurer paid or denied. If you've changed your story in emails, texts, or recorded calls, opposing counsel will find it.

Be candid with your expert about prior damage, modifications, warning lights, title history, and anything else that could affect value. Surprises hurt cases.

Understand the technical themes

You do not need to memorize the report, but you should understand its core logic. In stronger auto damage testimony, the technical proof often comes from combining vehicle damage patterns, crush profiles, and EDR or black box data with scene evidence to support dynamics and causation. That methodology is governed by Federal Rule of Evidence 702. Your expert handles the technical defense. You need to understand enough to avoid contradicting it.

If you don't understand a point in the report, ask until you do. Confusion shows up fast under questioning.

Vetting and prep checklist

Use this checklist before testimony or before hiring the expert in the first place:

Ask about qualifications

What training, certifications, and courtroom experience support the opinion?Ask about method

How did they move from physical evidence to market value?Ask about weaknesses

What facts could the other side use against your claim?Review all documents together

Photos, repair orders, valuation reports, invoices, and claim letters should all line up.Practice concise answers

Don't volunteer speeches. Answer the question asked, then stop.

How clients weaken good experts

The most common problem is not technical. It's behavioral.

Clients weaken strong cases when they exaggerate, hide prior issues, guess at facts they don't remember, or argue with simple questions instead of answering them. A calm, accurate vehicle owner is hard to shake. A defensive one creates openings.

Your expert is there to provide the specialized opinion. You help by being organized, honest, and steady.

If you're fighting a low total loss offer or a diminished value claim that doesn't reflect the actual market, Total Loss Northwest can help you put financial proof behind your position. They provide independent appraisals and expert witness support for vehicle value disputes, including cases where insurers rely on software instead of defensible market analysis.