You open the claim email, scan the number, and feel your stomach drop. The truck you maintained, upgraded, cleaned, and depended on has been declared a total loss, and the settlement offer doesn't even come close to what it would take to replace it in Tacoma.

That reaction is normal. It also doesn't mean the insurer's number is correct.

Individuals seeking Tacoma claim valuation help usually need more than generic advice. They need a practical plan for what to do after a low total loss offer, what language to use, what proof matters, and when to stop arguing with an adjuster and force the issue through the Appraisal Clause in the policy. That clause is often the turning point.

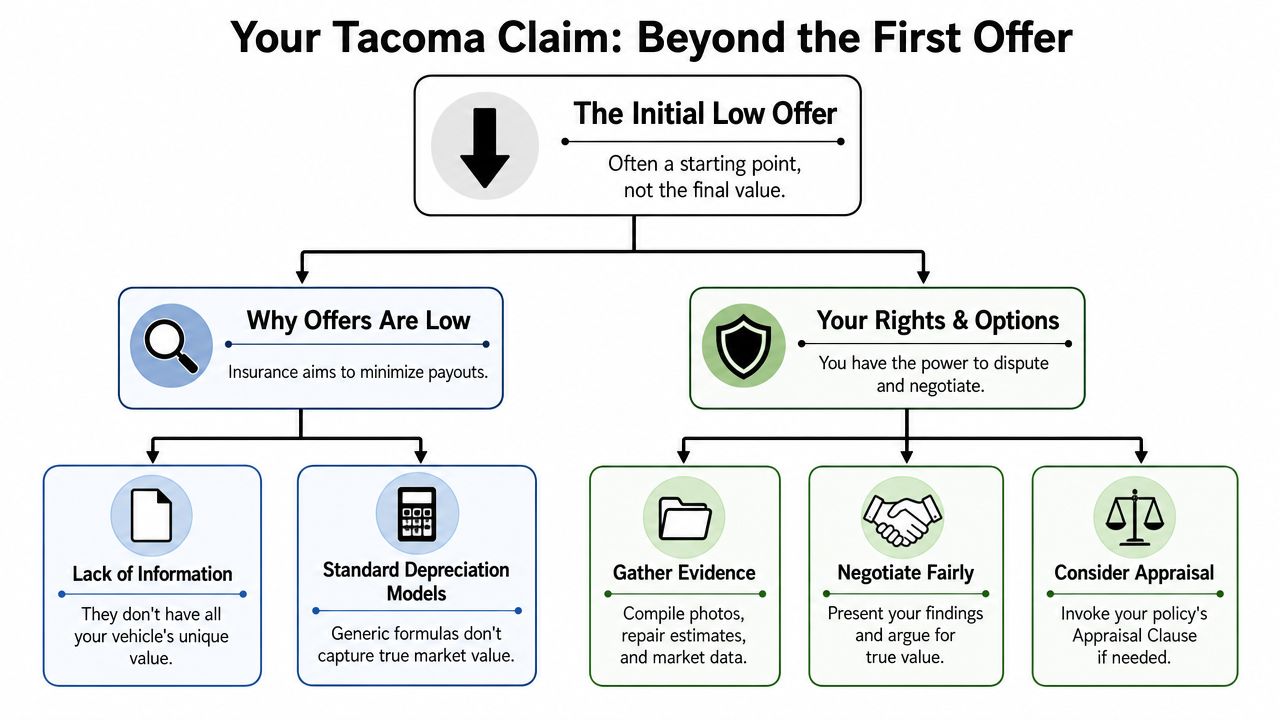

Why the First Insurance Offer Is Just a Starting Point

The first offer usually feels official because it arrives in a polished valuation report with line items, adjustments, and market references. But a formal-looking report isn't the same thing as a fair valuation.

Most initial total loss offers are built around the insurer's Actual Cash Value, or ACV, calculation. ACV is supposed to reflect the vehicle's pre-loss market value, not what you owe on it and not what a dealer is asking for a different vehicle that happens to look similar online. In practice, that number often comes from valuation software and templated condition adjustments that can miss what made your vehicle worth more in the local market.

What the insurer is really doing

An adjuster usually isn't hand-pricing your vehicle from scratch. They rely on software, standard condition grids, and selected comparable vehicles. That process can produce a number quickly, but quick and accurate aren't the same thing.

Common problems show up fast:

- Bad comparables that aren't comparable in trim, drivetrain, mileage, condition, or equipment

- Condition deductions that assume average wear when your vehicle was above average

- Option errors where added features aren't captured correctly

- Local market blind spots when the report leans on listings outside the Tacoma market

- Unsupported adjustments that lower value without giving you enough detail to challenge them

If you want a better sense of what fair market value should look like before you push back, this guide on how to calculate fair market value is a useful starting reference.

The carrier's first number is often a negotiation position wrapped inside a valuation report.

Why the vehicle was totaled in the first place

A lot of owners focus only on the payout and never stop to ask whether the total loss decision itself follows Washington rules. In Washington, a vehicle is legally a total loss when repair costs plus salvage value equal or exceed ACV, using the formula Repair Costs + Salvage Value ≥ ACV, according to Fuller Personal Injury Law. Their example is straightforward: a car with an ACV of $10,000, $9,000 in damage, and $2,000 in salvage value reaches $11,000, which exceeds ACV and triggers a total loss.

That matters because the salvage number is part of the equation. If either the ACV or salvage value is off, the entire total loss analysis can tilt against you.

What to do before you say yes

Don't start by arguing emotionally, even if you're angry. Start by getting organized.

Use this quick sequence:

- Request the full valuation report. Ask for every comparable, every adjustment, and the source of the condition ratings.

- Read for errors first. VIN details, trim, cab configuration, mileage, aftermarket parts, prior condition, and package options are where mistakes often hide.

- Compare the report to the Tacoma market. Not a broad national market. Your market.

- Keep every communication in writing. Phone calls are easy to forget and hard to prove.

- Do not accept the first number just because the vehicle has already been declared a total loss.

The key shift is mental. You are not asking for a favor. You are evaluating whether the insurer's ACV work is supportable.

Your Right to Dispute the Valuation with the Appraisal Clause

If negotiation stalls, stop circling around the same bad number. Use the strongest contractual tool most policyholders overlook: the Appraisal Clause.

This clause matters because it changes the dispute from “you versus the adjuster” into a structured valuation process. Instead of begging the carrier to revisit its own software output, you invoke the policy right to have the amount of loss determined through appraisal. That moves the discussion away from the insurer's internal system and toward independent valuation.

Why this works better than repeated back-and-forth

Basic negotiation has limits. You send comps. The adjuster says their report already accounted for market conditions. You point out equipment errors. They offer a small revision or none at all. Weeks pass.

The Appraisal Clause changes the dynamic because it requires movement.

Here's the practical difference:

| Approach | What usually happens |

|---|---|

| Informal negotiation | The adjuster keeps control of the file |

| Complaint without evidence | You get a scripted response |

| Appraisal Clause invocation | The valuation dispute moves into a formal process |

A lot of drivers confuse appraisal with arbitration. They aren't the same. If you want a simple comparison point, American Integrity binding arbitration is a useful example of how insurance dispute mechanisms can differ by endorsement and process. For total loss value disputes, appraisal is usually the more relevant policy tool.

You can learn the mechanics in more detail through this overview of the appraisal clause in auto insurance.

The Washington angle that helps you

Washington follows a pure comparative negligence system. That means a driver can still recover damages even if they were partly at fault, with recovery reduced by their percentage of fault, as explained by Pendergast Law. That same source also notes that owners have the right to challenge an insurer's valuation with evidence such as repair estimates, comparable vehicle listings, or independent appraisals.

For a valuation fight, that matters in two ways:

- Partial fault doesn't erase your right to dispute value

- Washington recognizes your right to challenge the insurer's number with evidence

Practical rule: If the adjuster keeps repeating the same report and won't address your evidence line by line, it's usually time to invoke appraisal.

Language that gets attention

Keep your communication short and controlled. Don't write a long rant. Send something like this:

I dispute your Actual Cash Value determination for my vehicle. The valuation report contains errors and does not reflect fair market value in the Tacoma market. Please treat this as my formal request for the policy language governing appraisal and confirm the procedure to invoke the Appraisal Clause on this claim.

If your policy already contains the clause and you're ready to proceed, tighten it further:

I formally invoke the Appraisal Clause under my auto policy for the dispute over the amount of loss. Please confirm your appraiser selection process and all next steps in writing.

That wording does two things. It creates a paper trail, and it tells the carrier you understand the difference between casual disagreement and formal appraisal.

Building Your Case with Powerful Evidence

A strong valuation dispute isn't built on one screenshot from a car listing site. It's built on a file that shows your vehicle's real pre-loss condition, equipment, and position in the local market.

The best evidence package usually combines market data with ownership records. One proves what similar vehicles are selling for. The other proves why yours belongs at the stronger end of that range.

What to collect first

Start with documents you already control.

- Maintenance history. Oil service records, brake work, suspension service, timing-related maintenance where applicable, and dealership service printouts can support above-average condition.

- Upgrade receipts. Tires, wheels, canopy, bed systems, lighting, towing equipment, and other add-ons may not all add dollar-for-dollar value, but they help prove the truck wasn't a stripped baseline unit.

- Pre-loss photos. Exterior, interior, odometer, bed, wheels, and any specialty features.

- Purchase paperwork. Helpful for verifying trim, packages, and factory equipment.

- Claim documents. The insurer's valuation report, total loss summary, and any email where the adjuster explains the offer.

How to find usable comparables

Not every listing helps. A bad comp can hurt your argument because it tells the insurer you're not being careful.

Look for vehicles that match as closely as possible on the things buyers pay attention to:

- Same body style and configuration

- Similar trim and drivetrain

- Close mileage band

- Same general condition level

- Comparable factory and major added equipment

- Available in the Tacoma-area market or a similar Washington market

When a listing differs from your vehicle, write down the difference instead of ignoring it. A comp with lower mileage or a higher trim can still help if you explain the distinction.

A simple worksheet helps:

| Evidence item | Why it matters |

|---|---|

| Service records | Supports condition rating |

| Option list | Catches missing equipment |

| Pre-loss photos | Counters unfair condition deductions |

| Local comps | Anchors the market value argument |

| Upgrade receipts | Shows the vehicle was not ordinary |

Gap coverage isn't the backup plan people think it is

Many drivers relax once they hear they have gap insurance. That's a mistake if the ACV is low.

According to the verified data tied to this topic, 68% of Washington drivers with gap insurance incorrectly assume it will cover full replacement costs when their vehicle is totaled, but gap only covers the loan balance exceeding ACV, not the deductible or the difference between a low ACV and the vehicle's true market worth, as referenced in this Tacoma total loss discussion.

That means a low ACV still hurts you, even with gap.

Common mistake: People stop fighting the ACV because they assume gap will make them whole. It won't if the valuation itself is understated.

Build your evidence file as if no one is coming to rescue a weak ACV. Because in many claims, no one is.

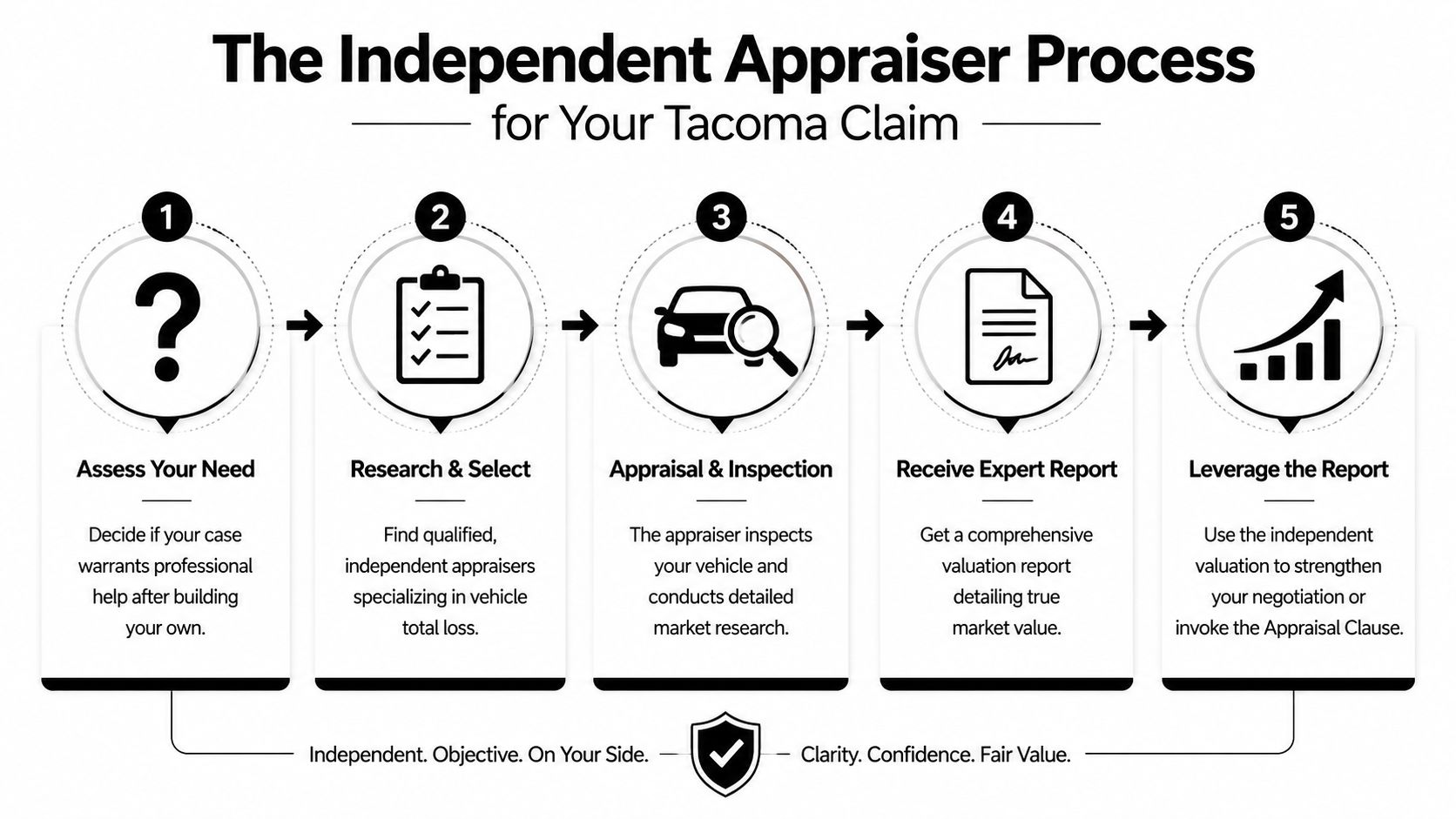

Hiring an Independent Appraiser in Tacoma

Some owners can handle the dispute themselves. Others should bring in an appraiser early.

The right time to hire help isn't based on frustration alone. It's based on the kind of vehicle you had, the quality of the insurer's report, and whether the gap between their number and the market reality is something you can prove and defend.

When doing it yourself starts to break down

A self-managed challenge often works when the insurer made obvious mistakes and the adjuster is responsive. It starts failing when the dispute becomes technical.

These are the situations where an independent appraiser usually adds the most value:

- The vehicle was specialized. Off-road builds, collector vehicles, rare trims, and heavily optioned trucks often don't fit cleanly into standard software templates.

- The report looks polished but thin. Lots of adjustments, weak comparable selection, and little explanation.

- You don't have the time to manage the file. Gathering comps, rebutting errors, and following the policy process takes sustained attention.

- The carrier has gone quiet or repetitive. Once every email gets the same answer, expertise matters more than persistence.

What a good appraiser actually does

A real independent appraiser doesn't just “pull comps.” They analyze the claim file, review the carrier's valuation method, identify unsupported deductions, document vehicle-specific features, and build a market-supported opinion of value that can stand up inside the appraisal process.

That process usually includes:

- Document review of the insurer's report and your supporting records

- Vehicle profile development based on trim, condition, factory equipment, and relevant upgrades

- Market research focused on usable comparables

- Written appraisal report that explains the reasoning, not just the conclusion

- Participation in the appraisal process if the policyholder invokes the clause

If you need a local starting point, this page on a Tacoma total loss appraiser shows the kind of service model to look for.

A strong appraiser is valuable because they can explain why the insurer's valuation is wrong in a way the file has to take seriously.

Questions worth asking before you hire anyone

Don't hire based on the word “expert” in a website header. Ask direct questions.

- Do you handle total loss valuation disputes specifically

- Do you work inside the Appraisal Clause process

- Will I receive a written report

- How do you choose comparables

- How do you address condition disputes and missing equipment

- Will you communicate with the insurer or only hand me a report

The point isn't to outsource your judgment. It's to put qualified analysis behind your position.

Mastering the Negotiation and Settlement Process

Once appraisal is invoked or your evidence package is ready, the tone of the claim should change. Stop arguing generally. Start pushing the file issue by issue.

This part is where many owners lose momentum. They gather good material, then send a vague message like “Please reconsider.” That rarely works. A better approach is to create a short, professional record that tells the insurer exactly what is wrong, what you want corrected, and what process you expect next.

A practical timeline after you push back

A typical dispute has a rhythm.

First, you request the valuation support and identify errors. Then you send a written rebuttal with your evidence. If the carrier still stands on its report or makes only cosmetic changes, you invoke the Appraisal Clause. After that, each side selects an appraiser, and if those appraisers can't agree, an umpire may be used under the policy procedure to resolve the amount of loss dispute.

You don't need to dramatize any of this. You need to stay precise.

Sample wording you can adapt

Use short emails and numbered issues. For example:

Subject: Total Loss Valuation Dispute

I dispute the valuation used to determine the Actual Cash Value of my vehicle. The report appears to contain material issues that affect the amount of loss.

- The comparable vehicles are not sufficiently similar in configuration and equipment.

- The condition adjustments do not reflect my vehicle's documented pre-loss condition.

- Certain options and value-bearing features appear to be omitted or undervalued.

I request a written response addressing each item and a revised valuation report.

If you're moving to appraisal:

Subject: Formal Invocation of Appraisal Clause

I am formally invoking the Appraisal Clause under my policy regarding the dispute over the amount of loss for my total loss claim. Please confirm receipt, identify your designated appraiser, and provide any policy-specific procedural requirements in writing.

What to say when the adjuster pushes back

Expect familiar responses. They often sound reasonable until you look closely.

| Adjuster response | Better reply |

|---|---|

| “Our report already reflects market value.” | “Please identify where the report addresses the specific comparable and condition issues I raised.” |

| “Those listings are not acceptable.” | “Please explain the selection criteria you applied and why my identified comparables fail that standard.” |

| “The condition adjustment is automatic.” | “Please provide the factual basis for the assigned condition rating.” |

Keep the conversation on documentation, comparability, and policy rights. Once it turns into opinion trading, you lose ground.

The role of the umpire

If the two appraisers don't agree, the umpire becomes important. The umpire isn't there to reward the louder side. The umpire reviews the valuation dispute and helps resolve the amount of loss when the appraisers remain apart.

That's why your file needs to be clean. Unsupported complaints don't age well in appraisal. Organized evidence does.

The strongest policyholders do three things well here: they communicate in writing, they make narrow objections instead of broad accusations, and they stop repeating themselves once the claim belongs in appraisal.

Your Final Checklist for a Fair Claim Outcome

A fair result usually comes from process, not luck. The owners who do best in these disputes aren't always the loudest. They're the most prepared.

Use this checklist before you sign anything:

- Read the valuation report carefully and mark every error involving trim, equipment, mileage, condition, and comparables.

- Confirm the claim is being handled as a Washington total loss under the proper rule, not just according to whatever number the software produced.

- Build a serious evidence file with local comparables, service records, pre-loss photos, and receipts.

- Don't rely on gap coverage to fix a bad ACV. If the base valuation is low, the rest of the claim usually stays low.

- Move the dispute into appraisal when negotiation stalls. The Appraisal Clause exists for exactly this kind of impasse.

- Keep every communication professional and in writing. Short, specific messages are more effective than emotional ones.

- Bring in an independent appraiser when the file becomes technical or the insurer keeps hiding behind its report.

Tacoma claim valuation help isn't about finding a clever phrase that scares the insurer. It's about knowing when the informal discussion is over and when the policy gives you the right to force a better process.

You don't have to accept a weak total loss number just because it arrived first.

If you're dealing with a low total loss offer and need experienced help using the Appraisal Clause, Total Loss Northwest provides certified independent appraisals for Washington vehicle owners. They focus on total loss and diminished value disputes, build market-based valuation reports, and help take the pricing decision out of biased insurance software so you can pursue a fair settlement.