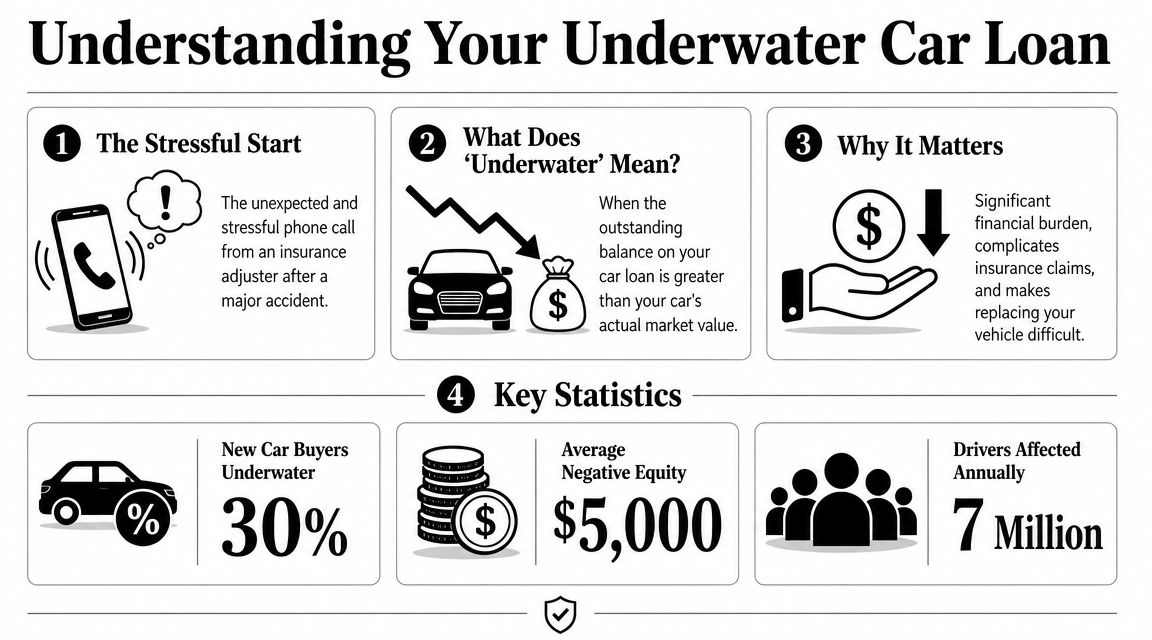

The call usually goes like this. The adjuster says your car is likely a total loss, explains that payment will be based on market value, and then goes quiet while you do the math in your head. You still owe the lender. You need another vehicle. You're already bracing for a number that won't be enough.

If you have an underwater car loan, a total loss turns a bad day into a debt problem fast. That's the part many drivers don't see coming. They assume insurance pays off the loan. It doesn't. Insurance pays what the vehicle was worth under the policy, not what you still owe.

I've seen people make the same mistake over and over. They accept the first valuation, sign paperwork too early, and only then realize they still owe a deficiency balance on a car they can't drive. Don't do that. If you're in this spot, you need a plan, not generic advice about “paying extra when you can.”

What Is an Underwater Car Loan and Why It Matters

An underwater car loan means your loan balance is higher than the vehicle's current market value. You owe more than the car is worth. It's the same basic problem homeowners face when a house drops in value below the mortgage balance.

That situation happens for ordinary reasons. You financed too much. The car depreciated faster than the loan balance dropped. You took a long term to keep the monthly payment manageable. You put little down. Or you rolled old debt from a previous vehicle into the next one.

None of that makes you reckless. It makes you normal in a market where depreciation and financing terms can work against you.

The problem is widespread

You are not alone in this. Edmunds reported that 28.1% of trade-ins toward new-car purchases had negative equity in its Q3 analysis, and the average amount owed on upside-down auto loans reached $6,905 in that same release. Edmunds said that was the highest share it had recorded since Q1 2021. You can review that data in the Edmunds Q3 negative equity analysis.

That matters because panic makes people do expensive things. They trade too early, roll debt into another loan, or accept a low insurance settlement because they think there's no other option.

Practical rule: If your car is totaled and you still owe money, your first job is not shopping for the next car. Your first job is protecting the valuation of the one you just lost.

Why this gets dangerous fast

An underwater loan doesn't always create an immediate crisis. If the car stays drivable and you keep making payments, time can solve part of the problem. A total loss changes everything because the loan doesn't disappear when the vehicle does.

Here's where people get trapped:

- Insurance pays value, not payoff: Your lender wants the loan balance. Your insurer owes actual cash value under the policy.

- The difference becomes your problem: If the settlement is short, you may still owe the lender after the claim closes.

- Replacing the car gets harder: You may need cash for the deficiency and cash for the replacement.

If you're also behind on payments or worried about repossession, get legal and practical guidance quickly. A state-specific resource like this Georgia guide to stop repossession can help you understand immediate options before the account gets worse.

The Total Loss Trap When You Have Negative Equity

The trap is simple. Your car is gone, but the debt survives.

Most drivers don't realize how the claim works until the numbers hit. The insurer calculates actual cash value, often called ACV. That's the carrier's opinion of what your vehicle was worth immediately before the loss, based on condition, mileage, options, and comparable vehicles. The lender, meanwhile, cares about only one number: the payoff.

Those two numbers are often far apart.

Why the shortage happens

Insurance doesn't insure your financing decision. It insures the vehicle under the policy. So if you financed taxes, fees, add-ons, or old negative equity, none of that automatically increases the total loss settlement. That debt may still be sitting on the loan long after the car's market value has fallen.

The blind spot is serious. The gap between an insurance payout and a loan balance is a major financial risk, and many consumer guides still spend more time on refinancing and trading than on the actual claims sequence after a total loss, as discussed in this consumer-focused explanation of the total loss gap problem.

Sample Total Loss Calculation

Below is the exact math you need to run the moment the carrier says “total loss.”

| Line Item | Amount | Description |

|---|---|---|

| Loan payoff | Your lender's payoff quote | The amount required to satisfy the loan as of a specific date |

| Insurance settlement | Insurer's ACV offer minus deductible, if applicable | What the carrier says the vehicle was worth under the policy |

| Deficiency balance | Payoff minus settlement | The amount you may still owe after insurance pays |

That last line is the whole fight. If there's a deficiency balance, you need to reduce it any way you legally can. The fastest lever is often the vehicle valuation itself.

Don't confuse a claim with a payoff

You need to separate three issues that people mash together under stress:

- What the vehicle was worth

- What the insurance company is offering

- What the lender is still owed

Those are related, but they aren't the same.

If the carrier undervalues the car, the deficiency gets bigger. Every dollar lost in valuation can become a dollar you still owe.

Before you discuss replacement vehicles, dealer offers, or loan rollovers, understand what happens in a financed total loss claim. This overview of what happens if you total a financed car is useful because it keeps the sequence clear: insurer valuation, lender payoff, then the remaining gap.

Immediate Steps to Take After Your Car Is Totaled

When the car is declared a total loss, the first two days matter. Small mistakes at this stage can box you into a weak settlement later. You need to slow the process down just enough to stay in control.

First calls and first documents

Start with the insurer if you haven't already opened the claim. Then contact your lender and ask for a written payoff quote with an expiration date. Don't rely on the balance shown in your app or monthly statement. You need the payoff amount, not a rough estimate.

Gather these documents in one folder:

- Loan paperwork: Your retail installment contract, recent statements, and payoff contact info

- Insurance documents: Declarations page, coverage details, deductible, and any GAP paperwork

- Vehicle records: Title or registration, service records, receipts for recent work, and option packages

- Loss evidence: Photos of the vehicle before and after the accident, police report if available, towing and storage info

What to say and what not to say

Keep your early conversations clean and short. You are reporting, not negotiating yet.

Use language like this with the adjuster:

“Please send me the valuation report, the comparable vehicles used, the condition adjustments, and the full settlement breakdown in writing.”

Use language like this with the lender:

“My vehicle may be a total loss. I need the current payoff quote, where insurance should send payment, and whether you have any forms I need to complete.”

Avoid these mistakes:

- Don't accept verbally on the first call: Ask for the valuation documents first.

- Don't guess about condition or prior damage: If they ask, answer carefully and stick to facts.

- Don't sign title or power-of-attorney forms immediately: Read them after you've reviewed the valuation.

- Don't stop making payments without a plan: A pending total loss claim doesn't automatically pause your loan obligations.

Build your file before the argument starts

A strong dispute file is boring, organized, and effective. Save every email. Write down claim numbers, names, and call times. If you had recent maintenance or repairs that affected condition, pull those invoices now.

Your checklist should include:

- Written valuation report from the insurer

- Payoff quote from the lender

- Photos showing pre-loss condition

- Window sticker or build sheet if available

- Receipts for tires, major service, and relevant equipment

- Your own notes on mileage, trim, packages, and condition

If you have GAP coverage, read the claim instructions before the settlement is finalized. If you don't, your dispute over ACV matters even more because that valuation may directly affect how much debt survives the loss.

How to Dispute a Low Total Loss Insurance Offer

The insurer's first number is not sacred. It's an opening position.

A low total loss offer usually comes from bad comparable vehicles, missed options, weak condition ratings, or valuation software that treats your car like a generic unit instead of the actual vehicle you owned.

Start with the valuation report

Read every line. It's often overlooked. That's where the errors hide.

Check for these problems:

- Wrong trim or drivetrain: A small trim error can distort value fast.

- Missing factory options: Sunroof, safety packages, premium audio, towing package, upgraded wheels.

- Bad comparables: Vehicles from far away, different equipment, or poor condition.

- Condition downgrades with no support: Interior, exterior, tires, and prior condition ratings.

- Mileage errors: Even a simple odometer mistake can move the number.

Push back in writing. Be specific. “Your report missed the premium package and used comps with materially different equipment” is useful. “I think the offer is too low” is not.

Build a market-based counter

You need evidence tied to your actual vehicle. That usually means local or regional comparable sale listings, proof of equipment, service records, and photos showing condition before the loss. Don't dump a pile of screenshots into an email and hope for the best. Explain why each piece matters.

A simple structure works:

- Identify the report error.

- Attach proof.

- State the correction you want.

- Ask for a revised valuation.

What wins disputes: Specific corrections beat emotional arguments every time.

If the insurer valued your vehicle using CCC, it helps to understand how that system works and where it can go wrong. This breakdown of CCC auto valuation issues gives you a practical lens for reviewing the report instead of just reacting to the bottom-line number.

Use the appraisal clause when negotiations stall

This is the tool most drivers never use, and they should.

Many auto policies include an appraisal clause. When you and the insurer disagree on value, that clause can let each side hire an appraiser. If the appraisers disagree, an umpire may decide the disputed amount under the policy process. That moves the fight away from a one-sided software output and toward an independent valuation process.

That matters because you don't need to win a philosophical debate with the carrier. You need a credible, defensible value supported by someone who knows total loss appraisal.

A short explainer can help if this process is new to you:

If your policy has an appraisal clause, use it strategically. One option is hiring an independent appraiser such as Total Loss Northwest to review the valuation and invoke that clause on your behalf when appropriate. The point isn't to escalate for sport. The point is to stop arguing in circles when the report itself is flawed.

Clearing the Deficiency Balance After a Settlement

Even if you improve the settlement, you may still owe money. That leftover debt is the deficiency balance. Deal with it directly. Don't bury it inside your next vehicle unless you've run the numbers and have no safer alternative.

Your main options side by side

| Option | How it works | Best use | Main risk |

|---|---|---|---|

| GAP claim | GAP may cover part or all of the remaining balance after the insurance settlement, depending on the contract | You already bought GAP and the loss qualifies | Exclusions, limits, and paperwork delays |

| Lender negotiation | You ask the lender to settle for less, waive fees, or accept a payment plan | You have no GAP or GAP doesn't cover the full gap | The lender may refuse or demand quick payment |

| Personal loan or structured repayment | You separate the leftover debt from vehicle financing | You need manageable terms and can qualify | Higher cost if terms are poor |

| Rolling into a new auto loan | Dealer or lender adds old debt to the next loan | Last resort only | You start the next vehicle underwater |

GAP first, then lender strategy

If you bought GAP, file that claim immediately and follow the instructions exactly. Ask what documents are required, where the insurer's payment needs to be sent, and whether the GAP administrator needs the final settlement letter. Keep copies of everything.

If you don't have GAP, call the lender before the account becomes delinquent. Be direct. Ask whether they'll consider a reduced lump-sum settlement, a hardship arrangement, or a fixed payment plan on the unsecured remainder after the insurance proceeds are applied.

The CFPB found that borrowers who finance negative equity are more than twice as likely to have the loan assigned to repossession within two years compared with borrowers who had positive equity trade-ins, according to the CFPB negative equity report.

What I recommend and what I don't

I recommend this order:

- First, use GAP if you have it: That's the cleanest path.

- Second, negotiate the remaining balance directly with the lender: Especially if you can offer a partial lump sum.

- Third, use a separate repayment method if needed: Keep the old debt isolated.

I do not recommend rolling the deficiency into your next auto loan unless every other option has failed. That move keeps the crisis alive. It also creates a new car payment built on old debt.

If you're trying to understand how GAP fits into this decision, this guide on whether GAP insurance is worth it is useful because it focuses on the primary problem: the loan shortfall after a total loss.

If you're considering surrendering the vehicle or you're already in default on another account, learn the consequences before acting. A state-specific legal explainer like this article on voluntary repossession in Utah can help you understand why surrender rarely wipes out the debt the way people hope it will.

The cleanest financial move is often the least exciting one. Settle the old balance, keep the next loan separate, and stop the cycle there.

Frequently Asked Questions About Underwater Loans

Can I voluntarily surrender the car and make this go away

No. Voluntary surrender usually gives the lender the vehicle back, but it doesn't erase what you owe. The lender can sell the vehicle and then pursue you for the remaining balance, plus allowed fees and costs under the contract and state law. Surrender can reduce collection pressure in some situations, but it's not debt forgiveness.

What happens if I stop paying the deficiency balance

The account can go delinquent, move to collections, and trigger credit damage and possible legal action. Whether a lender sues depends on the balance, the contract, and state law, but not communicating is the worst approach. If you can't pay in full, call early and try to negotiate before the file gets uglier.

Does bankruptcy erase a deficiency balance

Sometimes, but that's a legal question, not a valuation question. A deficiency balance is generally a debt, and some debts can be discharged or restructured in bankruptcy depending on your case. You need a bankruptcy attorney in your state to tell you what applies to your income, assets, and other obligations.

If I pay the deficiency, does that fix my credit

Paying it helps close the account and reduces the risk of further damage, but it doesn't rewrite the past. If there were late payments, collections, or a repossession-related event, those can remain on your credit report for a period set by credit reporting rules. Paying still matters because unpaid debt keeps causing problems.

Should I replace the car right away

Only if you must. If you can borrow a family vehicle, use transit, work remotely, or rent short term while the claim is sorted out, that breathing room can save you from rushing into another bad loan. Urgency is exactly what dealers and lenders use to make ugly numbers look “affordable” on a monthly payment basis.

What's the smartest move if I'm underwater but the car isn't totaled

Usually, keep the current vehicle, pay down principal aggressively if possible, and avoid trading unless there's a compelling reason. Treat it as a debt problem first. Chasing a lower monthly payment while extending the term often keeps you underwater longer.

If the insurer's total loss offer is too low, don't accept a weak valuation and hope the debt problem sorts itself out later. Total Loss Northwest handles total loss appraisals and appraisal clause disputes for drivers who need an independent valuation to challenge the carrier's number. If your settlement amount will decide whether you still owe money after the claim, get the valuation reviewed before you sign.