You've got a wrecked car, a claims adjuster on the phone, and an offer that feels wrong.

That instinct is usually worth listening to.

If your vehicle was damaged or totaled in Clark County, the number your insurer gave you is not some neutral truth pulled from the sky. It's a valuation built inside their process, using their software, with their payout goals in the background. If you want a fair result, you need your own number, your own evidence, and someone who knows how vehicle value works in the Vancouver and Portland market.

A Vancouver WA auto appraiser isn't just there to “estimate” value. A good appraiser is your counterweight. They take a one-sided insurance valuation and turn it into a documented, supportable market case.

Why Your Insurer's First Offer Is Not the Final Word

The first offer after an accident is often designed to end the conversation fast.

Most drivers assume the insurer already checked everything carefully. Year, trim, mileage, condition, options, local market, accident specifics. Sometimes they didn't. Sometimes they checked just enough to produce a number that sounds official. Those are not the same thing.

In Vancouver, this problem gets worse because the actual market doesn't stop at the city line. A credible appraisal often depends on broader metro comparables, including Portland, because this area works like a regional claims market, not a closed local bubble, as reflected in the BBB directory for Vancouver-area auto appraisers. If the insurer pulls weak comparables or ignores cross-border pricing and repair economics, the offer can miss the actual replacement market.

Why software misses the mark

Insurance valuation tools like neat, standard vehicles. They do better with common commuter cars than with vehicles that have unusual trim, exceptional condition, rare options, older restorations, or strong local demand.

That's why a one-page valuation sheet shouldn't intimidate you. It may look polished, but polished isn't the same as accurate.

Practical rule: If the offer won't buy a comparable replacement vehicle in the Vancouver-Portland market, challenge it.

A lot of drivers also confuse actual cash value with whatever number the insurer put on paper. They're not automatically the same. If you want a plain-English breakdown of how insurers frame that concept, read this guide to auto insurance actual cash value.

What an independent appraiser actually does

A real appraiser doesn't just say, “Your car is worth more.” They build the case.

They inspect the vehicle or review its documented condition. They look at VIN-specific equipment, packages, mileage, prior condition, and actual comparables that make sense for this market. Then they explain the adjustment path from those comparables to a final opinion of value.

That matters because insurance companies negotiate differently when they're facing a supported report instead of an angry phone call.

If you're in Vancouver and you think the offer is low, stop arguing from frustration. Start arguing from evidence.

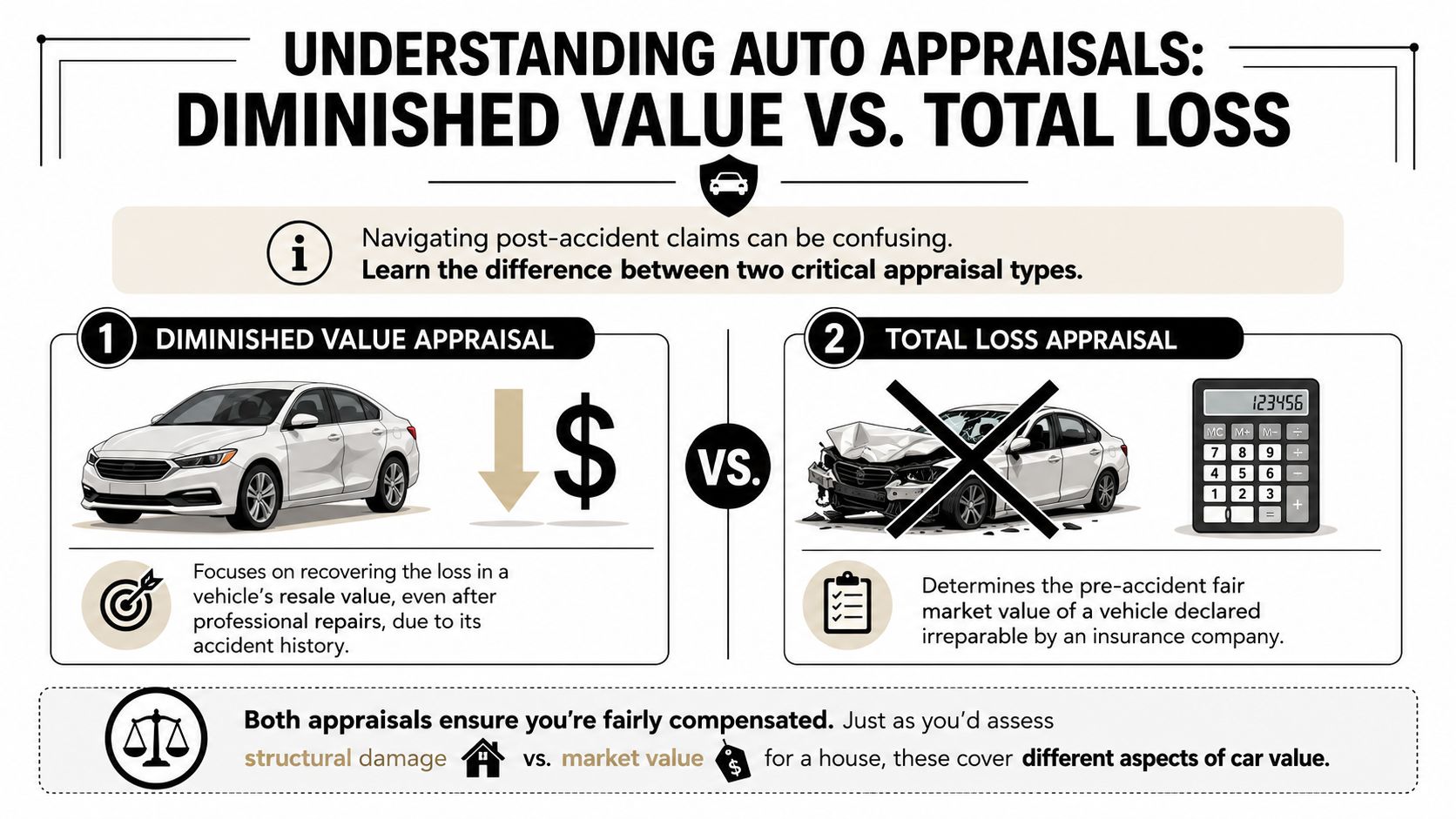

Diminished Value vs Total Loss Appraisals

Most drivers use the wrong term after a crash. That causes delays, confusion, and bad advice.

Here's the simple version. If your car was repaired but is now worth less because it has an accident history, that's a diminished value issue. If the insurer says the vehicle is a wipeout and wants to pay you for what it was worth before the crash, that's a total loss issue.

It's similar to real estate. A house that suffered damage, got repaired, and now scares off buyers has lost market appeal. That's diminished value. A house that burned beyond practical repair needs a pre-loss market value. That's total loss.

Side-by-side comparison

| Claim type | What's being measured | When you use it | What the dispute is about |

|---|---|---|---|

| Diminished value | Loss in resale value after proper repairs | The car is repaired or repairable | How much less buyers will pay because of accident history |

| Total loss | Fair market value before the accident | The insurer says repairs don't make economic sense | What it would cost to replace the vehicle with a comparable one |

When each one makes sense

A diminished value claim fits when your car is back on the road, but the market now treats it differently. Buyers often pay less for a vehicle with a collision record, even if the repair work was done well. That loss belongs in the claim conversation.

A total loss appraisal fits when the vehicle won't be repaired, or the insurer has already declared it a total loss and made an offer you don't trust. In that situation, the argument is about pre-accident market value, not repair quality.

A repaired vehicle can still lose value. A totaled vehicle raises a different question entirely. What was it worth right before impact?

If you're sorting through the legal and practical aftermath of a total loss, especially questions beyond the appraisal itself, this article on personal injury advice on totaled cars is a useful companion read.

Don't let the insurer define the category for you

Insurers like clear boxes. Real vehicles don't always fit neatly.

A custom truck, collector car, luxury vehicle, or unusually clean older car may need more than a basic software pass. Public-facing industry content often talks around this, but the important issue is whether a neutral appraisal does a better job than the insurer's initial system-based valuation, particularly for specialty or hard-to-comp vehicles, as discussed in this background on appraisal work involving total loss, diminished value, and specialty vehicles.

If you're dealing with post-repair stigma, learn more about automobile diminished value. If you're dealing with a total, stay focused on replacement-market proof. Mixing the two is one of the fastest ways to weaken your claim.

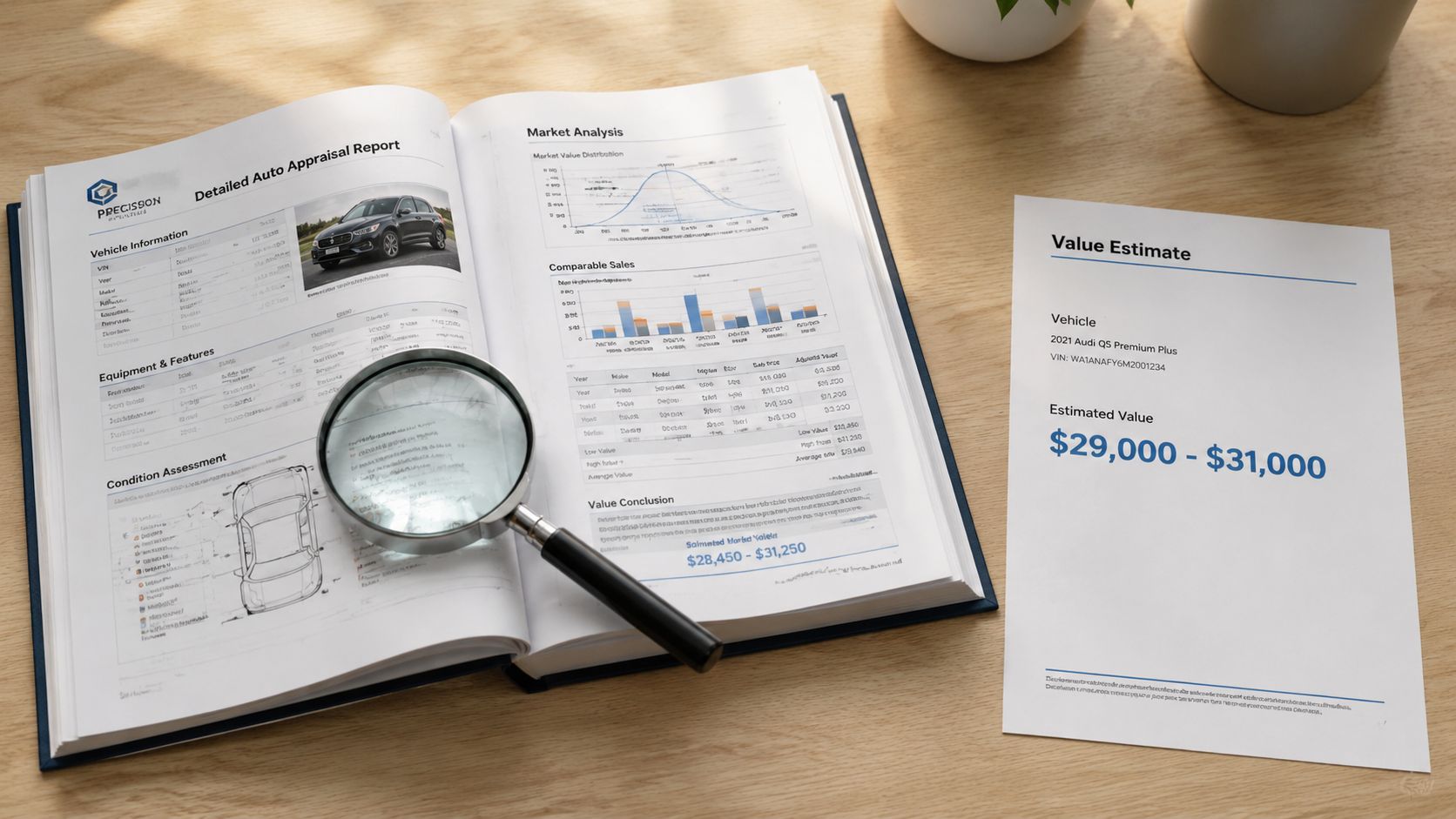

The Anatomy of a Defensible Auto Appraisal

A strong appraisal report doesn't win because it has a higher number. It wins because it shows its work.

That's the difference between a real valuation and a paper summary generated to close a file. If you're hiring a Vancouver WA auto appraiser, you're not paying for a guess. You're paying for a document that can survive scrutiny.

What Washington requires

In Washington, an appraiser handling this kind of dispute must have at least five years of experience as an auto-claims appraiser or collision-repair specialist under WAC 284-20-310. That requirement matters. It separates a qualified valuation specialist from somebody offering casual opinions.

Experience alone isn't enough, though. A credible report also needs to rely on VIN-specific market data and local comparables, not just a generic guide value. That's what makes the conclusion defensible.

What should be in the report

A proper appraisal should include more than a final figure. Look for these building blocks:

- Vehicle identity and configuration: VIN, trim, engine, drivetrain, packages, factory options, and equipment.

- Condition evidence: Pre-loss or post-repair condition notes, photos, and any proof of unusual cleanliness, upgrades, or defects.

- Comparable selection: Vehicles that resemble yours in configuration and market relevance.

- Adjustments: Clear reasoning for mileage, condition, options, and local market differences.

- Conclusion you can follow: A final value that connects logically to the data above it.

Kendall Hyundai in Vancouver describes trade valuation as a process that combines year, mileage, condition, features, options, equipment, packages, history, and real-time market data, with guidebooks used as comparison inputs, not as the whole answer, in its vehicle trade valuation overview. That's the right mindset for insurance disputes too.

If an appraisal can't explain how it moved from raw comparables to the final number, it's weak.

Red flags that should concern you

Some reports look professional but don't hold up. Be cautious if you see:

- Guidebook dependence: KBB or another guide standing in for actual market analysis.

- Bad comps: Listings from the wrong region, wrong trim, or wrong condition class.

- No adjustment trail: A value with no explanation for how the appraiser got there.

- Thin inspection notes: Little to no documentation of the vehicle's actual features and condition.

If you own a collector or agreed-value type vehicle, it also helps to understand how specialty coverage is supposed to work before a loss happens. This piece on agreed value classic car insurance gives useful context on that side of the issue.

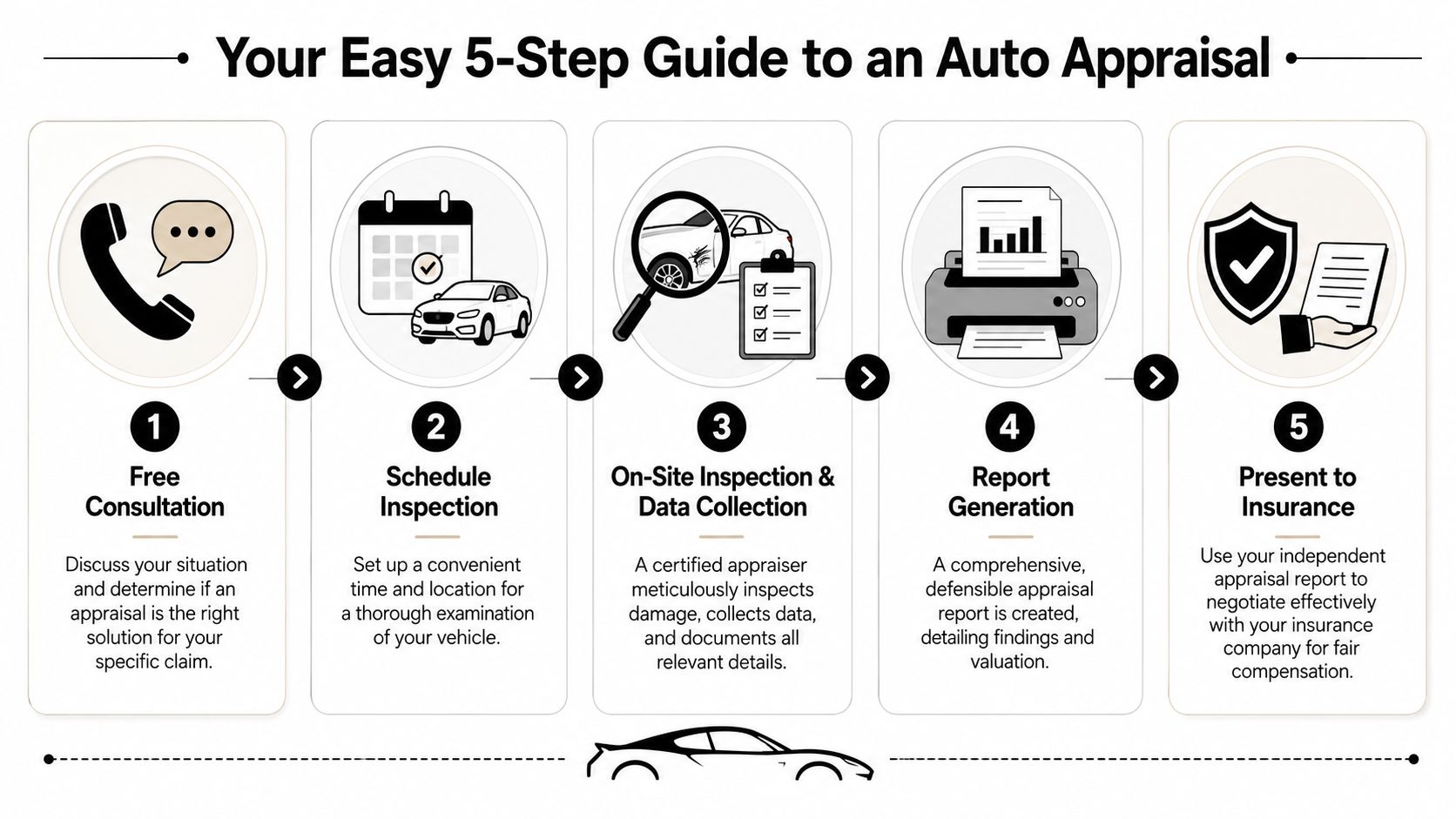

Your Step-by-Step Guide to Getting an Appraisal

The adjuster calls, gives you a number, and acts like the case is basically over. It isn't. If the value is wrong, the next move is to build a clean record that forces the insurer to deal with evidence instead of its own software.

That is the job here. You are not asking for a favor. You are putting an independent value on the table so the insurance company cannot control both sides of the argument.

Step one through three

Get the insurer's file and your own records together

Pull the valuation report, repair estimate or total loss letter, photos, registration, mileage, service records, and receipts for options, recent work, or upgrades. Start with documents. A weak insurance valuation often falls apart once the actual vehicle history is in front of someone who knows what to look for.Identify the exact dispute

Is the fight about what the car was worth before the loss, or how much value it lost after repairs? Those are different claims with different evidence. If you mislabel the problem, you waste time and give the adjuster room to stall.Hire an independent appraiser early

Do this before you spend a week arguing by phone. A good appraiser reviews the carrier's report, checks the vehicle details, and tests whether the comparables and adjustments hold up. If you need a local starting point, this guide to finding an independent auto appraiser near me helps you start the search.

Step four and five

Before you submit anything, it helps to hear the process explained in plain English.

Read the finished report before it goes out

Do not stop at the final number. Check that the VIN, trim, mileage, options, condition, and loss type are correct. Make sure the report explains why each comparable was used and why each adjustment was made. If a report cannot survive basic questions, it will not help you much in a dispute.Submit the report and press for the next formal step if the insurer refuses to correct the value

Some carriers change course once they see a well-supported appraisal. Others keep defending the original number because that is how their process is built. If that happens, use the appraisal clause or other dispute procedure available under the policy and claim facts. That is where an independent appraiser stops being just a valuator and becomes your counterweight to the insurer's built-in bias.

Bring records, photos, and receipts. Those move a claim faster than frustration ever will.

If you are dealing with diminished value, total loss, or an appraisal clause dispute in Washington or Oregon, Total Loss Northwest is one company that handles those claim types.

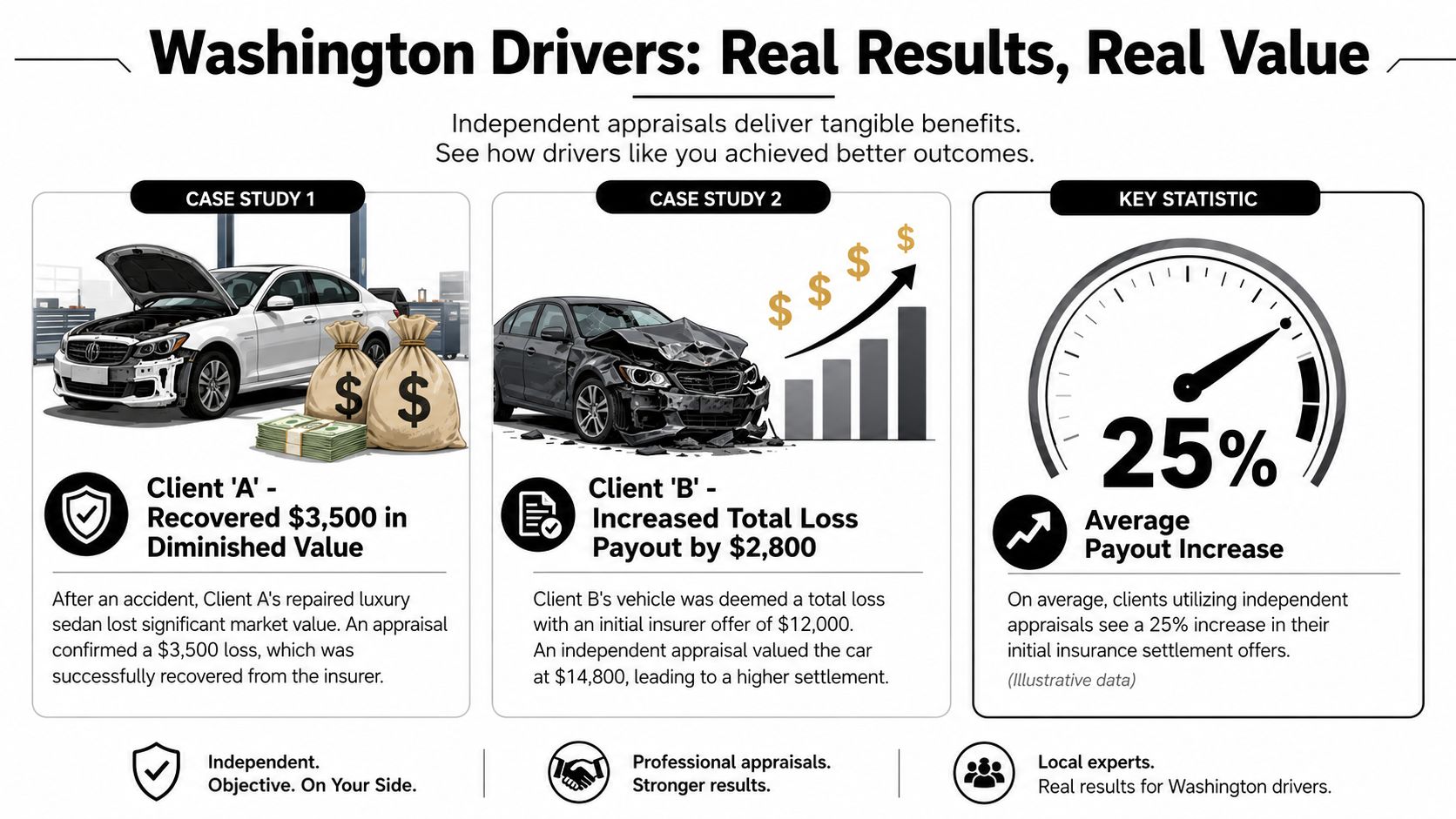

Real Results for Washington Drivers

You get the insurer's offer, look at the number, and know it is light. The car was clean. The mileage was good. The options mattered. Their valuation still treats it like a forgettable base model. That is the moment an independent appraiser starts protecting your money, not just naming a price.

One documented example that matters

As noted earlier, one Vancouver-area case involved a 1981 Chevrolet C10 Pickup. After an independent appraisal challenged the insurer's number, the settlement increased by $7,028.67, a 72% jump.

That result gets to the point fast. The insurer's first number can be badly wrong, especially when the vehicle does not fit neatly into their valuation system. A strong appraisal gives you evidence the adjuster has to answer, not just complaints they can ignore.

Why uncommon vehicles see the biggest gaps

Insurer valuation tools are built for speed and volume. They are not built to protect owners of unusual vehicles.

That matters if you drive something older, cleaner than average, modified, collectible, or loaded with options. Generic databases miss condition. They miss rarity. They miss equipment that buyers in the actual market will pay for. The insurance company benefits when those details disappear.

Vehicles that often need a harder review include:

- Older vehicles in unusually strong condition: insurer systems often compress condition and treat clean examples like average ones.

- Classics and collector vehicles: weak comparable choices can drag the value down quickly.

- Modified or option-heavy vehicles: added equipment and uncommon trims are easy for adjusters to undervalue or leave out.

- Vehicles with strong regional demand: local buyers may value the vehicle more than a broad database suggests.

The less your vehicle looks like an average used car, the less you should trust an average valuation system.

Not every appraisal produces a dramatic increase. Plenty do produce a fairer number, and that is the standard that matters. If the insurer's offer does not match the fair market for your vehicle, get an independent appraisal and make them defend their math.

Common Questions About Auto Appraisals in Vancouver

What does an appraisal usually cost

The only specific pricing I can cite from the Vancouver area is this: one appraisal-clause service lists fees starting at $295 for a normal auto, while specialty vehicles and property-damage claims are billed at $150 per hour. Costs vary by vehicle type, claim type, and how much work the dispute requires.

My advice is simple. Don't shop by price alone. Shop by methodology.

Can I use an appraiser if the crash wasn't my fault

Yes, that's often when an appraisal makes the most sense, especially in diminished value and total loss disputes. The bigger issue isn't fault. It's whether the insurer's number reflects the actual market and the actual condition of your vehicle.

How long does the process take

There isn't one universal timeline. It depends on how fast you can gather records, whether the vehicle is available for inspection, and how stubborn the insurer decides to be. Some disputes move quickly once a strong report lands on the adjuster's desk. Others drag because the carrier wants to test your patience.

What if the insurance company still won't agree

Then the dispute may move into the formal appraisal process described in your policy. That usually means each side selects an appraiser. If they still can't agree, an umpire may be brought in according to the policy terms.

That's why the quality of your first report matters. Weak appraisals create more friction. Strong appraisals create an advantage.

What should I do before I accept anything

Do not sign off just because you're tired of the process. Review the valuation report, the comparable vehicles, the equipment list, and the condition adjustments. If the insurer missed obvious features, used bad comps, or ignored regional market reality, stop and get a second opinion before you release the claim.

Take Control of Your Vehicle's Value Today

Your adjuster calls, gives you a number, and talks like the decision is already made. It is not.

Insurance companies use valuation systems built to protect their payout, not your equity in the vehicle. If the offer feels low, treat that as a warning sign and get an independent appraisal before you accept, release, or sign anything. That is how you level the playing field.

A qualified appraiser does more than put a price on your car. They review the insurer's file, challenge bad comparable vehicles, correct missing options, and document the current local market. That work gives you a defensible number you can use in a serious dispute, not just a complaint.

If your claim involves a total loss, diminished value, a collector car, a truck with upgrades, or an older vehicle in unusually good condition, get a second opinion. Those are the cases where carrier formulas miss value and drivers leave money on the table.

If you want a clear read on whether your insurance valuation is fair, contact Total Loss Northwest. They handle independent diminished value and total loss appraisals in Washington and Oregon and can explain your options before you accept a settlement.