The adjuster calls and says the words nobody wants to hear: your car is a total loss. You're still dealing with the crash, storage yard calls, rental issues, maybe work missed, and now there's a settlement number on the table that feels off.

A lot of owners focus on the vehicle's pre-loss value first. That matters. But another number often does quiet damage to the claim: salvage value. If the insurer sets that number too high, it can reduce what you receive or make the “keep the car” option far more expensive than it should be.

That's where people get blindsided. They hear a fast explanation, assume the number is fixed, and sign off. It usually isn't fixed. It's an estimate, and in Oregon and Washington total-loss disputes, that estimate can be challenged.

If you're staring at a low payout, or the insurer says you can retain the wreck only if they deduct a surprisingly large amount, you need to slow the process down and look at how they arrived at that figure. Even resources from outside the insurance world, such as guidance on smashed car removal Brisbane, can help illustrate a practical point: damaged vehicles still have a market, but that market depends heavily on condition, parts demand, and who is buying. A generic number rarely tells the whole story.

After the Crash Your Introduction to Salvage Value

When an insurer declares a vehicle a total loss, most owners assume the hard part is over. In practice, that's when the valuation fight starts. The carrier now decides what your vehicle was worth before the crash, what the damaged vehicle is worth after the crash, and how those numbers interact in the final settlement.

Salvage value assessment sits right in the middle of that process.

If the insurer takes the vehicle, salvage value affects what they expect to recover when they dispose of it. If you keep the vehicle, salvage value becomes a direct deduction from the settlement. That's why a lowball claim doesn't always come from only one bad number. Sometimes the pre-loss value is too low. Other times the salvage figure is too high. Sometimes both are wrong.

Where owners usually get caught off guard

The adjuster may present salvage value as if it's a standard administrative figure. It isn't. It's a market question. What would someone pay for this damaged vehicle, in this condition, through the channels where damaged vehicles sell?

That sounds simple until you have a specialty trim, aftermarket equipment, prior excellent condition, or severe impact damage that changed what parts are usable. Then the insurer's number can drift away from reality very quickly.

Your stress is real, but the settlement still has to be based on supportable market evidence, not just a software output.

Why this matters immediately

Owners in Oregon and Washington often have to make decisions fast. Release the car. Retain the car. Sign the power of attorney. Accept the deduction. Each of those choices can lock in the insurer's valuation assumptions before anyone has tested them.

A careful salvage value assessment helps answer two practical questions:

- If you surrender the vehicle: Is the insurer overstating what the wreck is worth to a salvage buyer?

- If you keep the vehicle: Is the insurer deducting more than a fair local market salvage amount?

When the answer is yes, you have grounds to challenge it.

Decoding Salvage Value What It Is and Why It Matters

Think of salvage value as the amount a dismantler, recycler, salvage yard, auction buyer, or specialized rebuilder might pay for your wrecked vehicle in its damaged state. They are not paying for a drivable car. They are paying for parts, metal, components, rebuild potential, or some mix of those.

Core definition: Salvage value is the market value of the damaged vehicle after the loss, not the value of the vehicle before the loss.

That distinction is why owners get confused. A total-loss claim involves two different valuations at once. One looks backward to the vehicle's pre-accident market value. The other looks at the remains.

Two claim paths that change the math

The first path is simple. You transfer the vehicle to the insurer. In that scenario, the insurer pays the covered value of the total loss and then disposes of the wreck through its salvage channels.

The second path is owner retention. You keep the vehicle. The insurer then deducts the salvage value from the settlement because you are keeping an asset that still has post-loss market value.

Here's the practical takeaway:

| Claim choice | What happens to the wreck | Why salvage value matters |

|---|---|---|

| Surrender the vehicle | The insurer takes title and sells the wreck | It influences the insurer's recovery position and often shapes negotiations |

| Keep the vehicle | You retain the damaged vehicle | The salvage amount is usually deducted from your settlement |

Why title issues matter too

Keeping a totaled vehicle often creates title branding and registration issues. Before you decide to retain the wreck, it helps to learn about salvage titles with VekTracer and also review Total Loss Northwest's explanation of what a salvage title means. Owners sometimes focus on getting the car back without thinking through inspection, rebuilding, financing, resale, and insurance consequences.

What works and what doesn't

What works is separating the issues. Pre-loss value is one issue. Salvage value is another. They need different support.

What doesn't work is accepting an adjuster's shorthand explanation that “this is just what the salvage number is.” If nobody can explain who would buy your specific damaged vehicle, where they would buy it, and why that figure fits the actual damage, the number needs more scrutiny.

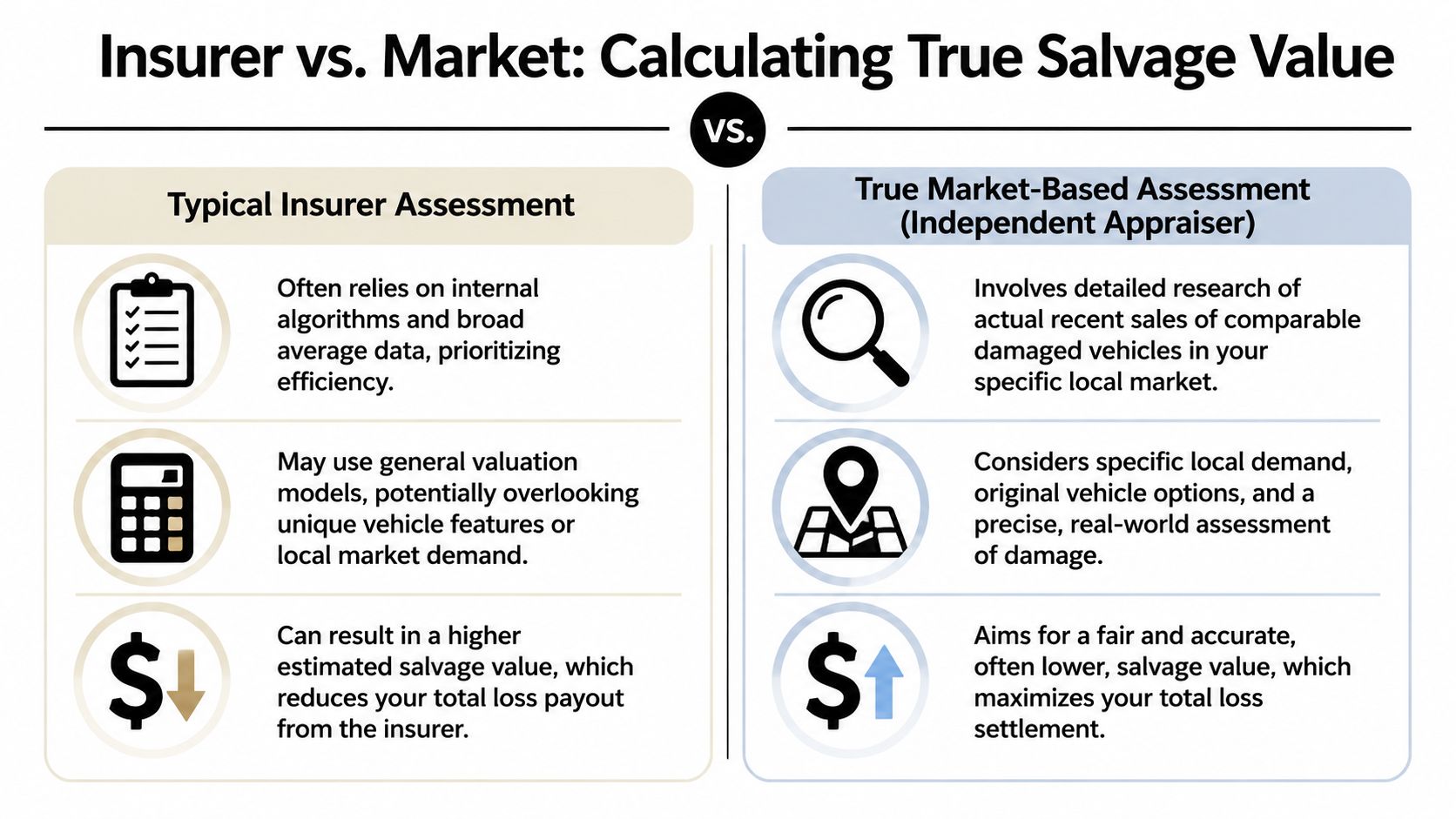

The Insurers Method A Look Behind the Curtain

Most insurers don't send a field appraiser out to build a fresh salvage market analysis from scratch on every total loss. They use systems, templates, historical returns, internal processes, and vendor-supported valuation tools. That approach is efficient. It also creates blind spots.

A claims department needs consistency and speed. The problem is that efficiency and accuracy are not the same thing, especially when the vehicle is unusual or the local salvage market has shifted.

How the number often gets built

In many files, the adjuster starts with a standardized workflow. Vehicle details go in. Damage type gets classified. The system references prior patterns, broad market assumptions, or auction-based logic. A salvage figure comes out that looks objective because it's tied to software.

The number may be useful as a starting point. It should not be treated as untouchable.

Here's where these systems usually struggle:

- Local demand: A damaged all-wheel-drive vehicle in the Pacific Northwest may have a different buyer pool than the same vehicle elsewhere.

- Usable parts mix: Front-end damage, water intrusion, suspension damage, deployed airbags, and driveline damage all affect what remains valuable.

- Pre-loss configuration: Trim level, drivetrain, factory options, and documented maintenance can matter to salvage buyers.

- Thin-market vehicles: Luxury, collector, custom, and heavily modified vehicles don't fit average databases well.

Why static assumptions age badly

Neutral industry guidance says salvage estimates should be reviewed when market conditions, asset condition, or planned service life changes materially. That matters because used-vehicle and parts markets don't stay still. The U.S. Manheim Used Vehicle Value Index was 208.2 in May 2025, down 4.7% year over year, which shows the market was still strong and supports the point that residual and salvage assumptions can move differently from older depreciation models (Tractian glossary on salvage value).

That doesn't mean every insurer number is wrong. It means an old rule-of-thumb approach can miss current market behavior.

A salvage figure that made sense under one set of market conditions may not make sense when buyer appetite, parts demand, or disposal channels change.

What owners should listen for

When an insurer explains its salvage value assessment, listen to the language. If you hear broad terms like “the system calculated it” or “that's the percentage we use,” ask the next question: what actual damaged-vehicle market evidence supports this figure?

If the answer stays abstract, that's usually the signal that the number came from a process designed to close files, not from a detailed analysis of your specific wreck.

That matters most when your vehicle doesn't fit the middle of the bell curve. A base commuter car with common damage is easier to model. A late-model SUV with expensive options, a performance vehicle, or a severely damaged unit with uncertain parts recoverability is not.

Calculating a True Market Salvage Value

A proper salvage value assessment starts in the market, not in a formula. The core question is practical: who would buy this damaged vehicle, through what channel, and for what amount?

That sounds basic, but it changes everything. Instead of assuming a percentage, an independent appraiser works outward from the actual buyer universe.

What a market-based review actually looks like

For vehicles with thin or distorted markets, such as higher-end, custom, or severely damaged cars, neutral appraisal guidance says the task is to determine whether there is a market for the damaged item, where buyers would look, and what comparable damaged items sell for. When standard comparables are missing, that may require auction houses, salvage stores, consignment channels, and online marketplaces (ISA appraisal guidance on determining salvage value).

That approach is more work. It's also closer to how real salvage buyers think.

The questions an appraiser should answer

A credible independent review usually asks questions like these:

- Damage scope: Which assemblies are destroyed, and which remain marketable?

- Buyer type: Is the likely buyer a dismantler, rebuilder, exporter, recycler, or specialty enthusiast?

- Channel fit: Would this vehicle move through a major salvage auction, a niche platform, a direct yard sale, or a specialist network?

- Vehicle specificity: Are there options, trim features, drivetrain components, or aftermarket parts that change salvage demand?

- Regional relevance: Does the Oregon or Washington market place different value on this type of damaged vehicle?

A side-by-side comparison

Here's a practical way to look at it:

| Approach | What it relies on | Common weakness |

|---|---|---|

| Typical insurer method | Standardized workflows, broad averages, internal disposal logic | Can flatten vehicle-specific differences |

| Independent market method | Actual damaged comparables, buyer outreach, channel-specific analysis | Takes more time and documentation |

A realistic example without invented numbers

Suppose a performance-oriented vehicle takes heavy rear damage. The insurer's process may classify it within a broad model family and generate a salvage number based on general auction expectations. A market-based appraiser may reach a different conclusion after finding that the rear impact compromised systems a rebuilder cares about, while also finding that some parts demand is stronger than average. The key is not whether the result goes up or down. The key is whether the conclusion is supported by actual market behavior.

That's why owners should ask for the underlying logic, not just the final figure.

Practical rule: If a salvage value can't be tied to real damaged-vehicle comparables or a defined buyer channel, it's not finished work.

For owners dealing with a total-loss dispute, it also helps to understand the broader valuation side of the file. Total Loss Northwest publishes a useful overview on how to calculate fair market value, which is separate from salvage value but closely related in negotiation.

What works best in difficult files

The hardest files are often the ones with the fewest clean comparables. That includes custom trucks, collector vehicles, luxury models, severe burn units, and heavily impacted newer cars with uncertain parts viability.

In those cases, the strongest salvage value assessment usually combines:

- Current damage documentation with clear photos and lot condition notes.

- Comparable damaged sales research from the channels where similar vehicles move.

- Buyer-type analysis that identifies whether the likely market is dismantling, rebuilding, or scrap.

- A written explanation connecting the evidence to the final opinion.

That process doesn't guarantee a fight-free claim. It does give you something far better than guesswork.

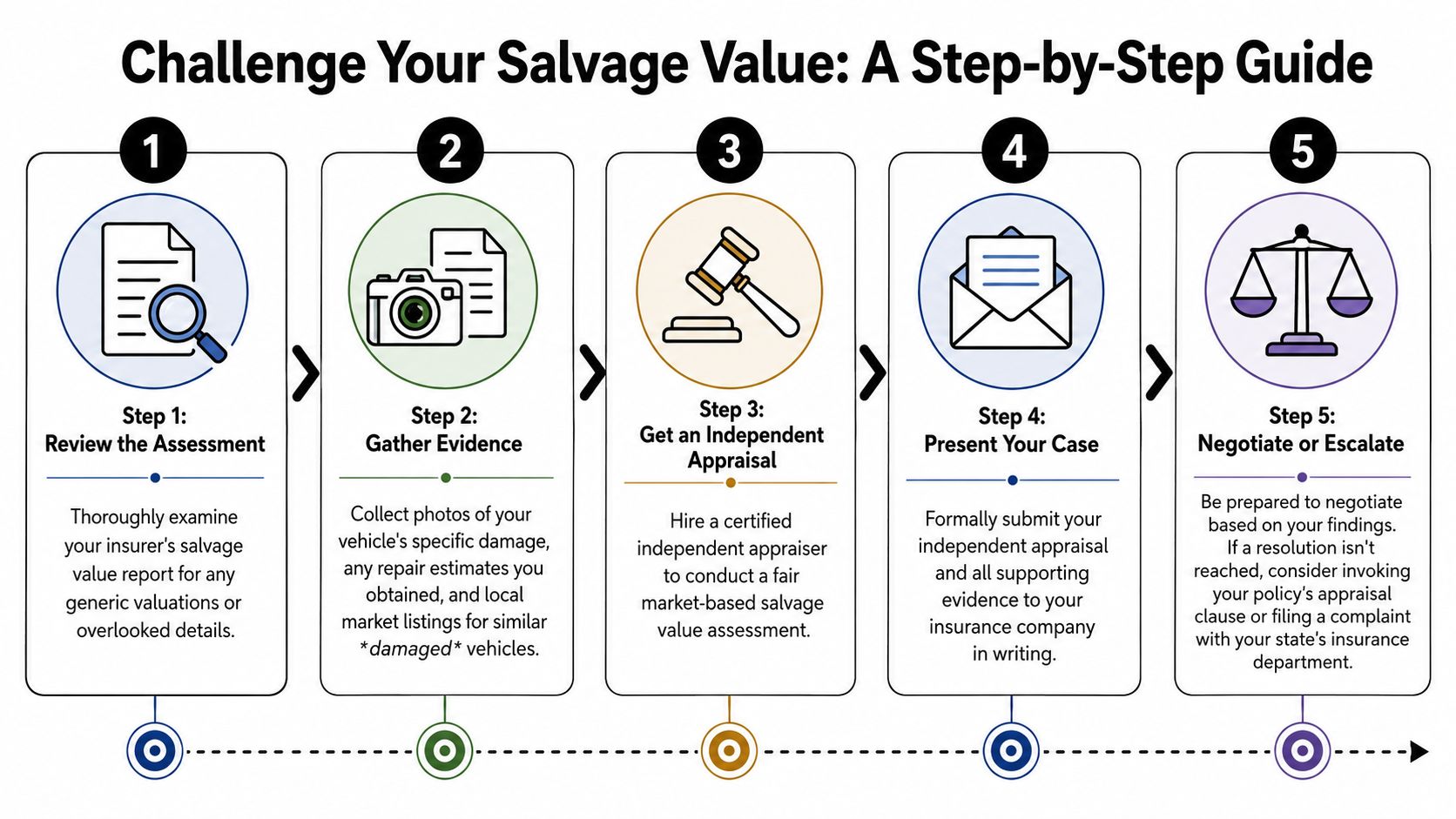

How to Challenge an Unfair Salvage Value Assessment

If the insurer's salvage number looks inflated, don't argue in generalities. Challenge it methodically. The goal is to move the discussion from “that's our number” to “show me the market support.”

The strongest disputes are organized, documented, and tied to the policy.

Start with the paper trail

Before you hire anyone, get the insurer's valuation material in writing. Ask for the total-loss valuation report, the salvage deduction if you're retaining the vehicle, and any explanation of how the salvage figure was derived.

Then review it for weak points:

- Missing vehicle details: Wrong trim, options, mileage assumptions, or condition notes.

- Generic damage descriptions: Labels that don't capture the actual extent of the loss.

- No market support: A number appears, but there's no evidence showing who would pay it.

- Wrong retention logic: The insurer deducts salvage value without clearly supporting owner-retention treatment.

Put your disagreement in writing

A phone complaint is easy to ignore. A written dispute isn't.

Send a concise letter or email that states:

- You disagree with the salvage value assessment.

- You want the insurer to identify the evidence supporting that figure.

- You reserve your rights under the policy, including the appraisal clause if available.

Keep the tone calm. Don't over-argue. You're creating a record.

If the insurer's number affects your payout, you're entitled to ask how that number was built.

Bring in an independent appraiser

Many claims turn when an independent appraiser evaluates the damaged vehicle, researches the actual salvage market, and prepares a report that challenges unsupported assumptions.

One option in Oregon and Washington is Total Loss Northwest, which handles total-loss appraisal disputes and can invoke the appraisal clause on behalf of policyholders. You can also work with another certified independent appraiser if that's a better fit for your case. What matters is that the person understands damaged-vehicle market valuation, not just pre-loss retail pricing.

A good appraiser will usually need:

- Photos of all damage

- The insurer's reports

- Tow yard or storage location information

- Vehicle build details and options

- Any information about aftermarket equipment or special condition before the loss

How the appraisal clause usually works

Many auto policies include an appraisal clause for valuation disputes. The wording varies, so read your policy. In general, the process works like this:

| Step | What happens |

|---|---|

| Policyholder invokes appraisal | You formally dispute the value and request appraisal under the policy |

| Each side names an appraiser | You choose your appraiser, and the insurer chooses theirs |

| Appraisers review the loss | They exchange information and try to reach agreement |

| If they can't agree | They select an umpire, who helps decide the disputed value issues |

That process can apply to total-loss disputes involving value components, including salvage-related disagreements, depending on policy wording and the issues in dispute.

A short explainer can help if this process is new to you:

What helps and what hurts

Helpful evidence is specific. Actual damaged comparables. Better damage photos. Yard condition. Missing components. Title status. Buyer-channel analysis.

Unhelpful evidence is broad. Clean retail listings. Random internet opinions. Arguments about what you still owe on the loan. None of that proves salvage value.

If negotiations stall, you can also consider a complaint to your state insurance regulator. That won't replace appraisal evidence, but it can matter if the claim handling itself becomes a separate concern.

Salvage Rules for Oregon and Washington Drivers

Owners in Oregon and Washington need to separate two issues that often get blended together in total-loss conversations. One is the claim valuation dispute. The other is the title and legal status of the vehicle after the loss. They overlap, but they aren't the same.

That distinction matters if you're thinking about owner retention.

What drivers should focus on first

The infographic above gives a quick visual comparison, but treat state-specific salvage and title handling as something to verify directly with the DMV, DOL, insurer, and your appraiser before you make a retention decision. Administrative treatment can affect whether you can register, rebuild, insure, or later sell the vehicle.

For Oregon and Washington owners, the practical checklist looks like this:

- Ask about title branding early: Don't wait until after you retain the vehicle.

- Confirm inspection requirements: A rebuilt path may involve procedural steps before the car returns to the road.

- Get the retention deduction in writing: You need the exact salvage amount and how it affects your settlement.

- Check lienholder issues: If there's a lender, owner retention may become more complicated.

- Understand constructive total loss logic: A vehicle can be uneconomical to repair even if it isn't physically destroyed. Total Loss Northwest has a useful explanation of constructive total loss for owners trying to understand that distinction.

The practical trade-off

Keeping a totaled car can make sense if you have a repair plan, access to parts, and a realistic view of the title consequences. It makes less sense when owners decide emotionally, then discover later that the deduction was too high and the vehicle is harder to put back on the road than expected.

That's why a fair salvage value assessment matters so much in Oregon and Washington. It isn't just an accounting detail. It can shape whether retaining the vehicle is financially sensible at all.

When to pause the claim process

Pause before signing if any of these are true:

| Warning sign | Why it matters |

|---|---|

| The salvage deduction feels high | You may be giving up claim value without market support |

| The insurer can't explain the number | The file may rely on generic assumptions |

| You want to keep the vehicle | Title, inspection, and rebuild consequences become central |

| The vehicle is unusual | Thin-market units often need a more careful appraisal |

If the insurer is moving quickly and the explanation stays vague, slow the process down. A rushed salvage decision is one of the easiest ways to leave money on the table after a total loss.

If you're in Oregon or Washington and the insurer's salvage number looks inflated, contact Total Loss Northwest for a review of your total-loss valuation and appraisal clause options. A qualified independent appraisal can clarify whether the salvage deduction is supported by the damaged-vehicle market or whether it should be challenged before you settle.