You got the call. The adjuster sounded calm, efficient, almost helpful. Then the number hit your inbox, and it felt detached from reality.

That reaction is justified.

When an insurer puts a low value on your vehicle after a crash, they're not handing you a neutral truth. They're giving you a position. Your job is to challenge it with better evidence, cleaner procedure, and zero hesitation. If you live in Oregon or Washington, that means using the process to your advantage instead of arguing in circles with an adjuster who works from software, templates, and payout pressure.

The Post-Accident Sticker Shock

The most common mistake I see is emotional surrender disguised as practicality. Your car was hit, your schedule is wrecked, and the insurer knows you want this over with. So they send a number that looks official and hope you treat it like a fact.

It isn't.

Post-collision valuation is the process of determining what your vehicle is worth after a crash, either for a total loss payout or for the loss in value that remains after repairs. That number affects what lands in your pocket. If the insurer controls the inputs, they control the outcome unless you push back.

This isn't a rare problem. Road traffic injuries remain a massive global issue, with the World Health Organization estimating about 1.19 million deaths each year and 20 to 50 million non-fatal injuries, and the automotive collision repair market was estimated at USD 199.56 billion in 2023, with the United States alone at USD 36.66 billion in 2023 according to the World Health Organization road traffic injuries fact sheet. You're not dealing with an unusual dispute. You're dealing with a systemized one.

If injuries are part of your claim too, get legal guidance early. A firm handling motor vehicle collision representation can help when the vehicle damage fight overlaps with bodily injury, liability, or settlement timing.

What the first offer usually means

The first valuation usually tells me three things:

- The insurer moved fast: Speed helps them more than it helps you.

- The report probably relies on selected comparables: If those comps are wrong, the value is wrong.

- They anticipate that many will accept it: Many do.

You need a better frame. The insurer's number is an opening bid, not the finish line. If your dispute involves a total loss payout, start by understanding how actual cash value works in practice with this guide on auto insurance actual cash value.

Don't argue that the offer “feels low.” Show exactly where the valuation is wrong.

That's how you stop reacting and start negotiating.

How Insurers Determine Your Vehicle's Value

Insurers love the phrase “market value” because it sounds objective. In practice, their valuation is only as good as the data, condition adjustments, and comparable vehicles fed into the report.

That's why you need to read the report like an appraiser, not like a customer.

The software is not neutral

Most carriers use valuation platforms and standardized reporting systems. The report may look polished, but polished isn't the same as accurate. The software selects comparable vehicles, applies condition adjustments, and can miss trim differences, package options, exceptional maintenance, local demand, and real-world replacement difficulty.

That's why I tell clients to stop saying, “The computer must know.” It only knows what was entered and what was ignored.

If you want a plain-English breakdown of how pricing logic works before you challenge a report, this piece on mastering vehicle valuation is useful background. Then compare that framework to the insurer's actual report, line by line.

The 17c formula pushes diminished value down

For diminished value claims, insurers often lean on formulas that limit what you can recover before the argument even starts. A widely used method is the 17c formula, which caps diminished value at 10% of the vehicle's pre-loss market value. Kelley Blue Book explains that on a $25,000 car, the starting ceiling is $2,500 before additional reductions for damage severity and mileage, and the mileage multiplier falls to 0 at 100,000 miles or more in the formula's structure, as outlined in Kelley Blue Book's explanation of diminished value calculations.

Here's the problem. That formula doesn't ask what your actual local buyer would pay after seeing an accident on the history report. It starts by limiting the claim.

Practical rule: If the insurer uses a formula, inspect the assumptions before you inspect the final number.

Where lowball reports usually break

A weak valuation report often has one or more of these defects:

- Bad comparables: Different trim, mileage, condition, or market area.

- Missing equipment: Packages, upgrades, or features left out.

- Condition downgrades: The insurer marks your pre-loss condition lower than it really was.

- Generic adjustments: They apply broad deductions without proving they fit your vehicle.

- Replacement mismatch: The comp cars don't reflect what it would take to buy a similar vehicle today.

If your claim is a total loss, review how carriers build and defend those reports in this guide on how an insurance company values a car.

Your counter isn't “I disagree.” Your counter is “Comp 2 has different equipment, Comp 4 is not local, your condition rating is unsupported, and your report omitted documented value.”

That's how this gets fixed.

Total Loss vs Diminished Value Claims

After a crash, your claim usually falls into one of two buckets. The money fight is different in each one, but the insurer's incentive is the same. Keep the valuation low.

The side-by-side reality

| Claim type | What happened to the vehicle | What the insurer focuses on | What you need to prove |

|---|---|---|---|

| Total loss | The vehicle is declared a total loss | Actual cash value before the crash | The report understates true market value |

| Diminished value | The vehicle is repaired but stigma remains | Whether any remaining loss should be paid | The repaired vehicle still lost market value |

Total loss means the payout lives or dies on ACV

In a total loss case, the insurer pays based on its view of your vehicle's pre-loss value. If they understate that number, your settlement drops immediately. At this point, bad comparables, missing options, and lazy condition ratings do the most damage.

Owners of high-value, collector, or custom vehicles get hit hardest because automated systems often fail to price them correctly. Industry material notes that automated valuation software can miss unique options, restoration quality, and local scarcity, which is why an independent appraisal matters when standard systems don't reflect true replacement cost or market value, as discussed in this Quality Collision Group article on valuation and data-driven outcomes.

Diminished value is about the loss that remains

A diminished value claim applies when the car is repaired, but the market still treats it as worth less because it now carries accident history, a fact that blindsides many people. They assume good repairs erase the loss.

They don't.

A buyer looking at a clean-history vehicle and a repaired accident-history vehicle does not treat them the same. That difference is the claim.

For a deeper look at the repaired-vehicle side of post-collision valuation, read this overview of automobile diminished value.

A repaired car can be safe, functional, and professionally restored. It can still be worth less in the market.

Which claim needs more scrutiny

If your vehicle is ordinary, current, and easy to match, a total loss dispute may be more straightforward because the replacement market is easier to document.

If your vehicle is newer, rare, customized, restored, or unusually clean for its age, both claim types deserve close review. Insurer systems tend to flatten important details. Your case gets stronger when you force the valuation back into the actual market instead of the insurer's template.

Your Right to a Fair Appraisal

Many individuals never use the strongest tool in their own policy because nobody points it out when the claim starts.

That tool is the appraisal clause.

When the fight is about value, not coverage, the appraisal clause can let you challenge the insurer's number through a structured process. You hire your appraiser. The insurer hires theirs. If those appraisers disagree, an umpire can break the tie. That changes the conversation fast because the insurer can no longer hide behind “our system says so.”

Why this matters in repaired vehicle cases

A big consumer blind spot is believing that a car is made whole once the body shop finishes the work. It often isn't. Independent industry references on collision-related valuation point out that a “fully repaired” car is not the same as one with fully restored market value, and that proving inherent diminished value takes evidence beyond the repair invoice, as explained by Collision Safety Consultants.

That evidence can include repair quality records, photos, parts details, frame measurements, paintwork documentation, and market-based support for the remaining stigma loss.

What the insurer hopes you won't do

They hope you'll keep arguing with the adjuster instead of invoking the process. Phone calls go nowhere because they cost the insurer nothing. A formal appraisal dispute creates work, deadlines, and independent review.

Use that advantage.

Here's the clean version of the process:

- Read your policy language for the appraisal clause.

- Put your dispute in writing and state that you reject the valuation.

- Hire an independent appraiser who knows total loss and diminished value methodology.

- Force the disagreement into the contract process if the insurer won't fix the number voluntarily.

If your damage involves a specialty vehicle, the principle is the same. You need someone who understands the asset, the repair implications, and the market. That's why owners of larger specialty units often seek experts in areas like RV collision repairs when repair quality and post-loss value become more complicated than a standard passenger vehicle claim.

The insurer already has a valuation professional in the room. You should too.

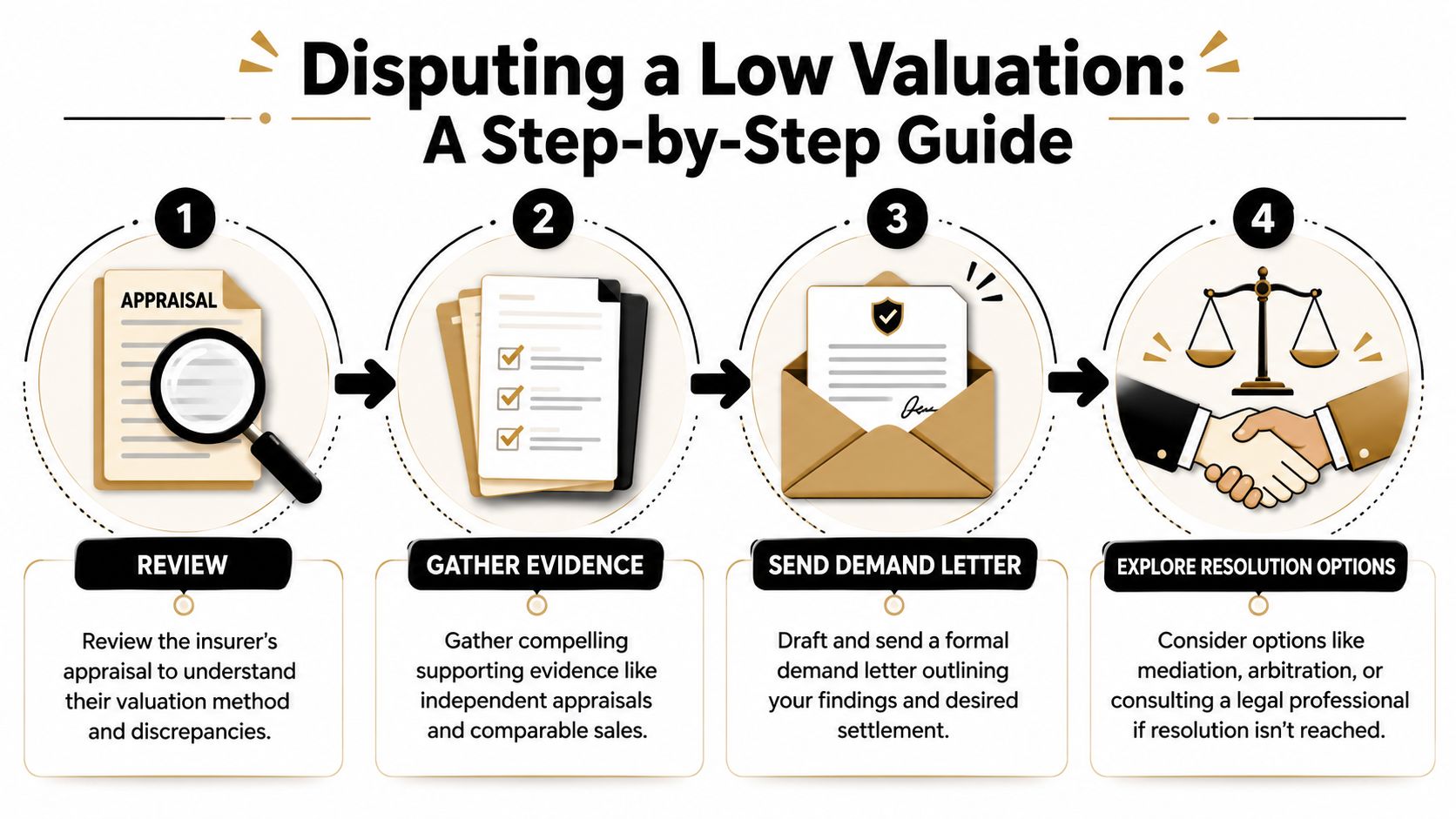

Disputing a Low Valuation Step by Step

You open the insurer's report and the number is thousands below what your vehicle would have sold for the day before the crash. That jolt is real. The mistake people make next is arguing on the phone and hoping the adjuster suddenly gets reasonable.

That rarely works.

A low valuation gets fixed when you challenge it in a disciplined way, on paper, and under the rules that apply in your policy and state.

Step 1: Protect your position before you touch the money

If the insurer sends a check, slow down. Read the letter that came with it. Look for any release language, final payment wording, or statements suggesting the claim closes once you endorse or deposit the check.

Do not guess. Ask a direct question in writing: “If I deposit this check, do you treat that as acceptance of your valuation?” Keep the answer.

That one email can prevent a bad argument later.

Step 2: Reject the valuation in writing, clearly and fast

Send a short dispute letter or email. Do it before the file goes stale and before the adjuster can say you accepted the number by silence.

Your message should do three things:

- Reject the amount: “I dispute your valuation and do not accept it as my vehicle's fair market value,” or, if applicable, “fair diminished value.”

- Identify the reason: “Your report relies on inaccurate comparables, unsupported adjustments, or missing equipment and condition details.”

- Reserve the next step: “Please reconsider the valuation. If this is not corrected, I will use the appraisal process available under the policy.”

Keep it firm. Keep it factual. You are creating a record the supervisor, appraiser, or arbitrator may read later.

Step 3: Audit the report line by line

Insurers count on owners reacting to the total number and missing the bad inputs that produced it. Go after the inputs.

Review the report for these common problems:

- Wrong vehicle description: trim level, drivetrain, engine, packages, title brand status, mileage, or factory options

- Bad comparables: vehicles with different equipment, accident history, condition, location, or asking prices that were never market-tested

- Weak adjustments: deductions for condition or prior damage with no photos, inspection notes, or repair support

- Missing value factors: new tires, service history, documented upgrades, rare options, or strong pre-loss condition

Write your objections next to each issue. Specific beats emotional every time.

Here's a practical explainer if you want to hear the dispute mindset in plain language:

Step 4: Send a counter-package that is easy to approve

Do the adjuster's work for them. If your evidence is scattered across texts, photos, and half-explained screenshots, your file stays weak. If your package is clean and organized, it becomes much harder for the carrier to ignore.

Use this order:

- A short demand letter with the value you believe is supported

- Corrected comparable vehicles with notes showing why they better match your car or truck

- Proof of condition and equipment such as photos, maintenance records, window sticker details, and receipts

- Repair and damage records if the dispute includes diminished value

- An independent appraisal if the insurer still refuses to move

This is an effective point to bring in an independent appraiser. In Oregon and Washington, that matters even more because a formal appraisal dispute can force the carrier to defend its number through the policy process instead of hiding behind repeated adjuster emails.

Step 5: Invoke appraisal when the insurer stalls

Once the carrier has your written dispute and support, stop repeating yourself. If they keep recycling the same number, invoke the appraisal clause in writing.

Be direct. State that you and the insurer disagree on value and that you are formally demanding appraisal under the policy. Ask them to confirm their appraiser and the next required step.

This changes the pressure. The claim moves out of the casual back-and-forth the insurer prefers and into a contract process with independent valuation work. That is how low offers get overturned.

If you live in Oregon or Washington, treat delay as part of the strategy you are up against. The insurer benefits when you get tired, cash the check, or miss the window to press the dispute properly. Do not let that happen. Put every objection in writing, support it with documents, and force the valuation issue into the process the policy allows.

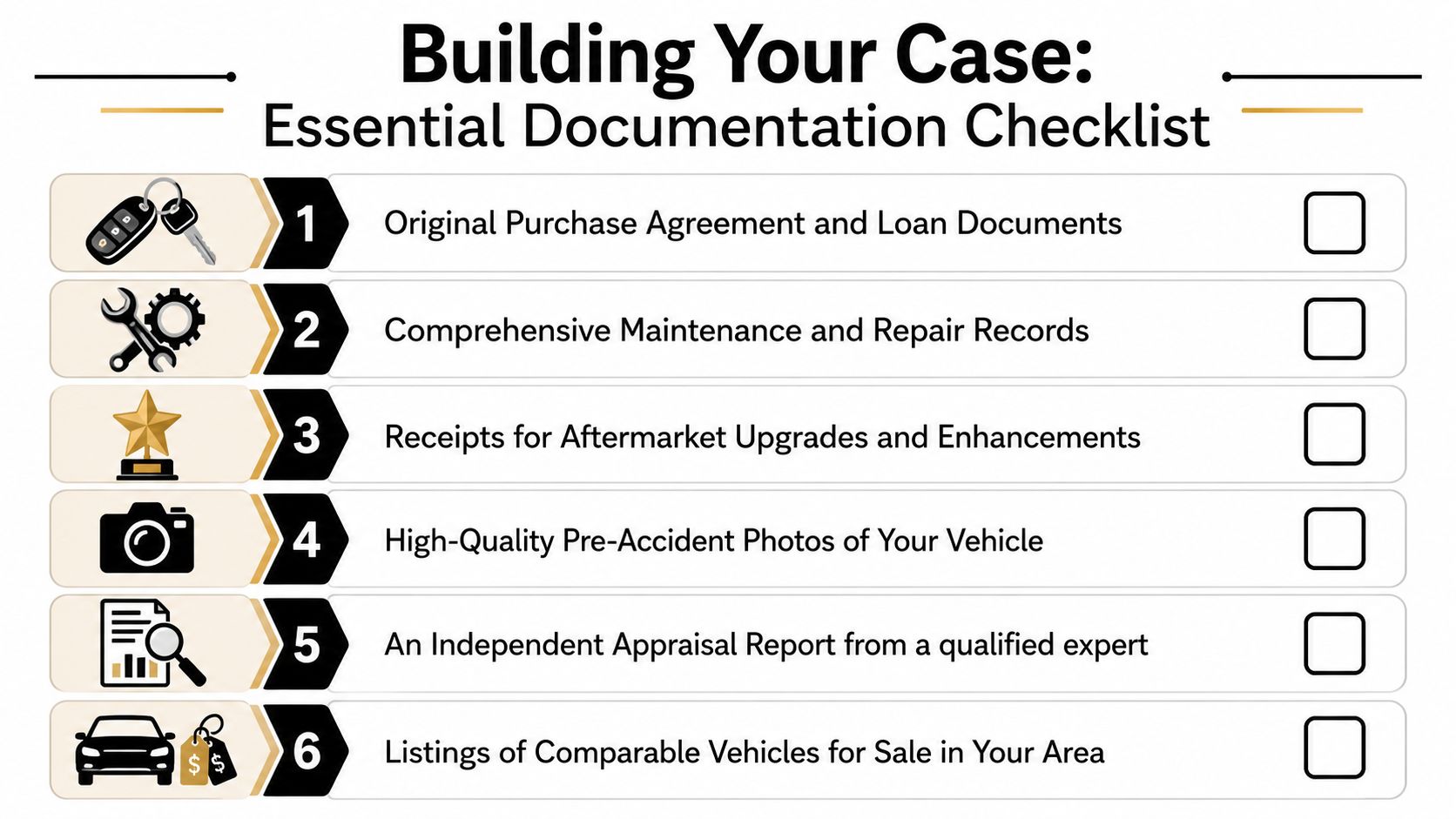

Building Your Case with The Right Documents

Valuation disputes are won on paper. If your file is thin, the insurer's report keeps the upper hand. If your file is organized, specific, and documented, their shortcuts become obvious.

The documents that actually move the number

Gather the file like you're preparing for a formal review, because that's what you're doing.

- Purchase and ownership records: Bill of sale, financing paperwork, title documents, and any paperwork showing original equipment or package details.

- Service history: Oil changes, major maintenance, brakes, tires, suspension work, dealership inspections, and any records that prove consistent care.

- Upgrade receipts: Wheels, premium audio, performance parts, bed covers, paint protection, towing equipment, or documented restoration work.

- Pre-accident photos: Exterior, interior, odometer, wheels, paint condition, and any angle that proves pre-loss cleanliness and condition.

- Insurer valuation report: This is not just their evidence. It's your roadmap for finding errors.

- Comparable listings: Similar vehicles offered in your market, with matching trim and meaningful equipment overlap.

Repair records matter more than most people realize

If the vehicle was repaired, don't stop at the final invoice. Collision industry guidance notes that the strongest valuation position is built from a complete repair file, including supplements discovered during disassembly, and from evidence that structural alignment, panels, suspension-related components, and paint matching were restored to pre-loss condition, as described by T and T Collision Centers on protecting vehicle value after repair.

That means you want:

- Initial estimate and supplements

- Parts invoices

- Frame or alignment measurements

- Paint and refinish documentation

- Before-and-after photos

- Any post-repair inspection results

Better documentation doesn't guarantee a higher settlement. It gives you something far more important. A valuation argument the insurer has to answer.

The file should tell one story

Your documents should make one point unmistakable. The insurer's valuation does not reflect the vehicle you owned or the loss you suffered.

If your paperwork is scattered, fix that first. A clean file changes how seriously your claim is treated.

FAQ Post Collision Valuation in Oregon and Washington

What are the total loss thresholds in Oregon and Washington

Insurers and state rules can treat total loss determinations differently depending on the facts, the carrier, and the vehicle. The practical point is this: don't assume the insurer's total loss decision or payout amount is self-proving. Even when everyone agrees the vehicle is totaled, the actual dispute is often the valuation, not the label.

If you're in Oregon or Washington, focus first on whether the insurer used accurate comparables, correct options, and a fair condition assessment.

Can you pursue diminished value if you were at fault

That depends on the claim path, the policy, and the legal posture of the loss. In many real-world situations, diminished value claims are most commonly pursued against the at-fault party's insurer rather than through your own policy. The key point is not to assume you have no option until someone reviews the facts and the policy language.

How does an independent appraiser strengthen your claim

An independent appraiser gives structure to your dispute. Instead of saying the offer is unfair, you present a valuation built on identifiable comps, documented condition, equipment verification, and repair-quality evidence where applicable.

That matters because insurers respond better to professional disagreement than to frustration. A credible appraisal also prepares you for appraisal-clause proceedings if negotiation fails.

What helps Oregon and Washington drivers the most

Four things:

- Act quickly: Delay gives the insurer momentum.

- Keep everything in writing: Phone calls disappear. Letters and emails don't.

- Document local market reality: Use vehicles that reflect your actual replacement market.

- Escalate when needed: If the adjuster stalls, move up the chain or invoke appraisal.

Is hiring an appraiser worth it

If the valuation gap is minor, maybe not. If the insurer missed major options, used weak comps, undervalued a clean vehicle, or ignored repaired-value stigma, professional help often changes the result because it changes the evidence.

The right question isn't “Do I want to pay for an appraisal?” The right question is “What does it cost me if I let the insurer's number stand?”

If you're in Oregon or Washington and the insurer's valuation doesn't match reality, get the file reviewed before you accept the offer. Total Loss Northwest provides independent total loss and diminished value appraisals, including appraisal clause support, for drivers who need a documented case instead of another argument with an adjuster.