That first phone call from the adjuster is more than just a check-in; it's the opening move in a negotiation you probably never wanted to be a part of. To come out on top, you need to control the information, politely but firmly sidestep giving a recorded statement right away, and whatever you do, don't jump at their first settlement offer. It’s almost guaranteed to be a lowball.

Navigating Your First Call with the Adjuster

When the adjuster calls, keep one thing front and center: their goal is to close your claim as fast and for as little money as possible. They work for the insurance company, not you. They might sound friendly and concerned, but that’s a well-honed tactic meant to get you to lower your guard and say something that could hurt your claim down the road.

Think about the sheer scale of their operation. The insurance claims industry has a workforce of over 342,000 adjusters, and they're all juggling a mountain of claims. This pressure cooker environment means they're incentivized to push for quick resolutions, which often translates to undervalued offers instead of fair, careful evaluations.

Setting Boundaries from the Start

This first conversation is your chance to set the tone for every interaction that follows. One of the first things the adjuster will likely ask for is a recorded statement to "get your side of the story."

My advice? Politely decline, at least for now. You're under no legal obligation to give one on the spot, and rushing into it without being fully prepared is a classic mistake.

You can say something simple and professional, like:

"I'm not ready to give a recorded statement just yet. I'm still getting all my information together, but I can schedule a time to talk more next week."

This response does a few things. It’s professional, not aggressive, and it buys you precious time to get your ducks in a row. It also signals to the adjuster that you're organized and taking this seriously, which is exactly the impression you want to make.

What to Share and What to Keep to Yourself

On this initial call, less is more. Stick to the absolute basics—the kind of factual information that's probably already in the police report.

- You can provide: Your name, address, and your car's make and model.

- You can confirm: The date and location of the accident.

- Don't discuss injuries in detail. It's enough to say you are getting or have already gotten medical care. Anything more can be twisted later.

- Never admit fault or even guess about what might have caused the accident.

Before you ever speak with an adjuster, it’s a good idea to ground yourself in the initial steps to take after a car accident. Knowing what to expect is half the battle. For an even more comprehensive checklist, our own guide on what to do after a car accident can walk you through every critical step.

When you control the narrative from day one, you start to shift the power dynamic back in your favor.

Building Your Counter-Offer: How to Prove Your Car's Real Worth

Insurance adjusters love an information gap. A lowball offer is easiest to push through when you don't have the facts to push back. So, your first and most critical job is to close that gap with a mountain of cold, hard evidence that proves your vehicle’s true value.

Your opinion on what your car was worth doesn't hold much weight in these conversations. But a meticulously organized file that tells the story of your vehicle? That’s something they can't just ignore. This is about building an undeniable case, piece by piece.

Tell Your Car's Story with Documents

Think of yourself as your car's biographer. You need to gather every document that proves it was well-maintained and in great shape right before the accident. This is your foundation for dismantling the adjuster’s low offer.

Every receipt is a piece of your argument. Start digging through your glove box, old emails, and file cabinets.

Your evidence file needs to have:

- A Full Service History: Every single oil change, tire rotation, and scheduled maintenance record you can find. This paints a picture of a car that was cared for, not neglected.

- Proof of Recent Investments: Did you just put $1,200 worth of new tires on it? Replace the transmission last year? Find those receipts. These are direct investments that add real, tangible value.

- Receipts for All Upgrades: If you installed a new stereo, custom rims, a roof rack, or even premium floor mats, get the proof. These features separate your car from the basic, stripped-down models the insurer will use for comparison.

- "Before" Photos: Scroll through your phone's camera roll and social media. Pictures from a recent road trip, a family outing, or just a shot of it looking clean in the driveway can be powerful proof of its excellent pre-accident condition.

Many of the same documentation principles apply to both your vehicle and your physical well-being. For a deeper dive, it’s worth reading about how to document your personal injury case from start to finish.

You're building a narrative. The story you want to tell is that this wasn't just any car—it was a well-maintained, high-value vehicle. The more detail you have, the harder it is for the adjuster to argue otherwise.

Finding Your Own, Realistic Comps

Sooner or later, the adjuster will email you a valuation report with a list of "comparable" vehicles, or "comps," that they used to justify their offer. Don't be surprised if these cars are base models, have spotty histories, and are located hundreds of miles away. This is a classic move.

Your job is to find better, more accurate comps.

Head to online car-selling sites and look for vehicles that are an actual match for yours. You're looking for the same year, make, model, trim package, and similar mileage. Crucially, they should also be listed for sale in your local area, because geography matters.

Save screenshots of these listings. Print them to PDF. Copy the links. You are creating a reality check based on the current, local market—not the insurer's skewed data.

If your vehicle is rare, heavily modified, or you simply feel out of your depth, getting a professional vehicle appraisal is a game-changer. An independent, certified appraisal gives you an expert valuation that carries serious authority. When you present your own data-driven comps, you force the conversation back to facts, not their flawed software.

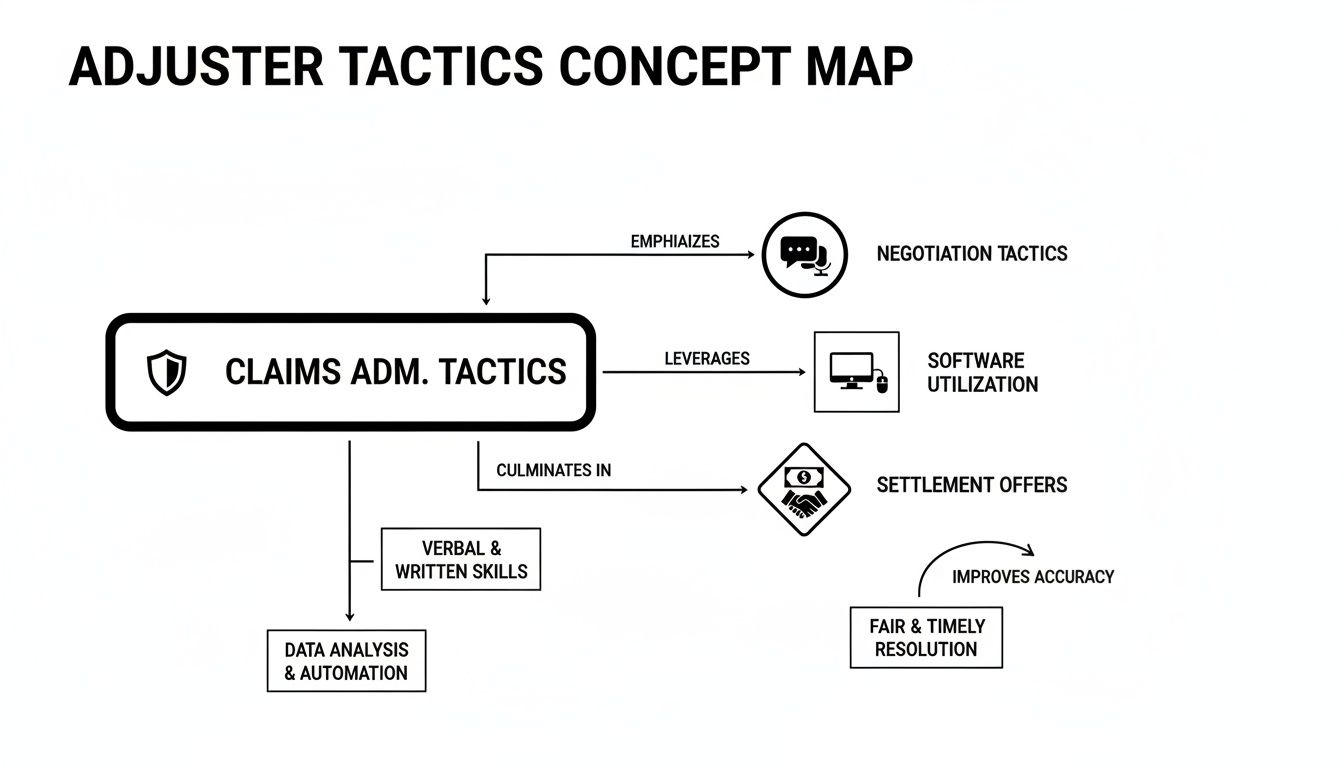

Understanding the Adjuster's Playbook

Insurance adjusters are skilled negotiators, and they walk into every conversation with a well-practiced script. Their job, first and foremost, is to protect their company's financial interests by settling your claim for the lowest possible amount. Knowing their go-to strategies is the first step toward leveling the playing field.

One of the most effective tools in their kit is the sympathy trap. The adjuster will often sound incredibly friendly, expressing how sorry they are about your accident. This isn't just them being nice; it's a tactic designed to build a false sense of rapport. When you feel like they're on your side, you're far more likely to accept a quick, low settlement just to get it over with.

Then there's the strategic delay. Ever wonder why it takes days for an adjuster to return your call, or why they keep "forgetting" to ask for a specific document? This isn't just bad service. It’s a deliberate strategy to drag things out, sometimes for weeks or even months. The longer the process takes, the more financial pressure you're under, making that lowball offer start to look awfully tempting.

Why Their Valuation Software Is Flawed

Nearly every lowball offer starts with a valuation report from software like CCC ONE or Mitchell. These systems scrape data from dealer inventories and recent sales to spit out your car's "Actual Cash Value" (ACV).

But here’s the catch: the data they use is often skewed in their favor. The software frequently:

- Pulls "comparable" vehicles from hundreds of miles away in entirely different markets where prices are lower.

- Ignores your car’s specific trim level, optional packages, and recent upgrades.

- Fails to consider your vehicle’s exceptionally low mileage or pristine pre-accident condition.

The adjuster will present this computer-generated report as if it's the final word—an objective, non-negotiable fact. It’s not. It's just an opening bid, and it’s based on data that conveniently supports their low number. Your job is to pick it apart with your own, better evidence.

The initial offer isn't a reflection of your car's true worth; it's a reflection of what the insurance company hopes you're willing to accept without a fight.

These aren't isolated incidents. Insurance companies rely on these sophisticated tactics to manage their claim payouts. While no single company has more than 5% of the claims adjusting market share, these practices are standardized across the industry. This results in a consistent pattern of undervaluation. For a deeper dive into these behaviors, you can find great information on adjuster tactics at ColoradoInjuryLaw.com.

How to Counter Their Arguments

Winning this negotiation isn't about getting emotional; it’s about being prepared. You need to anticipate what the adjuster will say and have a calm, fact-based response ready to go.

Here's a look at some of the most common things you'll hear from an adjuster and how you can respond with the evidence you've gathered.

Common Adjuster Tactics vs Your Strategic Response

| Adjuster's Tactic or Statement | Your Counter-Argument & Evidence |

|---|---|

| "Our software shows your vehicle is only worth $15,000." | "Your report seems to have overlooked some key details. My vehicle had the premium Technology Package and I have receipts for $2,500 in recent maintenance. I've found three local comps with the same trim selling for an average of $18,500." |

| "Those 'upgrades' don't add much value." | "According to my market research, features like the panoramic sunroof and upgraded audio system consistently increase the resale value for this model. The listings I've provided in my evidence file clearly show this." |

| "This is the best offer we can make." | "Based on the documented evidence I've sent over, including my independent research and maintenance records, a fair market value is closer to $19,000. I'm ready to walk you through the data that supports this figure." |

The key is to stay focused on your documentation. Don't let them pull you into a debate about opinions. Stick to the facts, and you'll keep control of the conversation.

Crafting a Compelling Counteroffer

That lowball offer from the insurance company? Don't think of it as the final word. Think of it as their opening move in a negotiation. Now, it's your turn.

To effectively push back, you need to move beyond phone calls and formally reject their valuation. The best way to do this is with a well-researched demand letter. This isn't just a quick email complaining about the number; it's your official, evidence-based counteroffer.

Your demand letter should professionally lay out your case. It needs to clearly state your rejection of their offer, present your own calculated Actual Cash Value (ACV), and include all the documentation you’ve gathered to back it up—from maintenance logs to your list of comparable vehicle listings.

Calculating Your True Actual Cash Value

The power of your counteroffer is in the data. The adjuster used their system to generate a number; your job is to use real-world market facts to arrive at a more accurate one.

Here’s how I recommend my clients build their counteroffer figure:

- Find Your Market Baseline: Take the 3-5 strong, local comparable vehicles you found and average their asking prices. This gives you a solid starting point grounded in your local market.

- Adjust for Condition: Was your vehicle in exceptional shape for its age, with low mileage? Your detailed service records and photos justify adding a reasonable amount, typically 5-10%, to that baseline.

- Account for Recent Investments: Did you just put on new tires or have a major service done? Add up the receipts for recent, significant work and valuable upgrades. You won't get the full cost back, but you can add a fair, depreciated value for them.

Following these steps gives you a specific, defensible number. It shows the adjuster you're not just guessing—you've done the research and can prove your vehicle's worth.

The adjuster's process is often designed to produce a low initial figure. Your evidence-backed counteroffer is the single most important tool you have to challenge it.

Essential Negotiation Best Practices

Once your demand letter is sent, the real back-and-forth begins. How you handle these conversations is just as critical as the letter itself.

I always tell people, the person who is the most prepared and remains the most professional usually comes out on top. Keep your cool and let the facts do the heavy lifting.

Even if the adjuster is dismissive, stay calm and stick to your evidence. When they call, keep the conversation focused on your documentation and the specific comparable vehicles you provided. Politely ask them to explain—in writing—exactly why your comps aren't valid or why your evidence is being ignored.

Crucially, get everything in writing. After every single phone call, send a short follow-up email. Summarize what you discussed, what they agreed to (or didn't), and what the next steps are. This creates a paper trail that keeps them accountable and is fundamental to successfully fighting for a fair settlement.

Taking It to the Next Level: The Appraisal Clause

You’ve done everything right. You’ve gathered your evidence, laid out a solid case in your demand letter, and tried to negotiate professionally. So what do you do when the adjuster simply won't offer a fair number? It can feel like you've hit a dead end, but there's one more ace up your sleeve, written right into your policy: the Appraisal Clause.

Think of this as your ultimate tool for breaking a stalemate. Invoking this clause formally removes the decision from the adjuster's desk. It's an absolute game-changer when you're up against an adjuster who is digging in their heels and refusing to negotiate fairly.

So, How Does This Actually Work?

Once you trigger the Appraisal Clause, a specific process kicks off. Both you and your insurance company are required to hire your own independent, unbiased appraiser. It's crucial that these are competent professionals.

These two appraisers then get to work, comparing notes and evidence to agree on your vehicle’s true actual cash value. If they can’t find common ground, they bring in a neutral third-party umpire to review everything and make the final call. That umpire's decision is binding for both sides.

What this does is completely sidestep the insurance company's internal valuation reports and software. It forces a resolution based on expert analysis and real-world market data, not a computer-generated lowball figure. You can get a much more detailed breakdown of how the insurance appraisal clause works and why it’s so powerful.

I've seen this clause be particularly effective in a few key scenarios:

- Classic or Collector Cars: Standard valuation tools have no idea how to price rarity, historical importance, or a frame-off restoration.

- Heavily Modified Vehicles: All those expensive aftermarket parts and custom work are often completely overlooked in an initial offer.

- Immaculate, Low-Mileage Vehicles: If your car was in showroom condition, a real appraiser can properly account for that premium value.

This is especially vital when dealing with a total loss claim on a high-value vehicle. Adjusters using their standard software almost always undervalue these cars, sometimes leaving owners short by thousands of dollars. Using the Appraisal Clause forces a fair, market-based evaluation.

Putting the Clause into Action

Ready to make your move? You can't just mention it on a phone call. You need to formally notify the insurance company, and it absolutely has to be in writing. An email works, but sending a certified letter is always my recommendation because it gives you a rock-solid paper trail.

Your letter doesn't need to be complicated. Just state clearly that you are invoking the "Appraisal Clause" or "Right to Appraisal" as outlined in your policy because you and the company have a dispute over the Actual Cash Value of your vehicle.

Once that letter is sent, the clock starts ticking for them. Your insurer is now contractually obligated to hire their appraiser and participate in the process. From this point on, you’re no longer arguing with the adjuster. You're letting the experts settle the dispute based on facts, which is often your best path to getting the settlement you truly deserve.

Your Top Questions About Total Loss Claims Answered

When your car is totaled, a million questions probably run through your mind. It's a stressful situation, and the insurance claim process can feel like a maze. Let's clear up some of the most common concerns people have when they're up against an insurance adjuster. I'll cover your rights, what to expect with timelines, how a car loan complicates things, and when it’s time to call in a lawyer.

Can the Insurance Company Force Me to Use Their Body Shop?

Absolutely not. You have the right to choose your own repair shop. This is a big one.

Insurance companies have their "preferred" shops, often called Direct Repair Program (DRP) shops, because they've cut deals for cheaper labor and parts. While they might push you in that direction, the final decision is yours.

This is especially important if you own a classic, custom, or high-end vehicle. You need a specialist who truly understands your car. Your best move is to get a comprehensive, itemized estimate from a shop you trust. That independent estimate isn't just a quote; it's your primary piece of ammunition when you negotiate, proving what a fair repair actually costs.

How Long Can the Insurance Company Drag This Out?

Every state has its own rules, but they can't leave you hanging forever. Generally, once you file a claim, the insurance company has to acknowledge it within a reasonable timeframe, often somewhere between 15 and 30 days.

After you and the adjuster finally agree on a settlement number, they usually have another 30 days or so to cut the check. These deadlines are there to protect you from getting the runaround.

A word of caution: If your adjuster is ghosting you for weeks or keeps asking for the same paperwork you’ve already sent, they might be operating in "bad faith." Keep a detailed log of every single phone call and email—dates, times, who you spoke with, and what was said.

If you feel the company is deliberately stalling, your next step should be filing a complaint with your state's Department of Insurance. That official paper trail often lights a fire under them to resolve the claim fairly.

What if I Still Owe Money on My Car Loan?

This is where things can get tricky. If your car is a total loss, the insurance settlement check will be made out to both you and your lienholder (the bank or credit union that financed the car). The lender always gets paid first.

The real problem pops up when the insurance company's offer is less than what you still owe on your loan. When that happens, you are on the hook for the difference.

This is the exact scenario that GAP (Guaranteed Asset Protection) insurance was invented for. It covers that "gap" between the car's value and your loan balance. Without it, you could end up in the awful position of making monthly payments on a car that's sitting in a salvage yard.

Is It Time to Hire a Lawyer?

Most of the time, a good independent appraiser can get the job done. But there are a few red flags that signal it's time to bring in legal muscle.

You should seriously think about hiring an attorney if:

- You or anyone else was injured. Personal injury claims are a whole different ballgame and add layers of complexity.

- The insurance company is acting in obvious bad faith (e.g., denying your claim with no valid reason).

- The adjuster has hit a wall and is refusing to negotiate or even look at the evidence you've provided.

An attorney can take over all communications, file the necessary legal paperwork, and show the insurance company you're serious about fighting for a fair outcome, even if it means going to court.

Navigating a total loss claim feels like a battle, but you don't have to fight it alone. If a lowball offer and a stubborn adjuster are standing in your way, the certified experts at Total Loss Northwest are here to step in. We invoke the Appraisal Clause in your policy to force the insurance company to recognize your vehicle's real-world market value. Visit us at Total Loss Northwest to get the settlement you're rightfully owed.