You open the settlement letter, look at the number, and know it's wrong.

That reaction is common after a serious crash, especially when a vehicle is declared a total loss or repaired with a damage history that will follow it for years. The insurer's figure often lands with an air of finality, as if a computer already decided what your car was worth and there's nothing left to discuss. There is.

A Third Party Auto Appraisal is the move that changes the conversation. It isn't just a second opinion. It's a formal valuation built from inspection evidence, comparable sales, condition analysis, mileage, options, and documented adjustments. Done correctly, it gives you something far more useful than frustration. It gives you evidence.

For drivers who weren't at fault, that matters. You're already dealing with towing, repairs, rental issues, lienholders, and adjusters who talk in shortcuts. If the carrier's number doesn't reflect the actual market, an independent appraisal can shift the dispute out of opinion and into proof.

Why Your Insurer's Offer Might Be a Lowball

A low settlement usually starts with a report that looks polished but feels disconnected from the actual vehicle you owned. The trim is off. The options are missing. The comparable vehicles aren't close matches. The condition adjustment doesn't make sense. On a total loss, those errors add up fast.

That's why many people reach out only after they've spent days arguing with an adjuster and getting nowhere. They've already pointed out the leather package, the recent tires, the lower mileage, or the upgraded safety equipment. The carrier still responds with the same bottom-line number.

Why the first number often misses the mark

Insurance valuations are often built for speed and consistency across large claim volumes. That doesn't mean every report is wrong. It does mean the report may not capture what made your vehicle worth more than the average unit in a database.

The dispute also starts from an uneven position. The insurer has a valuation system, internal process, and claims staff who read these reports every day. Most drivers are seeing this paperwork for the first time while also trying to recover from the accident itself.

Practical rule: If the insurer's offer doesn't line up with the actual market for a comparable vehicle in your area, treat their number as an opening position, not a final answer.

Texas insurance data gives a good benchmark for how this plays out. Appraisal showed up in less than 0.02% of payable auto claims, yet the average award was $29,541, which shows that appraisal is rare but often used in major valuation disputes, primarily total losses, according to the Texas Department of Insurance appraisal experience report.

What a third-party appraisal changes

A proper third-party appraisal replaces a vague complaint with a documented case. Instead of saying, “This feels low,” you're saying, “Here is the fair market value, here are the comparables, and here is how the adjustments were made.”

If you want to understand how injury damages and property damages are often evaluated together after a crash, this guide to car accident value gives useful context on the bigger financial picture. For the vehicle side specifically, it also helps to understand how software-driven reports are built and where they can go wrong, especially in CCC auto valuation disputes.

That's the primary benefit. An independent appraisal doesn't ask the insurer to be more generous. It forces the valuation dispute onto evidence.

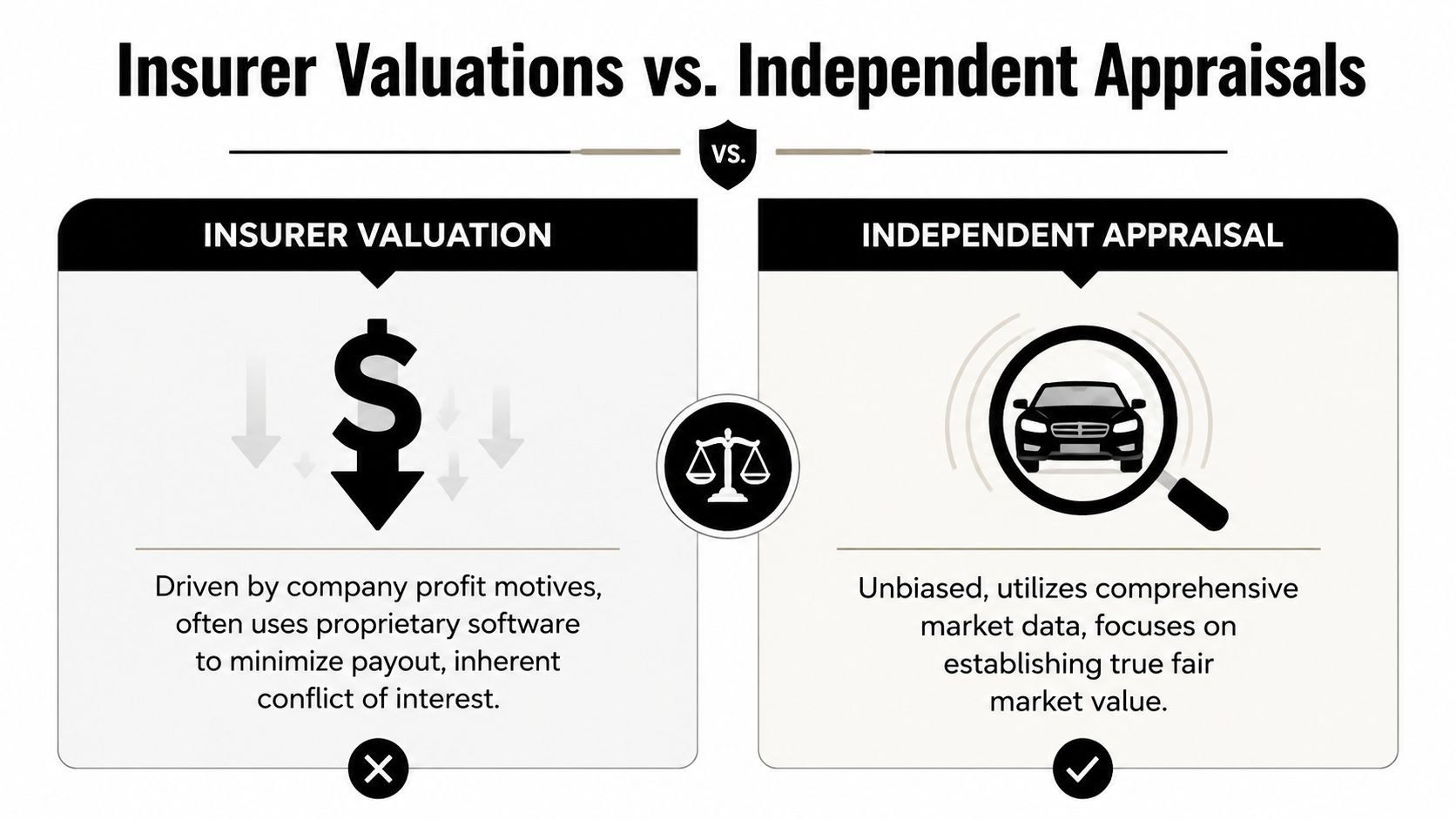

Insurer Valuations vs Independent Appraisals

The cleanest way to understand this dispute is to compare the two valuations side by side. They may both use market data, but they don't start from the same objective and they aren't accountable in the same way.

Insurer valuation and independent appraisal are not the same product

An insurer's valuation is part of a claim operation. It's designed to support a settlement decision. That process may rely heavily on software, preset rules, and comparable selections you didn't choose.

An independent appraisal is built to defend a number. The appraiser has to inspect the facts, select comparable vehicles that match, explain each adjustment, and put the reasoning in writing. That's a different standard of work.

| Factor | Insurer's Valuation | Independent Third-Party Appraisal |

|---|---|---|

| Primary objective | Support the carrier's claim settlement position | Establish fair market value with documented support |

| Who it serves | The insurance company handling the claim | The vehicle owner or claimant |

| Typical method | Proprietary valuation platforms and internal claim review | Inspection, comparable market research, and explicit adjustments |

| Comparable selection | May include broad market matches | Focuses on highly similar vehicles |

| Adjustment logic | Often summarized in a report format the driver didn't control | Explained line by line so the reasoning can be reviewed |

| Accountability | Driven through insurer claims process | Driven through a written appraisal report that can be challenged and defended |

Where independent reports get their force

A strong appraisal is specific. It doesn't lean on one book figure. It ties the vehicle to the market through comparable sales, condition analysis, mileage, option content, and documented adjustment logic.

That's also why I tell clients not to argue only from emotion. “I loved my car” isn't a valuation method. “The report omitted key options and used poor comparables” is.

Their appraiser works for their side of the claim. Your appraiser works to support a defensible market value.

If you want a clearer look at how carriers commonly arrive at these numbers, review how an insurance company values a car. Once you understand that process, the insurer's offer stops looking like an objective fact and starts looking like what it is: a valuation position that can be challenged.

When You Absolutely Need an Independent Appraisal

Not every claim needs outside help. Some insurer offers are close enough to market that it makes sense to settle and move on. But there are situations where an independent appraisal becomes the practical move, not an optional extra.

Total loss disputes

If your vehicle was declared a total loss and the offer doesn't buy a comparable replacement vehicle in the market, that's the clearest trigger. Drivers most often feel cornered in this situation because the carrier wants a quick title transfer and release, while the owner is still trying to verify whether the number is right.

A total loss appraisal is especially useful when the report missed trim level, option packages, condition, service history, recent upgrades, or strong local market pricing.

Diminished value claims

A repaired vehicle can still lose market value because the accident history stays with it. Buyers, dealers, and appraisers all factor that history into resale decisions. If you weren't at fault, you may have a basis to claim that loss in value even after repairs are complete.

For a general legal overview of this issue, this resource on compensation for diminished car value is helpful. The appraisal side of the claim is where that legal concept gets translated into a supportable dollar figure based on the vehicle, the damage, and the market.

Specialty, collector, and modified vehicles

Automated valuation systems struggle most with specific types of vehicles. A classic truck, a collector car, a heavily optioned luxury vehicle, or a properly modified enthusiast vehicle often can't be priced accurately by broad market software alone.

In those files, vehicle-specific evidence matters more. Build sheets, photos, restoration quality, originality, custom parts, and maintenance records all become part of the value discussion.

The appraisal clause matters, but so does claim type

The appraisal clause has a long-established role in insurance disputes because it gives the parties a way to resolve valuation disagreements using independent appraisers rather than software alone, as explained in this discussion of invoking the total loss appraisal clause. In practice, that process is most often associated with first-party claims, meaning disputes with your own insurer.

That distinction matters. Many drivers use “third-party appraisal” to mean an appraisal for a claim involving the at-fault party's carrier. But the contractual right to force a formal appraisal process usually lives in your own policy, not theirs. If you're pursuing a third-party claim, an independent appraisal can still be powerful evidence, but the exact procedure depends on the policy language, state rules, and claim posture.

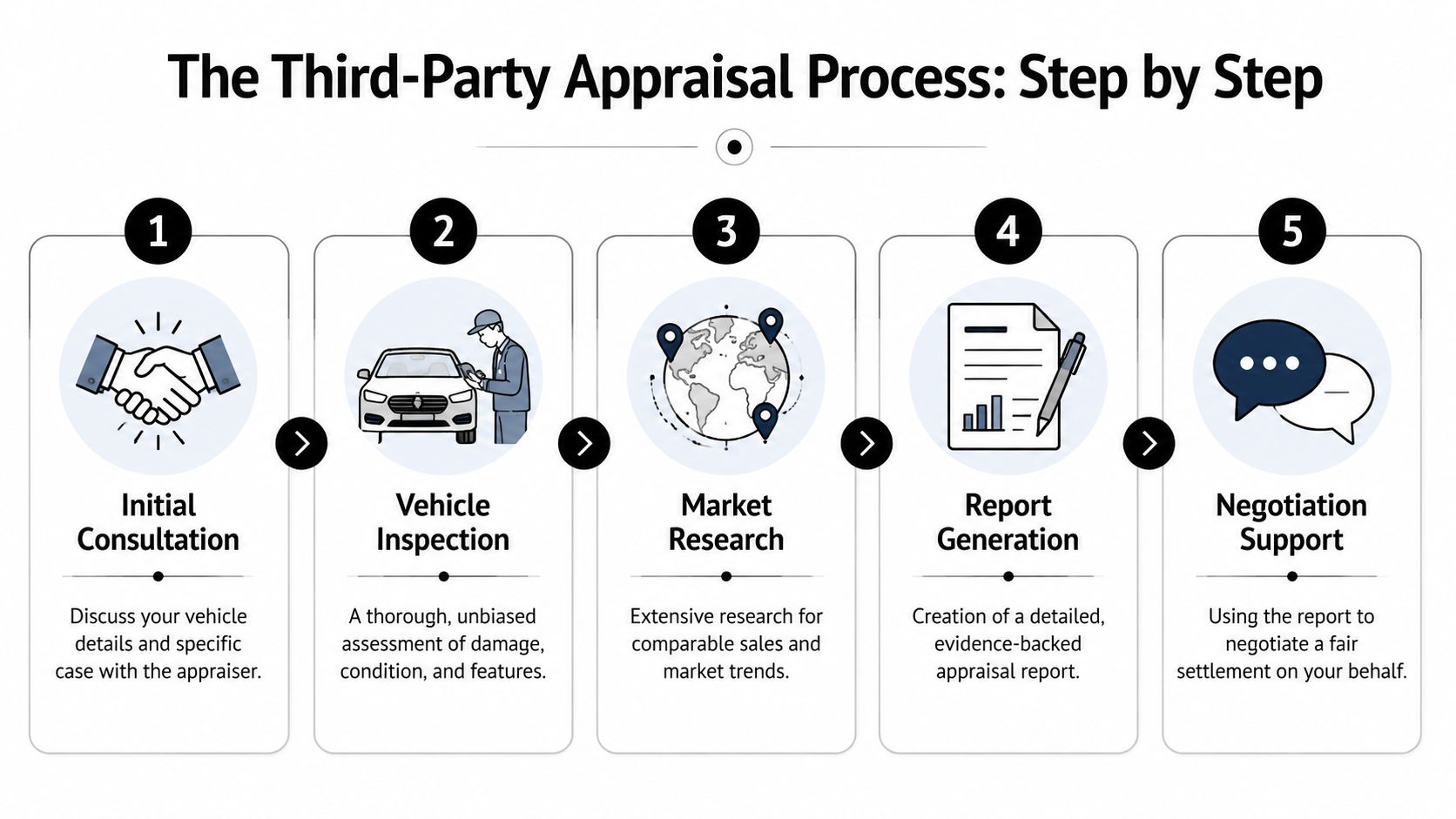

The Third Party Appraisal Process Step by Step

The appraisal process is often perceived as mysterious. It isn't. A competent appraiser follows a repeatable workflow and documents each step so the final number can survive scrutiny.

Here's what that process looks like in practice.

Step one through step three

The file starts with intake. The appraiser reviews the claim facts, the insurer's valuation, photos, VIN details, mileage, options, damage information, and any prior records that affect value.

Then comes inspection. For some losses, that means a physical inspection. In other cases, a desk review built on strong documentation can work. The point is the same. The appraiser needs direct evidence of the vehicle's condition, equipment, and loss scenario.

After that, the actual work begins in the market. A defensible appraisal uses a market-approach workflow. The appraiser researches similar comparable sales, then adjusts those comparables for differences in condition, mileage, and option content, as outlined in this explanation of vehicle appraisal methodology and USPAP reporting.

A good appraisal shows its math. It doesn't hide behind a single unsupported conclusion.

To see the process in plain language, this short video helps:

Step four and step five

Once the comparables are selected and adjusted, the appraiser writes the report. That report should explain what was inspected, which comparable vehicles were used, what adjustments were made, and why the final opinion of value makes sense.

The USPAP-compliant structure matters. USPAP stands for Uniform Standards of Professional Appraisal Practice. For the client, the practical value is simple. A USPAP-style report is organized, auditable, and easier to defend in negotiation or testimony because the assumptions and methods are visible.

The final stage is claim use. That may mean submitting the report directly to an adjuster, using it to challenge a total loss offer, supporting a diminished value demand, or preparing for a formal appraisal process if the policy allows it.

What a solid report usually includes

- Vehicle identification with VIN, trim, mileage, and option verification

- Condition evidence based on photos, inspection notes, repair status, and prior history

- Comparable market data chosen for similarity rather than convenience

- Adjustment logic for differences in mileage, equipment, wear, and marketability

- Written conclusion that ties the evidence to a supportable value opinion

That chain of evidence is what gives a Third Party Auto Appraisal weight. Without it, you only have disagreement. With it, you have a valuation argument the insurer has to answer.

Using Your Appraisal Report to Negotiate a Fair Settlement

Once the report is complete, don't just email it with a short note saying you disagree. Use it deliberately.

The report puts you in a stronger position because it changes the insurer's task. Before, they could brush off your objections as opinion. After a proper appraisal, they have to respond to evidence, comparable by comparable and adjustment by adjustment.

How to submit it effectively

Start with a written demand for reconsideration. Attach the appraisal report and identify the specific reasons the insurer's valuation was deficient. Missing options, poor comparable selection, unsupported condition deductions, wrong trim, and market mismatch are all stronger than general complaints.

If you're dealing with your own carrier and your policy includes an appraisal clause, this is usually the point where you invoke it in writing. Keep that notice direct. State that there is a dispute over value, that you are demanding appraisal under the policy, and that your appraiser's information will follow or is enclosed.

What happens if the appraisers disagree

In many appraisal clause frameworks, each side selects a competent, disinterested appraiser. If those appraisers can't agree, they select a neutral umpire to resolve the gap. The umpire reviews both appraisals and issues a final value, creating a bounded dispute-resolution mechanism that forces both sides to justify their numbers with evidence rather than generalized software, as described in this overview of North Carolina's third-party appraisal clause framework and umpire process.

That structure matters because it stops the endless loop of phone calls where nothing changes. Instead of “our system says,” the dispute moves into a defined process.

The appraisal report is not the end of the claim. It is the document that moves the claim into a forum where unsupported numbers have a harder time surviving.

What works and what usually doesn't

Some tactics move claims forward. Others waste time.

- What works: A clean written submission, a professional appraisal report, and a narrow focus on valuation evidence.

- What works: Pointing out factual errors in the carrier's report rather than attacking the adjuster personally.

- What doesn't: Sending online listings with no adjustment analysis and calling them proof.

- What doesn't: Invoking appraisal casually without checking whether the policy and claim type support it.

There's also a practical trade-off. Appraisal can create pressure, but it doesn't guarantee the insurer will agree with your position instantly. It does, however, force a more disciplined argument, and that's usually where lowball offers start to weaken.

How to Find and Hire a Certified Auto Appraiser

A lot of claimants call an appraiser after they have already spent weeks arguing with an adjuster and getting nowhere. At that point, the wrong hire can cost time, money, and credibility. The right hire gives you a report that can stand up in negotiation and, if the policy allows it, support a formal appraisal-clause dispute with evidence instead of guesswork.

Start by asking how the appraiser works, not what number they think they can get. A certified appraiser should be able to explain how they inspect the vehicle, verify options and condition, choose comparables, and make adjustments. If they cannot explain their method in plain English, the insurer will likely have an easy time attacking the report.

What matters most is whether the report is built for scrutiny.

- A defined valuation method based on inspection findings, vehicle configuration, condition, and market comparables

- A written report with visible adjustments so you can see how the final number was reached

- Experience with your type of dispute such as total loss, diminished value, or a specialty vehicle

- Independence from repair shops, dealers, or anyone else who profits from pushing the value in one direction

Credentials matter, but process matters just as much. A designation on a website does not help if the report reads like a sales pitch. Insurers and umpires look for supportable analysis, clean documentation, and reasoning they can follow line by line.

Red flags that should stop you

Be careful with anyone who promises a result before reviewing the file. No credible appraiser can tell you the correct value from a quick phone call and a hopeful description of the car.

Watch for softer warning signs too. Some appraisers rely heavily on unsupported listings, skip condition analysis, or make blanket statements about local market value without showing their work. That kind of report may sound forceful, but it usually folds as soon as the carrier asks basic questions.

If you are comparing providers, this guide to finding an independent auto appraiser near me is a useful place to start. Total Loss Northwest is one example of a firm that handles total loss appraisals in Washington and Oregon and diminished value matters more broadly. The name matters less than the file discipline behind the report. Hire the appraiser who can document the value, defend the adjustments, and use the policy process to shift the dispute away from insurer software and onto evidence.

Frequently Asked Questions About Auto Appraisals

Is a third-party auto appraisal worth paying for

It depends on the size and seriousness of the valuation dispute. If the insurer's number is close to market, an appraisal may not be worth the effort. If the offer is materially off, especially on a total loss, diminished value claim, or specialty vehicle, the report can become the evidence that changes the outcome.

Texas claim data is instructive here. The same state report noted that the average insurer expense tied to personal auto appraisals was about 2% of the award amount, increasing to about 3% when an additional factor was included, suggesting the appraisal process itself is usually a small administrative cost relative to the settlement value in those disputes, according to the Texas Department of Insurance report discussed earlier.

How long does the appraisal process take

The answer depends on the vehicle, the documentation available, and whether the claim stays in negotiation or moves into a formal appraisal procedure. A straightforward file can move quickly when photos, VIN data, options, and the insurer's valuation report are all available early.

Specialty vehicles and hard-fought diminished value cases usually take longer because the comparable research and adjustment work are more demanding. Delays also happen when the insurer's file is incomplete or the parties dispute what information should be considered.

Can a third-party appraisal help if my car was repaired, not totaled

Yes. This is common in diminished value claims. The issue isn't replacement cost after a total loss. It's the market stigma and resale impact that remains after structural or significant accident history shows up in the vehicle record.

Accident severity and the vehicle's pre-loss value are key inputs in that analysis. More serious damage on a higher-value vehicle typically creates a stronger valuation issue than a minor repair on an older commodity car.

What if the at-fault driver's insurer denies my diminished value claim

This is one of the biggest blind spots in accident claims. A third-party insurer may deny diminished value even when the owner believes the loss is real. In some situations, the driver may be able to pivot and file under their own Uninsured/Underinsured Motorist coverage, a fallback path that's often overlooked, as noted in this discussion of the diminished value claim fallback strategy in Texas.

That doesn't mean the pivot works in every state or every policy. It means you shouldn't assume a third-party denial is the end of the road. Check your policy language, your state's rules, and whether your own coverage creates another path to pursue the same loss.

If you're dealing with a low total loss offer or a disputed diminished value claim, Total Loss Northwest can help you understand whether an independent appraisal makes sense and what evidence will matter most before you respond to the insurer.