You open the email, see the number, and your stomach drops.

Your insurer says your car is a total loss. They attach a valuation report full of comps you've never seen, condition notes you don't agree with, and a settlement figure that won't buy anything close to what you had. You're already dealing with the crash, the rental, the loan, the title, and now they want you to accept a number that feels wrong.

That reaction is usually correct.

I've seen this from the appraiser's side. The first offer often reflects the insurer's system, not the actual replacement market you have to shop in. Their valuation may be structured and standardized, but that doesn't make it accurate. If the mileage is off, the trim is wrong, the options are missing, or the comparable vehicles aren't comparable, the settlement drops fast.

For drivers in Oregon and Washington, there's one point you need to understand early. You are not stuck with the insurer's number just because they printed it on company letterhead. In many policies, the Appraisal Clause gives you a direct way to challenge a low valuation without filing a lawsuit. That clause matters. It changes the conversation from “please reconsider” to “let's use the dispute process in the policy.”

Your Car Is Totaled Now What

You're sitting at the kitchen table with the valuation report in one hand and your phone in the other, trying to figure out whether you're missing something. The insurer says they used market data. You look online and can't find an equivalent vehicle anywhere near their number. Your car had the better trim, better maintenance history, and cleaner condition than what they're crediting.

Many individuals begin their journey at this exact point. Confused, rushed, and pressured to move on.

If that's you, start with this plain-English overview of what to do when your car is totaled. Then slow the process down and review every line before you agree to anything.

Why this keeps happening

This isn't a one-off problem. It's showing up more often because total loss claims themselves have become more common. The share of claims flagged as total loss hit a record in 2024, and through April 2025, 22.6% of all losses were declared total losses, up 0.9 percentage points year over year, according to Preqin's cited market summary. That same source notes that over 70% of total loss valuations in 2024 involved vehicles 7 years or older, rising to 74% in Q1 2025.

Older vehicles create valuation fights because condition, maintenance, trim level, prior damage, and local market demand matter more. Two cars with the same badge on the trunk can produce very different settlement values.

A total loss offer is not automatically a fair value. It's the insurer's starting position based on the inputs they chose.

What you should assume right now

Assume the first number needs checking. Not because every insurer acts in bad faith, but because the process is built around speed and standardization. That means errors happen, and those errors usually don't help you.

Focus on three immediate questions:

- Is the vehicle identified correctly: Year, make, model, trim, drivetrain, package, and mileage all need to be right.

- Did the report account for condition: Clean paint, interior care, service history, and major component replacement can matter.

- Are the comps legitimate: They should reflect your actual market, not a weak substitute list designed to pull value down.

If the offer feels low, you're probably not being difficult. You're seeing a system problem.

Understanding Total Loss Settlement Services

Total loss settlement services exist because insurers use valuation systems that are efficient, but not always complete. A good independent appraiser doesn't guess and doesn't just “argue for more.” The job is to rebuild value from the ground up using the correct vehicle configuration, the actual market, and supportable adjustments.

Hiring a professional for this process is comparable to hiring your own home inspector before buying a house. You don't rely only on the seller's version of condition. You bring in someone whose job is to verify what is there.

How the insurer builds its number

Insurers typically compare estimated repair cost against the vehicle's Actual Cash Value, then use automated valuation platforms that pull from comparable vehicles, mileage, condition, features, and options. Mitchell describes this as a structured workflow that also uses VIN decoding and build data, and notes that owner documentation such as service records, trim details, invoices, and photos can affect the ACV inputs in the valuation model on its total loss solutions page.

That process sounds neutral, and sometimes it is. However, here is where it breaks down in practice:

- Wrong trim or package lowers the baseline value.

- Missed options erase value you paid for.

- Condition downgrades can be overly harsh or unsupported.

- Weak comparable vehicles drag the market average down.

- Geographic mismatches use vehicles from the wrong market.

What an independent appraiser actually does

An independent appraiser should verify facts, not just complain about the insurer's report. That means inspecting documentation, checking how the VIN decodes, confirming installed equipment, reviewing maintenance history, and comparing the insurer's comps to the vehicles that compete with yours in the open market.

Here's the difference in plain terms:

| Issue | Insurer workflow | Independent review |

|---|---|---|

| Vehicle setup | Relies on decoded data and internal report | Verifies trim, options, packages, and equipment |

| Condition | Applies standardized adjustments | Checks whether those adjustments fit the actual car |

| Market comps | Uses selected comparable units | Challenges bad matches and finds stronger comparables |

| Goal | Close the claim | Support a defensible ACV |

Practical rule: If the report contains one clear error, keep looking. Valuation errors tend to come in clusters.

What helps your side most

You have more bargaining power than you think if you bring evidence.

Gather these before arguing about value:

- Service records that show consistent maintenance

- Window sticker or build information showing trim and packages

- Receipts for recent work such as tires, suspension, or major repairs

- Photos showing pre-loss condition

- Records of aftermarket equipment if it adds recognized value

Many owners lose money at this stage of the process. They know their car was nicer than the report suggests, but they don't document it in a way the valuation process can absorb.

Using the Appraisal Clause Your Secret Weapon

Claimants often overlook the strongest tool in their own policy. They call the adjuster, complain, send screenshots, and wait for goodwill. That's backwards.

If your policy includes an Appraisal Clause, you may have a contractual method to dispute the amount of loss. That's not a lawsuit. It's not a threat. It's the process built into the policy for valuation disputes.

For a direct breakdown, review this guide to the insurance appraisal clause.

What the clause does

The Appraisal Clause usually allows each side to hire its own appraiser when they disagree on value. Those appraisers try to reach agreement. If they can't, the process typically moves to the next contractual step described in the policy.

That matters because it changes the dispute from insurer-controlled review to a structured valuation process with independent input.

Owners in Oregon and Washington should pay attention here. The clause is often the cleanest way to fight a low total loss number without getting dragged into an endless adjuster loop.

Why insurers don't lead with it

Insurers generally won't rush to tell you about the mechanism that takes valuation out of their internal software pipeline. Their playbook is simple.

- They issue a fast number

- They create urgency

- They frame the report as objective

- They wait to see if you'll sign

None of that means you have to accept the result.

The moment you invoke appraisal, the conversation stops being “please review again” and becomes “let's follow the contract.”

A short explainer may help if the idea is new to you:

When to use it

Use the Appraisal Clause when the dispute is about value. Not coverage. Not liability. Value.

Common examples include:

- Bad comparable vehicles that don't match your trim or market

- Condition deductions that overstate wear or prior issues

- Missing options such as premium packages or factory equipment

- Collector or specialty vehicles that generic databases handle poorly

If your dispute is about whether the policy covers the loss at all, that's a different fight. But when the insurer agrees the car is totaled and you disagree with the dollar amount, appraisal is often the correct lane.

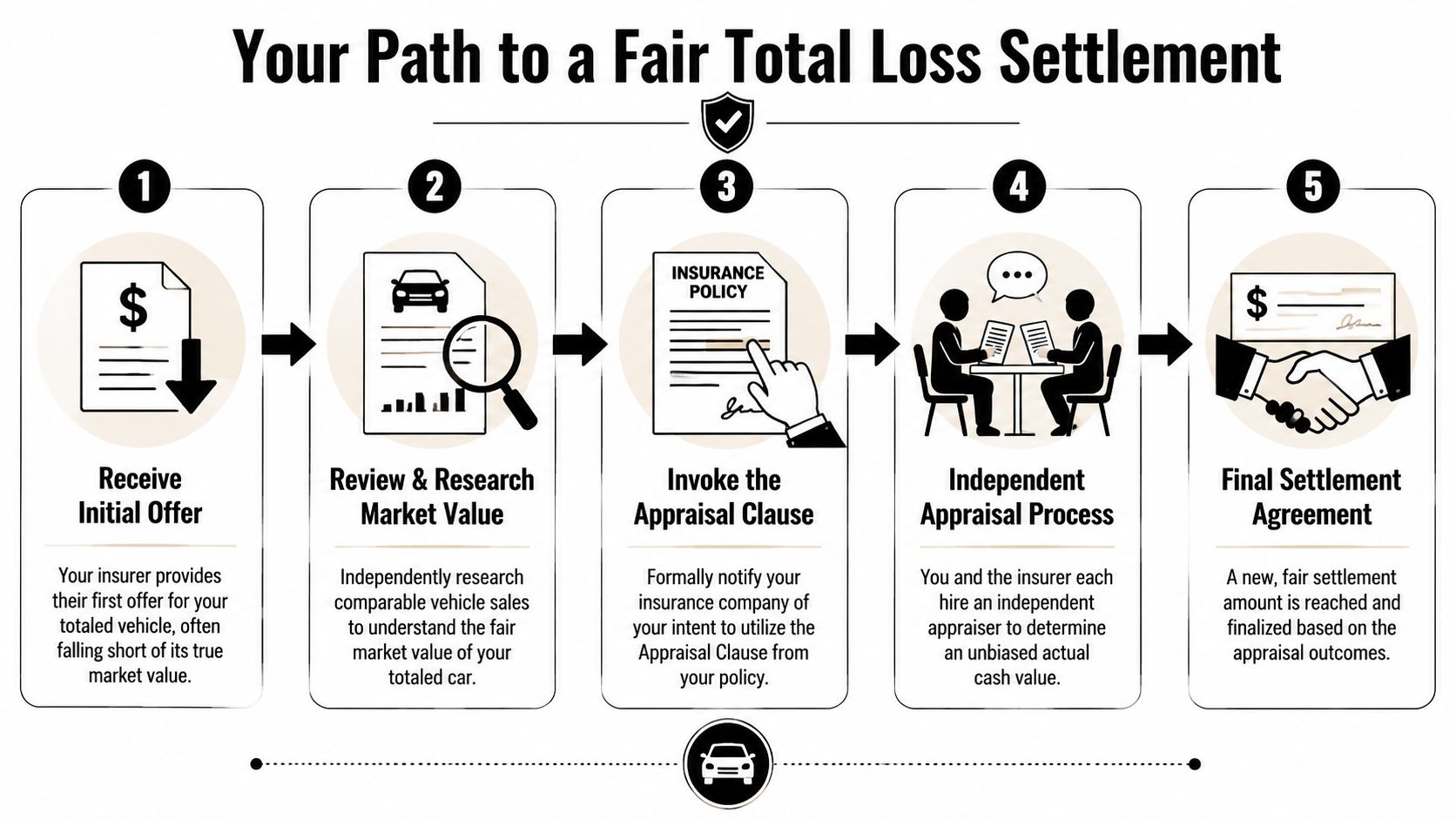

Your Step-by-Step Total Loss Settlement Process

The insurer sends a number. It looks official. The adjuster sounds confident. You still need to slow the claim down and check the math before you give up your bargaining power.

Step 1 Pause the claim before the insurer sets the pace

Insurers benefit when owners act fast. Their playbook is simple. Put a value in front of you, make it sound final, and see whether you accept it before reviewing the report.

Do not sign anything until you know exactly what it does. Ask for the settlement paperwork in writing. Ask what the payment covers, whether any release is included, and whether the carrier considers the property damage portion closed if you deposit the check.

If you have injury issues tied to the same loss, read every line carefully and separate the vehicle settlement from any bodily injury claim.

Step 2 Get the valuation report, not the adjuster's summary

A phone explanation is not evidence. You need the full valuation report in writing.

Request the comparable vehicles, trim level, mileage, condition adjustments, options list, taxes and fees treatment, and every deduction or addition used to calculate actual cash value. If the carrier used a third-party vendor, get that full report too.

Low offers usually originate here. The software output gets treated like a fact, even when the inputs are wrong.

Step 3 Check every line item like an appraiser would

Read the report slowly. Owners who do this often find the problem within minutes.

Focus on the items that move value the most:

- Wrong trim or drivetrain

- Missing factory packages or major options

- Incorrect mileage

- Unsupported condition deductions

- Comparable vehicles from the wrong market area

- Aftermarket or recent upgrades ignored entirely

- Prior damage notes that are vague, inflated, or unproven

Lowball settlements rarely come from one giant error. They come from a stack of smaller ones that push the number down.

Step 4 Build a file that supports your car's real market value

Pull together the documents that prove what the vehicle was before the loss. Good photos matter. Service records matter. Purchase documents, original window sticker details, tire invoices, recent maintenance, and receipts for major repairs all matter.

Keep your communication organized too. A clear written record makes it harder for an adjuster to dodge the issue or reset the conversation. If you want a practical format for laying out your position, this demand letter guide for car accidents is a useful model.

One strong file beats ten angry phone calls.

Step 5 Bring in an independent appraiser before the dispute drags out

Once you have the report and your supporting records, decide whether the valuation dispute is big enough to justify outside help. In many cases, it is.

A qualified independent car appraiser for a disputed total loss should review the insurer's report, identify valuation errors, support a market-based actual cash value, and prepare the claim for formal appraisal if the policy allows it. That matters in Oregon and Washington, where owners often get pushed into accepting weak comparable vehicles and inflated condition deductions unless someone challenges the file correctly.

Ask one question. Can this person support a defensible number with market evidence and explain it clearly?

Step 6 Use the process and stay patient

Once the value dispute is documented, the claim may slow down. That is normal. A slower process with a supported number is better than a fast underpayment.

If you still owe money on the vehicle, every dollar of actual cash value matters. A weak settlement can leave you short on replacement money or stuck with a loan balance after the car is gone. Experian's total loss settlement process guide explains that lienholders generally get paid first, with any remaining balance going to the owner.

Stay organized. Keep everything in writing. Push the claim onto evidence, policy language, and appraisal procedure instead of the insurer's preferred cycle of delay, repetition, and pressure.

How to Choose a Reputable Total Loss Appraiser

The right appraiser can clarify a claim. The wrong one wastes your time, inflames the adjuster, and hands you a glossy report that won't move the number. Choose carefully.

Start with competence, not marketing. You want someone who understands valuation methodology, insurer reports, vehicle configuration, and policy-based dispute procedures.

What to ask before hiring anyone

Use these questions and listen for direct answers.

What kinds of vehicles do you handle most often

A daily-driver valuation is different from a collector car, modified truck, or high-end import. Experience should match the vehicle.How do you develop value

They should talk about comparable vehicles, options, condition, market support, and correcting insurer report errors. If they only say they “fight insurance companies,” keep looking.Do you work with Appraisal Clause disputes

A valuation report is one thing. A report built for contractual dispute resolution is another.How do you charge

Ask whether the fee is flat, hourly, or tied to the outcome. You want a clear written explanation.Will you review my insurer's report with me

A serious appraiser should be willing to identify strengths and weaknesses in the carrier's valuation.

For a local benchmark, review what an independent car appraiser should do in a disputed loss.

Good signs and bad signs

A reputable appraiser usually sounds measured. They won't promise a miracle because honest valuation work doesn't come with guarantees.

Here's a quick screening table:

| Green flag | Red flag |

|---|---|

| Explains methodology clearly | Promises a guaranteed payout |

| Reviews insurer comps in detail | Talks only in generalities |

| Understands Oregon and Washington claim practice | Has no regional familiarity |

| Requests documents and photos | Barely asks for evidence |

| Distinguishes value disputes from legal disputes | Pretends every claim is the same |

My blunt advice

Avoid anyone who sells anger more than analysis. You don't need a louder voice. You need a stronger file.

The appraiser should be able to explain why a comp is weak, why an option matters, how condition should be handled, and where the insurer's report falls short. If they can't teach you their process in plain English, they probably can't defend it well either.

Special Considerations for Oregon and Washington Drivers

Drivers in Oregon and Washington need local awareness, not generic internet advice. Total loss rules are not uniform across the country, and state-level differences can change whether a vehicle is declared a total loss and how the valuation dispute plays out.

Why regional rules matter

Industry reporting notes that total-loss thresholds vary widely by state. Some states use a fixed percentage threshold, with examples cited as 60% in Oklahoma and 100% in Texas, while states such as California and others in the West use a Total Loss Formula where Repair Cost + Salvage Value > ACV, as described in this industry overview of total-loss thresholds and repair-cost pressure.

That matters for Oregon and Washington drivers because western claim handling often requires closer attention to formula-based total loss decisions rather than relying on a simple percentage rule you saw in an article written for another state.

What that means in practice

If your insurer tells you, “The repairs are below the vehicle's value, so this shouldn't be a total loss,” that statement may be incomplete in a formula-based environment. Salvage value can change the outcome.

If they total the vehicle quickly, the next fight becomes value. That's where local market knowledge matters most. A Portland-area buyer market is not the same as Spokane. Seattle retail listings aren't interchangeable with rural eastern Washington. Oregon coast inventory isn't the same as metro inventory.

Use this local checklist:

- Check market geography so the comparables reflect where a replacement vehicle would realistically be sourced

- Verify trim naming and package content because northwest inventories often mix shorthand listing language

- Confirm treatment of condition especially on older vehicles with strong maintenance history

- Ask about taxes and fees tied to replacement if those items are relevant to your claim handling

A total loss claim in the Pacific Northwest is won or lost in the details. The rule set matters, but the comp selection usually matters more.

Why Oregon and Washington owners should use the Appraisal Clause early

In these states, many drivers lose time trying to negotiate informally with adjusters who recycle the same report. If the dispute is value, moving to appraisal early often produces a cleaner, more disciplined process.

That's especially true for vehicles that generic software undervalues, including well-kept older cars, limited trims, enthusiast vehicles, and vehicles with documented maintenance that doesn't show up on a basic data pull.

Common Questions About Total Loss Claims

How much does an independent appraisal cost, and who pays for it

Ask for the fee in writing before you hire anyone. A straight total loss appraisal usually costs less than a drawn-out dispute that leaves you underpaid by thousands. In an appraisal clause claim, each side usually pays its own appraiser unless your policy says something different. Read the policy yourself.

Can I keep my totaled car

Yes, in many cases. The insurer will usually subtract the salvage value from your settlement, and the title may be branded. Oregon and Washington drivers also need to confirm what inspection, registration, and repair rules apply before agreeing to keep the vehicle. Do not rely on a phone call summary. Get the terms in writing.

What's the difference between a total loss claim and a diminished value claim

A total loss claim is about what your vehicle was worth one minute before the crash. A diminished value claim is about what a repaired vehicle is worth after the crash history attaches to it.

Insurers mix these concepts up all the time because it benefits them when owners do not know which claim they are dealing with. Keep the issue narrow. If the vehicle is a total loss, the fight is pre-loss market value.

What if the two appraisers can't agree

Your policy controls the next step. In many appraisal clause disputes, the appraisers choose an umpire. If they still cannot get to the same number, the decision process usually goes to that umpire.

This is why choosing a real total loss appraiser matters. A weak appraiser will fold. A qualified one will document the right comparables, challenge bad condition adjustments, and force the insurer to defend its numbers instead of repeating them.

Should I accept the first offer if I need money fast

Do not accept a bad number just because the insurer put a deadline on it. That pressure is part of the playbook.

At minimum, get the valuation report, check the comparable vehicles, confirm the trim and options, and have an independent appraiser review it before you sign anything. Once you sign a release, your bargaining power usually disappears.

I already took a check. Is it too late

Not always. The answer depends on what the payment was for and what you signed when you accepted it. Cashing a check does not automatically end every part of your claim, but a signed release can.

If the crash also involved bodily injury, read this guide on filing an injury claim after payment. The key point is simple. Payment and full release are not always the same thing.

If your insurer's total loss offer does not match the market, pause before you sign. Get the report. Get it reviewed. Then decide whether to invoke the appraisal clause and force a fair value discussion. Total Loss Northwest handles independent total loss appraisals and appraisal clause disputes for drivers in Oregon and Washington.