You open the mail or your claims portal and see a word that sounds like it belongs in a courtroom, not in your car claim: subrogation.

If you're dealing with a crash that wasn't your fault, a total loss offer that feels low, or a repaired car that's now worth less than it was before the accident, that word matters more than most drivers realize. It affects who pursues whom, who gets paid back first, whether your deductible comes home to you, and whether a weak valuation leaves money on the table.

A lot of articles explain subrogation like a legal dictionary entry. That misses the part drivers care about. Your settlement. Your deductible. Your diminished value. Your total loss number. Your wallet.

An Unexpected Letter from Your Insurer

The letter usually lands at the worst time.

You've already dealt with the tow yard, the body shop, the rental car, and the at-fault driver's insurer calling more often than you'd like. Then your own insurer sends a notice saying it may pursue subrogation. For many people, that sounds like bad news. It isn't necessarily bad news. Most of the time, it's just your insurance company telling you it may try to recover what it paid because someone else caused the loss.

Here's how it works: Your insurer paid the bill up front so you didn't have to wait for a long fight between insurance companies. After that, it may put on your shoes and walk the same path you could have used against the at-fault party. That's the basic idea.

Why the letter feels more alarming than it is

Drivers often confuse a subrogation notice with a denial letter, a lawsuit, or a warning that coverage is in danger. Sometimes it can also get mixed up with other formal claim documents. If you're sorting through insurer paperwork and aren't sure what each letter means, this plain-English guide to a reservation of rights letter can help you separate a coverage warning from a routine recovery notice.

Subrogation is common in auto claims because fault can often be traced to another driver. If your insurer pays for repairs or handles a total loss under your policy, it may later seek repayment from the other side.

Where this helps you

The practical upside is simple:

- Deductible recovery: If your insurer recovers money, you may get some or all of your deductible back.

- Faster payment path: Your insurer can resolve your claim first, then chase reimbursement later.

- Pressure on the right party: The cost doesn't just stay with your insurer if another driver caused the damage.

That matters in a small collision. It matters even more in a big one, especially when the dispute isn't only about fault, but about how much your vehicle was worth before the loss or how much value it lost after repair.

What Insurance Subrogation Rights Really Mean

Subrogation sounds technical because it is a legal right. But the plain meaning is straightforward.

Plain-English definition: Insurance subrogation rights let your insurer seek repayment from the person who caused your loss, but only after your insurer has paid your covered claim.

That timing matters. The right doesn't become active just because the crash happened. It becomes actionable after payment on a covered claim.

The shoes analogy is the right one

In auto and liability claims, subrogation is the insurer's post-payment recovery right. After paying its insured, the carrier steps into the shoes of the insured and can pursue the at-fault third party only to the extent the insured could have recovered, as explained in this overview of subrogation basics.

That "only to the extent" part is where many drivers get tripped up. Your insurer doesn't get some magical new super-claim. It inherits your rights, with your limits. If you could have made a claim against the at-fault party, the insurer may pursue that same path after paying you. If your underlying claim was damaged or signed away, the insurer's rights can be damaged too.

What your insurer is not doing

Subrogation usually isn't your insurer trying to take money from you. It's your insurer trying to move the financial burden back where it belongs.

A simple comparison helps:

| Situation | What happens |

|---|---|

| Your insurer pays and stops there | The insurer absorbs the loss |

| Your insurer pays and subrogates | The insurer seeks recovery from the responsible party |

| Recovery includes your deductible | You may get deductible money returned |

This general idea shows up across many kinds of claims, not just auto. If you want a non-auto example that explains how claims move from initial payment to later recovery, Awesim Building Consultants has a useful overview of how insurance claims work in practice.

One document can change everything

A release, waiver, or settlement signed too early can create problems.

If you sign away your claim against the at-fault party before talking with your own insurer, you may also wipe out the insurer's ability to recover.

That doesn't just affect the carrier. It can affect your deductible reimbursement and the overall handling of your claim. This is one reason insurers often tell policyholders to cooperate and to avoid cutting side deals with the other driver's insurer.

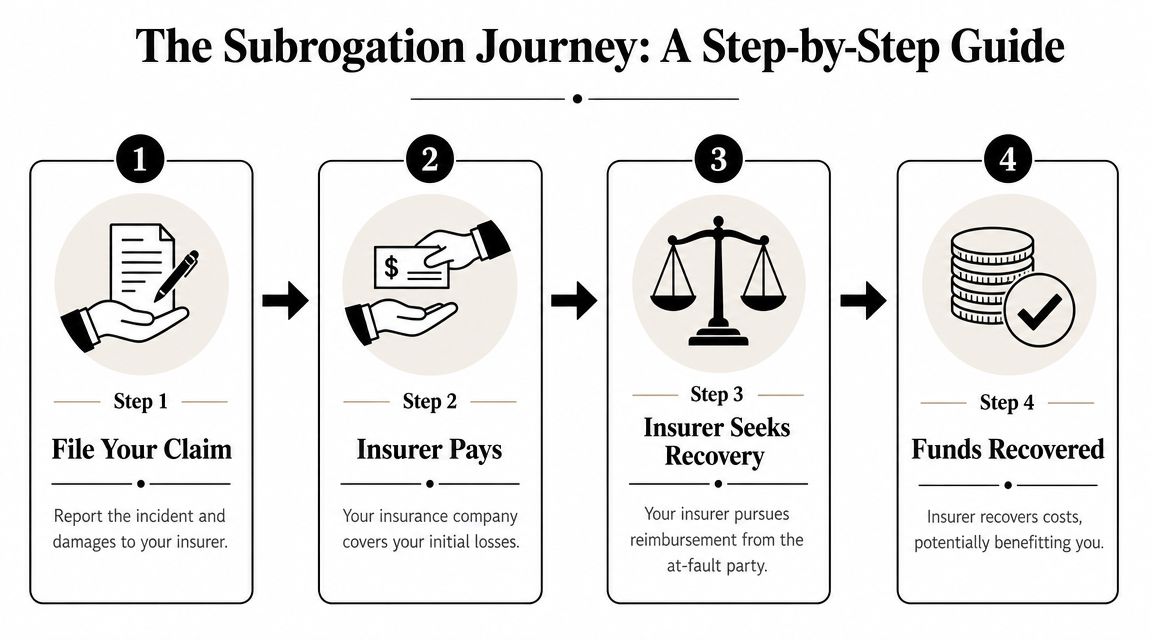

How the Subrogation Process Works Step by Step

Most drivers want the timeline more than the theory. Here's the usual sequence.

Step one is your claim, not their recovery

You report the accident, submit photos, estimates, statements, and any police or exchange information. If you need a practical checklist during the first days after the crash, this guide on steps after a car accident is useful for organizing what to do and what to save.

Then your insurer decides whether the loss is covered and pays according to your policy. That could mean repair costs, or it could mean a total loss settlement if the vehicle isn't economical to repair under the carrier's standards.

Step two starts after payment

Subrogation becomes actionable only after payment on a covered claim, and it's commonly used to recoup both indemnity and deductible amounts in auto collisions, as Progressive explains in its answer on what subrogation is.

For a driver, that usually looks like this:

- You pay your deductible if your collision coverage applies.

- Your insurer pays the rest of the covered repair or total loss amount.

- The insurer opens a recovery file against the at-fault party or that party's insurer.

What happens behind the scenes

After payment, the claim often shifts from the front-line adjuster to a recovery or subrogation unit. That team gathers liability support, payment records, photos, estimates, and policy details. Then it pushes for reimbursement.

That push can take different forms:

- Direct negotiation: One insurer sends a demand to the other.

- Dispute review: The carriers argue over fault, damage amount, or both.

- Formal resolution: If they don't agree, they may use arbitration or litigation.

Where your deductible fits

This is usually the question drivers care about most. If your insurer recovers money, it typically reimburses itself for what it paid and may refund your deductible in full or in part, depending on the outcome and the amount recovered.

Practical rule: Your deductible doesn't vanish. It usually rides along as part of the recovery effort.

If the recovery is complete, the deductible return is more straightforward. If the recovery is partial, things can get murkier. Fault disputes, limited insurance on the other side, or disagreements about the amount of damage can all affect what comes back.

Why the amount paid first matters

Subrogation starts from what your insurer paid. That means the starting number matters. If your insurer underpays a total loss or ignores a valid diminished value component, the recovery process may move forward while you're still undercompensated. That's why valuation disputes deserve attention before the file gets treated like a settled number.

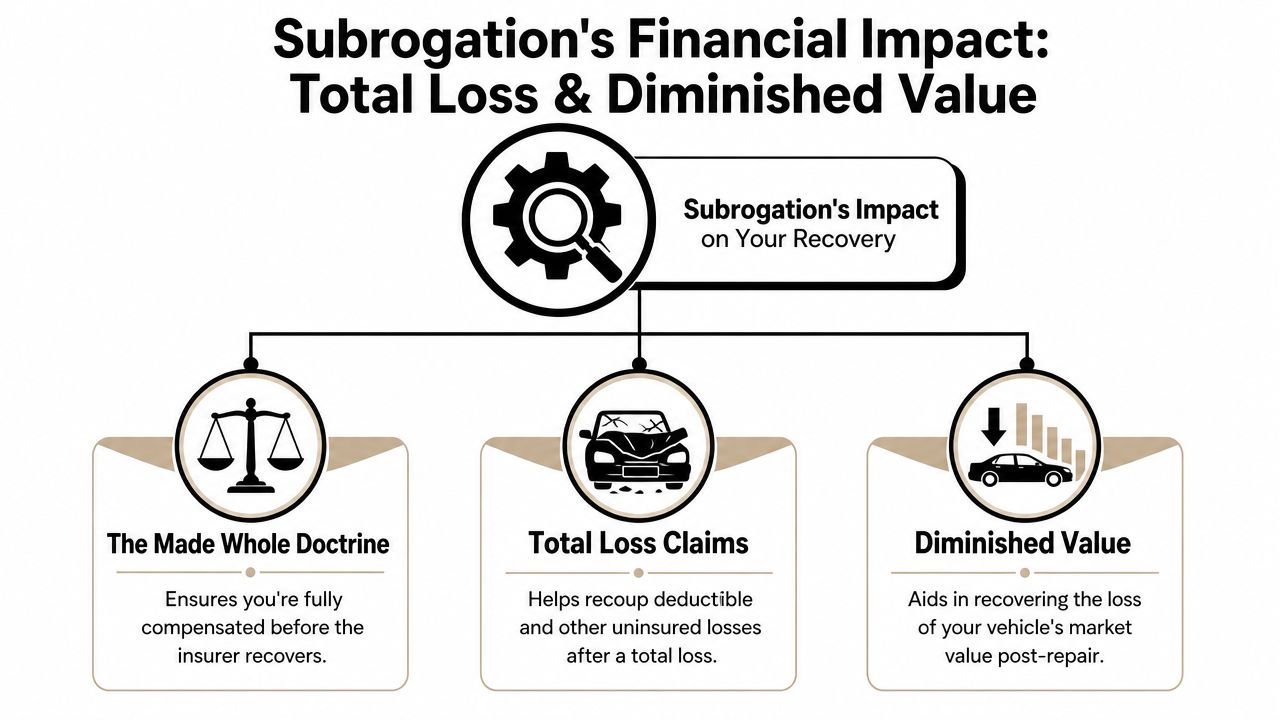

Subrogation's Impact on Total Loss and Diminished Value

At this point, subrogation stops being a background insurance concept and starts affecting your bottom line.

If your car is declared a total loss, the value your insurer assigns to it becomes the foundation of the claim. If your car is repaired but loses market value because it now carries an accident history, the same issue appears in a different form. You need a sound number before anyone starts acting like you've been fully compensated.

The made whole issue

Many courts allow insurers to recover only after the insured is fully indemnified, often called the made whole doctrine, yet policy language can modify that rule. That matters because a total loss payout or diminished value claim may still leave a claimant undercompensated while the insurer still asserts reimbursement rights depending on the contract language, as discussed in this article on subrogation and the made whole doctrine.

That sentence carries a lot of weight in ordinary life. "Made whole" doesn't just mean your insurer mailed a check. It means you've been compensated for the loss the accident caused, subject to the contract language that applies.

Why total loss drivers should pay attention

A low total loss offer can leave gaps such as:

- Vehicle value gap: The insurer's number may not reflect your car's real pre-loss market value.

- Out-of-pocket losses: Towing, storage, rental differences, and other non-covered costs may still be in play.

- Deductible issue: Even if the insurer later recovers, you may be stuck waiting on money that matters now.

If the insurer values your car too low at the start, subrogation doesn't fix that. It only tries to recover based on the path the insurer has taken. That's why drivers often need to challenge valuation before the claim hardens around a weak figure. If you're dealing with that specific problem, this explanation of automobile diminished value helps show why post-accident loss isn't limited to visible repair bills.

Diminished value is part of the real-world loss

A repaired car can still be worth less because buyers, dealers, and appraisal tools react to accident history. That's diminished value. Many legal discussions of subrogation barely touch it, but drivers shouldn't ignore it.

Here is the practical connection:

| Claim issue | Why it matters before subrogation recovery |

|---|---|

| Total loss value is low | You may not be made whole |

| Diminished value is ignored | Your actual economic loss may be understated |

| Deductible remains unpaid | Recovery priority becomes more important |

A short visual explainer can help connect those moving parts:

The appraisal clause is the overlooked pressure point

This is the link many subrogation articles miss. If the fight is over value, not just fault, the appraisal clause can be one of the most important tools in the claim.

When a policy allows appraisal, the dispute can move away from insurer valuation software and toward competing appraisers who focus on market evidence. That matters because subrogation is downstream. Your valuation is upstream. If the upstream number is wrong, the entire claim can feel resolved on paper while your loss remains unresolved in reality.

For drivers with a disputed total loss or a diminished value disagreement, an independent appraiser can help establish a stronger valuation record before recovery issues take over the file.

Navigating Subrogation in Oregon and Washington

Drivers in Oregon and Washington should pay attention to local claim rules and claim culture because the same subrogation letter can play out differently depending on the policy and the state context.

Oregon drivers

Oregon is often viewed as policyholder-friendly when the issue is whether the insured has been fully compensated before the insurer keeps recovery money. In practical terms, that can matter when a total loss settlement doesn't line up with real market value or when a repaired vehicle still carries a meaningful diminished value issue.

That doesn't mean every Oregon driver automatically wins a made whole argument. Contract language still matters, and claim facts matter. But it does mean you shouldn't assume that your insurer's first payment ends the conversation about whether you've been compensated.

Washington drivers

Washington drivers also need to look closely at whether they have been fully compensated and how attorney fees, settlement structure, and reimbursement claims interact. In real claims, these issues can become important when multiple buckets of loss exist at once, such as property damage, deductible, rental issues, and valuation disputes.

For total loss cases, another question sometimes hides in the background: was the vehicle an obvious total loss, or a borderline one? If you're trying to understand that line, this explanation of constructive total loss helps show why a vehicle can be treated as a total loss even when it's technically repairable.

What local drivers should do differently

A short checklist is more useful than broad legal slogans here:

- Read the policy wording: State doctrines matter, but contract terms can affect priority and reimbursement rights.

- Document the valuation dispute early: In both states, a clean record helps if the issue becomes whether you were fully compensated.

- Separate fault from value: The other driver may clearly be at fault while your own insurer still undervalues the car.

- Don't assume deductible recovery solves everything: Getting a deductible back is helpful, but it isn't the same as receiving a fair total loss or diminished value amount.

Local law can help you, but local law doesn't replace evidence. Your settlement still rises or falls on facts, records, and valuation support.

Your Role and Rights During the Subrogation Process

A common turning point in a claim happens after the first check arrives. You assume the hard part is over, then your insurer asks for documents, warns you not to sign anything, and starts talking about recovery from the other driver. At the same time, you may still be wondering whether your total loss offer was too low or whether diminished value was ignored.

That confusion is normal. Subrogation belongs to the insurer, but the dollars tied to valuation still affect you.

Your job is part cooperation, part self-protection. Cooperate with reasonable requests. Protect your right to question a bad number.

What to do

Use this as a practical checklist:

- Respond quickly: If your insurer asks for photos, the police report, witness information, repair invoices, or title papers, send them as soon as you can.

- Keep the full paper trail: Save emails, texts, tow bills, storage charges, valuation reports, estimates, and any settlement language.

- Pause before signing releases: A release from the at-fault driver's insurer can affect your insurer's recovery rights and your own unresolved claim issues.

- Read the valuation, not just the payment: A prompt check feels like progress, but the amount still has to be right.

What to avoid

The easiest mistake is treating subrogation as proof that everything else was handled correctly. It is not. Your insurer can pursue the other side while your total loss value is still too low, or while diminished value was never addressed at all.

Another mistake is signing a broad release because it looks like routine paperwork. A release works like a receipt that says the matter is settled. If the wording is too broad, you may give up rights before you realize what was missing from the claim.

Why this matters to your wallet

Subrogation happens in the background. Valuation hits your bank account directly.

If your insurer underpays a total loss by a few thousand dollars, its later recovery from the at-fault party does not automatically fix your settlement. The same goes for diminished value. An insurer may be focused on getting reimbursed for what it paid, while you are still dealing with whether what it paid was enough in the first place.

That is why the appraisal clause matters so much in this part of the claim. It gives you a way to challenge the amount of loss when the dispute is about value, not fault. In plain terms, subrogation is about who pays. Appraisal is about how much should have been paid.

Analysts at the NAIC found that insurers recover large sums through salvage and subrogation, according to its analysis of salvage and subrogation recoveries. That helps explain why carriers pay attention to recovery. You should give the same level of attention to the number used for your vehicle's value.

Your strongest tool if the number is wrong

The appraisal clause is your strongest tool when the fight is over a low total loss or diminished value figure. It does not stop subrogation. It separates the valuation dispute from the recovery effort so the amount can be tested on its own facts.

That link gets missed in a lot of legal discussions. A driver can fully cooperate with the insurer's recovery efforts and still insist on a proper valuation. Those two positions fit together.

Total Loss Northwest handles independent auto appraisals and appraisal clause disputes for total loss and diminished value claims in Oregon and Washington, as noted earlier.

Cooperate with recovery. Do not give up your right to dispute an unfair valuation.

If you want a simple example from another type of insurance claim, this guide with advice for Florida homeowners shows how records, timing, and early decisions can shape the final payout.

Frequently Asked Questions About Subrogation

What if the at-fault driver is uninsured or underinsured

Your insurer may still pay under your own coverage if the loss fits the policy, then look for whatever recovery is available from the at-fault driver. Whether that leads to actual reimbursement depends on the facts, available coverage, and collectability. For you, the more immediate issue is usually whether your own claim was valued correctly.

Can I tell my insurance company not to subrogate

Usually, no. If the policy gives the insurer subrogation rights, those rights belong to the insurer after it pays the covered loss. You can sometimes affect those rights accidentally by signing a release or making a side settlement, which is exactly why you should ask questions before agreeing to anything from the other side.

Will subrogation affect my insurance rates

Subrogation itself is a recovery process, not a rating explanation. Rate impact depends on the insurer, the policy, fault handling, and other underwriting factors. If you're concerned about premiums, ask your carrier directly how the accident is being coded and whether they consider you at fault.

What happens if my insurer only recovers part of the money

That depends on the policy language, the recovery amount, and the legal rules that apply. In some cases, the deductible is returned in full. In others, it may be returned in part. When the recovery is incomplete, the order of payment can become a real issue, especially if you still haven't been fully compensated for a total loss gap or diminished value claim.

Can subrogation help me recover diminished value

It can be part of the broader economic picture, but it doesn't automatically create a diminished value payment. The key issue is whether diminished value was recognized, documented, and pursued in the first place. If that component never makes it into the claim or remains disputed, subrogation won't magically correct the omission.

Is subrogation a major part of auto insurance or just an occasional back-office task

It's a recurring part of claims economics in auto insurance. The Department of Labor's discussion of healthcare subrogation notes recoveries there account for only about 0.2% to 0.3% of total health insurance expenditures, while the NAIC data cited in that same discussion says salvage and subrogation averaged 4.5% of net claims paid across the full auto sample and 6.2% of net claims paid in some periods, showing how regularly these rights are used in auto claims economics, as summarized in the Department of Labor's review of trends and practices in healthcare subrogation.

What is the biggest mistake drivers make with insurance subrogation rights

They focus on the word "subrogation" and ignore the number attached to their own settlement. If your vehicle value is understated, the rest of the process may keep moving while you're still short. That's why the fair value question should be handled early, especially in total loss and diminished value claims.

If your insurer's total loss or diminished value offer doesn't reflect the actual market loss, Total Loss Northwest can help you challenge the valuation through an independent appraisal and the appraisal clause. For Oregon and Washington drivers, that's often the key step to protecting your settlement before subrogation issues start affecting who gets paid and when.