It’s a gut-wrenching moment: the insurance adjuster calls and drops the news that your car is “totaled.” But what does that really mean? It’s not just about a smashed fender or a crumpled hood. A total loss is a purely financial calculation.

Put simply, your car is declared a total loss when the cost to fix it is more than what it was worth right before the accident. The key term you need to get familiar with is Actual Cash Value (ACV), as this is the foundation of your entire settlement offer.

Your Car Is Totaled, Now What?

So you’ve had a wreck, and after what feels like an eternity of waiting, the call comes in. The adjuster says your car is a goner. It's important to remember this isn't a reflection of how much you cherished your car or the care you put into it—for the insurance company, it's strictly a numbers game.

The decision hinges on whether the repair costs cross a certain line, known as the total loss threshold. This percentage is usually set by state law or your specific policy and often falls between 70-80% of your car's ACV. Grasping this concept is the first, and most important, step you can take toward getting the fair payout you deserve.

The Rise of the Total Loss Claim

If it feels like you're hearing about more and more cars being totaled, you're not wrong. This isn't just about bad accidents. Today, more than 30% of all collision claims in the U.S. end up as total losses.

This "Total Loss Tsunami" is being driven by skyrocketing costs for both parts and labor, which makes fixing even moderately damaged vehicles a bad bet for insurers. The problem got even worse after the pandemic, with supply chain snarls leading to massive delays and higher prices for critical components. These factors all work together to push repair estimates over the ACV threshold far more often.

Navigating the claims process right after an accident can be confusing. Knowing how to file a car accident claim correctly from the start is a huge advantage and lays the groundwork for your entire settlement negotiation.

Why Your Participation Is Essential

Here’s the single most important thing to remember: the insurance company’s valuation is their opening offer, not the final word. You should treat it as the start of a negotiation. Getting actively involved is critical, especially since the national valuation software they use often misses the mark on local market conditions where your exact car might be worth a lot more.

An insurer's initial ACV calculation is their perspective on your vehicle's value, often based on data that favors their bottom line. It's your right to present evidence that paints a more accurate picture.

To get what you're truly owed, you can't be a bystander. You have to become an active player in the process. This means:

- Gathering your evidence: Dig up maintenance records, find receipts for those new tires or that stereo upgrade, and collect any pre-accident photos you have.

- Understanding their report: You need to learn how to read the insurer's valuation report so you can spot mistakes, missing features, or lowball comparisons.

- Knowing your rights: Get familiar with your policy, especially a powerful but often-overlooked tool called the Appraisal Clause.

By taking these steps, you switch from being a passive victim to an informed advocate who can fight for your car's real value. If you're feeling stuck and wondering what comes next, our guide on what to do when your car is totaled can give you a clear plan of action.

How Insurers Determine Your Car's Actual Cash Value

When your insurance company declares your car a total loss, they don't just guess what it was worth. They bring in the heavy machinery—powerful, third-party valuation software from companies like CCC ONE or Mitchell. These systems spit out a detailed report that’s supposed to pinpoint your car's Actual Cash Value (ACV), the amount it was worth right before the crash.

Here’s the catch, though: these systems aren't neutral referees. They are tools programmed with the insurer's financial interests in mind. Their algorithms are often designed to hunt for the lowest-priced comparable vehicles in their database, which conveniently helps them justify a smaller payout to you.

Think of it like hiring an appraiser to value your home, but they only look at foreclosure sales and distressed properties for their comparisons. That's essentially what these automated systems often do for your car. It’s a process that can feel stacked against you from the very beginning.

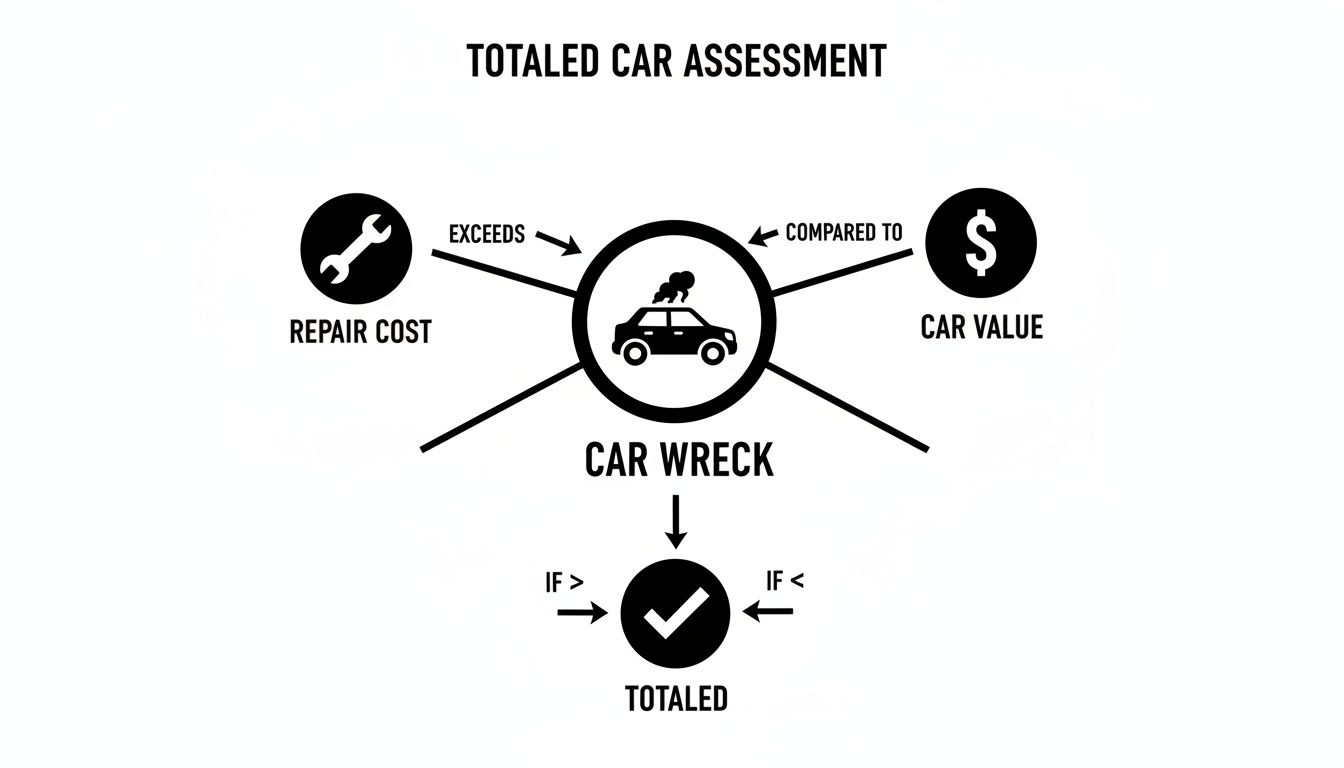

This diagram helps visualize how the total loss decision is made.

As you can see, the whole thing boils down to the pre-accident value versus the cost of repairs. When the numbers are generated by a system that favors the insurer, it’s easy to see how that calculation can be skewed.

The Key Factors In An ACV Report

That valuation report from the insurer’s software will look very official, breaking down several data points to reach its final number. But don't be intimidated. Each of these points can be a source of error or undervaluation.

Here’s what they typically look at:

- Year, Make, and Model: The basic DNA of your car.

- Mileage: A huge factor in depreciation. Higher mileage almost always means lower value in their system.

- Pre-Accident Condition: This is a big one. They'll grade your car (poor, fair, good, excellent), but the adjuster's rating is subjective and often lands on the lower side of reality.

- Optional Features and Trim Package: This is where thousands of dollars get lost. Sunroofs, premium sound systems, and advanced safety features are frequently missed or ignored entirely.

- Regional Market Adjustments: The value is supposedly adjusted for your local area, but "local" can be defined very broadly by the insurer—sometimes stretching hundreds of miles to find a cheaper market.

Knowing what’s in this report is your first step to fighting back against a lowball offer. For a more detailed look at the process, our guide breaks down what the actual cash value of your car really means and how it should be calculated.

Automated Reports vs. Independent Appraisals

The real heart of the conflict in a total loss settlement is the clash between two completely different ways of determining value. The insurer leans on their automated system, while an independent appraiser uses a hands-on, market-driven approach. The difference isn't just academic; it directly hits your wallet.

An automated report is a calculation based on historical data selected by an algorithm. An independent appraisal is a valuation based on current, real-world market evidence collected by a human expert.

To really understand why these two methods produce such wildly different results, it helps to compare them side-by-side.

Insurer Valuation vs. Independent Appraisal: A Comparison

The table below breaks down the fundamental differences between how the insurance company's software operates and how a certified independent appraiser works to find your vehicle's true worth.

| Valuation Factor | Insurance Company Method | Independent Appraiser Method |

|---|---|---|

| Comparable Vehicles | Uses a private database of sold vehicles, often cherry-picking the lowest-priced examples from a massive geographic area. | Finds vehicles currently listed for sale in your specific local market, showing what it would actually cost to buy a replacement today. |

| Condition Assessment | Relies on a quick, often remote inspection or photos, applying standardized, harsh deductions for even minor wear and tear. | Conducts a thorough, in-person inspection (or uses detailed photos) and factors in maintenance history to prove above-average condition. |

| Feature Recognition | Often defaults to the base model VIN, missing thousands of dollars in optional packages, trim levels, and aftermarket upgrades. | Meticulously documents every single factory option, custom feature, and recent upgrade, using receipts and market data to prove their added value. |

| Final Goal | To justify the lowest possible payout that closes the claim quickly and cheaply for the insurance company. | To determine the true, fair market replacement cost of your vehicle, ensuring you are made whole and can afford a genuinely comparable car. |

At the end of the day, the insurer's automated process is built for their own efficiency and cost control. An independent appraisal, on the other hand, is designed to uncover your vehicle's complete and honest value, arming you with the solid evidence you need to get the fair settlement you’re owed.

Why Your First Settlement Offer Is Often Too Low

When the insurance adjuster calls with their first settlement offer for your totaled car, it’s easy to feel a pit in your stomach. That number often seems shockingly low—nowhere near enough to buy a similar car to replace the one you lost. This isn't an accident. It's business.

Insurance companies are, at their core, for-profit enterprises. Every dollar they don't pay out on a claim is a dollar that contributes to their bottom line. That initial offer isn't a final figure; it's an opening bid in a negotiation they're banking on you not starting. They know many people are stressed, overwhelmed, and just want to get it over with, so they accept the first number and move on.

The Devil Is in the Details: Flaws in Valuation Reports

The valuation report the insurer sends over might look official, packed with data and seemingly objective. But when you dig in, you often find it’s full of mistakes that just so happen to drive down your car’s value. These aren’t tiny oversights—they can easily add up to thousands of dollars.

One of the most common and costly errors is getting the trim level wrong. Let's say you drove a fully-loaded SUV with the bigger engine, leather interior, and every tech upgrade available. If the report defaults to the VIN for the base model, it instantly erases all that value. Suddenly, your premium vehicle is being valued as the cheapest version that rolled off the factory floor.

You’ll also want to watch out for these other common slip-ups:

- Missing Features: That panoramic sunroof, premium sound system, or factory tow package? They're often completely left out of the calculation.

- Unfair Condition Deductions: Adjusters can be incredibly harsh, knocking off significant money for minor, everyday wear and tear like tiny scuffs or dings that are perfectly normal for a car of its age.

- Mileage Mix-ups: A simple typo in your car's mileage can dramatically—and unfairly—slash its value.

Since the goal is often to pay out as little as possible, understanding how to effectively deal with insurance adjusters is one of the most powerful things you can do. Knowing their playbook is your best defense.

The Problem with Their "Comparable" Cars

Perhaps the biggest shell game in any total loss valuation is the selection of so-called "comparable vehicles," or "comps." The software adjusters use scours massive databases for similar cars that have sold recently. The problem? Their definition of "similar" can be stretched to fit their needs.

They might pull comps from a dealership 300 miles away in a totally different market where cars sell for far less. This conveniently ignores the reality of what it would cost you to buy a replacement in your own town. It's a classic case of cherry-picking the lowest-priced data to justify a lowball offer.

An insurer's "comparable vehicle" is often just the cheapest one they can find in a wide net. A true comparable is a car you could actually go out and buy in your local area today.

Your Daily Driver Is a Prime Target

This problem is especially acute for older, reliable "daily driver" cars. A huge percentage of total loss claims involve vehicles that are seven years or older. These dependable cars are prime candidates for being totaled out because their book value drops faster than the cost of repairs goes up.

According to the latest Crash Course report from CCCIS, the market has seen major shifts. While cars used to lose about half their value in five years, recent dynamics have changed, and total loss frequency is still climbing.

The automated systems insurers use are just not built to see the real-world value of a well-maintained older car. They can't factor in your diligent maintenance history, that major engine work you just paid for, or the brand-new set of tires you put on last month. All of these things make your car more valuable than an identical one that's been neglected.

Recognizing these tactics is the first and most critical step in fighting for the fair settlement you deserve.

Using The Appraisal Clause To Secure A Fair Settlement

When you're at a standstill with your insurer over a lowball settlement offer, it can feel like you've hit a brick wall. But buried deep in the fine print of your auto policy is a powerful, often overlooked tool designed for this exact situation: the Appraisal Clause.

Think of this clause as a contractual escape hatch. It gets you out from under the thumb of the insurer's biased valuation software and puts you on a more level playing field. It’s a formal dispute resolution process you have a right to invoke. This isn't an aggressive or hostile move; it's a standard procedure built right into your policy to ensure a fair and impartial outcome.

Invoking this clause effectively takes the negotiation away from the adjuster and their computer-generated report. Instead, it places the insurance valuation of your totaled car into the hands of qualified, independent experts who rely on real-world evidence, not just an algorithm.

What Is The Appraisal Clause And How Does It Work

The Appraisal Clause lays out a clear process for settling disagreements over the value of a loss. When you trigger it, both you and the insurance company hire your own independent, competent, and impartial appraiser to value the vehicle. It’s a structured negotiation with defined roles.

Your appraiser's job is to build a rock-solid case for your car's true market value, representing your best interests. The insurer's appraiser does the same for them. These two experts then get down to business, working to reach an agreement on the Actual Cash Value.

The real power of the Appraisal Clause is that it levels the playing field. It forces the valuation to be based on verifiable market data and expert analysis, not some black-box algorithm designed to save the insurance company money.

What if the two appraisers can't agree? They mutually select a neutral third-party expert, known as an umpire. The umpire acts as a tie-breaker, reviewing the evidence from both sides and making a final decision. A number agreed upon by any two of the three parties becomes the final, binding settlement amount.

The Step-By-Step Process To Invoke The Clause

Putting the Appraisal Clause into motion isn't as simple as telling your adjuster you want to use it. It's a formal process, and you need to follow a clear sequence of steps to protect your rights.

Here’s how it usually plays out:

- Send Written Notice: You have to formally notify your insurance company in writing of your intent to invoke the Appraisal Clause. This letter needs to clearly state that you're disputing their ACV offer and are exercising this contractual right.

- Select Your Appraiser: This is the most important step you'll take. You need to hire a qualified, certified independent auto appraiser who specializes in total loss claims. Their expertise and reputation are your biggest assets here.

- Your Appraiser Submits Their Valuation: Your expert will conduct a thorough analysis, document every feature and the true condition of your vehicle, find actual local comparables, and submit a detailed valuation report to the insurance company's appraiser.

- Negotiation or Umpire Intervention: The two appraisers will then negotiate. If they can come to an agreement, the value is set. If they're at an impasse, they'll select an umpire to make the final call.

Getting the language and requirements right is critical. To dive deeper, you can learn more about the insurance appraisal clause and see how it truly empowers policyholders. This entire process is designed to ensure the final number reflects what it would actually cost you to replace your vehicle in your local market.

Building Your Case To Prove Your Car's True Value

If you want to successfully challenge a lowball insurance offer, you need to do more than just feel like the number is wrong. You need cold, hard evidence. Think of yourself as building a case for a judge—your goal is to present a complete, undeniable picture of what your car was worth moments before the accident.

This isn't about picking a fight. It’s about being prepared. The insurance company's valuation came from a standardized report that probably missed all the unique details that made your car special. Your job is to fill in those gaps with solid proof.

This prep work does more than just boost your confidence. It gives your independent appraiser the ammunition they need to argue for a fair settlement on your behalf. The more thorough you are, the stronger your position becomes.

Assembling Your Evidence Dossier

It’s time to gather every scrap of paper and digital file related to your car. This documentation tells the story of a well-maintained vehicle, not just another entry in a massive database.

Your evidence file should include:

- Detailed Maintenance Records: Every oil change, tire rotation, and service appointment proves you took care of the car, preserving its mechanical health and, by extension, its value.

- Receipts for Recent Upgrades: Did you install new tires six months ago? Upgrade the sound system? Add a tow hitch? Every single receipt is proof of added value that the insurer’s automated report almost certainly overlooked.

- Original Window Sticker: If you can find it, the "Monroney" sticker is the ultimate trump card. It lists every single factory option and package, leaving no room for the insurer to argue your car was a base model.

- Pre-Accident Photos: A picture is worth a thousand words—or in this situation, maybe thousands of dollars. Photos showing your car in pristine condition right before the crash are powerful proof against a lowball "fair condition" rating from the adjuster.

Becoming Your Own Market Analyst

With your documents in hand, it's time to find out what it would actually cost to buy your car again in your local area. This is where you directly counter the insurer's often-flawed list of "comparable" vehicles.

Hop on to online marketplaces like Autotrader, Cars.com, or even Facebook Marketplace. Run a search for vehicles that are a true match for yours—same year, make, model, trim, and similar mileage.

Insurers often cast a wide geographic net to find the cheapest "comps" possible. Your goal is to narrow that focus to your local market to prove what a true replacement would cost you right here, right now.

Save screenshots and links for at least three to five genuinely comparable vehicles for sale nearby. This real-world market data is one of the most persuasive pieces of evidence you can have.

Documenting The Intangibles

Finally, don’t forget about all the qualities an automated system can't see. Make a detailed list of everything that made your car stand out from the crowd.

Think about these points:

- Factory Packages: Did your car have the Sport, Tech, or Luxury package? List every single feature that came with it.

- Rare Options: Was your car a unique factory color? Did it have a hard-to-find engine or transmission combo? Highlight its scarcity.

- Exceptional Condition: Make notes about the flawless interior, the scratch-free paint, and anything else that proves your vehicle was in far better shape than the average car of its age.

This kind of meticulous documentation is more critical now than ever. With economic pressures like potential tariffs on the horizon, some analysts believe insurers will be looking to minimize payouts on total loss claims. As detailed in a report about the auto insurance market on Repairer Driven News, external factors can have a real impact. By building a powerful case file, you arm yourself—and your appraiser—with the undeniable proof needed to get a fair deal.

It's one thing to talk about valuation theory, but it's another to see it play out in the real world. Let’s walk through a story that happens all too often—a car owner, probably a lot like you, gets blindsided by a lowball offer after their car is totaled. This case study is a perfect example of how hiring an independent appraiser can completely change the game.

Picture this: a driver’s five-year-old SUV, kept in fantastic shape, gets totaled in a bad rear-end collision. A few days later, the insurance company’s offer lands: $18,500. The owner was shocked. A quick look at local listings showed similar SUVs selling for closer to $22,000.

When they dug into the insurer's report, they found it was a mess. It incorrectly listed their vehicle as a base model and used "comparable" vehicles from a dealership over 200 miles away. Sound familiar?

Turning Frustration into Action

Instead of just accepting it, the owner decided to hire a certified independent auto appraiser. This was the turning point. The appraiser got to work immediately, building a completely new case for the insurance valuation of the totaled car, ignoring the insurance company's flawed report entirely.

The appraiser’s approach was methodical and focused on three critical areas:

- Correcting the Record: First, they documented the SUV's actual trim—a premium package—and accounted for every single factory option the insurer conveniently missed, like the panoramic sunroof and upgraded sound system. Just correcting these details added $2,500 to the vehicle's value.

- Proving Superior Condition: The owner had kept meticulous service records and had plenty of pre-accident photos. The appraiser used this evidence to prove the vehicle was in "excellent" condition, not the "average" rating the adjuster had lazily assigned.

- Finding True Local Comparables: Finally, the expert located four genuinely comparable SUVs listed for sale within a 50-mile radius. This proved what the true local market value really was, and it wasn't what the insurer claimed.

The Successful Outcome

Armed with this evidence, the appraiser submitted a detailed report to the insurance company that laid out every error and provided concrete proof of the vehicle's actual worth. Faced with a professional, data-backed valuation, the insurer’s lowball offer became impossible to defend.

An independent appraisal isn't just a second opinion; it's a professional counter-negotiation grounded in market facts. It forces the insurer to address the actual replacement cost, not just a number generated by their software.

So, what was the final result? The insurance company revised its settlement offer to $23,200. That’s a $4,700 increase from their initial offer. Even after paying the appraiser's fee, the owner had more than enough money to go out and buy a truly comparable replacement.

This story is a perfect illustration of the value an expert brings to the table. It turns a frustrating, one-sided negotiation into a fair fight where you get the settlement you rightfully deserve.

Your Top Questions About Total Loss Valuation, Answered

When your car is declared a total loss, a flood of questions usually follows. Let's walk through some of the most common ones we hear from car owners trying to make sense of the insurance valuation process.

How Long Does This Whole Process Take?

It’s definitely not an overnight thing, so a little patience will go a long way. The journey from the adjuster's first look at your car to you getting a settlement offer typically takes at least a few weeks. They have to do a full damage assessment, run their valuation report, and push it all through their internal approval process.

What if you get a lowball offer and decide to fight it? If you use the appraisal clause in your policy, it will add more time to the clock, often several more weeks. But honestly, standing up for your rights is often the only way to get your insurer to budge from their first number and pay you what your car was actually worth.

Can I Just Keep My Car?

Absolutely. In nearly every case, you have the option to keep your vehicle after it's been totaled. This is called "owner retention." If you go this route, the insurance company will cut you a check for the car's Actual Cash Value (ACV) minus its salvage value. That salvage value is simply the amount they would have gotten for the wrecked car at a salvage auction.

Owner Retention in a Nutshell: You get a smaller check from the insurance company, but you get to keep the car. From there, you're on the hook for all repairs and meeting the state's requirements to get it back on the road.

Just know what you're getting into. The DMV will issue a salvage title, and you can't legally drive the car until it's fully repaired, passes a rigorous state safety inspection, and is re-titled as a "rebuilt" vehicle.

What Happens If I Owe More on My Loan Than the Car Is Worth?

This is a tough spot to be in, and it’s more common than you'd think. It's known as being "upside down" or "underwater" on your loan. It simply means the settlement offer from your insurance company isn't enough to pay off what you still owe the bank.

This is exactly why "gap insurance" exists. If you had the foresight to buy it when you got your car, you’re covered. Gap insurance pays for that "gap"—the difference between the insurance payout and your remaining loan balance. It saves you from the nightmare of making payments on a car that's sitting in a scrap yard.

If you don't have gap insurance, the unfortunate reality is that you are responsible for paying off the rest of the loan yourself, even after the insurance company sends its check directly to your lender.

At Total Loss Northwest, we're experts at proving your vehicle's real value. If you're in Oregon or Washington and feel like you're getting a lowball offer, don't just accept it. Reach out to us for a certified, independent appraisal to ensure you get the fair settlement you're entitled to. Find out how we can help at https://totallossnw.com.