Your car is sitting in a tow yard or body shop. The insurer has already sent a number. It looks official, polished, and final.

It usually isn't.

Across Oregon and Washington, drivers get pushed into the same mistake. They assume the carrier's first valuation is close enough, then sign off before anyone checks the local market, the options package, the actual condition, or what that vehicle would cost to replace in the Pacific Northwest. That's where money gets left behind.

A Pacific Northwest auto appraiser isn't there to add drama to a claim. The job is to take a valuation dispute out of the insurer's software and put it back into evidence. In total loss cases, that can change the actual cash value. In diminished value cases, it can mean getting paid for the loss in resale value that the carrier would rather ignore. And when the policy allows it, the Appraisal Clause gives you a formal tool to force that dispute into a process the insurer doesn't control by itself.

Recognizing When You Need an Independent Appraiser

The call usually comes after the insurer sends a valuation report that looks polished, detailed, and hard to argue with. Then the owner starts reading it. Wrong trim level. Missing options. Comparable vehicles from the wrong market. Condition adjustments that do not match the car that existed before the loss.

That is the point to stop treating the claim like a routine transaction.

The lowball total loss offer

A weak total loss offer rarely announces itself as weak. It arrives in a formal report, often backed by vendor software and a list of supposed comparables. The problem is that those reports can be built on bad inputs. If the insurer starts with the wrong trim, misses factory equipment, pulls vehicles from outside your actual market, or grades pre-loss condition too harshly, the final number can be off by thousands.

Pacific Northwest claims have their own pressure points. Oregon and Washington vehicles often carry value differences tied to AWD demand, rust exposure patterns, mountain and coastal use, local retail scarcity, and buyer preference for certain trims and packages. A valuation model built for speed will miss those details unless someone forces the issue with evidence.

Watch for these warning signs:

- Comparables that do not compare, such as different drivetrains, trims, mileage bands, or title histories

- Factory or dealer-installed options left out of the valuation

- Condition deductions that read more like assumptions than documented facts

- A refusal to revise the report after you send better local examples

- Pressure to sign and release the claim quickly, before the valuation dispute is fully documented

If that is happening, it is time to bring in an independent car appraiser for Oregon and Washington claims.

The diminished value claim the carrier wants to minimize

Diminished value fights follow a different script, but the insurer's goal is often the same. Keep the number low enough that the owner gives up.

A proper repair does not erase accident history from the market. Buyers, dealers, and appraisers all account for it. That matters most with newer vehicles, luxury models, performance cars, collector vehicles, modified builds, and clean examples that had strong resale appeal before the loss. On those claims, a casual demand letter without support usually goes nowhere. A market-based appraisal gives you a method, not just an opinion.

I have seen plenty of owners lose ground here because they argued fairness while the carrier argued formulas. Insurance companies are comfortable in that fight. They are less comfortable when the file contains documented comparable sales, repair-history impact, and a valuation analysis they have to answer point by point.

Practical rule: If the insurer has a report and you have a hunch, the insurer controls the conversation.

What usually tells you to get outside help

You do not need an appraiser for every claim. You do need one when the gap is real and the insurer is treating its number like the last word.

That tends to be the case when the vehicle is unusually clean, hard to replace, modified, classic, high-trim, or affected by local Pacific Northwest demand that generic software does not measure well. It also shows up when the adjuster keeps repeating the same valuation without addressing your evidence. At that point, the dispute is no longer about simple clarification. It is adversarial.

That is the part many drivers miss. The carrier may sound cooperative while still defending a number that saves it money. An independent appraiser changes the posture of the claim. Instead of asking the insurer to reconsider, you start building a record that can support formal action under the policy.

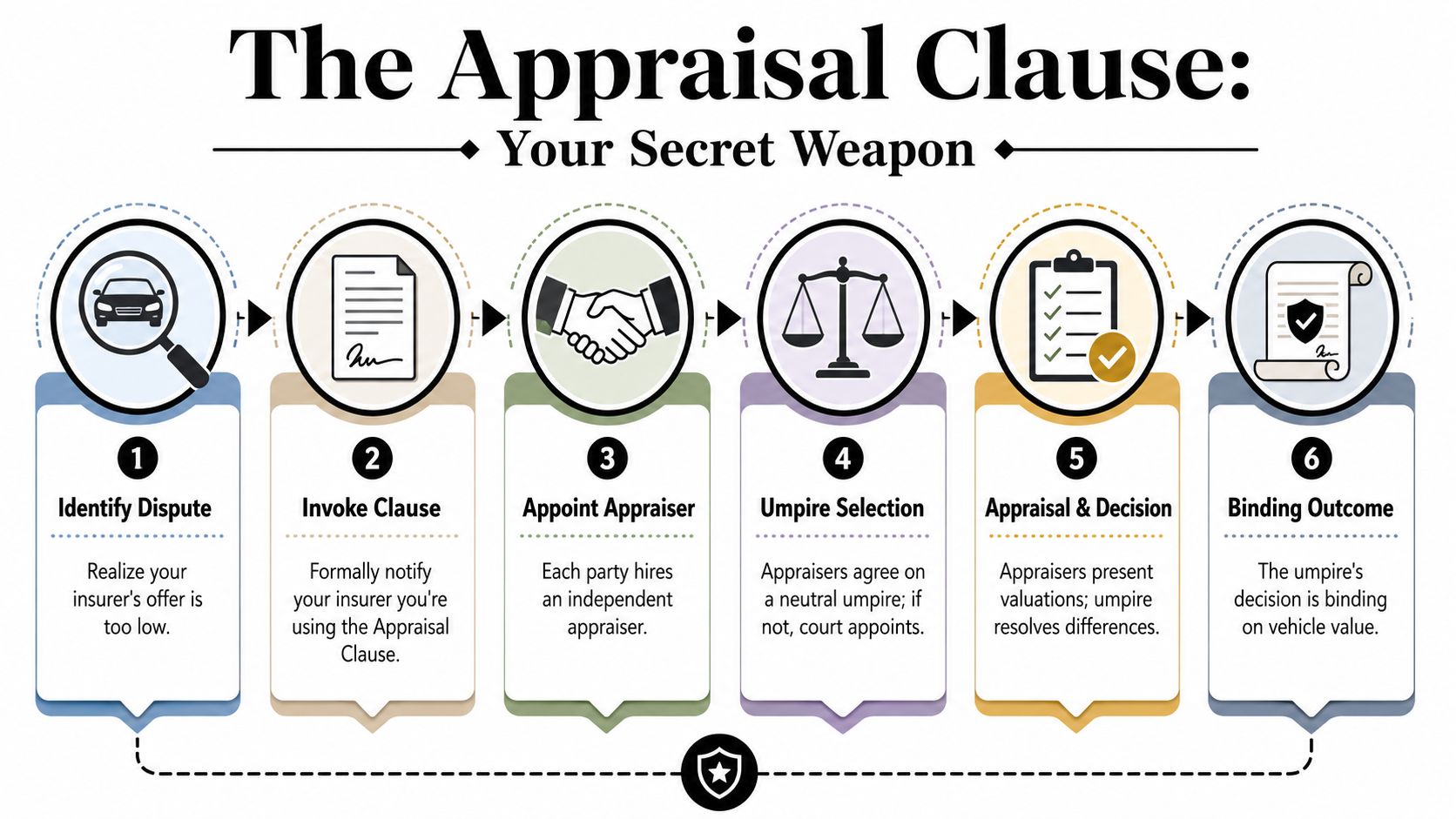

The Appraisal Clause Your Secret Weapon

Many policyholders have never heard of the Appraisal Clause until a valuation fight is already underway. That's unfortunate, because in the right claim it's one of the few tools that changes the balance of power.

The clause is part of the insurance contract. It exists for valuation disputes. In many auto policies, each side gets to choose an independent appraiser, and if those appraisers can't agree, a neutral umpire steps in. In the Pacific Northwest market, firms describe this as a binding process for disputes over vehicle value, including total loss, diminished value, and repair estimate disagreements, as explained by IAS Northwest's appraisal services overview.

Where to find it and why it matters

Look in your policy under terms like appraisal, dispute resolution, or conditions. You're looking for language that explains what happens when you and the insurer disagree on the amount of loss or value.

That language matters because it takes the claim out of a one-sided loop. Without the clause in play, the insurer can keep repeating its valuation position and force you to either accept it or escalate in less efficient ways. Once the clause is invoked correctly, the process becomes formal.

The Appraisal Clause doesn't guarantee a bigger payout. It guarantees a structured fight over value instead of a one-way conversation.

How the process usually works

The mechanics are straightforward even if the paperwork feels intimidating. Most claims follow a pattern like this:

A value dispute appears

You review the offer and identify a meaningful gap between the insurer's figure and market reality.The clause gets invoked

The policyholder or representative notifies the carrier in writing that the claim is being pushed into appraisal under the policy terms.Each side selects an appraiser

You hire your independent appraiser. The insurer selects its own.The appraisers compare evidence

They review comparables, options, condition, market adjustments, and any valuation methodology behind each number.An umpire may be selected

If the two appraisers remain far apart, they bring in a third neutral decision-maker.A binding value is reached

Depending on the policy language and the result of the appraisal process, the determined value becomes the number the claim moves forward on.

A practical starting point is learning how the insurance appraisal clause process works before you send anything to the carrier. The details matter.

What works and what doesn't

Some owners hurt their own case by invoking the clause too loosely. They send an angry email, attach random listings, and assume that's enough. It usually isn't.

What works is tighter and more disciplined:

- Use policy language carefully so the carrier can't pretend your request was informal

- Hire someone who handles valuation disputes, not just repair estimates

- Bring evidence, not opinion

- Stay focused on value, because appraisal is generally not the place to argue liability or bad faith

The biggest shift is psychological. Once appraisal starts, the insurer is no longer the only party framing what your vehicle is worth.

How to Choose a Certified Appraiser in Oregon and Washington

Not every appraiser is built for a disputed auto claim. Some are fine at describing a vehicle. Fewer can build a valuation file that stands up when an insurer pushes back.

In Oregon and Washington, the market has become specialized enough that independent appraisers explicitly market services for total loss claims, appraisal-clause disputes, and diminished value. One publicly listed provider even offers a flat fee of $550 for an appraisal, which shows how standardized this niche has become in the region, as noted on J&D's appraisal clause page.

What to look for first

Start with claim type experience, not marketing language. If your problem is a total loss valuation, you want someone who does total loss disputes routinely. If the issue is diminished value, you want someone who can explain post-repair market loss in a way that survives scrutiny.

Use this checklist when vetting a Pacific Northwest auto appraiser:

Local market knowledge

Ask how they account for Oregon and Washington comparables, not just national databases.Appraisal-clause experience

A person who only writes appraisals but never works disputed files may not be ready for insurer resistance.Documentation style

Ask whether the report includes comparable-sale support, option verification, condition analysis, and clear adjustments.Vehicle type familiarity

Classic, custom, lifted, performance, diesel, and specialty vehicles need different treatment than a standard commuter car.Fee structure clarity

Flat fees can be useful because you know the cost going in and can compare services cleanly.

Questions worth asking before you hire

Don't waste time with vague interviews. Ask direct questions.

| Question | Why it matters |

|---|---|

| Have you handled total loss and diminished value claims in Oregon or Washington? | It tests whether they know the regional market and carrier habits. |

| How do you support your opinion of value? | You want comparables, adjustments, and documentation, not a number pulled from memory. |

| Have you worked appraisal-clause disputes before? | Negotiated claims require a different skill set than basic valuation work. |

| What vehicles do you handle most often? | Specialty vehicles can expose weak appraisers fast. |

| Is your pricing fixed or open-ended? | Clear billing lowers the chance of surprise costs. |

A polished website doesn't prove an appraiser can defend a number. The report and the process do that.

Red flags that should make you walk away

Some warning signs are easy to miss:

- They promise a guaranteed increase

- They can't explain their comp selection

- They talk more about winning than documenting

- They treat all vehicles the same

- They dismiss the insurer's report without reviewing it closely

If you're comparing options, a directory-style starting point can help you narrow the field for an independent auto appraiser near you. Then call and test the person behind the service.

Preparing Your Case The Documentation Checklist

A strong appraisal file doesn't start with the appraiser. It starts with what you can hand over on day one.

When clients move quickly and gather the right material, the valuation work gets sharper. When they send half the story, the appraiser has to waste time chasing missing facts the insurer already has.

What to collect before the dispute gets messy

Get your documents together before phone calls turn into arguments. Keep everything in one folder, including screenshots and emails.

| Document | Why It's Important |

|---|---|

| Insurer valuation report | This shows the comparables, adjustments, and deductions that need to be challenged. |

| Settlement offer letter or email | It pins down the carrier's current position and prevents confusion later. |

| Full policy declarations and relevant policy language | The appraiser needs to verify the claim framework and whether appraisal language applies. |

| Photos of the vehicle before the loss, if available | These help establish pre-loss condition and rebut exaggerated deductions. |

| Accident photos | They help separate collision damage from prior condition issues. |

| Repair estimate or total loss paperwork | This gives context on how the insurer classified the claim and what it considered damaged. |

| Maintenance records | Service history supports condition, care, and sometimes buyer appeal. |

| Receipts for recent parts or upgrades | Tires, suspension work, audio, accessories, and other additions may affect value if properly documented. |

| Window sticker, build sheet, or option list | Missing options are a common reason insurer valuations come in low. |

| Title and registration | These confirm ownership details and vehicle identity. |

| Loan or payoff information | This doesn't determine value, but it affects settlement handling and timing. |

| Comparable listings you've found | Good local comps can help the appraiser identify where the insurer missed the market. |

Why owners lose leverage

The biggest self-inflicted mistake is sending documents one at a time over several weeks. That slows the file down and gives the insurer room to frame the vehicle before your evidence is organized.

A better approach is simple:

- Create one clean package with the insurer report at the top

- Label upgrades clearly so the appraiser can verify what was present on the vehicle

- Separate facts from opinions in your notes

- Keep all carrier communications because wording matters later

If you have receipts, photos, and maintenance records, don't assume the insurer will ask for them. They may not. You still need them in the appraisal file.

Special documentation for uncommon vehicles

Collector and modified vehicles need more than ordinary claim paperwork. If the car had custom wheels, performance parts, restoration work, rare trim, or unusually clean preservation, document each item as if nobody will give you the benefit of the doubt.

That isn't paranoia. It's how contested value claims work. The side with organized proof usually controls the discussion.

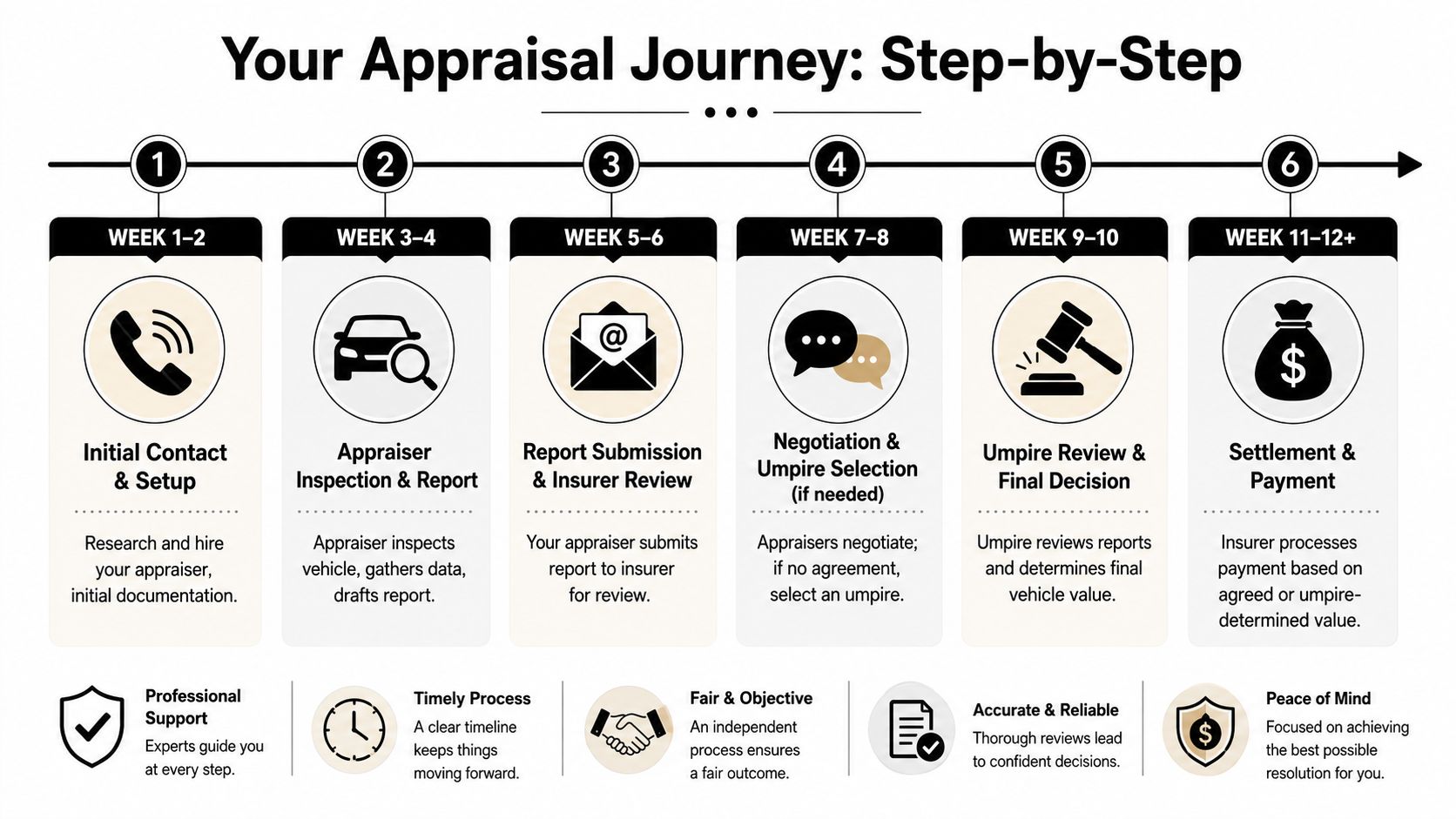

What to Expect from the Appraisal and Negotiation

Once the file is opened, most owners want two things right away. They want a quick finish, and they want certainty.

The process doesn't always give either one immediately. A disputed valuation usually unfolds in stages, and patience matters because rushed work is easy for the insurer to attack.

What happens first

The opening phase is mostly about intake and evidence review. The appraiser studies the insurer's valuation, confirms vehicle details, and identifies where the carrier's number may be vulnerable.

For many claims, that means checking:

- Comparable quality

- Trim and package accuracy

- Condition assumptions

- Local market relevance

- Any missing value factors tied to scarcity or modifications

Then comes report development. A defensible appraisal report should read like a case file, not a guess. It should explain why the selected comparables fit, how adjustments were made, and where the insurer's approach missed relevant facts.

What negotiation actually looks like

A lot of drivers imagine a dramatic standoff. Most of the time it's more technical than theatrical.

Your appraiser and the insurer's appraiser review the file, challenge each other's comparables, and argue over adjustments. Good appraisers don't just say a number is wrong. They show why the methodology behind it is weak.

The strongest appraisal reports don't rely on outrage. They rely on comparable-sale evidence, option verification, and adjustments that can be explained line by line.

If the two appraisers can't close the gap, the dispute may move to an umpire. At that stage, clarity becomes even more important. The better-organized report usually has the advantage because the umpire needs a record that makes sense without guesswork.

Timeline and client expectations

Appraisal disputes take time. They involve document exchange, report preparation, response periods, and sometimes umpire coordination. That's why owners should prepare for a process that unfolds over weeks rather than expecting a same-week correction.

What helps during that period:

- Respond quickly when your appraiser asks for missing records

- Avoid direct side arguments with the adjuster that undercut the formal process

- Stay consistent about the dispute being over value

- Read what you sign before accepting any settlement language

One factual option in this market is Total Loss Northwest, which handles certified independent appraisals for total loss and diminished value matters in Oregon and Washington and works within appraisal-clause disputes when applicable.

What the finish usually feels like

Sometimes the matter settles after appraiser-to-appraiser negotiation. Sometimes it reaches an umpire. Either way, the end result is usually less dramatic than people expect. The dispute narrows, the value gets set, and the carrier processes the claim on that number.

The primary difference is that you didn't let the insurer's first valuation become the last word.

Common Questions About PNW Auto Appraisals

Is an appraisal worth it on a smaller claim

Sometimes yes, sometimes no. The key question isn't whether the claim feels small. It's whether the valuation gap is meaningful after considering the cost, effort, and likely dispute path.

If the insurer missed major options, used weak comparables, or ignored a clear resale-value loss, an appraisal may still make sense. If the disagreement is minor and the documentation is thin, it may not.

Can you use this process if the other driver caused the crash

Often, the important issue is still value. In practice, many not-at-fault drivers run into the same low-valuation tactics whether the claim is being handled through the other party's carrier or under their own policy framework. The right path depends on the claim setup and policy language, so get the paperwork reviewed before assuming you can't challenge the number.

What vehicles benefit most from an independent appraiser

The need gets stronger when the vehicle is harder to value with generic software.

That usually includes:

- Classic vehicles with collector appeal

- Modified vehicles where added value is documented

- High-end trims with expensive option packages

- Scarce vehicles with limited local comparables

- Very clean examples where condition matters more than average-book assumptions

Will the insurer get hostile if you push back

Maybe. That doesn't mean you're wrong.

Valuation disputes are adversarial by nature. Once real evidence enters the file, the insurer may defend its number aggressively. That's normal. What matters is whether your side is organized, documented, and using the process correctly.

Should you negotiate on your own first

You can, and sometimes that works if the issue is obvious. But once the carrier starts digging in, repeated phone calls usually don't fix a valuation problem. Evidence does.

What's the biggest mistake drivers make

They settle too early. They see a formal report, assume it must be accurate, and don't test the comparables, options, deductions, or market assumptions underneath it.

If something about the number feels off, stop treating that instinct like a nuisance. In these claims, that instinct is often the first sign that the valuation needs to be challenged.

If you're dealing with a low total loss offer or a diminished value dispute in Oregon or Washington, Total Loss Northwest provides independent auto appraisal support built around market-based valuation evidence and appraisal-clause disputes. If you want to know whether your claim is worth challenging, start by having the valuation reviewed before you sign anything.