The moments right after a collision are a blur of adrenaline and confusion. It's completely understandable. But what you do in those first 15 minutes on the side of the road can make or break your insurance claim. This is where the battle for a fair settlement truly begins, long before you ever file a single piece of paperwork.

What to Do Immediately After a Car Accident

It’s hard to think straight when you’re shaken up, but your actions at the scene are about more than just safety—they're about collecting the raw evidence that will build your case. Think of yourself as the first investigator on the scene, because that's exactly what you are.

Your smartphone is your single most powerful tool in this situation. Don't rely on memory or the other driver's version of events. Your goal is to create a crystal-clear record of what happened.

On-Scene Documentation and Safety

First things first: check on everyone involved. If the cars are still in a traffic lane and can be moved, carefully guide them to the shoulder. Once you're out of harm's way, call 911 immediately.

A police report is non-negotiable. I've seen countless claims turn into a messy "he said, she said" nightmare simply because no official report was filed. The officer's report provides an objective, third-party account that insurance companies have a hard time ignoring.

While you wait for law enforcement, get to work. Use your phone to take more photos and videos than you think you need.

- Start with wide shots of the entire scene from multiple angles. Capture the road, any traffic signs or signals, and skid marks.

- Document the final resting position of all vehicles before they are moved.

- Then, move in for the details. Get close-up photos of the damage to your car and the other vehicle(s). Don't forget to photograph their license plate.

A Word of Caution from Experience: The absolute worst thing you can do is apologize or say anything that could be interpreted as admitting fault. Phrases like "I'm so sorry" or "I just didn't see you" will be used against you by an adjuster. Stick to the facts and exchange information. That's it.

The goal is to gather undeniable proof of the circumstances. To make this easier, here's a quick-reference checklist for what to collect at the scene.

On-Scene Evidence Collection Checklist

This table breaks down exactly what you need to grab at the scene and, more importantly, why it's so critical for your claim.

| Item to Collect | Why It's Critical | Insider Tip |

|---|---|---|

| Other Driver's Info | Name, address, phone, license number, insurance company, and policy number. | This is non-negotiable for filing a claim against the at-fault party. |

| Photos & Videos | Captures unbiased evidence of damage, position, and road conditions. | Narrate your videos. State the date, time, and location, and describe what you are recording. |

| Witness Information | Contact info for anyone who saw the accident. | Independent witnesses are incredibly valuable and can counter a false narrative from the other driver. |

| Police Report Number | The official record of the incident. | Ask the responding officer for their name, badge number, and the report number before they leave. |

Having this information neatly organized will give you a major head start and show the insurance company you are prepared and serious.

Taking these steps systematically ensures you don't miss any evidence that could be vital later on. This initial effort directly translates into leverage when it's time to negotiate. For an even more thorough guide, you can review the immediate steps after a car accident in our comprehensive walkthrough.

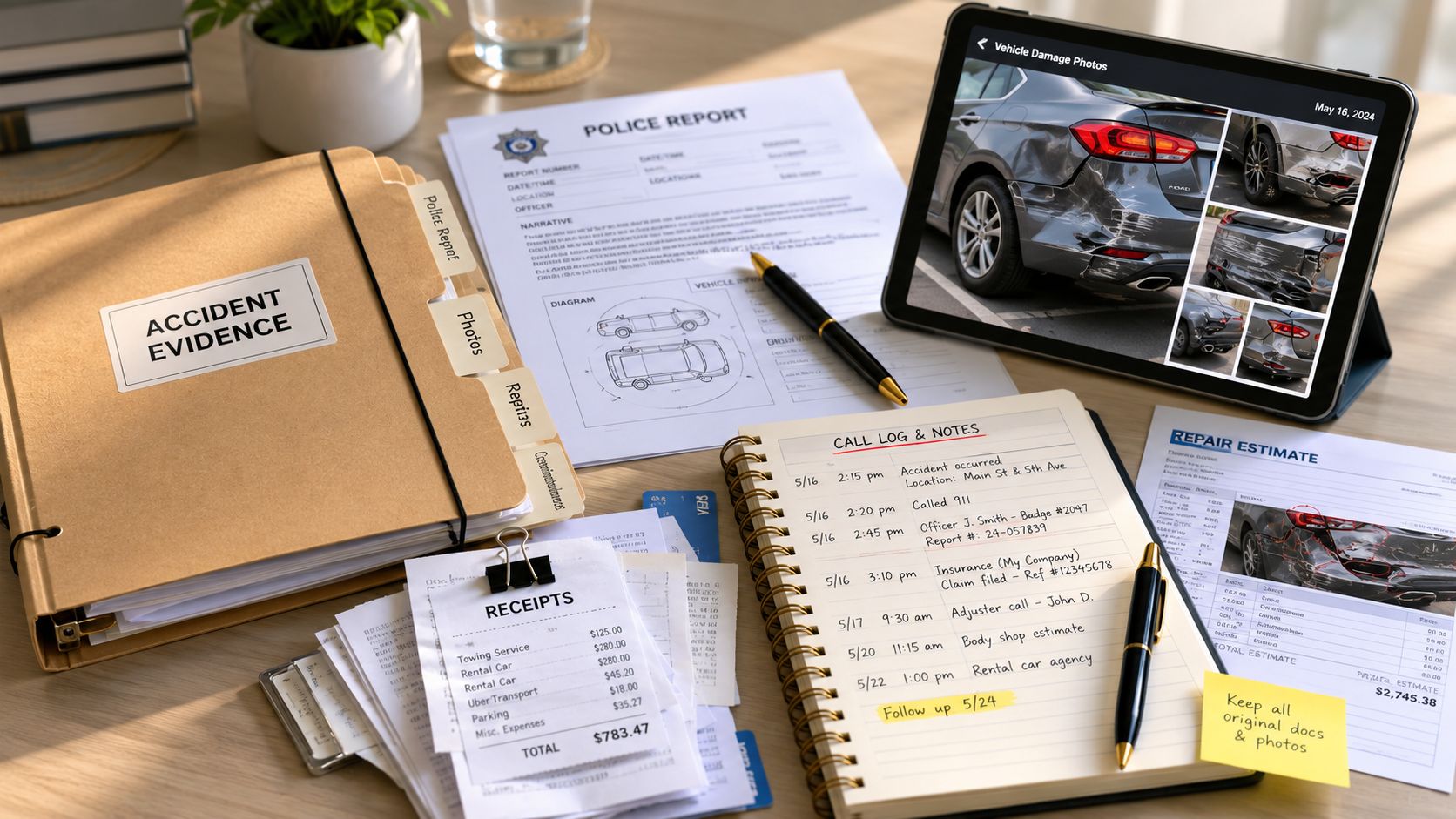

Building Your Evidence File for a Stronger Claim

Once you’ve alerted the insurance company, their adjuster gets to work. From this moment on, your job is to build an evidence file so thorough that it answers questions before the adjuster even thinks to ask them. We're not just talking about getting a few repair quotes; this is about getting the comprehensive insurance claim support you deserve.

Think of yourself as the lead investigator of your own claim. Get a dedicated folder—a physical one or a digital one on your computer—and make it the home for every single document, photo, and receipt. This includes the police report, all the pictures and videos you took at the scene, and any estimates you’ve gathered so far.

This isn’t about picking a fight with the insurer. It’s about being meticulously prepared. When you proactively assemble a rock-solid case, you change the dynamic. You’re no longer just a claimant passively waiting for an offer; you’re an informed owner, ready to negotiate from a position of undeniable strength.

Document Every Interaction and Expense

I can't stress this enough: keep a detailed log of every single conversation you have with the insurance company. Note the date, the time, who you spoke with, and a quick summary of the discussion. Honestly, an email is always better than a phone call because it creates an automatic paper trail.

I’ve seen it happen countless times. An adjuster might agree to something on the phone—like using only OEM parts—and then later claim to have no memory of it. A simple follow-up email (“Hi Jane, just wanted to confirm our conversation about the necessity of OEM parts for the repair…”) creates a written record they simply can't dispute.

You also have to track every dollar you spend because of the accident. These aren't just inconveniences; they are real, recoverable losses. Your list should include:

- Rental car fees

- Towing and storage charges

- Costs for public transport or rideshares

- Any other out-of-pocket expenses you have because your vehicle is out of commission

Building a strong evidence file is all about knowing how to prove your losses accurately. This principle is a cornerstone of assessing insurance claim losses and is just as true for a car as it is for anything else.

Don't forget that the average collision claim has risen sharply. Insurers are relying more on automated systems and algorithms to process claims quickly. Your own detailed, human-gathered documentation is your most powerful tool for challenging a lowball valuation that overlooks the real-world details of your specific situation. It's wise to understand the broader trends by reviewing current auto insurance statistics so you know what you're up against.

How to Challenge a Low Settlement or Total Loss Offer

Getting that first offer from the insurance company can feel like a punch to the gut. Whether it's for repairs, your vehicle's diminished value, or a total loss, the number is almost always lower than you expected. Don't panic. This is standard operating procedure, and it’s the starting point of the negotiation, not the end.

The adjuster’s initial figure is rarely personal; it's business. They often use standardized valuation software that simply can't account for the unique aspects of your vehicle—things like its pristine condition, recent upgrades, or a desirable options package. The goal is to close the claim quickly and cheaply. Your job is to make sure it’s closed fairly.

Formally Rejecting the Initial Offer

A phone call isn't going to cut it. You need to formally reject their lowball offer in writing. An email or a certified letter creates a paper trail and shows the adjuster you mean business.

Keep it simple and professional. State clearly that you are rejecting the proposed settlement because it doesn't accurately reflect your vehicle's true value. Mention that you'll be sending over supporting documentation to justify a higher amount. If you want to get a feel for the right tone and tactics, it's worth reviewing some expert tips for insurance claims before you hit "send."

The Power of an Independent Appraiser

Here’s how you level the playing field. An independent appraiser is your secret weapon—an expert who works for you, not the insurance carrier. Their only objective is to determine the vehicle’s real-world Actual Cash Value (ACV). They do this by digging into the details the insurer’s software glosses over, such as:

- Sales of comparable vehicles in your local market

- Your vehicle's specific condition, backed by maintenance records

- The value of any aftermarket parts or custom modifications

Think about it this way: a J.D. Power study noted that 26% of customers now have deductibles of $1,000 or more. If an insurer undervalues your $20,000 vehicle by just 10% ($2,000), that low offer has already cost you twice your deductible. This is why getting your own appraisal is so critical to protecting your finances. You can explore more insights from these findings on auto claims satisfaction.

The most powerful tool in your insurance policy is often the Appraisal Clause. When you invoke this clause, you legally require the insurer to engage in a binding appraisal process. This takes their lowball software out of the equation and forces them to negotiate based on facts presented by unbiased experts.

Hiring your own certified appraiser introduces a credible, evidence-based valuation that the insurer can't easily dismiss. It’s the single most effective step you can take to break a stalemate and get the fair settlement you deserve. You can learn more by checking out our guide on mastering car accident settlement negotiation.

Using the Appraisal Clause to Get a Fair Valuation

So, you’ve hit a wall with the insurance company. They’ve given you a lowball offer for your vehicle, and no amount of back-and-forth seems to be working. This is precisely when the Appraisal Clause becomes your best friend. It’s a provision built into most auto insurance policies that allows you to break the stalemate and force a negotiation based on actual evidence, not just the insurer's software.

Invoking the clause is a formal process, but it doesn't need to be confrontational. All it takes is a formal letter to your insurance carrier. You simply need to state that you are invoking the Appraisal Clause found in your policy to resolve the dispute over your vehicle’s Actual Cash Value (ACV). Keeping it professional and to the point is always the best approach.

Selecting Your Champion: An Independent Appraiser

Once you’ve invoked the clause, the next step is crucial: you must hire your own certified, independent appraiser. This isn’t a job for your mechanic or a car-savvy friend. You need a state-licensed professional who lives and breathes total loss and diminished value claims.

Think of this appraiser as your expert advocate. Their job is to build a rock-solid case for your vehicle's true worth, completely independent of the insurance company's influence.

A truly professional appraisal report is the foundation of your entire argument. It must be detailed and defendable, including elements like:

- Comparable Local Sales: The report has to analyze recent sales of vehicles just like yours, right there in your local market. This is critical for getting a fair value in specific areas like Oregon and Washington where markets can vary significantly.

- Detailed Condition Analysis: A great appraiser will document everything about your vehicle’s pre-accident condition—its maintenance history, low mileage, pristine interior, and overall care.

- Accounting for Unique Value: Did you have custom modifications? A rare trim package? Is it a collector car with a unique market? Your appraiser needs to factor in everything that made your vehicle special and valuable.

The ultimate goal here is to create a valuation report so thorough and well-documented that it effectively replaces the insurer’s low offer as the starting point for a final settlement. You’re swapping out their algorithm for a real-world, market-based valuation by an unbiased expert.

This expert-driven process is how you sideline the insurer's biased numbers and fight for the fair outcome you deserve. To get a much deeper look into how this powerful policy provision works, check out our detailed guide on the appraisal clause in auto insurance.

So, you’ve done your homework, presented a rock-solid independent appraisal, and the insurance company still won't budge on their lowball offer. It’s a frustrating spot to be in, but your fight isn't over. It just means it's time to take things to the next level.

Your first move should be filing a formal complaint with your state's insurance commissioner. This isn't just another email—it’s a powerful step that gets a different kind of attention. In Oregon, you’ll be dealing with the Division of Financial Regulation, and in Washington, it’s the Office of the Insurance Commissioner. Once they receive your complaint, they’ll open a case and formally require the insurer to respond. Often, just the threat of regulatory oversight is enough to make an adjuster suddenly see things your way.

Weighing Small Claims Court and Legal Counsel

But what if even a regulatory complaint doesn't break the stalemate? Your next stop is likely small claims court. This is a fantastic option for many people because it's designed to be navigated without a lawyer, keeping your costs down while you seek a legally binding decision.

- Oregon: You can sue for up to $10,000, which is enough to cover the disputed amount on most diminished value or total loss claims.

- Washington: The limit is also $10,000, making it a practical path for holding an insurer accountable for a fair valuation.

That said, some situations really do call for a professional. You should seriously consider talking to an attorney if your claim involves significant injuries, a classic or high-value vehicle where the settlement gap is huge, or if you suspect the insurance company is acting in bad faith.

Here's the reality: with liability claims soaring by 57% over the last decade, insurers are increasingly using AI algorithms to analyze—and often minimize—payouts. In this data-driven world, your independent documentation and expert appraisal are more critical than ever. It's the only way to effectively challenge a computer-generated low offer. If you're curious, you can discover more about insurance claims trends and see what you're up against.

Knowing when to push and how to use these tools provides you with the insurance claim support you need to confidently see the process through to a fair conclusion.

Frequently Asked Questions About Car Insurance Claims

Dealing with the aftermath of an accident brings up a lot of questions. Here are some clear answers to the most common concerns we hear from vehicle owners in Oregon, Washington, and beyond who need reliable insurance claim support.

Can I Choose My Own Repair Shop?

This is a big one we hear all the time. The short answer is yes, you absolutely can. In fact, it's your legal right.

Your insurance company will likely have a list of "preferred" or "network" shops they'll push you toward. It's how they control costs. But you are never obligated to use them. I always recommend getting an estimate from a shop you trust—especially one with experience working on your specific make and model. Their quote becomes a powerful benchmark to ensure the insurer's offer is fair and that the repairs are done right.

What Exactly Is a Diminished Value Claim?

Think of it this way: even after perfect repairs, a vehicle with an accident on its record is worth less than one without. A diminished value claim is how you get compensated for that permanent drop in resale value.

This isn't a theoretical loss; it's real money. This type of claim is filed against the at-fault driver's insurance policy. It's important to know that in states like Oregon and Washington, you generally can't file this kind of claim against your own insurance policy. Success depends on proving the other party's negligence caused this specific financial damage to your asset.

Key Takeaway: The gap between your car's value right before the accident and its value right after repairs is its "inherent diminished value." A well-documented claim helps you recover the money you've lost.

How Long Does an Insurance Claim Take?

Unfortunately, there's no single answer. The timeline really depends on the claim's complexity. A simple fender-bender might be wrapped up in a week or two.

However, a more involved case—like a total loss valuation dispute or a diminished value claim that requires invoking the Appraisal Clause—can easily stretch into several weeks or even a few months. Your best defense against delays is staying organized and being persistent with your follow-up. A clean, well-documented file keeps things moving.

What if the Other Insurer Is Ignoring Me?

If the at-fault party's insurance adjuster is giving you the silent treatment, it's time to get serious. Stop relying on phone calls. From this point forward, every communication needs to be in writing, ideally sent via certified mail with a return receipt. This creates an undeniable paper trail.

If the silence continues, your next move is to file a formal complaint with your state's Department of Insurance. This official action usually gets their attention and prompts a much faster response. When dealing with specific coverage questions, like those covered in this guide for motorists on key insurance, having clear proof of your communication attempts is just as critical.

At Total Loss Northwest, we provide the expert appraisal and documentation you need to fight back against lowball offers. If you're struggling with a total loss or diminished value claim in Oregon or Washington, get the professional insurance claim support you deserve.