When a crash happens, what you do in those first few minutes is absolutely critical. It’s not just about safety; it’s about protecting your rights and setting the stage for everything that comes next. Your top priorities are simple: check for injuries, call 911, and make the scene safe.

Your First Moves at the Accident Scene

The moments right after a collision are a blur of adrenaline and confusion. It’s completely normal to feel disoriented and overwhelmed, but taking a deep breath and focusing on a few deliberate actions can make all the difference for your health and your eventual insurance claim. The main goal here is to prevent any more harm and start gathering the facts.

Prioritize Safety Above All

Before anything else, think safety—for you, your passengers, and everyone else on the road. If your car is still drivable, carefully pull it over to the shoulder or the nearest safe spot, well out of the way of traffic.

The second you're stopped, hit those hazard lights. It’s a simple flick of a switch, but it’s the universal signal for "caution" and can prevent a second, worse accident. This is especially true at night or in bad weather. If you have them, setting up reflective triangles or flares a good distance behind your car adds another crucial layer of visibility.

Assess Injuries and Call for Help

Next, do a quick check on yourself and anyone else in the car. Are you hurt? Is anyone else? Remember, adrenaline is a powerful painkiller. Serious injuries like whiplash, concussions, or internal bleeding might not be obvious right away.

If there's even a hint of an injury or anyone complains of pain, call 911 immediately. Don't hesitate. Getting police and paramedics on the scene is essential, even for what seems like a minor fender-bender. An officer will create an official accident report, a document that will become the backbone of your insurance claim.

Key Takeaway: Never talk yourself out of calling 911 because the accident seems "too small." A police report is an unbiased, official record of what happened, and it can shut down any "he-said, she-said" arguments down the road.

The importance of this can't be stressed enough. The National Highway Traffic Safety Administration (NHTSA) reported that an estimated 17,140 people died in motor vehicle crashes in just the first half of a recent year. Many of those tragedies started with injuries that may have seemed minor at first glance. You can find more detailed statistics in the NHTSA's press releases.

How to Document and Gather Evidence

Once you've confirmed everyone is safe, what you do next at the scene can make or break your insurance claim. Your smartphone is your most powerful asset right now. Think of yourself as a detective building a case—the evidence you collect in these first few minutes lays the groundwork for getting the compensation you deserve.

Your goal is simple: create a factual, undeniable record of what happened. Put yourself in an adjuster's shoes. What would they need to see to understand the crash without having been there?

Your Smartphone is Your Best Witness

Start snapping photos right away, before anyone moves their car. A few quick pictures of your bumper won't cut it. You need to capture the entire story from every possible angle. A thorough visual record can stop a "he said, she said" dispute in its tracks.

Here's what to photograph:

- The Big Picture: Stand back 50-100 feet and take wide shots showing where all the cars ended up.

- All Vehicle Damage: Get detailed photos of the damage on every car involved, not just yours. Take close-ups and shots from various angles.

- The Scene Itself: Photograph any relevant traffic signs (stop signs, speed limits), traffic lights, and road conditions.

- The Little Details: Don't forget skid marks, broken glass on the road, or even the weather. Sun glare or a rain-slicked road can be a huge factor.

These photos are your objective proof. Memories fade, but pictures don't lie.

Exchanging Information (Without Admitting Fault)

When you speak with the other driver, stick to the facts. The goal is to swap essential information, not to debate what happened or apologize. Keep your cool and stay focused.

Pro Tip: Never, ever admit fault. An innocent "I'm so sorry" can be twisted by an insurance company and used against you. Let the facts and the police report speak for themselves.

Make sure you get this info from every other driver:

- Full Name and Phone Number

- Insurance Company and Policy Number

- Driver’s License Number

- License Plate Number

- The Vehicle's Make, Model, and Color

I always recommend taking clear photos of their documents—it's faster and avoids typos.

Getting the Official Story on Record

The police report is the official, third-party account of the accident, and it carries a lot of weight. When the officer arrives, calmly and clearly state what happened. If you aren't 100% sure about something, like the exact speed you were traveling, don't guess. Just say you're not sure.

Before you leave, grab the officer's name, their badge number, and the police report number. This report is a cornerstone document for your claim. Later on, if your car's value has plummeted, this documentation will be crucial when you hire an independent auto appraiser near me to fight for its true diminished value. The strength of your entire claim starts with these first critical steps.

Navigating the Insurance Claim Process

Once the dust settles at the accident scene, your focus needs to shift to the insurance companies. This part of the journey can feel like a maze, but with a clear head and a methodical approach, you can protect your rights and work toward a fair settlement. The whole game boils down to two things: prompt, factual communication and keeping meticulous records.

Your very first call should be to your own insurance company. Yes, even if the other driver was 100% at fault. Most policies require you to report any accident within a specific timeframe, and skipping this step could put your coverage at risk. When you call, have your policy number, the police report number (if you have it), and the other driver’s information handy.

Your Initial Report: Sticking to the Facts

When you speak to a claims representative, your job is simple: report the facts, and only the facts. Tell them when and where the accident occurred, what vehicles were involved, and share the contact information for any witnesses.

What you don't say is just as critical.

Don't guess about fault, speeds, or distances. If you're not sure, say you're not sure. Most importantly, do not agree to give a recorded statement to the other driver's insurance company right away. Their job is to find ways to pay out as little as possible, and their questions are designed to corner you.

Crucial Takeaway: You're required to cooperate with your insurance company. You are not obligated to give the other driver's insurer a recorded statement on their terms. Politely tell them you need time to review everything before doing so.

Dealing with the Insurance Adjusters

It won’t be long before an adjuster from your insurance company—and likely one from the other driver's—gets in touch. They're tasked with investigating the accident, figuring out who's liable, and evaluating the damage. This is precisely when all the evidence you gathered at the scene becomes your most powerful asset.

Before you even speak with an adjuster, get organized. Create a dedicated folder, either on your computer or a physical one, for every single document related to this accident. Staying organized is one of the smartest things you can do to keep control of the situation.

To make sure you don't miss anything, here’s a quick checklist of the essential information you'll need.

Car Accident Information Checklist

This table breaks down everything you need to have on hand. Having these details ready shows the adjuster you're serious and prepared.

| Category | Information to Collect |

|---|---|

| Scene Details | Date, time, and specific location of the accident (street names, mile markers). |

| Driver Information | Names, addresses, phone numbers, and driver's license numbers for all drivers. |

| Vehicle Information | Make, model, year, license plate number, and VIN for all involved vehicles. |

| Insurance Details | Insurance company name and policy number for all drivers. |

| Witnesses | Full names and phone numbers of anyone who saw the accident. |

| Police Report | The official report number and the name/badge number of the responding officer. |

| Visual Evidence | All photos and videos of vehicle damage, the surrounding scene, and any injuries. |

Keep this information in your accident folder. It’s your single source of truth for the entire claims process.

Your file should also include a simple communication log. This can be a notebook or a document where you track every conversation—every call, every email. Note the date, time, who you spoke with, and a quick summary of what was discussed.

This log is your secret weapon. It prevents "he said, she said" arguments and keeps everyone accountable. When you can reference a specific conversation, it shows the adjuster you mean business. For more advanced strategies, our guide on how to deal with insurance adjusters offers proven tips for navigating these critical discussions. Being prepared transforms you from a passive claimant into an informed advocate for your own claim.

Getting What You're Owed: Diminished Value and Total Loss Claims

Let's talk about the financial hit that happens after the body shop is done. Even with flawless repairs, your car now has an accident on its permanent record. That one little detail can cause its resale value to tank, a loss we call diminished value. It's a very real financial loss, and it's one you absolutely have the right to be compensated for.

Think about it from a buyer's perspective. You're looking at two identical used cars. Same make, model, year, and mileage. But one has a clean history, and the other was in a significant collision. Which one are you buying? Even if the repaired car looks perfect, you'd demand a serious discount to even consider it. That discount is the diminished value you've already lost.

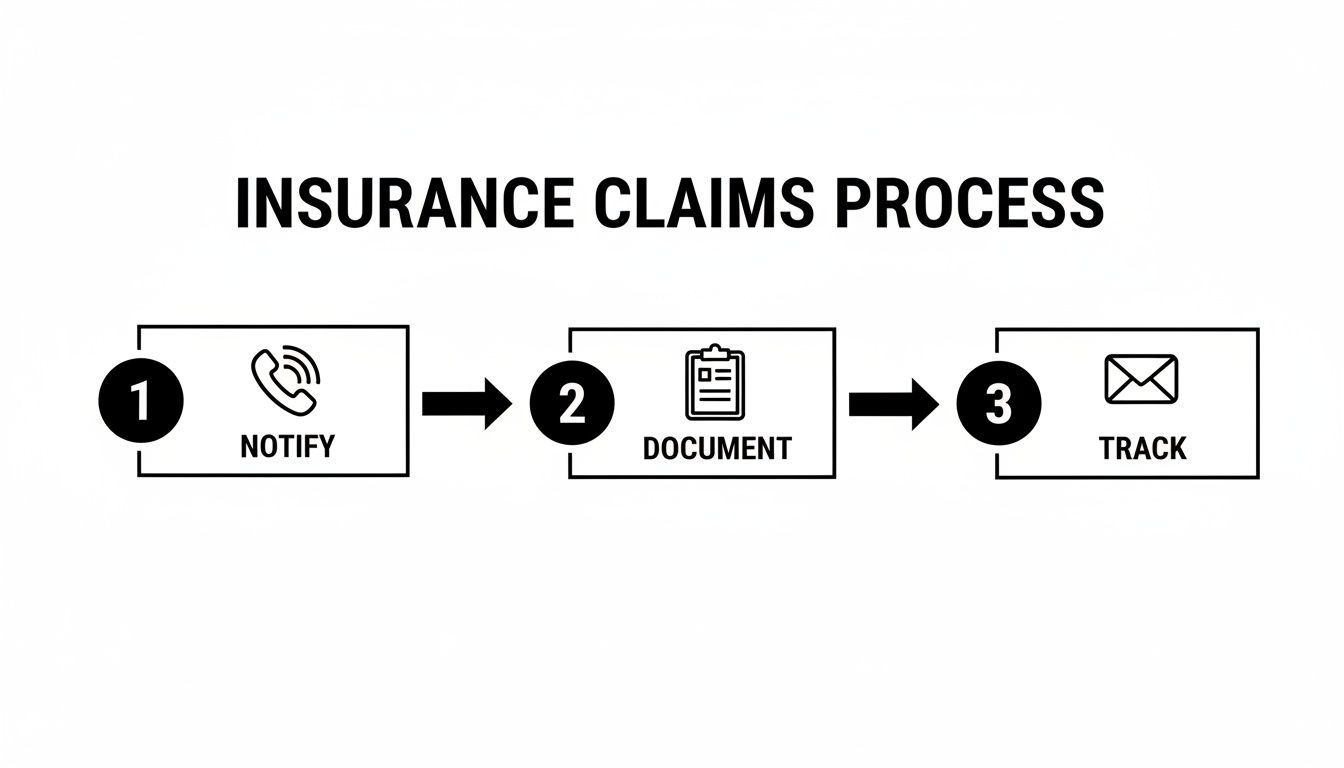

The claims process for this starts the same way as any other. It’s a simple, foundational process you need to nail down from the beginning.

Starting with these three steps—notifying the insurer, documenting everything, and tracking all communication—is how you build the groundwork to fight for every dollar you're owed.

So, What is a Diminished Value Claim?

A diminished value claim is your formal demand to the at-fault driver's insurance company to pay you for this loss in market value. It has nothing to do with the repair bill. The repair check covers the physical damage; the diminished value check covers the financial damage left behind.

Here’s a real-world scenario: Your meticulously kept SUV was worth $35,000 before someone ran a red light and hit you. The repairs cost $8,000, which their insurance covers. But now, with an accident on its CARFAX report, dealers will only offer you $29,000 on a trade-in. You've lost $6,000 in equity through no fault of your own. That $6,000 is your diminished value.

The bottom line is this: The law says you're entitled to be "made whole" after an accident caused by someone else's negligence. That doesn't just mean fixing the bent metal; it means restoring the financial value your car lost.

Winning this kind of claim requires a solid, evidence-based case. For a complete breakdown, our guide on diminished value after a car accident walks you through exactly how to build a claim that insurance companies can't ignore. This is a crucial step if you want to recover your full financial loss.

When Your Car Is Declared a Total Loss

In a more severe crash, the insurance company might just write the car off as a total loss. This happens when the cost of repairs gets dangerously close to, or exceeds, the car's actual cash value (ACV) before the accident. The exact formula varies by state, but a common trigger is when repair estimates hit 75-80% of the car's pre-accident value.

Don't be surprised when the insurer's first settlement offer for your totaled car feels like a slap in the face. It almost always is. They rely on valuation software that often uses data from wholesale auctions or overlooks your car's excellent condition, recent upgrades, or unique features.

You don't have to accept their lowball number. It's time to do your own homework.

- Find Your Own Comps: Search local online listings (like AutoTrader or Craigslist) for cars just like yours—same year, make, model, and similar mileage and condition. Save screenshots.

- Show Your Receipts: Did you recently buy new tires? Have major engine work done? Compile every receipt for recent maintenance and upgrades that add value.

- Demand Their Report: Ask the adjuster for the complete valuation report they used. Go through it line by line to find errors in their assessment of your car's condition, features, or mileage.

The Secret Weapon: The Appraisal Clause

What happens if you've presented all your evidence and the insurance company still won't budge on their low offer? Buried deep in most auto policies is a powerful provision called the Appraisal Clause.

This clause gives you the right to move the valuation dispute out of the insurance company's hands and into the hands of neutral experts. It’s your trump card.

Here’s the typical process:

- You hire your own state-certified, independent appraiser.

- The insurance company hires one of their own.

- The two appraisers then negotiate a fair value. If they can agree, their decision is binding.

- If they're at a stalemate, they mutually agree on a third-party appraiser, called an "umpire," to cast the deciding vote. The umpire's valuation is final.

Invoking the Appraisal Clause forces the issue. It takes the insurer's biased software out of the picture and ensures the final settlement is based on real-world market data, not a self-serving algorithm.

How to Negotiate a Fair Settlement

One of the biggest mistakes you can make after an accident is grabbing the first check the insurance company dangles in front of you. Let's be clear: that first offer is almost never their best offer.

It’s a starting point. Their goal is to close the claim as quickly and cheaply as possible, and that initial lowball number is designed to do just that. Real negotiation takes patience, solid preparation, and knowing exactly what your claim is worth.

Your leverage in this conversation comes from all the work you've already done—the photos you took at the scene, the detailed records you’ve kept, and a crystal-clear calculation of every single loss. We're not just talking about the body shop estimate; this includes your medical bills, lost income from missing work, and that all-important diminished value claim.

Crafting Your Demand Letter

Your opening move isn't a phone call—it's a formal demand letter sent directly to the adjuster handling your claim for the at-fault driver. This isn't a simple email asking for a check. Think of it as a professional, evidence-backed argument that tells the story of your accident and its financial impact.

Here's what your letter absolutely must contain:

- The Facts: Start with a concise summary of how the accident happened, clearly stating why their insured driver was responsible. Don't forget to reference the police report number.

- The Numbers: Provide an itemized list of every single expense you've had. This means medical bills, car repair estimates, rental car receipts, and documentation for any lost wages.

- The Proof: You need to back up every claim. Attach copies of all your documentation—invoices, pay stubs, doctor's notes, and, of course, your independent diminished value appraisal.

You'll wrap up the letter with your "demand"—the total settlement figure you expect. Make this number realistic but on the higher end of what you'd accept. It gives you crucial wiggle room to negotiate later and signals to the adjuster that you're serious and well-prepared.

Countering the Inevitable Lowball Offer

I can almost guarantee the adjuster’s first counteroffer will be a fraction of what you demanded. It’s a classic tactic. Don't get angry or discouraged. This is just part of the game; the real negotiation starts now.

Your response should be simple: ask the adjuster to justify their low number in writing. What specific facts, reports, or policies are they using to come up with that figure? Their answer, or lack thereof, often exposes the weak points in their argument.

Pro Tip from the Trenches: Keep your negotiations grounded in facts, not emotions. If they question a medical expense, you counter with your doctor's official report. If they dismiss your car's value, you present your independent appraisal. Every move you make should be backed by the evidence you've already organized.

This process can feel like a slow-motion tennis match, with offers and counteroffers going back and forth. Stay professional, be persistent, and keep logging every single phone call and email. When it comes time to talk dollars and cents, knowing how to negotiate an insurance settlement is a game-changer.

In the end, the objective is to be made whole again. Don't let an adjuster pressure you into taking a bad deal just to get it over with. By staying organized, building a case based on solid evidence, and standing firm, you put yourself in the strongest possible position to get the fair compensation you truly deserve.

Common Questions After a Car Accident

Once the initial shock of an accident wears off, a whole new set of questions and worries can start to creep in. It’s a confusing time, and feeling uncertain is completely normal. Getting straight answers to the most common concerns can make all the difference in feeling like you're back in the driver's seat.

Let's tackle a few of the big ones I hear all the time.

"It Was Just a Fender-Bender. Do I Really Need to Report It?"

This comes up a lot. You tap someone's bumper in a parking lot, you both get out, and there’s no visible damage. It feels easier to just exchange numbers and move on, right?

The answer is, you should always file a report. I've seen it happen too many times: what looks like a minor dent can hide serious frame damage underneath. Even worse, injuries like whiplash sometimes don't show up for a day or two. A police report creates an official, unbiased record of what happened, protecting you if the other driver suddenly remembers they have a "sore neck" or claims more damage later on.

"What If the Other Driver Doesn't Have Insurance?"

This is a scary thought, but it's exactly why you have your own policy. This is where your Uninsured/Underinsured Motorist (UM/UIM) coverage becomes your best friend.

If the at-fault driver is uninsured or their policy limits aren't enough to cover your expenses, your UM/UIM coverage kicks in. It helps pay for your medical bills and vehicle repairs. It’s a crucial piece of protection that, frankly, everyone should have.

"How Long Do I Have to File a Claim?"

Time is of the essence. Every state has a legal deadline for filing a claim, known as the statute of limitations. This window can be anywhere from one to several years, and it's often different for property damage versus personal injury claims.

Don't wait. The best move is to notify your insurance company immediately after the accident. Missing your state's deadline means you could lose your right to any compensation, so it's critical to act fast.

Once you've sorted out the insurance side of things, your focus will shift to getting your car fixed. This is another critical step, and you'll want to be sure it's done right. Taking a moment to learn how to find a good mechanic can save you a world of headaches and ensure your vehicle is safe to drive again.

Navigating the aftermath of an accident is all about being informed and proactive. Knowing the answers to these questions puts you in a much stronger position.

If your car was declared a total loss or its value has dropped significantly after repairs, don't just accept the insurance company's first offer. Total Loss Northwest provides independent, expert auto appraisals that establish the true market value of your vehicle. We give you the evidence you need to demand fair payment. It's time to get what you're rightfully owed. Learn more at https://totallossnw.com