You open the settlement email, scan the number, and your stomach drops. The truck you maintained obsessively, the SUV with new tires and recent service, the custom car you spent real money upgrading, is suddenly being valued like an average used vehicle with none of that history. That reaction is justified.

If you're dealing with a total loss in Washington, you need to stop treating the insurer's number like a verdict. It's an opening position. In a lot of cases, it's built from valuation software that misses the things that made your vehicle worth more in the actual market. A Total Loss Expert Washington vehicle owner can rely on is not someone who repeats insurance jargon. It's someone who can prove value with market evidence and force a proper dispute process when the offer is wrong.

Why Your Insurer's First Offer Is Rarely the Last Word

You paid premiums for a fair settlement. What you often get first is a number generated by a system built for speed.

The number often starts with software, not your actual car

Insurers commonly rely on tools like CCC ONE or Mitchell. Those systems don't inspect your pride of ownership. They don't care that you replaced major components, installed quality aftermarket parts, or kept the vehicle in exceptional condition. They compare data points, apply adjustments, and produce a figure.

That sounds efficient. It also creates obvious problems.

For upgraded or custom vehicles, automated tools like CCC ONE or Mitchell can miss regional pricing trends and specific modifications, and reported data shows these systems can undervalue vehicles by 15% to 25% when they ignore recent repairs, upgrades, or local market nuances, according to The Auto Mediator's analysis of total loss valuation problems.

The first offer tells you what the insurer's system produced. It doesn't tell you what your vehicle was actually worth.

I've seen owners assume the insurer already accounted for the lift kit, the wheel package, the rebuilt transmission, the recent bodywork, or the unusually clean condition. That's where they get trapped. The carrier may have priced your vehicle like a stock version in average condition because that's what the software recognized.

Why this matters more in Washington

Washington drivers feel this especially hard when the local market is stronger than the data set used in the valuation. If the comps are weak, outdated, badly matched, or pulled from outside your actual market, the offer slides downward fast.

The answer isn't to call and say the number "feels low." The answer is evidence. You need comparable vehicles, records, receipts, photos, and if necessary, an independent appraiser who works from the actual market instead of insurer software.

There's a useful contrast here. In claims operations, automation can reduce routine mistakes when it's used correctly. That's why resources like How AI reduces claims errors are worth reading. But speed and consistency don't fix a bad valuation model. If the system starts from the wrong assumptions about your vehicle, the error gets scaled, not solved.

What to do with the first offer

Treat it as the beginning of the dispute, not the end.

- Read the valuation report line by line. Don't focus only on the payout number.

- Check the comparable vehicles. Wrong trim, wrong mileage, wrong condition, wrong market. Any of those can drag value down.

- Pull your own proof. Service records, receipts, upgrade invoices, and pre-loss photos matter.

- Pause before accepting payment. Once you move too quickly, you can lose your advantage.

If you're frustrated, good. Frustration means you recognized the problem early. That's better than accepting a bad offer and trying to unwind it later.

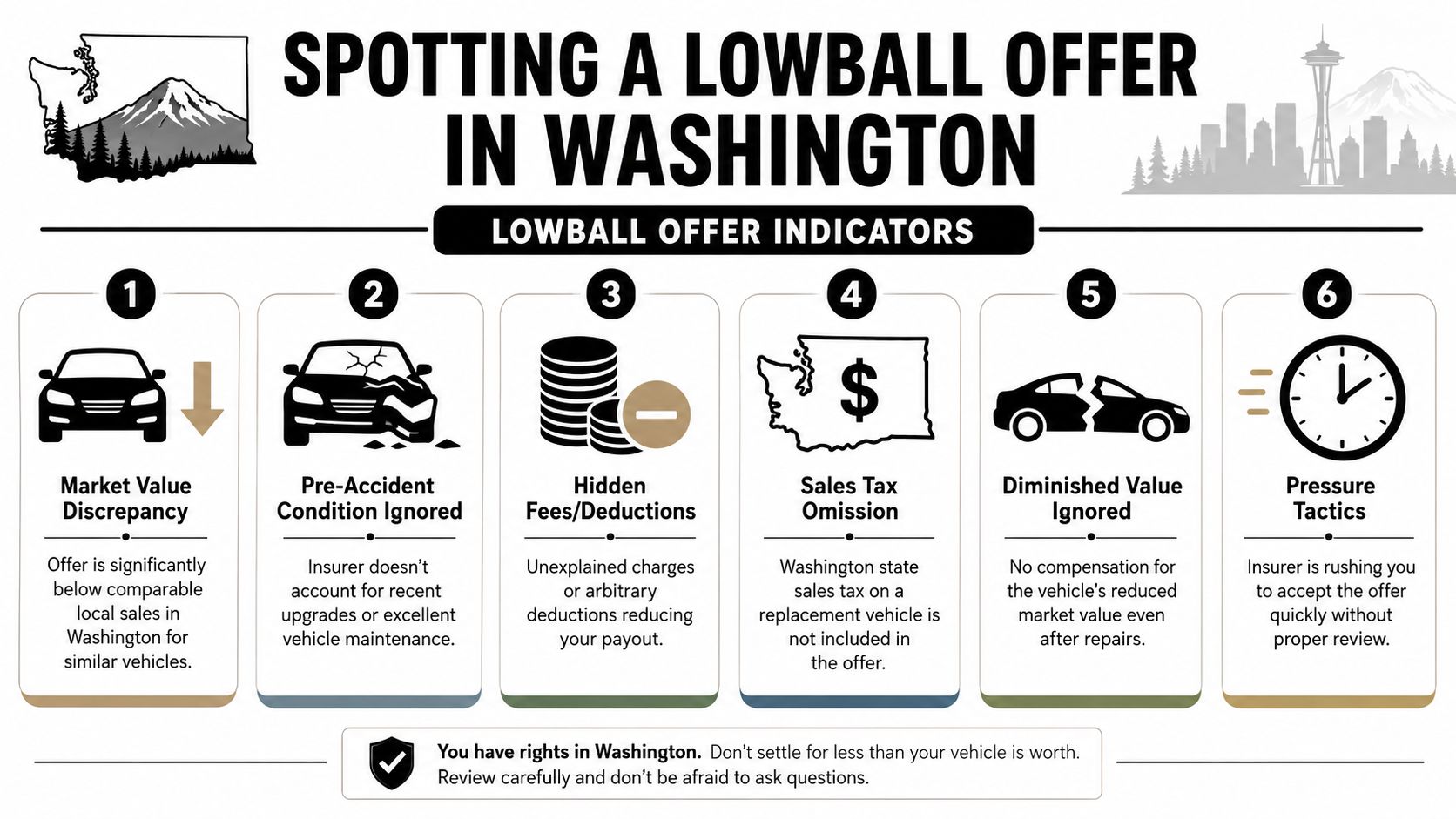

Spotting a Lowball Offer in Washington

A lowball offer usually leaves fingerprints. You just need to know where to look.

Check the valuation report before you argue

Don't call the adjuster and say the offer is unfair until you've reviewed the report. Start with the comparable vehicles used to support the settlement.

Look for these red flags:

- Wrong trim or package: A base model comp against your higher trim vehicle is a valuation shortcut.

- Mileage mismatch: Higher-mileage comps push your value down.

- Condition mismatch: If your car was clean, maintained, and mechanically sound, average-condition comps don't fit.

- Local market mismatch: A comp from a weaker market can understate what buyers in your area are paying.

- Upgrades ignored: Recent tires, mechanical work, audio, suspension, or cosmetic improvements may not appear anywhere.

One of the clearest explanations of how insurer software can distort value appears in this breakdown of CCC auto valuation issues. Read it while comparing it to your own report. You'll usually spot the shortcuts quickly.

Washington gives you more footing than most drivers realize

If the claim involves diminished value rather than a total loss, Washington is not a state where you're stuck hoping the insurer feels generous. In Washington, the statute of limitations to file a diminished value claim is 3 years from the date of the accident, and third-party claims are explicitly permitted under WAC 284-30-391. That rule requires insurers to calculate settlement as the lesser of repair costs plus the difference in fair market value before and after repair, or the difference in fair market value before the occurrence and the unrepaired value after, as explained in this summary of Washington diminished value claim rules.

That matters because the rule is built around fair market value, not a blind formula.

Practical rule: If the insurer's report doesn't reflect your vehicle's actual pre-loss market position, challenge the report, not just the payout number.

You also need to separate two issues that owners often lump together:

| Issue | What you're looking for |

|---|---|

| Total loss valuation | Whether the insurer undervalued the vehicle before the loss |

| Diminished value | Whether a repaired vehicle is now worth less in the market because of the accident history |

Signs the insurer wants speed more than accuracy

The behavior around the offer tells you a lot.

- Rushed acceptance requests: If they want quick signoff, they know delay gives you time to inspect the report.

- Vague explanations: If the adjuster can't explain the comps clearly, the file may rely too heavily on software output.

- Missing line items: If taxes, options, or condition adjustments aren't clear, ask for the full basis of valuation in writing.

- No room for discussion: That's often a negotiation tactic, not a legal reality.

Washington owners don't need to guess whether they can push back. They can. The stronger question is whether they can document why the number is wrong.

Your Documentation Checklist for a Stronger Claim

The fastest way to lose advantage is to argue from memory. Build a file instead.

Build the case file before you send one more email

When I review a disputed total loss, the owners with the strongest outcomes usually have one thing in common. They can prove what they had. Not vaguely. Not emotionally. On paper.

Use this checklist and gather everything in one folder.

| Document Type | Why It's Important |

|---|---|

| Insurance valuation report | Shows the comps, adjustments, and errors you need to challenge |

| Vehicle title and registration | Confirms ownership and exact vehicle identity |

| Window sticker or build sheet | Helps prove trim, packages, and factory options |

| Maintenance records | Shows the vehicle was cared for and supports condition arguments |

| Receipts for recent repairs | Proves money spent that may affect market value |

| Receipts for aftermarket parts | Counters base-model valuations that ignore custom equipment |

| Pre-accident photos | Documents condition, upgrades, wheels, interior, and overall presentation |

| Mileage documentation | Confirms odometer reading if the insurer used the wrong figure |

| Comparable listings you found | Gives your appraiser or dispute file local market support |

| Loan or payoff information | Helps you understand the financial gap if the settlement is low |

Why each item changes the fight

Maintenance records matter because condition isn't theoretical. If you have documented service history, the insurer has a harder time treating your vehicle like an average neglected unit.

Upgrade receipts matter because valuation tools often strip custom value out unless someone forces the issue. If you installed parts, repaired major systems, or improved the vehicle shortly before the loss, put every invoice in the file.

Photos matter more than people think. A clean interior, straight body, quality paint, and documented extras can support a better condition adjustment when the insurer's report paints your car as ordinary.

Don't make the appraiser hunt for proof you already have. Hand over a file that shows the vehicle's story in one pass.

Organize it so someone can use it fast

If your records are scattered across email, text messages, PDFs, and glove-box paperwork, consolidate them now. A simple digital file with labeled folders is enough. If you need help sorting and condensing large claim packets, a practical starting point is this guide to transforming document workflow, especially if you're dealing with long valuation reports and repair records.

You should also keep a timeline of what happened after the crash, including towing, inspection, communication with the adjuster, and any deadlines mentioned by the insurer. If you're still dealing with the aftermath of the collision itself, this checklist of steps after a car accident helps keep the claim side and the evidence side from getting mixed together.

A strong file does two things. It shows the insurer you're not bluffing, and it gives your appraiser usable material from day one.

How to Officially Invoke the Appraisal Clause

If your policy includes an appraisal clause, this is your advantage. Use it correctly or don't use it at all.

Start with the policy, not the adjuster

Find your policy and search for Appraisal. This process applies to first-party claims only, so confirm you're dealing with your own carrier under your own policy before you go further.

The standard method is straightforward. You confirm the clause exists, hire a certified independent appraiser, notify the insurer in writing that you're invoking appraisal, the insurer appoints its own appraiser, and if the two appraisers still disagree, they select a neutral umpire whose agreement with either appraiser binds the final value. That process is outlined in this explanation of how to invoke a total loss appraisal clause.

One point matters more than owners realize. You need to do this before accepting or cashing the settlement payment. Once you accept the payout in a way that closes the dispute, your options shrink fast.

The written notice needs to be clear

Don't send a rambling complaint. Send a short, direct notice.

Use language like this:

I dispute the insurer's valuation of my total loss vehicle and formally invoke the appraisal clause under my policy. I am appointing an independent appraiser on my behalf. Please confirm your appraiser in writing and direct all appraisal-related communication accordingly.

Keep it simple. Send it in a way you can document. Save the letter, the email, and any delivery confirmation.

If you want a plain-language explanation of how this clause works in an actual insurance dispute, this summary of the insurance appraisal clause process is a helpful companion to your policy language.

Choose the appraiser like the claim depends on it

It does.

You want someone who works from market evidence, understands valuation disputes, and can document condition, trim, and comparable vehicle support in a report that holds up under scrutiny. A certified independent appraiser can be critical here. In the Pacific Northwest, some firms handling total loss disputes report settlement increases of $4,000 to $6,000, with most reports delivered within 2 weeks, and identify a $550 flat upfront fee as a standard cost for USPAP-compliant appraisal work, according to Portland Total Loss's description of the appraisal process.

That doesn't mean every claim will move by that amount. It means there is an established dispute mechanism with a real track record of changing settlement numbers.

A short video can help if the clause still feels more legal than practical:

What happens after both appraisers are appointed

Owners often relax too much at this point. Stay involved, but don't interfere.

- Your appraiser evaluates the vehicle: They use your records, market comps, condition evidence, and valuation methodology.

- The insurer's appraiser does the same: Sometimes carefully. Sometimes not.

- If they agree, that's the number: The dispute ends there.

- If they don't agree, the umpire step begins: Two of the three decision-makers can bind the result.

Your job is to provide documents and stay responsive. Your appraiser's job is to argue value.

This process sounds formal because it is. That's exactly why it works. It takes the valuation fight out of call-center scripts and puts it into an evidence-based framework.

Navigating the Negotiation What to Expect

Once appraisal starts, the claim usually gets more serious. That's good. It also means you need realistic expectations.

The timeline and the money

A proper appraisal isn't a same-day favor. The vehicle has to be researched, the market has to be supported, and the report has to be credible enough to survive pushback from the insurer's side. If you're expecting instant movement, you'll get impatient at the wrong moment.

There is also the cost question, and a lot of Washington drivers get blindsided by it. Washington does not guarantee that the insurer will reimburse your total loss appraisal fee. That's a critical detail many owners don't hear up front. Industry analysis focused on Washington notes that the settlement increase often covers 70% to 90% of the appraisal fee, which is often $550 to $600, but reimbursement is not required by statute, as discussed in this review of Washington total loss appraisal fee realities.

That means you need to think like an adult making a business decision, not like a claimant hoping every cost gets shifted to the carrier.

Bottom line: In Washington, the appraisal can still make financial sense. Just don't assume the insurer has to pay for you to challenge them.

When the fee makes sense

If the vehicle is custom, collector-grade, high-trim, unusually clean, or recently improved, the risk of undervaluation is higher. In those cases, paying for a qualified appraisal often makes more sense because there is more value at stake and more room for software-driven mistakes.

If the vehicle is older, average, heavily worn, and close to commodity pricing, the math can be tighter. That's not a reason to give up. It's a reason to compare the likely gain against the appraisal cost before you commit.

Some appraisers, including firms that work in Washington total loss disputes, will review the insurer's offer and tell you whether a formal appraisal appears justified. That's the right first question. Not "Can you get me more?" Ask, "Does this file show enough valuation error to justify the expense?"

What your role should be during negotiation

After you've hired the appraiser and delivered your documents, stop trying to personally out-negotiate the insurer every day. Repeated emotional calls usually don't help.

Do this instead:

- Respond quickly to document requests

- Keep communication in writing when possible

- Don't accept or cash a disputed settlement while appraisal is active

- Let the market evidence do the heavy lifting

A higher settlement isn't automatic. A stronger challenge is. Those are different things. If your case is solid, the negotiation becomes less about persuasion and more about whether the insurer wants to defend weak valuation data in a structured process.

Next Steps if Your Insurer Still Refuses to Pay

If the insurer still won't move after a documented dispute, stop circling the same argument. Escalate.

When it's time to go beyond the adjuster

Some claims stall because the file is weak. Others stall because the carrier is betting you'll quit. If you've already documented the errors, followed the policy process, and the insurer still refuses to address obvious valuation problems, you may need legal help.

An attorney becomes more relevant when the issue stops being a normal disagreement over value and starts looking like claim mishandling, refusal to engage with evidence, or failure to follow policy procedures. Before that meeting, organize every communication, every report, and every valuation document in date order.

If you want to get smarter about legal research before paying for a consultation, tools like advanced case law AI tools can help you review legal materials and frame better questions for a lawyer.

Two practical escalation paths

- Attorney review: Best when the insurer's conduct looks unreasonable or the amount in dispute justifies formal pressure.

- Small claims court: Worth considering if the dispute is limited, the facts are clean, and you want to press the issue yourself.

Small claims can work when the evidence is simple and you can clearly show why the insurer's valuation was wrong. Bring the valuation report, your records, your comparable vehicles, your receipts, and a short timeline. Keep your explanation factual. Judges don't care that you're angry. They care whether your evidence is better.

If you're still getting stonewalled, the issue is no longer whether the offer was low. The issue is whether you're willing to force a decision.

Don't wait passively while deadlines slide by or paperwork gets buried. Claims don't improve because time passes. They improve because somebody builds a stronger file and pushes the dispute into the right forum.

If your Washington total loss offer doesn't match the actual market, get a professional review before you accept it. Total Loss Northwest provides certified independent total loss and diminished value appraisals for Washington drivers and can help determine whether your offer supports a formal appraisal dispute.