You open the claim portal, read the valuation, and feel that sinking mix of anger and confusion. The insurance company says your vehicle is worth less than what you know similar vehicles sell for in Vancouver. The adjuster sounds confident. The report looks official. But the number still feels wrong.

That reaction is common, and in many cases it's justified. A lot of people search for a Vancouver WA appraiser at this point and end up in the wrong lane entirely. They find real estate appraisers, county property information, or generic valuation pages that have nothing to do with accident claims. That's a serious mismatch when the problem is an auto total loss or a post-repair value drop.

The Insurance Offer Is In Now What

The first mistake most drivers make is assuming any “appraiser” can help. In practice, a home appraiser and an auto appraiser solve completely different problems.

A real estate appraiser works on houses, refinance files, estates, and lender requirements. An auto appraiser works on damaged vehicles, total loss disputes, diminished value, comparable vehicle research, policy language, and insurer valuation methods. If your carrier just declared your car a total loss or made an offer that doesn't line up with the local market, you need the second one.

Recent information tied to the “Vancouver WA appraiser” search term shows that most content doesn't make this distinction, even though 68% of total loss claims in Washington State involve settlements below actual market value because insurers rely on biased software, which independent auto appraisers are equipped to challenge, as noted in this Washington claim valuation discussion.

What usually happens after the offer lands

The insurance company sends over a valuation packet. You skim it and notice a few familiar problems:

- Wrong comparables that don't reflect your trim, mileage, options, or condition

- Condition adjustments that seem harsh in one direction and generous in the insurer's direction

- Missing local market context for Vancouver and the surrounding area

- Pressure to settle fast before you've had time to review the report carefully

That last part matters. A rushed settlement often becomes a final settlement.

Most bad vehicle settlements don't happen because the owner has no case. They happen because the owner accepts the insurer's number before anyone checks the math.

If the claim has already turned tense, it can also help to understand how broader expert insurance dispute resolution works when a carrier digs in. An appraiser and an attorney do different jobs, but both become relevant when an insurer treats its first number like the last word.

For drivers dealing specifically with a total loss dispute in Clark County, a practical next step is to review how a Vancouver total loss appraiser approaches market valuation, report support, and policy-based dispute handling.

The core shift in mindset

Don't treat the insurance valuation as a verdict. Treat it as an opening position.

Once you see it that way, the path gets clearer. You stop asking, “Why are they doing this?” and start asking, “What evidence do I need to challenge it?”

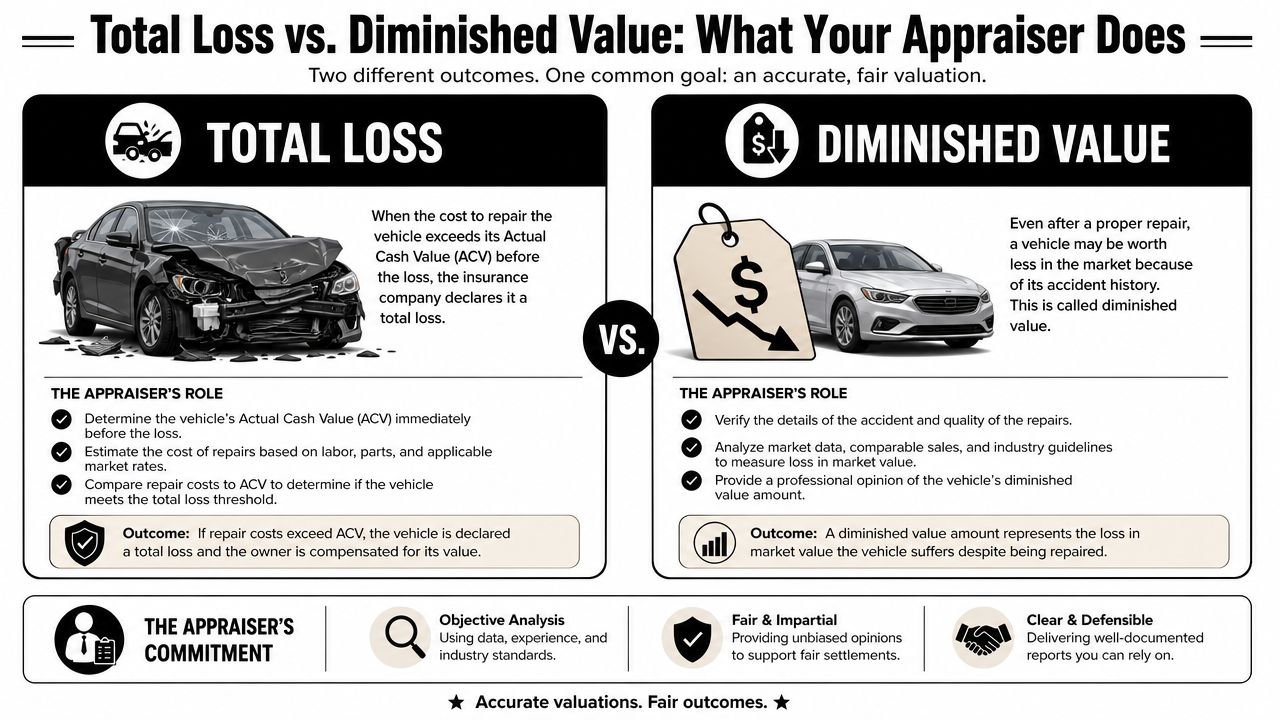

Total Loss vs Diminished Value What Your Appraiser Does

Most accident-related auto appraisals fall into two categories. Total loss and diminished value. People often know about the first one and miss the second.

That's a costly oversight, especially when the vehicle is repaired but still worth less on the open market because it now carries an accident history.

Total loss work

A total loss appraisal answers one question. What was the vehicle's actual market value immediately before the loss?

That sounds simple, but it rarely is. The answer depends on the right comparable vehicles, proper option matching, condition support, title history review, prior damage analysis, and local market judgment. If the insurer's valuation software starts with bad inputs or weak comparables, the payout can come in low.

An independent appraiser's role is to rebuild that value from market evidence, not from the carrier's preferred template.

Diminished value work

Diminished value is different. Your car is repaired. It drives fine. But buyers still pay less for a vehicle with an accident record than for a similar clean-history vehicle.

That lost resale value is real, and it often gets ignored. A key question many drivers miss is whether an auto appraiser can handle diminished value on a repairable car. The answer is yes. The Insurance Research Council figure cited in this diminished value FAQ context notes that 42% of Washington drivers in non-total loss accidents face an average hidden value loss of $1,800 per vehicle.

A repaired car and an undamaged car are not the same asset in the marketplace, even if the repair work is excellent.

A simple way to think about it

Use this comparison:

| Claim type | What happened to the vehicle | What the appraiser measures |

|---|---|---|

| Total loss | The vehicle is written off | Pre-loss market value |

| Diminished value | The vehicle is repaired | Post-accident loss in market value |

That's why a generic appraiser won't help much here. This work depends on insurance claim mechanics and vehicle-specific valuation.

If you want a plain-language example of how repair costs and insurance conversations can quickly get complicated even in a lower-impact crash, this overview of NY car repair bills and insurance is useful background. The state is different, but the consumer problem is familiar. Repair economics and insurance positioning often drift apart.

When each service makes sense

- Use a total loss appraisal when the insurer has declared the car a total loss or is close to doing so.

- Use a diminished value appraisal when the car was repaired but now carries a measurable stigma in the resale market.

- Use expert review early if the vehicle is custom, collector-grade, high-trim, low-mileage, or hard to comp.

The insurance adjuster works for the carrier. Your independent appraiser works from the market evidence tied to your specific vehicle.

Why a Certified Independent Appraiser Is Your Best Advocate

A good appraisal doesn't win because it sounds persuasive. It wins because it's built on standards, documentation, and policy rights that the carrier has to take seriously.

That's where many claimants get stuck. They argue with the insurer in emails, send screenshots from listings, and hope the adjuster changes course. Sometimes that helps. Often it doesn't. A formal dispute needs more structure than that.

The Appraisal Clause matters

Policyholders often don't read the valuation dispute language in their auto policy until they're already frustrated. That's where the Appraisal Clause usually enters the conversation.

When available under the policy, it gives the vehicle owner a structured way to challenge the amount of loss. In plain English, it moves the dispute away from “the insurer says so” and toward a process where independent valuation professionals do the work. That matters because software doesn't settle claims. People do.

If you're comparing options, an independent car appraiser can be part of that process by preparing the evidence-backed valuation and supporting the dispute path tied to the policy.

Standards separate real work from opinion

In Washington, certified auto appraisers must follow USPAP, the Uniform Standards of Professional Appraisers Practice. That requirement means the valuation has to be independent, evidence-based, and built on hard market data. It also means the resulting reports are accepted by courts and insurance carriers because they're based on real market conditions rather than insurer-biased software, as described in this Washington auto appraiser standards overview.

That's the difference between saying, “I think my car is worth more,” and presenting a report that documents why.

What a standards-based report usually includes

- Vehicle identification with trim, options, mileage, and condition details

- Comparable market research selected for relevance, not convenience

- Adjustment logic that explains why one vehicle is not equal to another

- Supporting documentation packaged in a format that can survive scrutiny

Practical rule: If the valuation can't explain its comps and adjustments clearly, it's not strong enough for a serious dispute.

Washington changed the umpire rules

There's another practical point many drivers haven't heard yet. In Washington State, auto appraisers involved in dispute resolution must register as umpires under a new rule effective January 31, 2026, which means only registered professionals can serve as neutral arbiters in disputed claims, according to this Washington umpire registration notice.

For claimants, that matters because credentials are no longer just marketing language. They affect whether the professional can fully participate in the dispute process when appraisers can't agree and an umpire becomes necessary.

The Appraisal Process From Start to Settlement

Most drivers feel better once the process stops being mysterious. A claim dispute becomes manageable when you know what happens first, what you need to send, and what the appraiser handles for you.

Start with the visual overview below.

Step one and step two

The first step is a claim review. The appraiser needs to know whether this is a total loss dispute, a diminished value issue, or a claim that may head toward formal appraisal under the policy. You don't need a polished summary. You just need the facts.

Then comes document collection. Most clients can move this part quickly if they gather everything in one place.

Documents that usually help

- Insurance valuation report from the carrier

- Policy language if you have it, especially the appraisal provision

- Photos of the vehicle before and after the loss if available

- Repair estimate or total loss notice

- VIN, mileage, and option details

- Receipts or records for upgrades, recent work, or major maintenance

Step three and step four

Once the file is complete, the appraiser inspects the vehicle when needed, reviews the condition, and researches comparable market data. For a total loss, that means building a supportable pre-loss value. For diminished value, that means measuring the market penalty tied to the accident history.

After that, the appraiser issues the report. In a solid file, the report isn't just a number on a page. It's the reasoning, support, and documentation behind that number.

Here's a brief explainer that helps many drivers understand how the process unfolds in practice.

What happens near settlement

The final phase is negotiation or formal appraisal activity under the policy. Sometimes the carrier reviews the report and adjusts the offer. Sometimes both sides appoint appraisers and move deeper into the clause process. If disagreement remains, the umpire issue can become important, which is why Washington's registration rule now matters in real claim handling.

A practical workflow usually looks like this:

- You send the claim file and explain where the insurer's number feels wrong.

- The appraiser tests the insurer's valuation against actual market support.

- A formal report is produced and submitted or used in the appraisal process.

- The dispute narrows because unsupported assumptions are easier to spot.

- Settlement follows through revised negotiation or the policy mechanism.

The fastest claims aren't always the fairest. The useful question is whether the process is moving toward a supportable value.

Turnaround can matter when storage fees, rental issues, or replacement vehicle pressure are building. That's why organized documents and quick response from the owner make a noticeable difference.

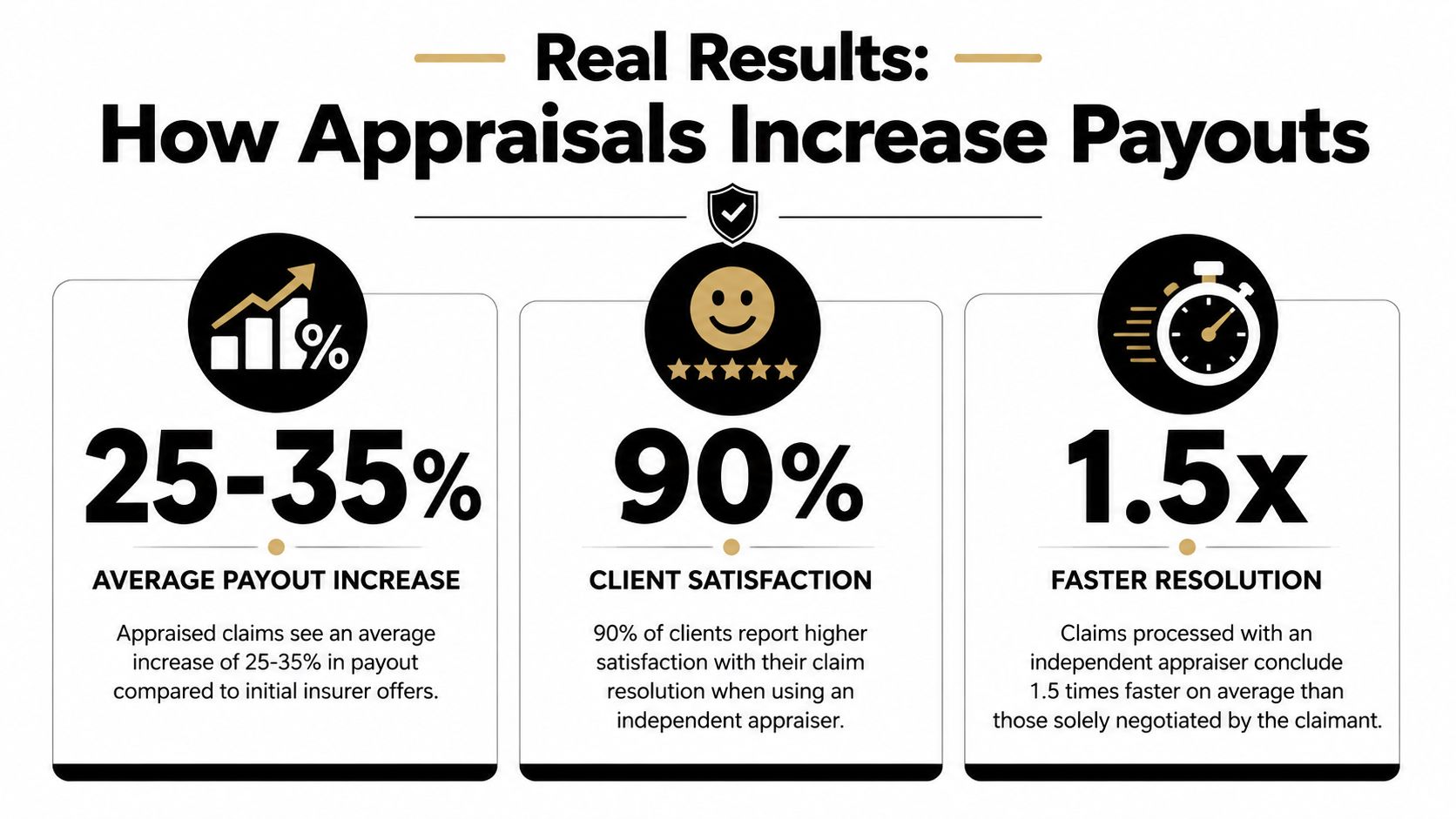

Real Results How Appraisals Increase Payouts

Theory only goes so far. A common inquiry arises: Does an independent appraisal change the outcome?

In documented Vancouver-area cases, the answer is yes. One reported example shows a settlement increase of 180%, moving from an initial insurance offer of $1,970.91 to a final adjusted value of $3,529.09 after professional appraisal and negotiation intervention, according to this Vancouver auto appraisal case example.

Why that gap happens

Insurance valuations often start from software-driven assumptions. If the software selects weak comparables, misses equipment, mishandles condition, or ignores local realities, the offer comes in low. The owner sees one number. The appraiser sees the build choices behind that number.

That's why the correction can be dramatic. The appraiser is not “adding value” out of thin air. The appraiser is documenting value the insurer's method failed to capture.

Reading the case like a practitioner

This kind of result usually tells you a few things were going wrong in the initial valuation:

| Likely issue | What it does to the settlement |

|---|---|

| Poor comp selection | Pulls the baseline value down |

| Weak option matching | Leaves equipment value out |

| Aggressive condition treatment | Reduces the insurer's number further |

| Limited negotiation support | Makes it easier for the first offer to stick |

When clients ask whether this work is worth paying for, this is the practical answer. A well-supported appraisal can alter the dynamic in the file because it replaces frustration with evidence.

Why Vancouver has strong demand for this work

That local demand shows up in the profession itself. In Vancouver, WA, the median annual salary for an auto appraiser is $78,390, which is 9% above the national average, according to Indeed's Vancouver auto appraiser salary page. That doesn't prove every appraiser is effective, but it does tell you the local market values this specialty.

And it should. A capable Vancouver WA Appraiser doesn't just inspect a car. They test a claim valuation under pressure, in a market where low offers are common and mistakes are expensive.

Understanding Appraisal Costs and Your Return on Investment

People usually ask about cost after they start to believe the insurer may be wrong. That's the right order. First decide whether there's a valuation problem. Then decide whether hiring help makes financial sense.

In this field, fees vary by assignment type and complexity. The Vancouver market information provided for auto appraisal services notes that flat-rate pricing for total loss appraisals typically ranges around $550 for standard vehicles, and that specialized services may also be billed hourly in some cases, as outlined in this auto appraisal pricing discussion.

Cost should be compared to the claim gap

If the insurer's valuation is only slightly off, paying for a formal appraisal may not be the smart move. If the file shows a substantial gap, the fee starts to look like an investment instead of an expense.

Use the logic from the earlier case example. When the settlement difference is large enough, the appraisal cost can be small compared with what's left on the table. That's especially true for vehicles with uncommon trims, collector interest, aftermarket upgrades, unusually clean condition, or scarce local comps.

Don't ask whether an appraisal costs money. Ask whether accepting the carrier's number costs more.

Why pricing stays firm in this niche

This is specialized work, and the local market reflects that. Vancouver auto appraisers show a median annual salary of $78,390, which sits 9% above the national average in the cited employment data. That points to sustained demand for professionals who can handle total loss and diminished value disputes with credible market support.

A careful appraisal is a business decision. Sometimes the right answer is yes. Sometimes it isn't. The key is to make that decision after reviewing the insurer's valuation, not before.

Common Questions and Your Next Steps

Can't I just negotiate this myself

Yes, sometimes. If the insurer made an obvious clerical mistake, direct negotiation may fix it.

But most disputed files aren't that simple. The carrier usually has a formatted valuation report, internal process, and adjusters trained to defend it. You may have instinct, screenshots, and frustration. That imbalance is why independent appraisals matter. They convert your position into a professional valuation file.

What if the insurance company ignores the appraisal

Carriers may resist it at first, but a proper appraisal report changes the conversation because it creates a documented dispute over the amount of loss. The next move depends on the policy language and the posture of the claim. In many cases, the issue is no longer whether you complained. It's whether the carrier can defend its number against evidence.

If the policy's appraisal mechanism applies, that process gives the dispute a structure that ordinary back-and-forth emails do not.

Is my car valuable enough for this process

Value alone isn't the test. Claim gap is the test.

A daily driver can justify an appraisal if the insurer's number is materially wrong. A high-end vehicle can fail to justify one if the offer is already fair. The stronger candidates usually involve one or more of these:

- Hard-to-find comparables because the car has rare options, low mileage, or unusual trim

- Accident stigma after repair where resale value dropped even though the car is back on the road

- Weak insurer support when the comps or adjustments don't make sense

- Pressure tactics where the carrier wants a fast release before meaningful review

What should you do next

Pull the valuation report. Read the comparable vehicles line by line. Check mileage, trim, condition, options, and whether the comps reflect your market.

Then decide whether the report looks merely imperfect or seriously flawed. If it's the second one, get an independent review before you sign anything.

A low insurance offer feels personal because it lands when you're already dealing with a wrecked car, lost time, and replacement pressure. But the solution is practical. Identify the claim type. Review the policy. Put real market evidence in the file. Use the dispute tools that apply.

If you're dealing with a low total loss offer or a repaired vehicle that lost resale value after an accident, Total Loss Northwest handles independent auto appraisals for Washington and Oregon claims, including Appraisal Clause disputes, total loss valuations, and diminished value reports. A no-obligation conversation can tell you whether the insurer's number is likely supportable or whether it's time to challenge it.