The adjuster calls. The words come fast. “Total loss.” Then your mind jumps ahead to the questions nobody answered in the first minute. Can you keep the car? Can you fix it? Will Montana let you register it again? What happens to the title? And if you do keep it, are you walking into a money pit with paperwork attached?

That's the moment most owners start searching for montana salvage title information, and most of what they find is too general to help. Generic advice won't tell you which inspection Montana wants, what paperwork you need to save, or why a cheap state filing fee doesn't mean the decision is financially cheap.

I work from the value side of total loss claims, and the pattern is familiar. Owners get pushed to focus on the settlement check because that's the immediate issue. But the bigger financial decision often comes right after that. Keeping a totaled vehicle can make sense in the right situation. It can also trap you in a long repair-and-title process with lower resale value and tougher insurance options.

This guide is for the owner who needs a calm, Montana-specific roadmap. Not theory. Not slogans. Just what the title branding means, how the rebuild path works, and where people lose money when they move too quickly.

The Phone Call You Never Wanted to Get

You might be standing in a body shop parking lot, staring at a bent fender and hoping the repair estimate still leaves you a way out. Or you might be at your kitchen counter when the insurer says the vehicle is being totaled, and suddenly the conversation shifts from repairs to settlement, title transfer, and whether the car is worth saving.

That call is stressful because it changes the problem. Before the call, you were dealing with damage. After the call, you're dealing with ownership, value, title branding, and next-step risk. Those are very different issues, and they need different questions.

What owners usually want to know first

Readers don't care about the legal phrase first. They want practical answers:

- Can I keep the vehicle: If you want to retain it, what does Montana require before it can ever go back on the road?

- Can it be driven now: A damaged vehicle with a salvage status is not the same thing as a road-ready rebuilt vehicle.

- Will insurance cover it later: Repairing the car is only one part of the decision.

- Am I being underpaid: The total loss offer affects every option that comes after it.

A total loss decision doesn't automatically mean the vehicle is worthless. It means the insurance claim has moved into a different category, and your choices need to be evaluated differently.

Why this moment matters financially

A rushed decision here can cost more than the accident itself. Owners sometimes accept a weak settlement, keep the car because the buyback sounds affordable, then discover the paperwork trail is harder than expected and the finished vehicle is still worth less because of the branded history.

The right move depends on three things. First, the vehicle's pre-loss market value. Second, the quality and cost of repairs. Third, your tolerance for a longer process that includes inspection, documentation, and future insurance headaches.

If you understand the Montana rules early, you stop reacting and start deciding.

Salvage vs Rebuilt Titles in Montana

The biggest point of confusion is simple. A salvage certificate and a rebuilt salvage title are not the same thing.

Imagine a damaged house. One status means the property has serious issues and isn't ready for normal occupancy. The other means someone repaired it, documented the work, and cleared the required process to put it back into lawful use. That same basic distinction applies to a montana salvage title situation.

The difference that matters

A salvage certificate is the branding that follows a total loss event. It identifies the vehicle as one that has been declared salvage. It is primarily an ownership and administrative document.

A rebuilt salvage title is what comes later, after the vehicle has been repaired and passed Montana's required inspection and title conversion process. That later title is what makes legal registration and ordinary road use possible again.

For a broad primer on how salvage branding works across the industry, this overview of what a salvage title means is a useful starting point.

Montana Salvage vs. Rebuilt Title Comparison

| Attribute | Salvage Certificate | Rebuilt Salvage Title |

|---|---|---|

| Legal status | Identifies the vehicle as salvage | Shows the salvage vehicle has completed the required retitling path |

| Road use | Not the status owners should assume is road-legal | Used after the vehicle clears the required process for legal operation |

| Registration path | Not the endpoint for normal registration | The title status owners pursue to register and drive again |

| Inspection role | Starts the paper trail | Follows repair and inspection requirements |

| Insurance reality | Often difficult to place in ordinary coverage channels | Usually easier than pure salvage status, but still subject to branded-title limits |

| Market perception | Seen as damaged and unresolved | Still branded, still discounted, but more usable than salvage-only status |

What doesn't work

What doesn't work is assuming repairs alone solve the problem. They don't. A mechanically sound car can still be stuck if the paperwork is incomplete, the title path wasn't handled correctly, or key receipts are missing.

Practical rule: In Montana, a repaired vehicle isn't the same thing as a retitled vehicle. The document trail matters as much as the repair work.

That's why owners get frustrated. They spend money on parts and labor, then discover the state is looking for proof of identity and part ownership, not a verbal explanation that the car was “fixed up.”

What Happens After a Total Loss Declaration

Once the insurer declares the vehicle a total loss, the claim shifts from repair administration to settlement and title handling. Many owners then lose track of who has to do what.

If the insurer acquires the vehicle as part of the settlement, Montana law places a specific duty on the insurer. Under Montana Code Annotated 61-3-211, when an insurer acquires a vehicle less than 15 years old, it must apply for a salvage certificate. The application must include the assigned title unless the insurer can show it made at least two attempts to obtain that title from the owner after the settlement was accepted.

Your role in the paperwork

From the owner's side, the practical issue is simple. If the insurer is taking ownership, title paperwork becomes part of finishing the claim. Delays often happen because the owner still has a lien payoff question, can't locate the title, or doesn't understand why the insurer keeps asking for signatures after the vehicle has already been declared totaled.

That confusion is normal. A total loss declaration does not complete the ownership transfer by itself.

A solid overview of the insurance side of this transition appears in this guide to what happens when your vehicle is totaled, especially if you're trying to understand where the title issue fits inside the larger claim.

When the claim isn't a standard crash loss

Some claims become more complicated because the vehicle was stolen, recovered, moved, or stored before the valuation was resolved. In those situations, owners often benefit from seeing the claim process from a different angle. This car theft insurance claim guide is useful background for understanding how documentation, possession, and insurer procedures can shape the next step.

Don't hand over title documents casually, and don't ignore them either. Review the settlement terms first, then make sure the paperwork you sign matches the outcome you actually agreed to.

Where owners get stuck

These are the most common choke points:

- Missing title issues: The insurer may need the assigned title, or proof that efforts were made to obtain it.

- Lienholder delays: A lender's interest can slow the transfer process.

- Retained salvage confusion: If you keep the vehicle after settlement, the title path changes and the owner's responsibilities increase.

- Settlement timing disputes: Owners sometimes think title transfer pressure means they must accept the first offer. It doesn't.

The title process and the valuation process are connected, but they are not the same negotiation. Keep them separate in your mind.

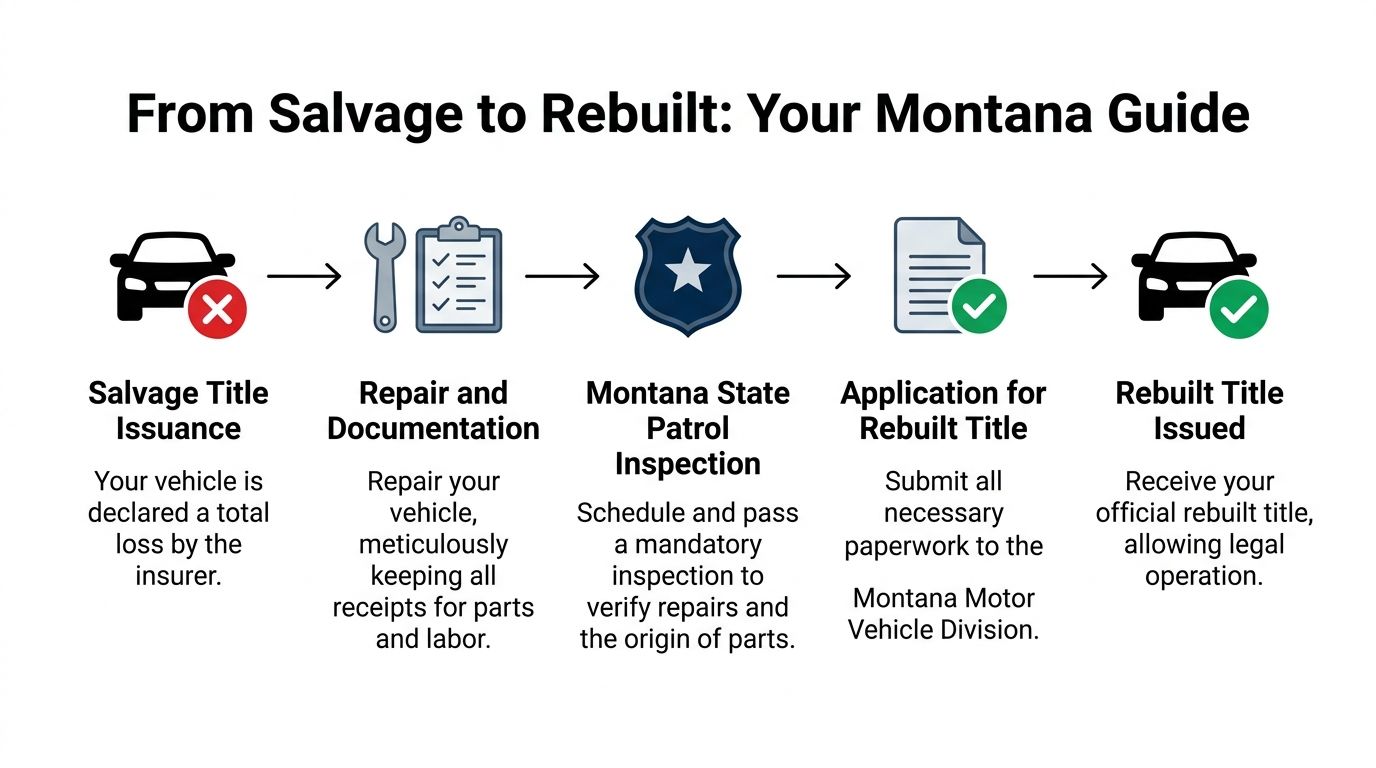

Your Step-by-Step Guide to a Rebuilt Title

You get the car back from the body shop, it looks straight again, and the hard part feels over. In Montana, that is usually the point where title problems start. A rebuilt title is won or lost on paperwork, part sourcing, and inspection prep just as much as repair quality.

Treat the process like an audit from the first day.

Step one, confirm the vehicle is actually on the salvage path

Before you order parts or authorize paint, verify the current title status and confirm what document Montana expects next. Owners often assume a repairable total loss automatically becomes a rebuilt title case. The state process starts with salvage status first, and your file has to match that status all the way through.

The filing cost itself is small, as noted earlier. The primary expense is the decision to rebuild. Parts, labor, storage, rental coverage ending before the car is done, and reduced resale value matter far more than the state fee.

If you are financing the repair yourself, pause here and run the numbers realistically. I have seen owners spend replacement-car money trying to save a familiar vehicle, then end up with a car that is harder to insure and worth less at resale.

Step two, rebuild with receipts in mind

Repair quality matters, but documentation is what gets the title over the line. Montana wants a clear trail showing what the vehicle is, who owns it, and where the replacement parts came from.

Keep these items together from the start:

- Salvage certificate: This is the foundation of the rebuilt-title file.

- Bills of sale for the vehicle: Save every ownership document tied to the car.

- Detailed parts receipts: Major component purchases should be easy to trace.

- Repair records: Shop invoices and work orders help explain what was repaired and when.

One missing receipt can hold up an otherwise solid application.

The risk is higher if you buy used parts from private sellers, swap components between vehicles, or rely on cash transactions with thin paperwork. Those choices can save money on the front end, but they create inspection problems later. If you use recycled parts, make sure the invoices identify the part, seller, and vehicle information clearly enough to answer questions.

Step three, get ready for the Stage III inspection

Montana requires a Stage III VIN inspection before a rebuilt title can be issued. According to Montana's VIN inspection guidance, you must present the salvage certificate, bills of sale for the vehicle, and detailed receipts for all component parts used in the rebuild.

That inspection is narrower than many owners expect. It is centered on identity and lawful ownership of the vehicle and its major parts. It is not a blanket endorsement that every repair meets your insurer's standards or that the car is free of mechanical issues.

That distinction matters. A vehicle can look finished and still fail to move through the title process if the paperwork is sloppy or incomplete.

A quick visual summary can help if you're mapping the sequence before scheduling anything:

Step four, submit a clean rebuilt-title package

Once repairs are complete and the inspection is done, submit the retitling paperwork with the same care you would give a tax filing. Names, VINs, dates, ownership documents, and parts receipts need to match cleanly.

The most common delays are avoidable:

Receipts that are too vague

If an invoice says “parts” without identifying what was purchased, expect questions.Breaks in the ownership trail

A major component with no clear source tends to stop the file.Submitting before the file is complete

The car being repaired does not make the application ready.

I tell owners to lay every document out in order before they go in. If a stranger cannot follow the story of the vehicle from salvage to rebuild, the clerk or inspector may not be able to either.

Step five, decide whether the finished result still makes financial sense

A rebuilt title is legal clearance to put the car back on the road. It is not proof that rebuilding was the right financial decision.

Run the full comparison again after the repair estimate hardens. Include what you paid to retain the salvage, actual repair bills, towing, storage, rental gaps, inspection-related delays, and the lower market appeal that follows a branded title. In Montana, this step gets skipped too often. Owners focus on getting the car back, not on whether the rebuilt car will still protect their budget six months from now.

Some rebuilds pencil out. A well-maintained truck, a specialty vehicle, or a car with light cosmetic damage and well-documented repairs can justify the effort. A common commuter car with heavy structural damage usually deserves a harder look before you keep spending.

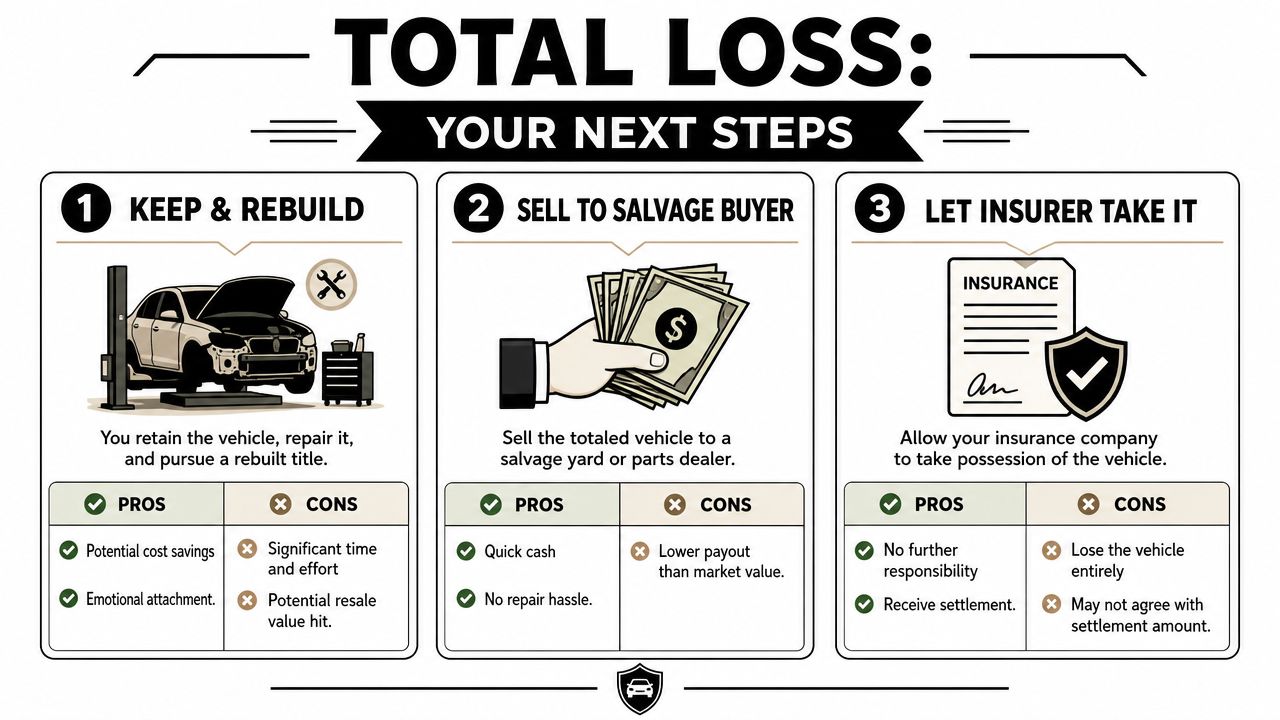

Your Three Options After a Total Loss

The hard part is not understanding the label "total loss." The hard part is deciding what to do next without giving away money or taking on a project that no longer makes sense.

In Montana, owners usually end up with three real choices. Keep the vehicle and rebuild it. Sell it in salvage condition. Or release it to the insurer and take the settlement. Each option carries a different mix of cash, delay, paperwork, and future value loss.

Option one, keep and rebuild

Keeping the vehicle can work well when the car has strong pre-loss value, the damage is repairable, and you have access to competent labor at a reasonable cost. I see this choice make sense most often with well-kept trucks, specialty vehicles, and cars the owner plans to keep for years rather than resell soon.

The filing cost for a salvage certificate is small, as noted earlier. The larger question is whether the full math still works after salvage retention, repairs, towing, storage, replacement parts, inspection preparation, and the lower resale appeal that follows a branded title.

That last piece gets missed. A vehicle can be fully roadworthy and still trade for less because buyers and lenders treat branded history cautiously. If you want a clearer sense of that market penalty, this explanation of how automobile diminished value affects resale after a loss is useful context before you commit to rebuilding.

Choose this path if these conditions are true:

- You have reviewed the insurer's valuation and believe the settlement is fair, or you have already pushed it higher.

- You have a repair plan based on actual estimates, not guesswork.

- You expect to keep the vehicle long enough to offset the branded-title discount.

- You can keep records organized from salvage retention through final inspection.

Option two, sell the vehicle in salvage condition

Selling the vehicle as-is gives you more control than surrendering it, without requiring you to fund and manage a rebuild. That can be the right call when the damage is heavy, parts availability is poor, or you do not want months of follow-up tied to one claim.

This option tends to protect time better than it protects top-dollar value. Salvage buyers price for risk, parts value, and auction alternatives. Owners who choose this route usually value speed, reduced hassle, and a clean break over trying to recover every last dollar.

A practical warning applies here. If your claim value is low, selling the salvage too quickly can lock in two weak numbers at once: a soft insurance settlement and a modest salvage sale.

Option three, let the insurer take the vehicle

For many owners, this is the cleanest exit. You settle the claim, sign the required transfer paperwork, and avoid the repair, title, and inspection process.

It is also the option that leaves the least room to recover value later. Once the vehicle is gone, your negotiating power is mostly tied to the settlement amount you accepted. That is why I tell owners to slow down long enough to check the valuation report, comparable vehicles, options, condition adjustments, and prior maintenance evidence before they sign.

If you expect to replace the vehicle right away, it also helps to compare coverage and replacement costs early. The PTL Insurance Associates auto guide can help you think through that side of the decision while the claim is still open.

A simple way to choose

Use four filters before you decide:

- Settlement value: Does the insurer's number reflect the vehicle you owned, including condition, mileage, trim, and recent work?

- Repair reality: Are the repair costs based on written estimates that account for supplements and hidden damage?

- Ownership horizon: Will you keep the vehicle long enough for a rebuilt title to matter less financially?

- Administrative burden: Do you have the time and discipline to handle title paperwork, receipts, inspections, and follow-up without errors?

If two or more of those answers are uncertain, pause. In Montana total loss cases, the best decision is often the one that protects your cash position first, then your transportation needs second.

How a Branded Title Affects Value and Insurance

A rebuilt vehicle can be useful transportation. It can also be a weaker financial asset. Those are both true at the same time.

The problem isn't only what was repaired. The problem is the title history. Once a vehicle carries a branded title, many buyers treat it as a different class of asset. They worry about prior damage severity, repair quality, hidden issues, and future financing or coverage limits. That hesitation tends to suppress what the vehicle can command in the market, even when the repairs were done correctly.

Why the settlement offer matters so much

This is why the total loss valuation deserves careful review before you agree to anything. If you retain the vehicle and move toward a rebuilt title, you're accepting a future in which the car may be harder to sell and harder to insure on the same terms as a clean-title equivalent.

That's the practical side of diminished value. For a deeper explanation of how post-loss market stigma affects what a vehicle is worth, this overview of automobile diminished value is worth reading.

Insurance is often a second negotiation

Even after a proper rebuild, coverage can become its own project. Some carriers are comfortable with liability-only coverage on rebuilt vehicles. Others may be more cautious with physical damage and collision, or they may want documentation and underwriting review before offering broader protection.

If you're comparing options after the rebuild stage, a general resource on shopping coverage like this PTL Insurance Associates auto guide can help you think through quote comparisons and carrier differences. The key is to ask direct questions about branded-title underwriting before assuming the policy you want will be available.

A rebuilt title can restore legal usability. It does not restore clean-title market perception.

Where expert help fits

If the insurer's value feels light, it often makes sense to get an independent opinion before making the keep-or-surrender decision. That can come from a certified appraiser, a repair professional with strong market knowledge, or a specialist who works with appraisal-clause disputes. One option owners look at in valuation disputes is Total Loss Northwest, which handles total loss and diminished value appraisal work and can be relevant when the disagreement is about market value rather than repair procedure.

That kind of help matters most before you lock yourself into a path that assumes the insurer's number was fair.

Protecting Your Investment and Moving Forward

The Montana title process is manageable when you stop treating it like a mystery and start treating it like a sequence. First, verify the settlement. Then decide whether keeping the vehicle makes financial sense. If you rebuild, document everything and expect the title process to care as much about receipts and inspection as the body shop cares about parts and paint.

Owners get into trouble when they focus on only one piece. Some chase the settlement check and ignore the title consequences. Others focus on fixing the car and underestimate how a branded history affects future value and insurance. The better approach is to evaluate the whole chain before you commit.

If you're dealing with a montana salvage title issue right now, protect your position in three ways:

- Question the valuation early: Don't assume the insurer's first number reflects its true market value.

- Choose the rebuild path carefully: It works best when the repair economics are solid and the vehicle is worth keeping long term.

- Keep documents like they matter: In Montana, they do.

The most expensive mistake is making a permanent decision during the most stressful part of the claim. Slow the process down enough to check the numbers, understand the title path, and decide from a position of control.

If your total loss offer feels low, or you need an independent opinion before deciding whether to keep or surrender the vehicle, Total Loss Northwest is one resource to consider. They provide total loss and diminished value appraisal support, and that kind of valuation work can help owners make a better-informed decision before a branded-title outcome affects the vehicle's future.