You're probably dealing with this right now. The tow truck has left, your car is sitting at a yard or body shop, your phone is full of missed calls, and the insurance company sounds calm enough that you're tempted to assume they'll sort it out fairly.

That's the moment many people lose money.

An auto claim isn't just paperwork. It's a valuation fight. If the carrier has thin documentation, they can lean on assumptions, generic condition adjustments, incomplete repair logic, or software outputs that don't reflect your vehicle's real market value. If you have a tight file, they have less room to do that.

For everyday drivers, that matters after any collision. For total loss and diminished value claims, it matters even more. Those claims often turn on details individuals overlook preserving until it's too late.

Why Your Insurance Claim Documentation Is Crucial

Insurance claim documentation is the difference between a story and a provable claim. After a crash, it's often thought that the key step is reporting the accident fast. Reporting matters, but proof provides the advantage.

The carrier's job is to evaluate exposure and close the file. Your job is to show what was lost, what the vehicle was worth before the collision, what happened to its value after the collision, and where the insurer's numbers fall short. If you don't document that well, you're left arguing from memory while the adjuster argues from a file.

That's why documentation isn't bureaucratic busywork. It's your negotiating position.

The broader claims world works this way too. The Insurance Information Institute notes that the overwhelming majority of property claims depend on accurate photos, inventories, repair estimates, and cause-of-loss records, and that in auto claims, total loss and diminished-value disputes often turn on valuation records and proof that the vehicle's pre-loss condition was better than the insurer's first estimate suggests, as explained in the III homeowners and renters insurance facts.

What insurers do with weak files

A weak file gives the insurer room to:

- Question condition: If you don't have service records, prior photos, or upgrade receipts, they can treat your vehicle like an average example instead of a well-kept one.

- Rely on incomplete comparables: If their market comps are poor and you don't challenge them with better comps, their report becomes the default.

- Downplay repair impact: In a diminished value claim, missing repair details make it easier for them to minimize stigma and resale loss.

- Stretch the timeline: Every missing item creates another request, another review, and another delay.

Practical rule: If it isn't documented, expect the insurer to treat it as disputed, uncertain, or irrelevant.

The real objective

A fair claim file does one thing. It turns subjective disagreement into documented disagreement.

That's the point. You're not trying to sound convincing. You're building a file that forces the insurer to deal with facts.

What to Document Immediately After an Accident

The first 24 hours matter because they produce the cleanest evidence you'll ever have. Fresh scene photos, vehicle position, debris, weather, roadway markings, and visible impact damage are much harder to dispute than a description given days later.

Around 25% of claim disputes happen because of a lack of proper evidence, and 22% stem from delays in claim processing, according to these insurance claim statistics. Early documentation helps on both fronts.

What to capture at the scene

Start with wide shots before close-ups. The goal is to preserve context first, then detail.

- Overall scene photos: Get the vehicles in final position, lane markings, intersections, traffic controls, shoulder position, and surrounding area.

- All vehicle damage: Photograph each damaged area from multiple angles. Then step back and show where that damage sits on the vehicle as a whole.

- The other vehicle: Capture plate, VIN if visible, make, model, and damage pattern.

- Road conditions: Include skid marks, debris, fluid trails, broken parts, potholes, standing water, ice, gravel, and visibility conditions.

- Signs and landmarks: Street signs, mile markers, business fronts, and traffic lights help lock the location down.

- Interior details if relevant: Airbag deployment, seatbelt marks, dash warnings, and odometer reading can all matter later.

If your phone timestamps images automatically, keep that setting on. Don't edit originals. Save copies if you need to crop or label them.

What to collect before you leave

You don't need a perfect investigation at the roadside, but you do need the basics.

- Police report number

- Other driver's insurance and contact information

- Witness names and contact details

- Tow destination and storage yard information

- Any immediate medical evaluation records if you were checked at the scene or shortly after

For a more detailed post-crash action plan, review these steps after a car accident.

Don't fill the silence by guessing. If someone asks what happened and you're unsure, say you're still gathering facts.

What not to say

This part matters more than is often realized.

Don't admit fault. Don't speculate about speed, distance, visibility, or injuries. Don't say you're “fine” if you haven't been evaluated. Don't tell the insurer what repairs should cost, what the car is worth, or whether it's probably a total loss.

Stick to observable facts:

- where you were

- what direction you were traveling

- what you saw

- what made contact

- what damage is visible

Later in the claim, the same rule applies. Observations carry weight. Opinions invite pushback.

A short visual guide can help if you're overwhelmed in the moment:

Your Complete Auto Claim Documentation Checklist

Once the scene is over, your job changes. Now you're building a file that can survive review by an adjuster, supervisor, appraiser, or attorney. Weak files fail for predictable reasons. Industry sources cite denial rates as high as 15%–20% in settings with poor documentation, with incomplete records and inconsistent information being common triggers, as outlined in this guide on avoiding common claims errors.

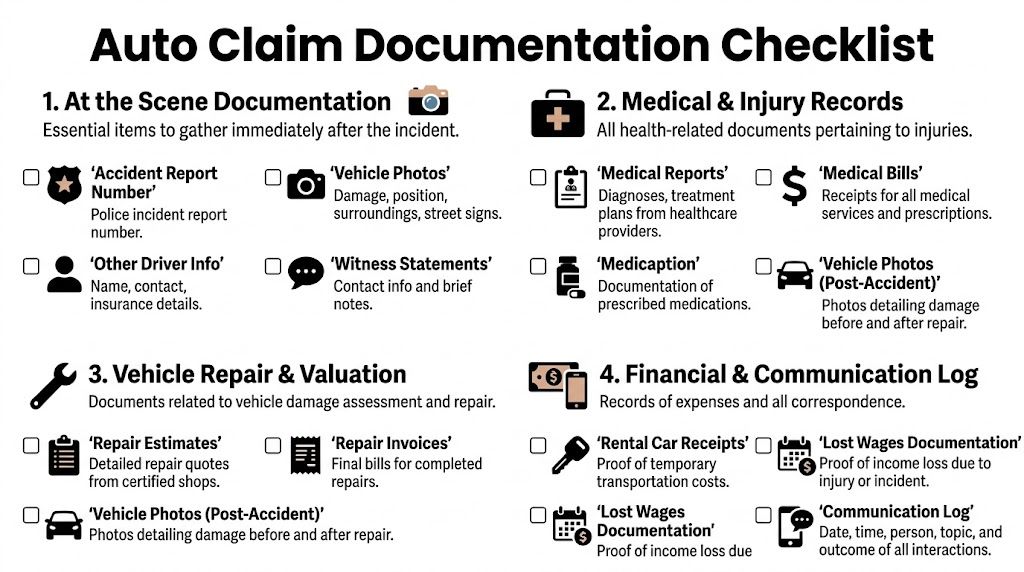

Ownership and policy records

These documents establish that you have the right to pursue the claim and identify who has an interest in the vehicle.

- Registration and title paperwork: Clear proof of ownership matters in total loss claims.

- Lienholder or lease information: If a lender is involved, payoff documents become part of settlement handling.

- Declarations page or claim assignment details: Keep the policy information tied to the file.

A weak version is a blurry phone photo with half the page cut off. A strong version is a clean scan or clear image with every identifier legible.

Damage and repair records

This is the core of most auto claims. The insurer will build its repair or valuation position from this material, whether you provide it or not. Better that you control it.

- Accident scene photos and walkaround photos

- Body shop estimates

- Supplement estimates

- Final repair invoice if repairs were completed

- Parts lists showing OEM, aftermarket, or recycled parts if relevant

Good estimates are itemized. They show line items, labor operations, part descriptions, refinish steps, scan or calibration charges where applicable, and shop identity. A one-line total is weak because it gives the insurer almost nothing to evaluate beyond price.

If your shop doesn't give you a clean invoice or receipt trail, a customizable auto service receipt can help you understand the information that should be captured and preserved in your file.

Pre-accident condition proof

Many owners fall short, particularly in total loss and diminished value disputes. The insurer may treat your car as ordinary unless you prove otherwise.

Consider gathering:

- Service records: Oil changes, major maintenance, dealer service visits, recent mechanical work.

- Tire and brake receipts: These help show recent upkeep.

- Photos from before the crash: Marketplace listings, social posts, detailing photos, or sale prep photos can all help if they clearly predate the loss.

- Upgrade receipts: Wheels, suspension, audio, protective film, specialty trim, towing equipment, or performance parts.

- Window sticker or build sheet if available: Useful for options packages and trim accuracy.

A clean service history doesn't just show maintenance. It helps counter any quiet assumption that your vehicle should be valued below market because it was neglected.

Expense and loss records

These documents often get scattered across email, glove boxes, text messages, and shop counters.

Keep:

- Tow bills

- Storage invoices

- Rental receipts

- Ride-share or temporary transportation receipts if tied to the loss

- Personal property loss notes if items in the vehicle were damaged

- Medical visit records if your claim involves injury-related vehicle issues or timeline disputes

A simple file standard

Use this test before submitting anything:

| Item | Strong version | Weak version |

|---|---|---|

| Photos | Dated, clear, multiple angles, scene plus close-ups | Blurry, cropped, random order |

| Estimates | Itemized and shop-branded | Lump sum with no parts detail |

| Service history | Chronological and identifiable to VIN | Loose receipts with no vehicle info |

| Ownership records | Full-page, legible copies | Partial screenshots |

| Expenses | Dated receipts tied to the claim | Verbal recollection only |

How to Organize Your Claim and Log Communications

A strong claim file isn't just complete. It's usable. Adjusters deal with fragmented information all the time, and fragmented files create delay, confusion, and room for the carrier to keep asking for “just one more thing.”

A well-structured workflow involves timestamping every contact and evidence upload, distinguishing observations from interpretations, and keeping a running chronology. Missing communication logs are repeatedly cited as causes of claim denial or negotiation weakness, according to ClaimWizard's discussion of documentation mistakes.

Build a claim folder like a case file

Don't keep this scattered across your camera roll, text messages, and downloads folder. Create one master folder, then split it into subfolders such as:

- 01 Scene photos

- 02 Vehicle photos after tow

- 03 Estimates and invoices

- 04 Ownership and policy

- 05 Service records

- 06 Communications

- 07 Rental and out-of-pocket expenses

- 08 Valuation and comparable vehicles

That structure does two things. It helps you respond fast, and it signals that you're organized. That changes how many adjusters handle the file.

Keep a communication log

This is one of the most underused parts of insurance claim documentation.

For every call, email, text, or portal message, log:

- Date and time

- Name and role of the person

- Phone number or email if available

- What was discussed

- What the insurer requested

- What you sent

- Any deadlines or promises made

Use plain language. “Adjuster stated valuation report would be sent by Friday.” That's better than “They were difficult and evasive.”

If you want a cleaner way to track receipts and claim-related spending alongside your log, tools focused on digital records can help. This overview of Snyp for efficient expense tracking is useful for keeping scattered expenses from slipping out of the file.

Separate fact from argument

This matters when you write emails and upload notes.

| Write this | Not this |

|---|---|

| “Rear bumper cover is torn and detached on passenger side.” | “The insurer is obviously undervaluing severe damage.” |

| “Vehicle had recent tire replacement. Receipt attached.” | “This car was basically perfect.” |

| “Requested corrected comparable vehicles due to trim mismatch.” | “Your report is ridiculous.” |

Organized claimants get taken more seriously because their file is easier to defend, easier to escalate, and harder to dismiss.

If you're already dealing with a difficult adjuster, these practical notes on how to deal with insurance adjusters will help you stay factual without giving up ground.

Use follow-up emails strategically

After a phone call, send a short summary email. Keep it neutral.

Example:

- claim number

- date of loss

- what was discussed

- what documents you attached

- what you're waiting on next

That follow-up turns a conversation into a record. If the file later moves to a supervisor, appraiser, or legal review, those emails matter.

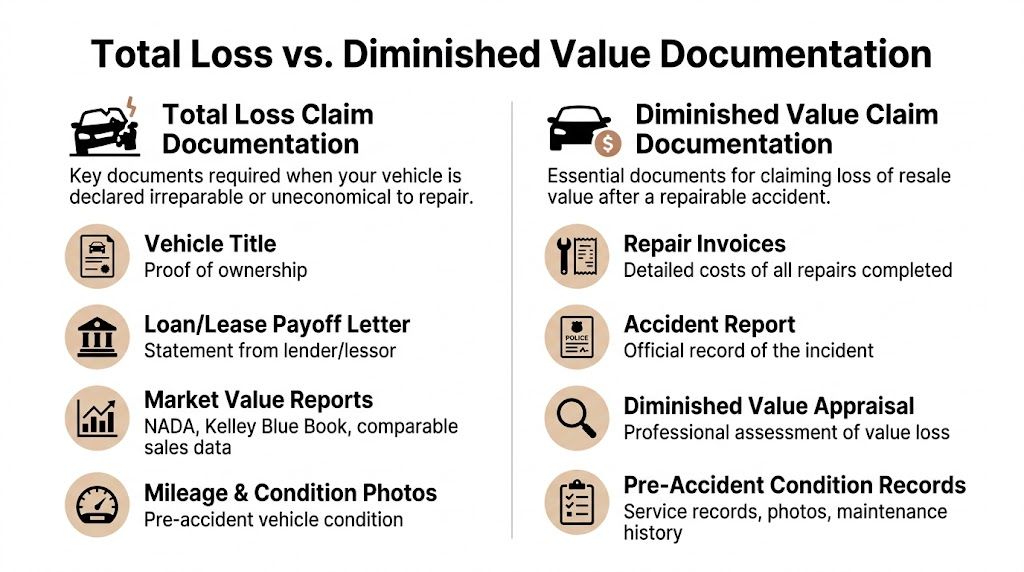

Documentation for Total Loss and Diminished Value

Two owners can have the same vehicle, the same damage, and very different outcomes. The one with clean proof of condition, options, prior care, and repair impact usually has a better chance of pushing back when the insurer comes in low. The one with gaps in the file often gets told the carrier's number is “supported.”

That is the fundamental difference in total loss and diminished value claims. The fight is over value, and insurers know exactly where weak documentation gives them room to cut it.

What changes in a total loss claim

A total loss claim turns on actual cash value. The carrier usually builds that number from comparable vehicles, trim and option codes, mileage, condition adjustments, and its reading of the local market.

That process sounds objective. It often is not.

I regularly see valuation reports built on the wrong trim, missing packages, weak comparable vehicles, or condition deductions that do not match how the vehicle was maintained. Specialty vehicles, enthusiast builds, and well-kept older cars get flattened into generic categories all the time. Once that happens, the burden shifts to you to show why their report is wrong.

A solid total loss file usually includes:

- title and registration

- lien payoff information, if financed

- pre-loss photos from multiple angles

- maintenance records

- receipts for recent major work, tires, brakes, battery, and upgrades

- proof of factory and added options

- independent comparable listings that match your vehicle

- the carrier's valuation report with specific errors identified

What changes in a diminished value claim

Diminished value is the loss in market value after proper repairs. The car may be fixed, but the accident history still affects what buyers will pay.

That means your file has to prove market impact, not just damage. A useful starting point is understanding how an automobile diminished value claim works and what evidence tends to hold up when the carrier argues the loss is minimal.

The strongest diminished value files show four things clearly:

- the vehicle had strong pre-loss condition

- the damage was significant enough to matter to a future buyer

- the repair involved items that affect buyer confidence, such as structural work, panel replacement, paintwork, calibrations, or safety systems

- the insurer's number does not reflect real resale resistance in the market

How insurers use documentation gaps to reduce payouts

Basic checklists are insufficient. A missing record is not just an oversight. It gives the insurer a place to stand.

In a total loss claim, missing service history can support an “average” condition rating instead of above average. No proof of options can strip real value out of the report. Weak pre-loss photos make it easier for the carrier to defend condition deductions, prior damage assumptions, or generic comparable selections.

In a diminished value claim, the pattern is just as predictable. If the repair invoice is vague, they argue the damage was minor. If there are no calibration records, frame measurements, or parts details, they downplay the seriousness of the repairs. If you cannot show pre-accident condition, they suggest the car already had resale weaknesses.

Insurers do not need a perfect argument. They need enough uncertainty to keep their number alive.

This same documentation discipline shows up in other property claims too. The process behind filing your home insurance claim relies on the same principle. Gaps in the record usually help the carrier, not the policyholder.

Why the Appraisal Clause matters in Washington and Oregon

Vehicle owners in Washington and Oregon often spend weeks arguing with an adjuster as if the adjuster is the final word on value. In many cases, that is the wrong fight.

If the dispute is about value, the Appraisal Clause may give you a direct path to challenge the number. You hire your appraiser. The insurer hires its appraiser. If they cannot agree, an umpire decides the remaining value dispute based on the evidence. That changes the setting from internal carrier review to a structured valuation process.

For total loss and diminished value cases, that matters. A well-documented file becomes more than a stack of attachments. It becomes evidence that can be applied in appraisal, where bad comparable vehicles, wrong option coding, and unsupported deductions are easier to expose.

One option in that process is Total Loss Northwest, which handles total loss and diminished value appraisals and invokes the Appraisal Clause for vehicle owners dealing with disputed valuations.

Submitting Your Claim and Protecting Your Rights

When your file is ready, submit it as a package, not as a drip of random attachments over two weeks. Send a short cover email that identifies the claim number, date of loss, vehicle, and what the documents support. Then attach or link the materials in organized folders.

Make it easy for the adjuster to review:

- label files clearly

- name photos by subject

- group estimates together

- include a short index if the file is large

- state what you want reviewed and why

That last point matters. Don't just send documents. State the issue. If the valuation report used the wrong trim, say so. If your repair invoice shows more serious damage than the carrier acknowledged, say so. If the total loss offer ignores recent maintenance and options, identify those items specifically.

Don't mistake the first offer for the correct offer

The insurer's first number is an offer. It is not a verdict.

If the file is incomplete, the carrier has room to stay low. If the file is organized, supported, and tied to real evidence, your position improves. If they still won't move and the dispute is about value, that's when you stop repeating yourself and start using the rights built into the policy.

A note on broader claim discipline

The same principles show up outside auto claims too. If you've ever dealt with property damage, this guide on filing your home insurance claim is a useful reminder that organized evidence, prompt reporting, and a clean paper trail matter across insurance lines.

Your leverage comes from records, chronology, and proof. Not frustration, not repetition, and not assuming the carrier will fix its own undervaluation.

If you're facing a low total loss offer or a brushed-off diminished value claim, don't treat that as the end of the process. Treat it as the point where the documentation either starts working for you, or exposes where you still need stronger evidence.

If you're in Washington or Oregon and the insurer's total loss or diminished value number doesn't match market value, Total Loss Northwest can review the documentation, identify valuation gaps, and help you use the Appraisal Clause to challenge a low offer with independent market-based evidence.