A diminished value claim is your tool to recover the money your car loses in resale value after an accident, even when the repairs are flawless. Getting started means confirming the other driver was at fault, meticulously gathering all your repair documents, and getting an independent appraisal to prove your financial loss. The final step is bundling this evidence with a formal demand letter and sending it to the at-fault driver's insurance company—that's what kicks off a successful negotiation.

Understanding Diminished Value and Your Eligibility

Before you jump into filing a claim, you need to be crystal clear on what you're actually asking for. This isn't about shoddy repair work. It’s about the permanent financial hit your vehicle’s record takes just by being in an accident. The official term for this is inherent diminished value.

Here’s a simple way to think about it. Imagine you’re shopping for a used car and find two identical models. Same year, same mileage, same features. But one has a clean history, and the other was in a reported accident. Which one would you pay more for? The one with the clean record, of course.

That price difference is exactly what diminished value is. The stigma of an accident creates a real, measurable loss that you, as the innocent driver, shouldn't have to carry alone.

What is Inherent Diminished Value?

This is the core of your claim. Inherent diminished value is the automatic loss in a car's market value that happens the second it's involved in a wreck. Even if the best body shop in town makes your car look brand new, its vehicle history report now has a permanent scar. That scar makes it less appealing to savvy buyers down the road.

You're filing this claim because your car is worth less after the repairs than it was just moments before the crash. It's a direct reflection of a buyer's hesitation to pay top dollar for a car with a documented accident history. For example, a 3-year-old SUV valued at $32,000 before a collision might only fetch $28,400 on the market after repairs. That creates a $3,600 diminished value loss you can—and should—claim. For a deeper dive, you can find more insights about diminished value claims by state over at FrancisInjury.com.

Do You Qualify to Make a Claim?

Not every fender bender qualifies for a diminished value claim. Your eligibility really boils down to a few key factors that the insurance company will check right away. Knowing these upfront will save you a ton of hassle and help you set realistic expectations from the start.

To help you figure out where you stand, I've put together a quick reference table.

Quick Guide to Diminished Value Claim Eligibility

Use this table to quickly assess the key factors that determine if you can file a successful diminished value claim.

| Factor | Why It Matters | Example |

|---|---|---|

| Fault | You must not be the at-fault driver. The claim goes against the other party's liability insurance. | Another driver runs a red light and hits your car. Their insurance is responsible for your property damage, including diminished value. |

| Vehicle Value | Newer cars with low mileage and no prior accidents suffer the biggest hit to their resale value. | A 2-year-old luxury sedan will have a much larger diminished value loss than a 10-year-old commuter car with 150,000 miles. |

| Damage Severity | The damage must be significant. Minor dings or cosmetic scratches typically don't justify a claim. | A crumpled quarter panel and bent frame are significant. A small scratch on the bumper that gets buffed out is not. |

| Statute of Limitations | Each state sets a deadline for filing property damage claims, usually two to six years from the date of the accident. | If your state's statute of limitations is three years, you lose the right to file a claim on the third anniversary of the accident. |

Ultimately, your case is strongest if the other driver was clearly at fault, your car is relatively new and valuable, the damage was more than just cosmetic, and you're well within your state's legal time limit to file.

How Market Conditions Affect Your Claim's Value

Your diminished value claim doesn't exist in a vacuum. Its success hinges on proving a real, tangible financial loss in the current used car market, and that market is always in flux. The economic forces at play—think supply and demand, interest rates, even the price of gas—set the stage for how your car’s post-accident value is ultimately judged.

Imagine trying to sell your car in two different scenarios. In a hot market where used cars are flying off the lots, buyers are less picky. The accident history on your vehicle is still a negative, but with fewer options available, the financial hit might be softer.

Now, flip that around. When the market is flooded with used cars and buyers hold all the cards, they can afford to be choosy. That accident history suddenly becomes a massive red flag, giving them powerful leverage to demand a steep discount. This is precisely the environment where a strong diminished value claim becomes even more critical.

The Real Data Behind the Numbers

A good appraiser isn't just guessing a number; they're essentially a market analyst building a case for the insurance company. They have to ground their assessment in real-time data to show why your car is now worth less.

They look at the natural depreciation curve for your specific make and model. For example, vehicles depreciated around 12.5% on average in 2024, but that number means very little without context. A pickup truck depreciates very differently than a luxury EV. An accident adds a permanent, unnatural dip to that curve because the damage is now a public record on reports from services like CARFAX.

This is where the rubber meets the road. Buyers see the accident and immediately offer less. This effect can be even more pronounced when high interest rates cool the market, making every dollar count for a potential buyer. You can get a deeper dive into these trends by checking out the 2025 car value depreciation overview.

The Bottom Line: Your claim isn't just about the damage to your car. It's about how that damage is perceived by real buyers in today's economic climate. A professional appraiser is the one who connects those dots for the insurance company.

To build a compelling argument, an appraiser will dig into several key sources of information:

- Local Market Comps: They’ll find similar, accident-free cars for sale right in your area to establish a baseline value.

- Auction Data: Results from wholesale auctions like Manheim or ADESA show what dealers are actually paying for vehicles like yours, both with and without accident histories.

- Economic Signals: Broader trends, from new car inventory levels to shifts in consumer confidence, all play a role in shaping used car values.

Seeing how all these pieces fit together helps you understand the logic behind your claim's final figure. It shifts your request from "I think my car is worth less" to a data-backed argument that an insurance adjuster can't easily ignore.

Assembling Your Evidence to Build a Strong Case

To get the diminished value you're owed, your opinion alone won't cut it. You need proof—the kind of concrete evidence that insurance adjusters can't ignore. They live in a world of facts and figures, so your task is to build a case file that leaves no doubt about your financial loss.

Think of yourself as the lead detective on your own claim. Your mission is to paint a crystal-clear "before and after" picture of your vehicle's value. The more organized and detailed you are, the less wiggle room an adjuster has to lowball you.

Your Essential Document Checklist

Let's start gathering the paperwork. Every document related to your car and the accident tells a piece of the story, from its pristine pre-accident condition to the nitty-gritty of the repairs. Don't overlook anything.

Here’s what you absolutely need to pull together:

- The Official Police Report: This is ground zero. It establishes the facts of the accident and, most importantly, who was at fault.

- The Body Shop's Itemized Repair Invoice: This is your heavyweight evidence. It details every single part, every hour of labor, and every procedure performed. A $12,000 repair bill tells a much more powerful story than just saying the car was "badly damaged."

- Photos and Videos: Dig up any photos you have of your car before the crash to establish its condition. Pair these with photos of the damage at the scene and, if you have them, during the repair process.

- Vehicle History Report: Pull a CARFAX or AutoCheck report. That accident is now a permanent part of your vehicle's history, and this report is the official record that proves it to any future buyer.

A meticulously organized file sends a clear message to the insurance adjuster: you're serious, prepared, and you mean business. It forces the negotiation to be based on your documented facts, not their assumptions.

Proving Your Car's Pre-Accident Condition

Saying your car was in "excellent condition" is just an empty claim without proof. You need to back it up. This is where your maintenance records become your best friend.

Find those receipts for oil changes, new tires, brake jobs, and any other service you’ve had done. Together, these documents create a portrait of a vehicle that was meticulously cared for, justifying a higher pre-accident value.

As you compile these documents, it’s smart to understand how to evaluate information sources. This ensures that every piece of evidence you present is credible, reliable, and makes the strongest possible impact on your claim.

With all your documents in hand, you can get a ballpark idea of your potential claim. While it's no substitute for a formal appraisal, a good online tool can give you a solid starting point. To get a rough estimate, you might want to use a specialized https://totallossnw.com/diminished-value-claim-calculator/ to see what your claim could be worth. This initial figure helps you set realistic expectations as you prepare for the next step.

Why a Professional Appraisal Is Your Strongest Asset

You’ve done your homework and gathered your evidence, which is great. But the single most powerful tool you can bring to this fight is an independent, professional appraisal. Honestly, trying to negotiate with an insurance adjuster without one is like showing up to a legal battle without a lawyer. You might have the facts on your side, but they have the system, and they know how to make it work for them.

A proper appraisal report completely changes the dynamic. It’s no longer just your opinion against theirs. Instead, it's a formal, data-driven valuation from a certified expert whose entire job is to pinpoint your vehicle’s true loss in market value. This is your ace in the hole to counter the adjuster's lowball offer.

Finding a True Diminished Value Specialist

Let's be clear: not all appraisers are the same. You need someone who lives and breathes diminished value, not a generalist who dabbles in it. A real specialist understands the subtle details that justify a higher claim and, more importantly, knows how to build an airtight report that an insurance company can't just brush aside.

When you're looking for the right person, here's what truly matters:

- USPAP Compliance: The report absolutely must comply with the Uniform Standards of Professional Appraisal Practice (USPAP). This isn't just jargon; it's the gold standard. Without it, the insurer can—and likely will—dismiss your appraisal out of hand.

- Court Experience: Has the appraiser ever served as an expert witness in court? This is a huge green flag. It tells you their work is credible enough to withstand serious legal challenges, giving you immense leverage before things ever get that far.

- Vehicle-Specific Knowledge: Try to find an expert who's familiar with your car’s make and model. Someone who understands the market for a Porsche 911 will approach the valuation differently than for a Ford F-150, leading to a much more accurate number.

A professional appraisal isn't just a number—it's a comprehensive market analysis that provides an irrefutable, third-party validation of your financial loss. This documentation forces the insurer to argue against a certified expert, not just your opinion.

What a Good Report Actually Looks Like

A high-quality appraisal is so much more than a final dollar amount. It’s a detailed story that meticulously explains how the appraiser arrived at that figure. A report worth its salt will always include:

- A deep dive into your specific local used car market.

- Direct comparisons of similar vehicles—some with clean histories, some with accident histories.

- A transparent methodology that clearly explains the formulas and factors used.

I get it—the upfront cost of an appraisal, which can be a few hundred dollars, might feel steep. But think of it as an investment. In my experience, that cost often leads to a final settlement that is thousands of dollars higher than what the insurance company initially put on the table.

A report from a certified professional is what turns your evidence into a successful claim. To get a better feel for the process, you can explore specialized auto insurance appraisals and see how the experts build their case. It’s the one step that elevates your claim from a simple request to a formal demand they have to take seriously.

Filing Your Claim and Negotiating a Fair Settlement

Alright, you've done the legwork. You’ve gathered your evidence and have a professional appraisal in hand. Now it’s time to move from preparation to action and formally demand the compensation you're owed. This is where your meticulous effort turns into a check from the insurance company.

Your first official move is to draft and send a demand letter. Think of this not as a simple email asking for money, but as the formal opening statement in your negotiation. It needs to be professional, clear, and based on facts, presenting your case without getting emotional. This letter officially notifies the at-fault driver's insurance company that you are pursuing a claim for your vehicle's inherent diminished value.

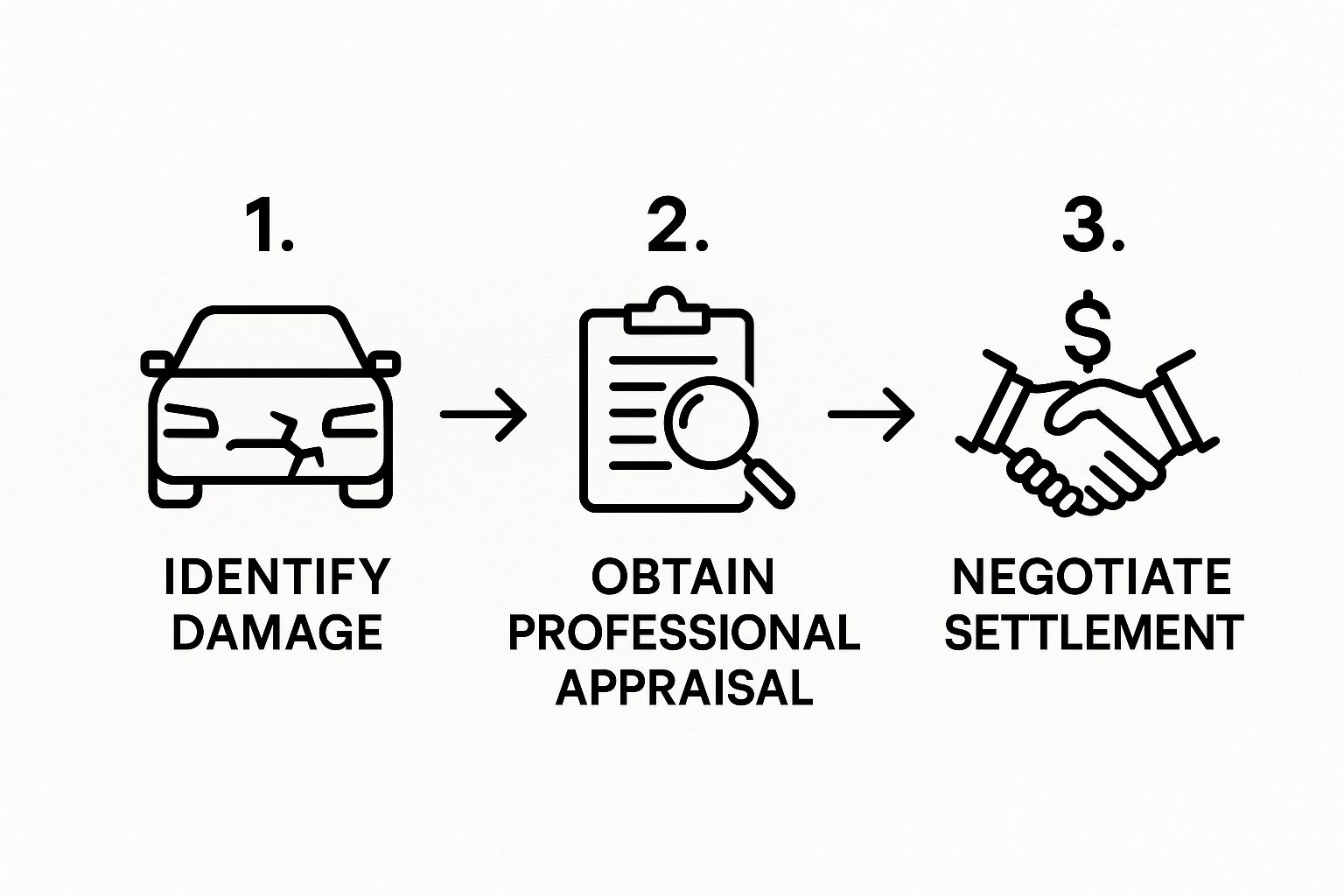

The process really boils down to three key stages: identifying your loss, proving it with a solid appraisal, and then successfully negotiating your settlement.

This roadmap shows that a winning claim is a logical progression. You’re not just arguing; you’re moving from the tangible damage on your car to a proven financial loss, and finally, to a fair resolution.

Engaging With the Insurance Adjuster

Once you send your demand letter, an insurance adjuster will be assigned to your case. It is absolutely critical to remember their job: to settle the claim for the least amount of money possible for their employer. This isn't a friendly chat; it's a business negotiation, pure and simple.

You need to be ready for their common tactics and objections. One of the first things you might hear about is the infamous "17c formula." Some insurers love this outdated method because it consistently spits out an artificially low number. It's a non-starter.

When the adjuster mentions their formula, don’t get drawn into a debate. Simply state that the 17c method is not a recognized appraisal standard and redirect them to your USPAP-compliant report. Let the expert analysis in your appraisal do the talking. Honestly, knowing how to deal with insurance adjusters is a skill that can make a huge difference in your final payout.

Key takeaway: Stay calm, be professional, and remain persistent. Document every single conversation with the adjuster—write down the date, time, and a summary of what was discussed. This paper trail is your best friend if things get difficult.

Mastering the Art of Negotiation

The back-and-forth is where most people get worn down. The adjuster will almost certainly start with a lowball offer, hoping you’ll get frustrated, take the quick money, and disappear. Don't fall for it.

Here’s a playbook for handling the most common pushback you'll get from insurance adjusters.

Navigating Insurer Objections and How to Respond

| Insurer's Objection | Your Fact-Based Response |

|---|---|

| "We don't pay for diminished value." | "That’s incorrect. Inherent diminished value is a recognized component of property damage in this state, and courts have consistently upheld it." |

| "Your car was repaired to pre-accident condition." | "The physical repairs are complete, but the vehicle now has a permanent accident history, which negatively impacts its market value. My appraisal documents this loss." |

| "We use the 17c formula, and it says your loss is only $X." | "The 17c formula is a generic, unaccepted calculation. My claim is based on a USPAP-compliant appraisal performed by a certified expert, which is the industry standard." |

| "Can you provide invoices from dealers saying they'd pay less?" | "Appraisers determine market value loss based on extensive market data, not by soliciting speculative quotes. My comprehensive report already proves the loss in value." |

Remember, your appraisal is your leverage. Use the specific data points—like local market comparisons or dealer quotes within the report—to shut down their arguments.

If the adjuster won't budge or negotiate in good faith, don't be afraid to politely ask to speak with their supervisor. A manager often has more authority and a different perspective on settling the claim to avoid further hassle.

Should you hit a total wall, your final options are filing a formal complaint with your state's Department of Insurance or, if necessary, taking the at-fault driver to small claims court. More often than not, the credible threat of escalating the issue is all it takes to bring the insurer back to the table with a much more reasonable offer.

Common Questions About Diminished Value Claims

https://www.youtube.com/embed/qkDiTlDCGe4

Even with a solid game plan for your diminished value claim, you’re going to have questions. That’s completely normal. Getting answers to the most frequent ones can help you sidestep common pitfalls and feel much more confident moving forward.

One of the first things people wonder is whether they can file a claim if the accident was their fault. In almost every situation, the answer is a hard no. Diminished value is considered a third-party claim, which means you’re claiming it against the at-fault driver's insurance, not your own. Your policy's collision coverage is there to fix your car, not to compensate you for its lost market value.

There is one major exception to this rule: Georgia. Drivers there can sometimes file a first-party claim, but for the rest of us, the only path is through the other driver's liability insurance.

Time Limits and Lowball Offers

Another question I hear all the time is about deadlines. Is there a time limit for filing? Absolutely. Your claim falls under your state's statute of limitations for property damage, which is usually somewhere between one to three years from the date of the accident. If you miss that window, your right to file is gone forever, no matter how solid your case is.

This is exactly why you need to get the ball rolling as soon as your repairs are done. Waiting too long is one of the easiest ways for an insurer to shut down your claim before they even glance at your evidence.

But what if you do everything right and the insurance company comes back with a ridiculously low offer? Don’t be surprised—it happens all the time.

Expert Insight: Never, ever accept the first offer, especially if it feels like an insult. This is a classic negotiation tactic they use to test you and see if you'll just give up. A low offer isn’t the end of the road; it's just the beginning of the conversation.

When you get that lowball offer, the key is to stay cool and get strategic. Here’s how you should handle it:

- Put it in Writing: Politely respond and restate your case. Reference your professional appraisal report and use the facts you've gathered to directly push back on their reasoning.

- Ask for a Supervisor: If the adjuster won't budge, calmly ask to speak with their manager. Supervisors often have more leeway to approve a higher settlement.

- File a Formal Complaint: Your next step is to file a complaint with your state's Department of Insurance. This official action usually gets the insurance company’s attention pretty quickly.

- Think About Small Claims Court: If all else fails and the amount is within your local court's limit, filing a lawsuit is your final move. Often, just the threat of legal action is enough to make the insurer come back with a much fairer offer.

At Total Loss Northwest, we specialize in providing certified, independent appraisals that give you the leverage you need to secure a fair settlement. If you're facing a diminished value or total loss situation, don't let the insurance company dictate what you're owed. Visit us at https://totallossnw.com to get the expert support you deserve.