When your car is damaged in an accident, one of the biggest financial hurdles is dealing with the insurance company's valuation. An independent car appraiser is the expert you bring to the table—a neutral, third-party professional whose only job is to determine your vehicle's true fair market value, completely separate from the insurance company's influence.

Think of them as your personal financial advocate, fighting to make sure you get every dollar you're rightfully owed.

Your Ally In Automotive Valuation

Here’s a simple analogy: if you were selling your house, you’d never let the buyer’s agent be the one to set the final price, right? You’d hire your own appraiser to get an objective, fair market value. An independent car appraiser does the exact same thing for your vehicle after a collision.

Their entire purpose is built on one simple but powerful word: independence. They have no skin in the game with any insurance company. This complete neutrality is what makes their work so valuable, as it cuts through the obvious conflict of interest that happens when an insurer has to value a claim they are responsible for paying.

To get a clearer picture of why this matters so much, let's compare the two side-by-side.

Independent Appraiser vs Insurance Appraiser At a Glance

The table below breaks down the key differences between the appraiser you hire and the one the insurance company uses. It highlights how their roles, motivations, and the final outcomes they produce can be worlds apart.

| Attribute | Independent Car Appraiser | Insurance Company Appraiser |

|---|---|---|

| Who They Work For | You, the vehicle owner. | The insurance company. |

| Primary Goal | To determine the vehicle's true, fair market value. | To assess the loss based on company guidelines, often aiming to minimize the payout. |

| Motivation | Accuracy and objectivity. Their reputation depends on it. | Efficiency and cost control for their employer. |

| Allegiance | To you and the factual evidence. | To the insurance carrier's financial interests and policies. |

| Valuation Method | Detailed physical inspection, deep local market analysis, and customized report. | Often relies on standardized software (e.g., CCC, Audatex) with generic market data. |

| Report Detail | Comprehensive, evidence-based document designed to stand up to scrutiny. | Typically a standardized, software-generated report with limited detail. |

As you can see, hiring an independent appraiser isn't just about getting a second opinion—it's about leveling the playing field with a professional who is 100% on your side.

How An Appraiser Determines Value

An independent appraiser’s process is a world away from the automated, one-size-fits-all software that insurers lean on. It’s a hands-on, meticulous investigation into what makes your specific vehicle unique.

Here's what that looks like in practice:

- Thorough Physical Inspection: They go over your vehicle with a fine-tooth comb, documenting its real-world condition. They look for things the software misses, like custom upgrades, exceptional maintenance history, or rare features that bump up its value.

- Hyper-Local Market Research: Instead of using a national database, they dig into your local market to find actual, recent sales of truly comparable vehicles. This ensures the valuation reflects what a buyer in your specific area would realistically pay.

- Comprehensive Documentation: All of this information is compiled into a robust, detailed report. This isn't just a number; it's a piece of evidence that lays out a compelling, fact-based case for your car's true worth.

This methodical approach is critical. Since appraisers often help people navigate complicated claims, having a solid foundation in understanding car insurance is a huge plus for any vehicle owner.

An appraiser's report isn't just an opinion; it's a fact-based argument for your vehicle's worth. It forces the insurance company to justify their lower offer against a detailed, evidence-backed valuation prepared by a certified professional.

Two Critical Scenarios For An Appraiser

While their expertise is valuable in many situations, an independent appraiser is an absolute game-changer in two specific claims scenarios where thousands of dollars are on the line.

- Total Loss Claims: The insurer declares your car a "total loss," but their settlement offer is way too low for you to buy a similar replacement vehicle. An appraiser builds a rock-solid case for a higher, fairer payout.

- Diminished Value Claims: Even after perfect repairs, your car is now worth less because it has an accident on its record. An appraiser calculates this loss in market value—known as diminished value—so you can claim that difference from the at-fault party's insurer.

Getting familiar with the appraisal process is your first step toward getting a fair settlement. You can learn more about how a professional vehicle appraisal works to protect your investment.

Securing a Fair Payout for a Total Loss

When the insurance company declares your car a "total loss," that first settlement offer can feel like a punch to the gut. It's almost always a lowball number, leaving you wondering how you're supposed to buy a similar car for that amount. There's a reason for this: insurers lean on massive, automated valuation systems designed for speed and volume, not for accuracy.

These systems pull data from huge regional, or even national, markets. They simply can't account for what makes your car special or what it's really worth in your specific town. This is where an independent car appraiser comes in. They provide a crucial reality check, shifting the process from a generic calculation to a detailed, hands-on investigation of your vehicle.

Uncovering Your Vehicle's True Worth

An independent appraiser’s entire job is to determine your car’s Actual Cash Value (ACV)—its fair market price the second before the crash happened. They don't just plug a VIN into a computer. They perform a deep dive into your specific vehicle and its standing in your local market.

This careful, methodical approach almost always finds value that the insurance company's software completely overlooks. For instance, did you just spend a grand on new premium tires? Did you upgrade the sound system? An appraiser documents these improvements and adds that value back where it belongs.

They also look for the little things that reflect how well you cared for the car:

- Exceptional Maintenance: A glovebox full of service records is hard proof of a well-maintained vehicle, and that's worth more money.

- Pristine Condition: If your car was garage-kept with immaculate paint and a spotless interior, that adds real value.

- Rare Features or Packages: A special trim level or a sought-after factory option can make your car much more desirable—and valuable—to a potential buyer.

A total loss settlement isn't about what some software algorithm decides. It's about what a real person in your local area would have actually paid for your car. An independent appraisal is the only way to establish that true figure.

The Power of Local Market Data

Maybe the biggest game-changer an independent appraiser offers is their focus on your local market. An insurer’s report might pull "comparable" vehicles from hundreds of miles away, but a true expert finds cars for sale and recently sold right in your community. This is absolutely critical. A popular truck in rural Washington, for example, might be worth significantly more than the same model in downtown Portland.

This local evidence creates a powerful, fact-based argument you can take back to the insurance company. It’s no longer your word against their computer; it's a detailed, professional report against a generic printout. With repair costs and vehicle technology on the rise, more cars are being totaled out than ever. An appraiser who understands these dynamics is essential, and you can learn more about how market conditions affect total loss appraisals to see just how deep it goes.

By building a case piece by piece, an independent car appraiser forces the insurer to defend their lowball offer against real-world data. It puts you in the driver's seat during negotiations and helps you get the fair settlement you’re owed.

Recovering Your Car's Diminished Value

Even after the best body shop works its magic, a car with an accident on its record is worth less than an identical one without. This hit to your car’s market price is called diminished value. It's a very real financial loss, but one that insurance companies almost never volunteer to pay for.

Let's put it in practical terms. Imagine you're shopping for a used truck. You find two identical models, same year, same mileage. The only difference? One has a documented history of a major collision. Which one are you going to pay top dollar for? The answer is obvious, and that price gap is the diminished value your car now has to live with.

This isn't just about a few lingering scratches. The accident stigma alone creates doubt for future buyers. They'll wonder about the car's structural integrity and long-term reliability, forcing you to slash the asking price when you eventually sell.

Proving an Invisible Loss

The real challenge with a diminished value claim is that the loss is invisible. You can't point to it like you can a dented bumper. This is exactly why insurers often push back on these claims—they bank on the fact that it's tough for the average car owner to prove and calculate.

This is where an independent car appraiser becomes your most powerful ally. These experts specialize in turning that "invisible" loss into a solid, evidence-backed number. They know exactly how to analyze the market and the specific details of your situation.

They'll look at several key factors:

- Severity of Damage: Was it a minor parking lot scrape or a major frame-bending collision?

- Vehicle Age and Value: A newer, more expensive car will lose a much bigger chunk of its value than an older, high-mileage vehicle.

- Quality of Repairs: The skill and thoroughness of the shop's work matter. The quality auto repair services a car receives post-accident directly influences its final market value.

- Accident History Reporting: The moment that accident hits a vehicle history report like CarFax, its value takes an immediate nosedive.

A diminished value claim isn't about getting a bonus payout. It’s about being made whole again by recovering the true market value that was stripped from your property because of someone else's mistake.

A good independent appraiser pulls all of this information together into a detailed, professional report. This document gives you a clear, justifiable calculation of the exact dollar amount your car has lost. It’s the ammunition you need to file a successful claim with the at-fault driver's insurance company.

Without that expert analysis, you're just guessing—and likely leaving thousands of dollars on the table.

How to Find the Right Independent Appraiser

https://www.youtube.com/embed/5JnVFJtBLwA

Deciding to hire an independent appraiser is the first step. The next, and arguably more important, is choosing the right one. Not all appraisers have the same level of skill or experience, and the outcome of your claim hinges on finding a pro whose work can hold up under an insurance company's microscope.

You're not just looking for a certified appraiser; you're looking for an advocate for accuracy.

Think of it this way: you wouldn't ask your family doctor to perform open-heart surgery. You'd want a specialist. The same logic applies here. You need an independent car appraiser with a deep, proven track record in the specific type of claim you have—whether that’s a total loss or diminished value.

Vetting Your Appraiser Checklist

Before you sign on the dotted line, you have to do your homework. A few pointed questions can quickly tell you if you're talking to a seasoned expert or someone who just got their certification last week. This checklist will help you make a smart, confident choice.

Here are the key things to dig into:

- Industry Certifications: Credentials from respected organizations like I-CAR (Inter-Industry Conference on Auto Collision Repair) or ASE (Automotive Service Excellence) are a great sign. They show a real commitment to professional standards and staying current.

- Specific Experience: Don't be shy—ask them directly how many total loss or diminished value claims they’ve handled. It also helps if they have experience with your car's make and model. An appraiser who works mostly with modern Hondas might not be the best fit for your classic Porsche.

- Sample Reports: Ask to see a redacted sample report. This is your window into their work. Is it detailed? Is it professional? Does it back up its claims with solid market data and clear evidence? A flimsy report won't get you far.

This simple vetting process helps ensure you're teaming up with someone who truly has your back. For anyone just starting their search, finding a qualified independent auto appraiser near me is the perfect first step to getting a truly professional evaluation.

Key Questions to Ask and Red Flags to Avoid

Once you have a couple of candidates, a quick phone call can tell you everything. A good appraiser will be upfront and transparent, happy to walk you through their process and explain their fees without any hesitation.

Make sure you ask how they find comparable vehicles, what standards their reports adhere to, and how they structure their fees. A flat fee is the industry standard. A professional independent car appraiser will never, ever charge a percentage of your settlement—that's a massive conflict of interest.

The biggest red flag of all? An appraiser who guarantees a specific outcome or settlement amount. A true expert can only promise to deliver an accurate, unbiased, and evidence-based valuation. They can't promise a magic number.

The car market is always changing, which impacts vehicle values and the need for skilled appraisers, especially as total loss claims become more frequent. This makes the appraiser's job of establishing a fair value for classic, custom, or even just well-maintained cars more critical than ever. Taking the time to properly vet your appraiser is how you hire a true professional who can effectively fight for what you're rightfully owed.

What to Expect: A Step-by-Step Look at the Appraisal Process

So, you've decided to hire an independent appraiser. It might seem like a daunting step, but the process is actually straightforward and methodical. It’s all about building an ironclad case for your vehicle's true value, piece by piece.

Think of it less as a simple look-over and more as a forensic investigation. It starts with a fact-finding mission, moves to a hands-on inspection, and ends with a powerful, evidence-based report that an insurance company can't just ignore. Each stage builds on the last, creating a complete and accurate picture of your car's pre-accident worth.

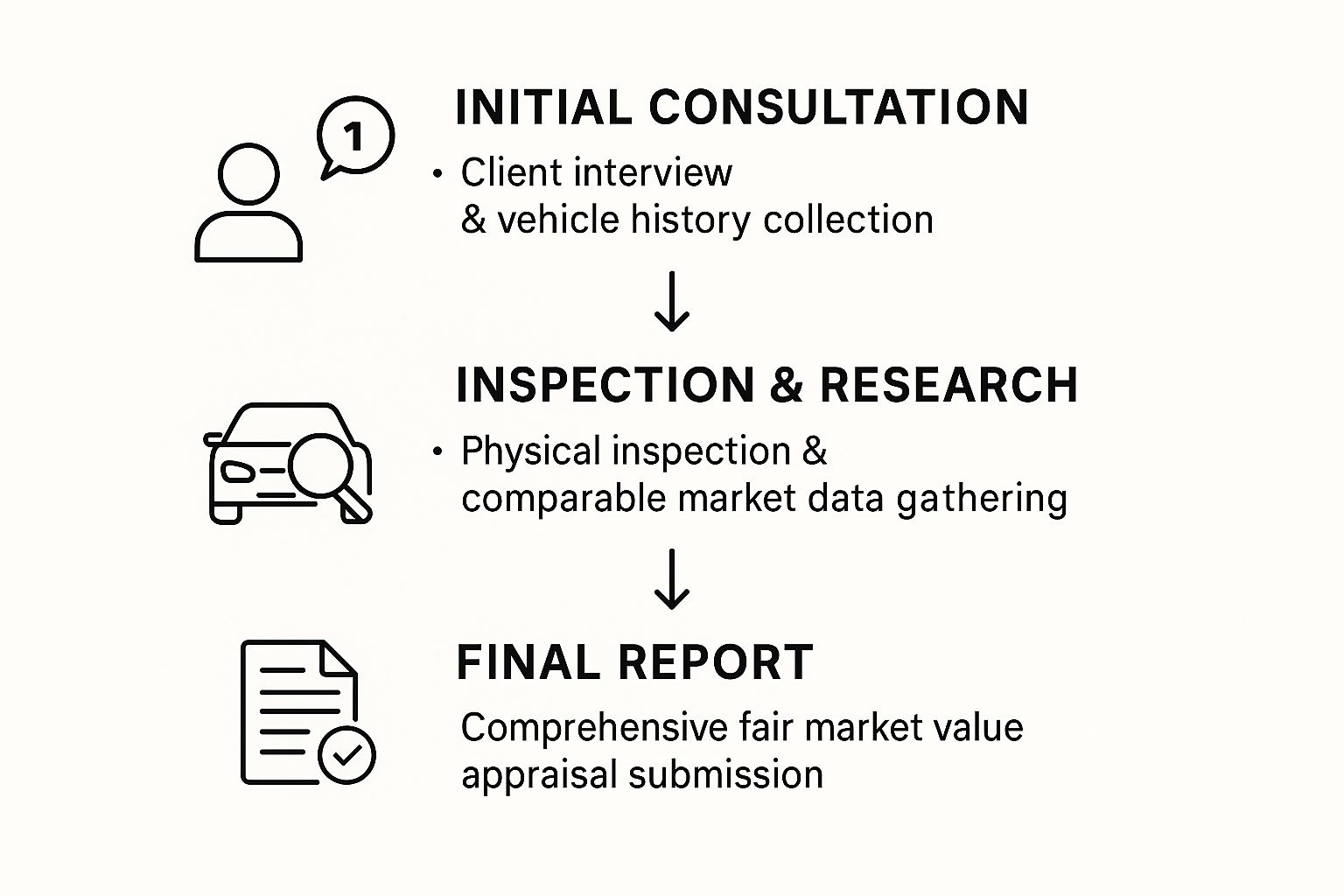

This infographic breaks down the core stages you'll go through, from that first phone call to the final report.

As you can see, a real appraisal isn't a quick glance. It's a detailed analysis that pulls together your story, the physical evidence from the car, and hard data from the market.

Step 1: The Initial Consultation and Document Roundup

Your journey starts with an in-depth consultation. This is where a good appraiser puts on their detective hat to gather the preliminary evidence. You’ll talk through the accident, the insurer's lowball offer, and anything special about your vehicle that makes it unique.

To get started, you'll need to pull together a few key documents:

- The insurance company’s valuation report (the one you're challenging)

- The official police report from the accident

- All repair estimates and invoices

- Maintenance records for your vehicle

- Any photos you have of the car before and after the collision

This initial step is crucial. It gives your appraiser the full story and context before they even lay eyes on your car, helping them zero in on exactly where the insurance company's valuation went wrong.

Step 2: The Hands-On Inspection and Market Deep Dive

Next up is the most critical part: the physical inspection. Your appraiser will go over your vehicle with a fine-tooth comb, documenting its pre-accident condition, every factory option, and any upgrades you’ve made. This is where they find the value that automated systems always miss—things like brand-new tires, a high-end stereo, or pristine interior condition.

At the same time, they'll be conducting deep, hyper-local market research. They won't just pull data from some generic national database. A true pro finds real, comparable vehicles—often called "comps"—that recently sold or are for sale right in your area. This local focus is non-negotiable, as a car's value can swing wildly from one city to the next.

The whole point is to figure out what a real person in your local market would have paid for your exact car a moment before it was hit. That means finding comps that are true apples-to-apples comparisons, not just a similar model listed 300 miles away.

Step 3: Crafting and Submitting the Report

Finally, the appraiser pulls all this information together into a comprehensive, multi-page report. This isn't just a number on a page; it's a detailed, evidence-backed argument for your car's value.

The report breaks down the vehicle's condition, lists its features, presents the local market comps, and provides a clear, justifiable fair market value. It becomes your single most powerful tool for negotiation. This professional document is then submitted to the insurance company, officially challenging their number and, if needed, invoking your policy's Appraisal Clause.

To see how these reports function in a formal dispute, you can learn more about their role in auto insurance appraisals. This is the step that flips the script, forcing the insurer to defend their low offer against a much more accurate, data-driven valuation.

Got Questions? We’ve Got Answers.

Dealing with a car accident is stressful enough. The last thing you need is to feel like you’re getting a raw deal from your insurance company. Let’s clear up some of the most common questions people have when they first think about hiring an independent appraiser.

What’s This Going to Cost Me?

You can expect an independent appraisal to cost somewhere between $300 and $700. The exact price tag really depends on what kind of vehicle you have, how complicated the claim is (a total loss is different from a diminished value case), and even where you live.

A quick word of advice: any appraiser worth their salt will charge a simple flat fee. If someone asks for a percentage of your settlement, run the other way—that’s a huge conflict of interest. Think of it as an upfront investment, because a good appraisal can boost your payout by thousands, easily covering its own cost and then some.

When Does It Make Sense to Hire an Appraiser?

Hiring an expert is a no-brainer in a couple of key situations. If the insurance company’s offer for your totaled car feels shockingly low—we're talking thousands less than what you see similar cars selling for—it’s time to call in a pro. The same goes for diminished value claims, especially if you have a newer, high-end vehicle that needed significant repairs.

Here’s a simple way to look at it: if the difference between the insurer's offer and your car's true value is big enough to pay for the appraisal several times over, you should do it.

On the flip side, if you’re dealing with a minor fender-bender on an older car with tons of miles, the cost of the appraisal might not be worth the potential payout.

Can I Get an Appraisal for My Leased or Financed Car?

Absolutely. In fact, for leased or financed cars, it's often even more important.

When your car is totaled, the insurance payout needs to be enough to settle your loan or lease. If the insurer’s offer comes up short, you’re on the hook for that “gap” unless you have gap insurance. You could end up owing money on a car you can’t even drive anymore.

An independent car appraiser makes sure the settlement reflects what your car was actually worth (its ACV). This is your best tool for ensuring the insurance check is big enough to pay off the lender, protecting you from a nasty financial surprise.

If you're staring at a lowball settlement offer or need to prove your car has lost value, don't just accept it. The certified experts at Total Loss Northwest are here to fight for the fair, accurate payout you deserve. Visit us online to start your claim.