The key to getting a fair settlement for your totaled car is to calculate its fair market value yourself. This isn't about guesswork; it's about finding recent, local sales of cars just like yours and then adjusting their prices to account for any differences in mileage, condition, and options. It’s a process we call the market approach, and it’s your single best tool for creating a solid, defensible value to push back against an insurer's lowball offer.

Why Your Insurer's Offer Is Just a Starting Point

When your car is declared a total loss, that first settlement offer from the insurance company can feel like a final decision. It's not. Think of it as their opening bid in a negotiation, and it's almost always calculated using third-party software that’s designed to protect their bottom line, not make you whole.

These automated valuation systems are notorious for using wholesale data, outdated comps, and generic condition ratings that completely miss the real-world worth of your specific vehicle.

This is where understanding the difference between their "Actual Cash Value" (ACV) and the true Fair Market Value (FMV) becomes so important. While insurers often use these terms interchangeably, their ACV calculation is skewed in their favor. Your job is to pinpoint the FMV—the price your car would have actually sold for in your local area right before the accident.

The Power of the Market Approach

The most credible way to establish FMV is by using the market approach, which is the same gold standard used in real estate appraisals. It’s powerful because it relies on hard evidence, not some black-box formula. By analyzing real, recent sales of comparable cars right in your own community, you can build a fact-based argument that’s tough for an adjuster to ignore.

This approach boils down to a few key actions:

- Gathering evidence: You’ll be hunting down actual for-sale listings and sales records for cars that are a close match to yours.

- Making adjustments: This involves putting a dollar value on differences in mileage, options, and overall condition between your car and the comps.

- Presenting your findings: Finally, you'll compile all this data into a clear, professional report to give to the insurance adjuster.

Let's say your well-maintained 2019 Ford Mustang is totaled, and the insurer’s offer seems way off. You’re probably right. Shockingly, independent appraisal data shows that initial total loss payouts often average only 72% of a vehicle's true market value. Knowing how to do this calculation yourself is your best defense against leaving thousands of dollars on the table.

Challenging the Insurer's Valuation

One of the biggest hurdles you'll face is the insurer's reliance on their preferred valuation reports. They'll hand you a document from a company like CCC Intelligent Solutions or Mitchell International, often filled with "comparable" vehicles from hundreds of miles away or cars that are a completely different trim level. Worse, they’ll apply vague and arbitrary "condition adjustments" to slash the value without any real justification.

Your job isn't to simply accept their number. It's to challenge it with better data. A well-researched FMV report based on local, verifiable market evidence is almost impossible for an adjuster to dismiss without a very good, documented reason.

Remember, that first offer is a negotiation tactic. The insurance company is counting on you to take it without a fight. By preparing your own valuation, you completely change the dynamic. You're no longer just a claimant asking for more money; you're an informed party presenting evidence that supports your claim. And if you're still not happy with your settlement offer after presenting the facts, you have further options.

This guide will walk you through the exact steps to build that case, turning their low starting point into a fair final settlement. For a deeper dive, check out our guide on the differences between ACV and FMV: https://totallossnw.com/what-is-actual-cash-value-of-my-car/

Finding Comparable Vehicles to Build Your Case

Now that you understand what Fair Market Value is, it's time to roll up your sleeves and gather the evidence to prove it. This is where the real work begins, but it’s also where you take back control of the conversation with the insurance company.

Your mission is to find several "comps"—comparable vehicles for sale or recently sold that are a close match to your own. You’re not just looking for cars that look similar; you're building a data-driven argument that an adjuster can't simply brush aside. Think of it as creating a hyper-local market report for your exact car.

Where to Hunt for Quality Comps

Your search needs to be grounded in reality, which means focusing on real-world listings, not just theoretical book values. The best proof comes from online marketplaces and local dealership inventories where you can see actual asking prices and get all the vehicle details.

Here’s where I always start my search:

- Major Online Marketplaces: Sites like Autotrader, Cars.com, and Cargurus are your best friends. Their search filters are powerful, letting you zero in on the right make, model, year, trim, mileage, and location.

- Local Dealership Websites: Don't overlook the websites of dealerships in your immediate area. This includes big franchised dealers (like your local Ford or Toyota store) and independent used car lots. They often have high-quality, well-documented vehicles that make for perfect comps.

- Classifieds and Niche Sites: For older, classic, or unique vehicles, platforms like Craigslist, Facebook Marketplace, and even enthusiast forums can be absolute goldmines. Just a pro tip: listings on these sites vanish quickly, so always save a permanent record—a PDF or a full-page screenshot of the ad is crucial.

The goal is to cast a wide but focused net. Pull together a solid pool of potential comps, and then we’ll whittle them down to the very best matches.

The Secrets to Finding a True "Comparable"

A powerful comp is basically your vehicle’s identical twin. The more differences there are, the more adjustments you have to make later on, which can give the adjuster an opening to dispute your value. As you hunt, make sure you’re laser-focused on finding vehicles that line up on these critical points.

Your Comp Selection Checklist

- Same Year, Make, and Model: This one’s non-negotiable. A 2019 Honda CR-V is not a valid comp for a 2018 model. Period.

- Identical Trim Level: An EX-L trim has different features, a different engine, and a different original price than a base LX model. It has to be an exact match.

- Similar Mileage: Aim for comps within 15% of your car’s mileage. If your car had 50,000 miles, your sweet spot for comps is between 42,500 and 57,500 miles.

- Key Options and Packages: Did your truck have the factory tow package and a panoramic sunroof? Then you need to find comps that have those high-value options, too.

- Drivetrain and Engine: An all-wheel-drive (AWD) model is valued very differently than a front-wheel-drive (FWD) version, especially here in Oregon and Washington. The same goes for engine size (like a V6 vs. a V8).

A classic insurance tactic is to use comps that are base models or stripped of options to justify a lowball offer. By finding vehicles that truly mirror your car's features, you shut down that strategy before it even starts.

Why Local Comps Are Your Strongest Weapon

Geography plays a massive role in a car’s value. A Subaru Outback is worth a lot more in Seattle than it is in Miami, and a convertible commands a premium in Phoenix, not so much in Portland. Because of this, your comps must come from your local market.

Define your local area as a 100-200 mile radius from where your vehicle was primarily kept. This ensures the asking prices you find reflect local supply and demand, economic factors, and even regional tastes. Insurers often love to pull comps from hundreds of miles away—or even other states—to find cheaper examples. This is a flawed tactic, and your local data is the perfect way to challenge it.

For instance, in the Pacific Northwest market, local values are everything. A clean-title 2019 Mustang GT with 45,000 miles might have an average asking price of $32,500 across Oregon and Washington. But an insurer's software, pulling from a national database, might try to claim it's only worth $29,000. Local data is paramount.

Building Your Evidence File

For every solid comp you find, you need to be meticulous about documentation. Don't just bookmark a link—links die and ads get taken down. You need to capture the evidence permanently. Take screenshots of the entire vehicle listing and save them as a PDF.

Comparable Vehicle Data Collection Checklist

Use this template to gather and organize essential information for each comparable vehicle you find, building a strong and defensible valuation case.

| Comp # | Source (Link) | Year, Make, Model, Trim | Mileage | Listed Price | VIN | Location (Distance) | Key Features & Condition Notes |

|---|---|---|---|---|---|---|---|

| 1 | |||||||

| 2 | |||||||

| 3 | |||||||

| 4 | |||||||

| 5 |

This organized data is the foundation of the valuation report you’ll eventually present to the adjuster. Having a detailed file shows you've done your homework and are ready to back up your number with cold, hard facts—not just opinions.

Adjusting for the Details That Add Thousands

Finding a few similar cars for sale is a solid start, but it’s far from the finish line. The real work—and where you can add significant money to your settlement—is in the adjustments. This is where we turn a simple list of asking prices into a bulletproof fair market value calculation that tells your car's unique story.

An insurer's software often applies generic, sweeping adjustments that rarely capture the full picture. Your job is to meticulously account for every detail that adds or subtracts value. We'll walk through the four most critical areas: mileage, condition, options, and location.

This methodical process of additions and subtractions is what makes your final number so powerful. It proves to the adjuster you’ve done far more than just cherry-pick a few online ads; you’ve conducted a proper analysis.

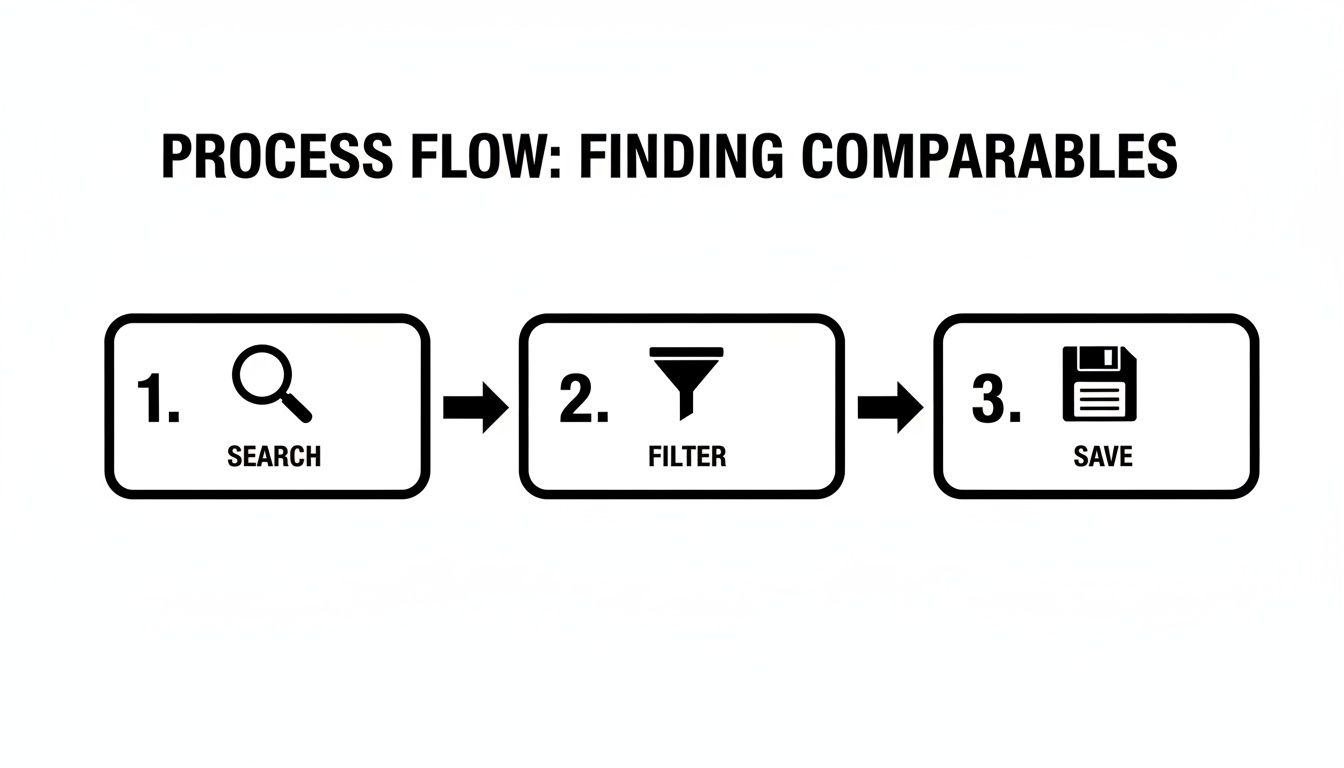

Before we dive into the math, this simple workflow is key to getting your foundation right.

Following this Search, Filter, and Save process ensures you have a solid, well-documented list of comps before you even begin the crucial adjustment phase.

Quantifying the Impact of Mileage

Mileage is one of the biggest drivers of a vehicle's value, and it's an area where adjusters love to make broad, often unsubstantiated deductions. To fight back, you need a repeatable, industry-standard formula. The most widely accepted method is adjusting the price by $0.15 to $0.45 per mile, depending on the car's age and class.

- For newer or luxury vehicles, you'll want to use the higher end of that range (~$0.45/mile).

- For older or more basic economy cars, the lower end is more appropriate (~$0.15/mile).

Let's imagine your totaled car had 50,000 miles. You find a perfect comparable vehicle listed for $28,000, but it has 60,000 miles on the odometer. That's a 10,000-mile difference. Using a mid-range adjustment of $0.30 per mile, you’d make a positive adjustment of $3,000 (10,000 miles x $0.30). The true, adjusted value of that comparable is now $31,000.

Making Objective Condition Adjustments

"Condition" is inherently subjective, which is precisely why insurance companies lean on it so heavily. They'll often slap a generic "average" or "fair" rating on your vehicle without a shred of proof. You need to get specific and break "condition" down into tangible, documented proof points.

First, assign your car a clear rating—Excellent, Good, Average, or Fair—based on real evidence.

Proof of Excellent Condition Can Include:

- Maintenance Records: A complete service history from a dealership or trusted mechanic is your best friend. It’s hard evidence of a well-maintained vehicle.

- Recent Big-Ticket Maintenance: Did you just drop $1,200 on new premium tires or $800 on a full brake job? These aren't just maintenance; they're direct additions to the car's value that an insurer's software will almost certainly ignore.

- Pre-Loss Photos: Clean, clear photos showing off a pristine interior and glossy, swirl-free paint can instantly shut down any argument that your car was just "average."

An "Excellent" condition rating can easily add 5-10% to a vehicle's value compared to an "Average" one. On a $30,000 car, that’s a $1,500 to $3,000 adjustment you simply can't afford to leave on the table.

Valuing Your Options and Packages

Factory options can add thousands to a car's original sticker price, and that value absolutely carries over to the used market. This is a huge blind spot for insurers, who often compare your fully loaded, top-trim model to a spartan base model.

Make a detailed list of every single optional feature your car had. Dig out the original window sticker if you have it, or use a VIN decoder service to get a build sheet.

High-Value Features to Document:

- Tech & Luxury Packages: Premium sound systems, navigation, sunroofs, and advanced driver-assist safety features.

- Appearance & Sport Packages: Upgraded wheels, sport-tuned suspensions, special edition paint colors, or body kits.

- Performance & Utility Upgrades: Factory-installed tow packages, off-road equipment, or the more powerful engine option.

To see how these individual components contribute to the overall value, it helps to understand the core valuation principles. You can learn more about asset-based valuation methods on the Corporate Finance Institute's website. This knowledge is your leverage, especially when you consider how much vehicle values have shifted—surging a staggering 42% from 2020 to 2023 alone.

Accounting for Location and Time of Sale

Finally, the context of the sale matters. Vehicle values aren't static; they fluctuate with seasonal and regional demand. For instance, a 4×4 truck in a snowy, rural part of Washington will always fetch a higher price than the exact same truck in a sunny, urban area of Oregon.

If your comparable vehicles come from a different town or were sold a few months ago, you need to make a logical adjustment. A great way to do this is by looking for patterns. If similar cars consistently sell for 3% more in your local market than in the neighboring city where you found a comp, it's perfectly reasonable to apply a +3% adjustment to that comp's price. This last step shows you’ve truly mastered how to calculate fair market value in your specific market.

To put this all together, let’s look at a sample adjustment table. This is exactly how you should lay out your math for the insurance adjuster, making it clear, logical, and difficult to refute.

Sample Adjustment Calculation

| Attribute | Comparable Vehicle | Your Vehicle | Adjustment Amount | Adjusted Comp Value |

|---|---|---|---|---|

| Starting Price | $28,000 | $28,000 | ||

| Mileage | 60,000 miles | 50,000 miles | +$3,000 | $31,000 |

| Condition | Good | Excellent | +$1,500 | $32,500 |

| Options | Base Stereo | Premium Sound | +$800 | $33,300 |

| Final Adjusted Value | $33,300 |

As you can see, a vehicle that initially looked like it was worth $28,000 is, after a proper and evidence-based analysis, actually worth over $33,000. This is the power of doing your homework.

Putting It All Together: Your Final Value and Report

You’ve done the legwork. You've found solid comparable vehicles and meticulously adjusted their values. Now it’s time for the final push: turning all that raw data into a single, bulletproof number and presenting it to the insurance adjuster in a way they can't ignore.

This final step is more than just math; it’s about crafting a compelling story backed by irrefutable evidence. A professional, logically structured report doesn't just ask for a fair settlement—it demands it.

Calculating the Adjusted Average

Start by lining up the final adjusted values for each of your strongest comps. You should have at least three, but ideally closer to five, that have been carefully adjusted for mileage, condition, features, and location.

Now, do the simple math. Add up the final adjusted values and divide by the number of vehicles you used. This gives you your calculated Fair Market Value. For instance, if your three adjusted comparables landed at $33,300, $32,900, and $33,800, your average FMV is $33,333. This isn't a number you pulled from thin air; it's a figure firmly rooted in what the market says your car was worth.

But don’t forget the extras. Things like a premium audio system (+$1,200), high-end tires (+$800), or even a custom vinyl wrap (+$2,500) add real value. Insurer software often misses these details or applies unfair, blanket condition deductions of 25% or more. Here in Washington State, where we fight these battles daily, a 2024 DMV analysis found that post-accident appraisals uncovered 18% in "hidden" value from modifications alone.

Once you have your total, just remember to subtract any outstanding loan balance or account for a salvage title (which can reduce value by 10-20%). If you want to dig deeper into valuation principles, you can find more great info about vehicle market value on corporatefinanceinstitute.com.

Watch Out for Outliers

As you look over your adjusted comps, you might see one or two that just don't fit. Maybe one is priced way too high, or another is suspiciously low. These are outliers, and they can poison your entire calculation.

Get rid of them. An outlier could be anything from an over-enthusiastic dealer with an unrealistic price tag to a private seller in a rush to sell. If you leave these in, you give the adjuster an easy opening to question your entire valuation method. Stick to the comps that create a tight, believable price range.

Your goal is to present a value that is not just high, but also realistic and credible. Removing outliers demonstrates that you’re being fair and analytical, not just cherry-picking the highest possible prices to inflate your claim.

Focusing on a tight grouping of the most relevant comps builds a much stronger, more defensible position. It shows the adjuster you understand how to calculate fair market value with the same objectivity they claim to use.

Assembling Your Valuation Report

Okay, now it's time to package everything into a clean, professional report. Don’t make the mistake of just firing off an email with a few links and a number. A well-organized document walks the adjuster through your logic, making it difficult for them to push back.

Here’s what your report should look like:

- A Clear Cover Letter: Get straight to the point. Introduce yourself, state the report's purpose is to establish the FMV for your vehicle, and present your final calculated value right up front.

- Your Vehicle's Spec Sheet: List everything about your car: year, make, model, trim, VIN, mileage at the time of the accident, and a detailed list of all factory options, packages, and aftermarket upgrades.

- Pre-Loss Condition Statement: Write a detailed paragraph describing the condition of your car before the accident. Back it up with maintenance records or recent photos if you have them.

- Comparable Vehicle Breakdown: Give each comparable vehicle its own page. Include screenshots of the original advertisement, the link to the listing, and a clear, step-by-step breakdown of your adjustment calculations.

- The Final Calculation: A simple summary page that lists the final adjusted value for each comparable vehicle and shows the final average you calculated.

Presenting your case this way sends a powerful message. It shows you're organized, you've done your homework, and you won't be pushed around. It immediately changes the dynamic from them dictating a number to you starting a serious negotiation.

When Negotiations Stall, It's Time for the Appraisal Clause

You’ve done everything right. You've gathered solid, local comps, adjusted them meticulously, and presented a rock-solid case for your vehicle's value. But the insurance adjuster just won't budge from their lowball number. It’s an incredibly frustrating stalemate, and it happens all the time.

This is exactly where your insurance policy gives you a powerful, often overlooked tool: the Appraisal Clause. Think of it as your ultimate trump card. Invoking this clause takes the decision out of the adjuster's hands and gives it to neutral, certified professionals who understand true market value.

What is the Appraisal Clause, Exactly?

Buried in the fine print of your auto policy is a provision that outlines a formal process for settling valuation disputes. The Appraisal Clause gives both you and your insurer the right to hire your own independent, certified appraiser to value the vehicle. It's a binding process designed to break the deadlock and land on a fair number.

This isn't a lawsuit—it's a contractual right you've been paying for with every premium. It becomes absolutely essential when dealing with classic cars, highly modified vehicles, or any unique ride where standard software like CCC ONE just can’t grasp the real Fair Market Value. When an insurer simply ignores your research, the Appraisal Clause is the formal, professional way to force the issue. You can get a deep dive into the specifics in our detailed guide on the insurance appraisal clause.

The real power of the Appraisal Clause is that it completely removes the adjuster's opinion from the equation. It forces the insurance company to have an independent expert defend its valuation—a battle they often lose when their number is based on shoddy data.

And this isn't just a hypothetical. The proof is in the numbers. A 2022 study showed that a stunning 68% of claimants who invoked their Appraisal Clause recovered an extra $4,200 on average by getting away from the insurer's biased software. You can find more insights on how these professional valuations work from the experts at Hedgestone Business Valuations.

How the Process Actually Works

Once you formally invoke the clause (always do it in writing), a clear path to resolution kicks into gear. While the exact steps can vary a bit by state and policy, it almost always looks like this:

- You Hire Your Expert: First, you find and hire a certified, independent appraiser who knows total loss claims inside and out. They will do their own deep dive into the market to establish your vehicle's true FMV.

- The Insurer Hires Theirs: The insurance company is then required to do the same and hire its own appraiser to produce a valuation.

- The Experts Negotiate: The two appraisers get together, present their findings, and work to negotiate a settlement value they can both agree on.

- The Umpire Makes the Call: If the two appraisers can't come to an agreement, they select a neutral third party, called an umpire. A final, binding settlement is reached when any two of the three parties agree on a value.

This framework guarantees the final number is based on expert analysis and real market data, not an adjuster's internal pressure to close claims for less. It's your single most effective tool when your own good-faith efforts are met with a brick wall.

Answering Your Top Questions About Vehicle Valuations

Even when you know the steps, the reality of a total loss claim brings up specific questions. When you're facing down an insurance company, having clear answers is crucial for both your confidence and your final payout. Let's tackle the most common questions we hear every day.

Can I Just Use KBB or NADA Guides for My Value?

It's a common starting point, but relying solely on guides like Kelley Blue Book or NADA is a mistake. Think of them as broad market thermometers, not a precise price tag for your specific car in your neighborhood.

The biggest problem? Insurance companies love to cherry-pick the lowest numbers from these guides, often citing "trade-in" or "auction" values. Those figures have nothing to do with what you could have sold your car for in a private sale just before it was wrecked. A true Fair Market Value comes from analyzing actual cars for sale—real-world evidence—and then making precise adjustments.

How Many Comps Do I Really Need to Find?

Forget about a magic number. Quality beats quantity every single time. Your goal should be to find three to five rock-solid, highly relevant comparable vehicles.

A few excellent matches from local dealerships will build a much stronger case than a dozen "sort of similar" cars from across the country. The key is to zero in on comps that are the same year, model, and trim, with nearly identical mileage and options. This is what proves you know how to calculate fair market value like a pro.

Remember, a single, perfect match from a dealership 15 miles away is worth more than ten "close enough" examples from three states over. Precision is your best negotiating tool.

What Happens if the Adjuster Just Says 'No' to My Report?

This is a classic insurance company tactic. If the adjuster dismisses your detailed report without offering their own specific, verifiable comps to justify their lowball number, it’s a major red flag. Don't argue with them—escalate.

Your most powerful tool is found right in your policy: the 'Appraisal Clause'. Invoking this clause is your contractual right to take the decision out of the adjuster's hands. It allows you to hire your own independent, certified appraiser. Their valuation, along with one from an appraiser the insurance company hires, forces a binding settlement. It’s the ultimate check and balance against an insurer who refuses to be fair.

Navigating a total loss claim can feel like an uphill battle, but you don't have to let the insurance company dictate the terms. Total Loss Northwest provides independent, certified auto appraisals for vehicle owners throughout Oregon and Washington, ensuring you get a settlement that reflects what your vehicle was actually worth. If you’re ready to get the fair payout you’re owed, visit us at https://totallossnw.com to get started.