You open the claim email, see the number, and your stomach drops. The carrier says your vehicle is a total loss. The offer looks clean, official, and final. It also looks nothing like what it would cost to replace the car you owned.

That reaction is normal. It doesn't mean you're emotional, greedy, or confused. It usually means the first number is exactly what it often is in a loss settlement negotiation: an opening position.

I've seen this pattern over and over. The owner maintained the car, added new tires, kept records, maybe drove a harder-to-find trim, and then gets handed a valuation built from a system they can't inspect. The adjuster sounds confident. The paperwork looks polished. None of that makes the number right.

That Sinking Feeling The Lowball Settlement Offer

The first offer often lands when you're still dealing with towing, rental issues, work disruption, and the hassle of finding another vehicle. That timing matters. People are tired, and insurers know tired people are easier to close.

You're not alone if the number feels off. In the U.S., the average paid auto physical damage claim rose from about $4,500 in 2020 to nearly $6,100 by 2022, about a 35% increase, and in many states more than 10% to 20% of claimants formally contest the first offer, according to the Insurance Information Institute. Replacement costs climbed fast. Settlement friction climbed with them.

Why this keeps happening

A total loss valuation isn't just about whether your car ran well. The insurer is trying to assign an Actual Cash Value, usually based on market data, condition adjustments, mileage, and internal valuation methods. The problem is simple. If the comparables are weak, the condition adjustments are unfair, or key features are missed, the offer can come in low.

That doesn't mean the adjuster is required to be your advocate. They aren't. Their job is to settle the claim. Your job is to make sure the number reflects the vehicle you lost.

Practical rule: Treat the first total loss offer like a draft, not a verdict.

There's another issue people miss. Bad paperwork and procedural mistakes can weaken a claim before valuation even becomes the fight. If you're dealing with a carrier that's stalling, narrowing coverage, or pointing to technicalities, it helps to understand common insurance claim denial reasons so you can spot whether the valuation dispute is being mixed with a coverage dispute.

What a normal next step looks like

A proper response isn't anger. It's documentation.

Start by asking for the valuation report, the full comparable vehicle list, every condition adjustment, and the exact options the insurer says your vehicle had. Then compare that to your own records. If you want a clearer picture of how the process usually unfolds, this guide on negotiating a total loss settlement is a useful companion to the steps below.

What works:

- Requesting the full report before arguing about the number

- Checking trim and options line by line

- Looking for bad comparables, especially vehicles with different drivetrains, packages, or much worse condition

What doesn't:

- Saying the offer feels unfair without evidence

- Citing only one price guide

- Rushing to sign because the adjuster says they need an answer quickly

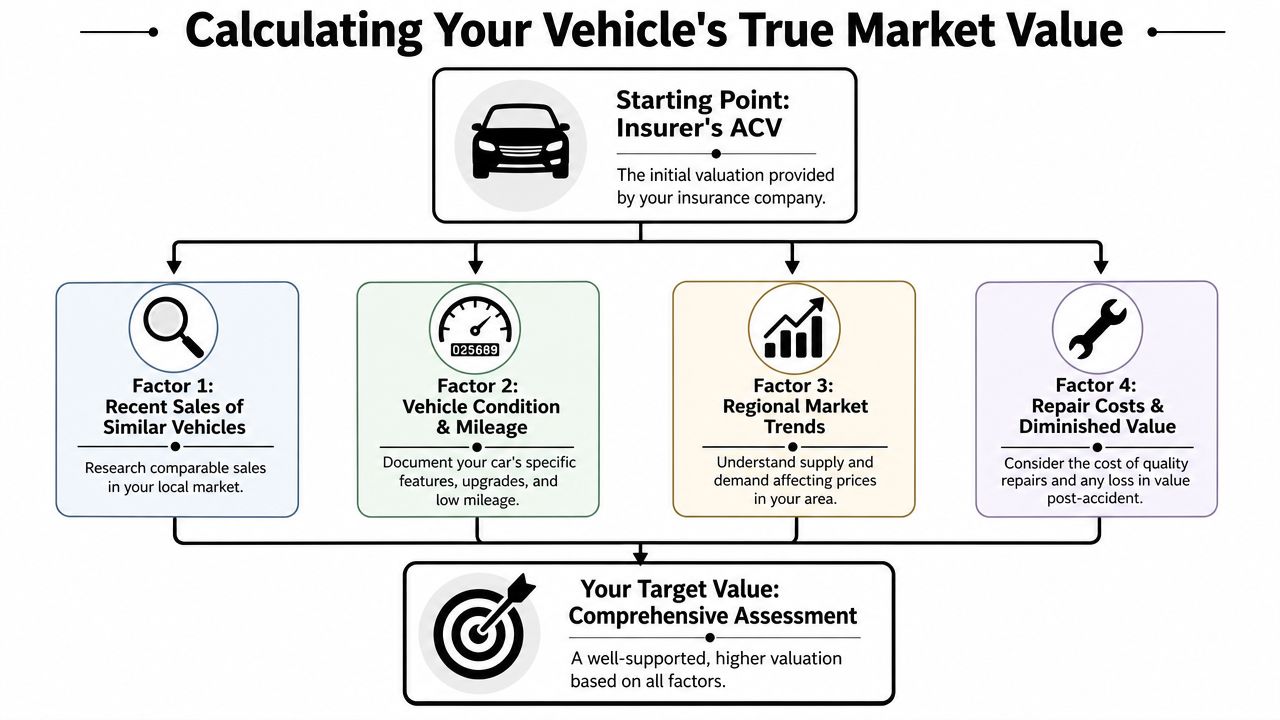

Calculating Your Vehicle's True Market Value

The insurer's valuation isn't sacred. It's one number generated by one process. You need your own number, built from evidence you can defend.

The black box problem

Many drivers still think the fight is just KBB versus the adjuster. It isn't. Over 70% of personal auto claims now incorporate algorithmic valuation, and those tools can blend auction data with internal loss histories in ways consumers can't meaningfully audit, as noted by Total Loss Northwest's fair market value guide.

That's the core imbalance. The insurer may be using a dynamic model that makes hidden adjustments for mileage, condition, region, and prior data trends, while you're staring at a public price guide that doesn't show the same inputs. If you don't build a file around real-world market proof, you'll end up arguing conclusions instead of evidence.

Build a replacement market file

Your target value should answer one practical question: what would it cost to replace your vehicle with a substantially similar one in your market?

Use actual listings and recent market offerings. Focus on vehicles that match as closely as possible on the points that matter most:

- Year, make, model, and trim: An LX isn't an EX. A base truck isn't a premium package truck.

- Mileage: Similar mileage matters. A low-mile example deserves low-mile treatment.

- Drivetrain and engine: AWD versus FWD, hybrid versus gas, turbo versus naturally aspirated. These aren't minor details.

- Factory packages and options: Navigation, upgraded audio, tow package, safety package, premium wheels, leather, sunroof.

- Condition before the loss: Clean interior, no warning lights, good paint, service history, recent tires or brakes.

Pull listings from dealer sites and major marketplaces. Screenshot them. Save the URL. Note the date. If a listing disappears, your screenshot still exists.

A short working table helps keep your file organized:

| Item | What to record |

|---|---|

| Comparable vehicle | Year, trim, mileage, location |

| Asking price | Full listed price, not just monthly payment |

| Key match points | Engine, drivetrain, packages, condition |

| Key differences | Higher mileage, damage history, missing options |

| Evidence saved | Screenshot, URL, dealer name, date captured |

Adjust for your vehicle, not a generic version

Many owners leave money on the table. They collect comps, but they don't explain why their own vehicle should sit at the top, middle, or bottom of that range.

Use hard proof:

- Maintenance receipts for major recent work

- Pre-loss photos showing clean body and interior

- Window sticker or build sheet if available

- Upgrade documentation for quality additions that affect marketability

- Ownership records showing care and consistency

Your evidence package should make it easy for a stranger to understand why your specific vehicle was worth more than an average unit.

Routine maintenance usually doesn't create a dollar-for-dollar add-on. But it absolutely helps support condition. New tires won't always be paid as a separate line item, yet they strengthen your position against an unfair downward condition adjustment.

Diminished value is a different animal

People often mix up total loss value and diminished value. They aren't the same claim. Diminished value usually comes up when a vehicle is repaired and has lost market value because it now carries accident history.

State law and policy language matter here. Many states allow third-party diminished value claims against the at-fault insurer, while others restrict them, and policy wording can narrow the path further. That's why you should never assume a repaired vehicle automatically qualifies, or that your own policy treats it the same way as a third-party claim.

If your loss involves a repairable vehicle rather than a total loss, check your state-specific rules before making diminished value part of your demand.

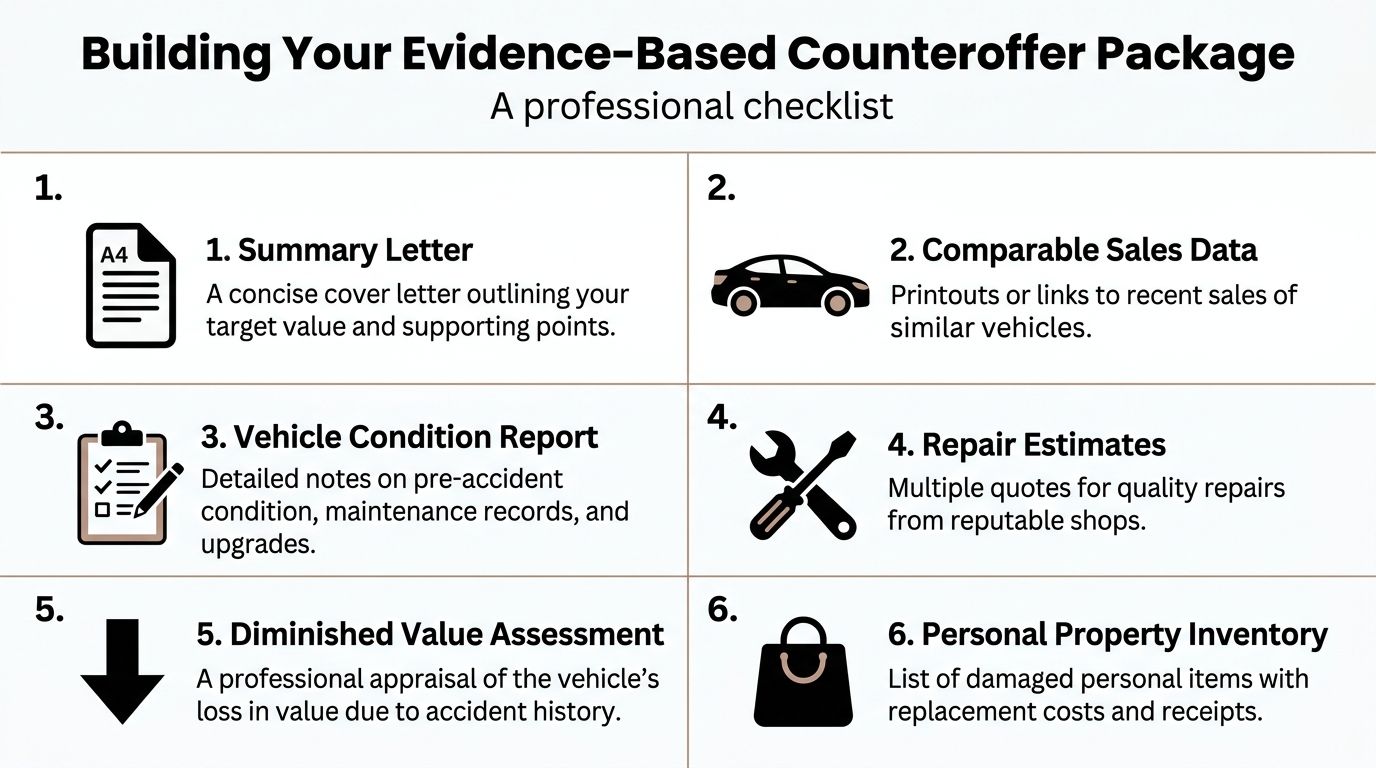

Building Your Evidence-Based Counteroffer Package

A strong counteroffer doesn't read like a complaint. It reads like a file prepared by someone who expects their work to be reviewed line by line.

A detailed demand package matters. A study cited by Slam Dunk Attorney found that claimants who submitted a documented demand package after completing their documentation had median recoveries 27% to 42% higher than those who accepted early offers, and adjusters routinely low-ball the first offer by 30% to 50% of a well-documented demand.

What goes in the package

Think of your package as a rebuttal to the insurer's report.

Include these pieces:

A cover letter

Keep it short. State the claim number, vehicle details, insurer's offer, your target value, and the reason for the dispute.Comparable vehicle exhibits

Attach your best listings with screenshots, seller information, pricing, and notes explaining why each comp is relevant.A vehicle condition summary

Describe pre-loss condition accurately. Don't overstate it. If the car had flaws, acknowledge them. Credibility matters.Maintenance and repair records

Recent tires, brakes, suspension work, major scheduled service, battery replacement, and dealership service history all support condition and marketability.Options and package proof

Build sheet, window sticker, VIN decoder output, original sales documents, or manufacturer records.Photos

Exterior, interior, odometer, wheels, seats, cargo area, and any especially clean features from before the loss.

The cover letter structure that works

You don't need legal theater. You need clarity.

Use this framework:

- Opening paragraph: Identify the claim and dispute the valuation.

- Second paragraph: State that the offer does not reflect comparable local replacement vehicles.

- Third paragraph: List the enclosed evidence categories.

- Closing paragraph: Request a revised valuation in writing and a response by a reasonable date.

A sample tone:

I am disputing the current total loss valuation because it does not reflect the retail market for a comparable replacement vehicle of like kind, condition, trim, mileage, and equipment. Attached are comparable market listings, maintenance records, option documentation, and pre-loss condition materials supporting a revised value.

Common package mistakes

These mistakes weaken good claims fast:

- Too many weak comps: Three strong comparables beat ten sloppy ones.

- National search results without context: Local and regional relevance matters.

- Listings for the wrong trim: This happens constantly.

- Arguments without exhibits: If you say it had premium equipment, prove it.

- Messy files: Label every attachment clearly.

A simple exhibit naming system helps:

- Exhibit A, valuation report discrepancies

- Exhibit B, comparable listings

- Exhibit C, maintenance records

- Exhibit D, option verification

- Exhibit E, pre-loss photos

If you need an independent valuation

At some point, the dispute may be too technical for a DIY package alone. That's where an independent appraiser can help. One option is Total Loss Northwest, which prepares total loss and diminished value appraisals and can support appraisal-clause disputes with documented market analysis. That's useful when the insurer's file is built around software outputs you can't fully audit.

Navigating the Negotiation Conversation

Once your package is in, the game starts. The adjuster doesn't need to agree with you immediately. They need to answer the evidence.

Stay on the record

Phone calls are fine for speed. They are bad for memory. Use the call to identify the dispute, then follow up by email the same day.

Ask for three things in writing:

- The revised offer amount

- The reason each of your comps was accepted or rejected

- Any adjustments applied to mileage, condition, or options

That paper trail matters. It keeps the conversation tied to facts instead of drifting into vague statements like "our system doesn't support that value."

Scripts that keep control

If the adjuster says your comps aren't valid:

Please identify specifically which differences make each comparable invalid, and whether your position is based on trim, mileage, equipment, condition, or location.

If the adjuster says they don't pay for maintenance:

I'm not asking for routine maintenance as a separate reimbursement item. I'm providing maintenance records to support pre-loss condition and to challenge any negative condition adjustment.

If the adjuster dismisses your higher-value comp because it has lower mileage:

Then apply a consistent mileage adjustment and explain it in writing. A comparable doesn't become irrelevant just because it supports a higher value.

Many disputes also get tangled up over diminished value language. That's a problem because many states permit third-party diminished value claims, others restrict them, and policy language can limit recovery further. Fewer than half of claimants fully understand how those rules interact, which is why adjusters can use that confusion to shut down discussion early. Keep the conversation narrow. Ask whether they are denying the category entirely, limiting it under policy language, or disputing the proof.

A quick explainer can help if you want to hear another breakdown of adjuster tactics and response framing:

What gets movement and what stalls it

A short comparison makes this clear:

| Adjuster tactic | Weak response | Strong response |

|---|---|---|

| "Those aren't comparable" | "Yes they are" | "Please identify the exact mismatch for each listing in writing" |

| "Our valuation vendor already adjusted for that" | "I don't believe it" | "Please provide the adjustment category and amount applied" |

| "Maintenance doesn't increase value" | "I spent a lot on the car" | "These records support condition and rebut downward condition treatment" |

| "Diminished value isn't owed" | "I know my rights" | "Please confirm whether the denial is based on state law, policy language, or proof" |

Calm beats outraged. Specific beats loud. Written beats verbal.

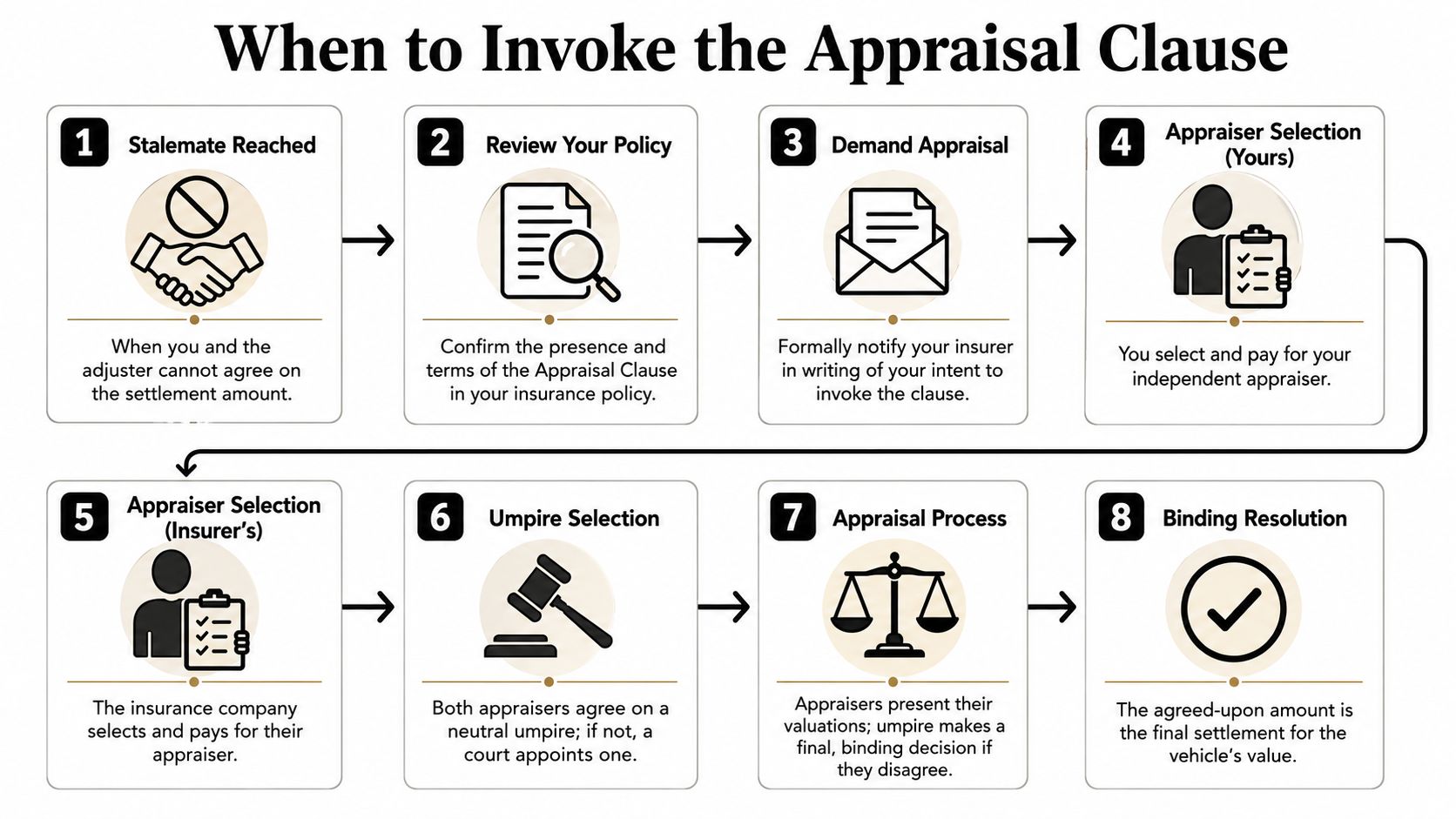

When to Invoke the Appraisal Clause

Sometimes you've done everything right and the number still won't move enough. That's when you stop repeating yourself and use the tool built into many policies.

The standard Personal Auto Policy has included an Appraisal Clause for decades, and while only about 2% to 5% of total loss claims trigger it, that still amounts to tens of thousands of negotiations annually in the U.S., as described in this overview of the insurance appraisal clause.

What the appraisal clause actually is

It isn't a lawsuit. It isn't an accusation of bad faith by itself. It's a formal valuation dispute process.

You and the insurer each select an appraiser. Those appraisers try to agree on value. If they can't, they submit the dispute to an umpire. The value determined through that process is binding on the amount of the loss, subject to the policy terms.

That's why the appraisal clause matters. It moves the valuation issue away from back-and-forth with a desk adjuster and into a structured process run by valuation professionals.

When it's the right move

Appraisal makes sense when:

- Coverage isn't the primary dispute and the fight is mainly about value

- The carrier has stopped meaningfully engaging with your evidence

- The amount at stake justifies the cost of hiring your own appraiser

- Your comparables and records are solid, but the insurer keeps relying on its own report

It makes less sense when the claim involves a pure coverage denial, title issue, fraud allegation, or a dispute over whether the policy covers the loss at all. Appraisal is for value, not every possible claim problem.

How to trigger it cleanly

Keep the written demand simple and formal.

Your letter should:

- Cite the appraisal clause in your policy

- State that a dispute exists over the amount of loss

- Name your appraiser, if you've selected one

- Request that the insurer identify its appraiser within the timeline required by the policy

A practical version sounds like this:

I am invoking the appraisal provision of my policy due to a dispute regarding the amount of loss. Please confirm receipt of this demand and provide the name and contact information of the appraiser selected on behalf of the insurer.

Don't bury that in a long emotional narrative. The point is to start the process.

What to expect once it starts

This stage becomes more technical. The appraisers will review valuation materials, comparables, options, condition evidence, and any prior adjustments. If they disagree, the umpire resolves the difference.

That changes the advantage. The insurer is no longer the only party framing the value.

Finalizing Your Settlement and Next Steps

Once the number is resolved, the last stage is paperwork. People often relax too early here and sign before checking the details.

Read the settlement documents carefully. Confirm the vehicle description, settlement amount, deductible treatment if applicable, title transfer requirements, payoff handling if there's a lender, and whether the release language matches what was agreed upon. If the car is a total loss, you'll usually need to transfer title and deal with any personal property still in the vehicle before the claim closes.

Before you sign

Use this quick checklist:

- Match the final number to the agreed amount

- Check payoff instructions if a lienholder is involved

- Confirm salvage terms if you're retaining the vehicle

- Remove personal items and document anything still missing or damaged

- Save every final email and letter in one folder

If you've never had to decode policy wording before, it helps to spend a few minutes learning the structure of insurance contracts in general. A practical guide on reading a homeowners insurance policy is useful for understanding how exclusions, conditions, and settlement language are often buried in plain sight. Different line of insurance, same lesson: read the form, not just the summary.

If the result still isn't fair

Most valuation disputes end before this point. If yours doesn't, the remaining options are escalation paths, not panic moves.

You can:

- File a complaint with your state Department of Insurance

- Consult an attorney if the issue looks bigger than valuation and starts looking like claim handling misconduct

- Preserve your full file so every offer, report, email, and attachment is organized

The core rule through the whole loss settlement negotiation process is simple. Evidence beats emotion. A clean file, strong comparables, accurate vehicle details, and written follow-up will do more for your payout than arguing ever will.

If you're stuck on a low total loss offer or need an independent valuation to support an appraisal demand, Total Loss Northwest provides total loss and diminished value appraisal support built around documented market evidence rather than insurer software outputs.