You open the claim email, read the number, and immediately know it's wrong.

Your truck was clean before the crash. The mileage was reasonable. The trim level mattered. The options mattered. The local market mattered. None of that seems to have made it into the insurer's valuation. Instead, you get a settlement that feels assembled by software, approved by someone who never saw your vehicle, and designed to see if you'll give up quickly.

That's where most drivers make the same mistake. They argue too long inside the insurance company's process. They send listings, point out bad comps, explain the condition, and wait for a “re-review.” Sometimes that works. Often it doesn't.

If you're in Washington, your policy may already contain the tool that changes the balance of power. It's the appraisal clause. Used correctly, it forces a value dispute out of the insurer's internal loop and into a formal process built around independent appraisers.

The Lowball Offer and Your Secret Weapon

A Washington driver gets rear-ended, the body shop estimate climbs, and then the carrier says the vehicle is a total loss. A few days later, the offer arrives. It's based on “comparable vehicles” that don't match the trim, don't match the condition, and sometimes don't even reflect the right market. The driver points this out. The adjuster says they'll “submit it for review.” Then the revised offer barely moves.

I've seen that pattern more times than I can count.

The same thing happens with diminished value. The vehicle is repaired, but now it carries an accident history. The owner knows that matters when it's time to sell or trade. The insurer acts like it doesn't. That gap between what the car is worth in real life and what the carrier wants to pay is where frustration turns into an advantage, if you know your rights.

The problem isn't just the number

The problem is the setup. You're trying to challenge an insurer valuation while the insurer controls the process, the software, the review path, and the pace. That's not a fair fight.

The Washington appraisal clause is your built-in answer. It's not a favor the insurance company grants. It's typically a contractual right in the policy. If the disagreement is about amount of loss, the clause can move the dispute into a structured appraisal process.

You don't have to win an argument with the adjuster. You need to trigger the process that stops the adjuster from being the final gatekeeper on value.

If you're also trying to understand how diminished value is treated in other states, this overview of diminished value information for Colorado drivers is useful because it shows how much state-specific rules and strategy matter. Washington drivers should approach their own claims with the same mindset. Don't assume the insurer's first answer is the only answer.

Your ace in the hole

Most policyholders never invoke the clause because they either don't know it exists or they think it sounds too legal, too expensive, or too aggressive. That hesitation costs money.

If the insurer is lowballing your total loss value or brushing off diminished value, the appraisal clause is often the cleanest way to stop debating and start forcing a fair valuation process.

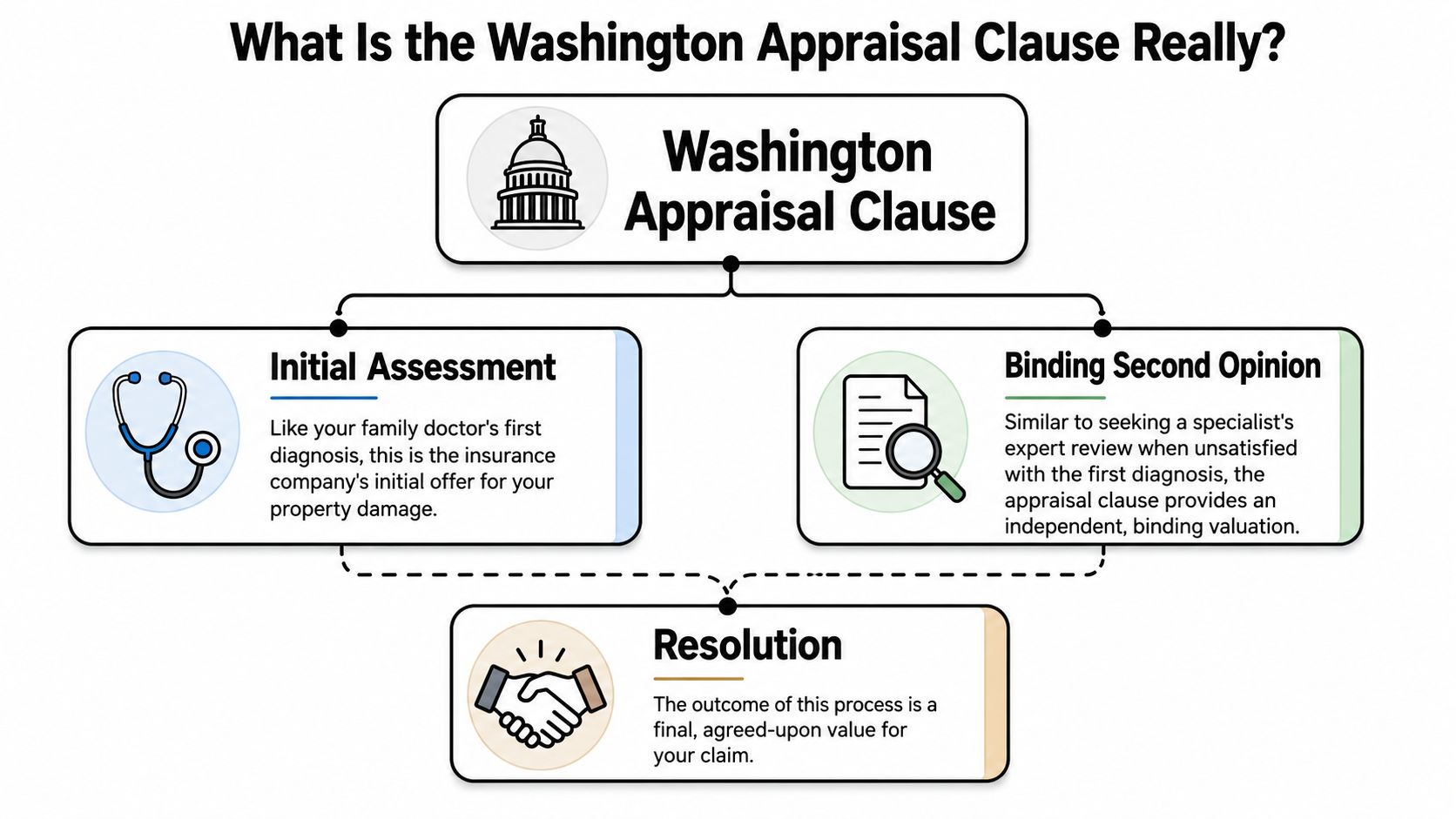

What Is the Washington Appraisal Clause Really

You get the insurer's valuation report, and the number is thousands short of what your vehicle would sell for in Washington. At that point, you need more than another email to the adjuster. You need the clause in your policy that forces a real value dispute into a defined process.

The Washington Appraisal Clause is a contract tool for settling disagreements over the amount of loss. In plain terms, it gives both sides a way to put the valuation in the hands of independent professionals instead of leaving it inside the carrier's internal review loop.

Here is how it usually works. You select your appraiser. The insurance company selects its appraiser. If those two appraisers reach agreement, that number sets the value. If they do not, they submit the dispute to an umpire, and the final figure is decided from there.

What the clause actually decides

Drivers often waste time using the wrong tool for the wrong dispute.

Appraisal is built for valuation fights. That includes disputes over actual cash value, total loss value, repair-related value questions, and in many claims, diminished value if the policy language and facts support it. The central question is simple: what was the loss worth?

Coverage disputes are different. If the carrier says the policy does not apply at all, appraisal usually does not resolve that issue. The same goes for legal arguments about fault, exclusions, or whether the claim should have been denied outright. Those are separate fights.

That line matters in practice. If your position is, “My car was worth more than your report shows,” appraisal is often the right lane. If your position is, “You should have covered this loss in the first place,” you are dealing with a coverage issue.

Why insurers do not like appraisal

Insurance companies prefer valuation methods they can control. Their systems are fast, repeatable, and built around their own vendors, assumptions, and review standards. Appraisal takes the valuation out of that controlled setting and puts it in front of people who have to justify the number with real market support.

That changes the pressure. An independent appraiser has to account for trim, options, mileage, condition, local market reality, prior damage, and the quality of the comparable vehicles used in the report. A weak carrier valuation gets exposed quickly when someone experienced pulls it apart line by line.

The clause has teeth because it does not ask for courtesy. It requires participation.

If you want a practical explanation of how that contract right works in auto claims, read this guide on the auto insurance appraisal clause process.

Practical rule: If the dispute is about value, stop spending weeks trying to persuade the adjuster to reverse their own number. Invoke the process that puts the valuation in independent hands.

Why this clause matters in Washington claims

Washington drivers give insurer paperwork too much weight. A written offer is still just the carrier's position. It is not the market, and it is not automatically fair because it came in a formal report.

The appraisal clause exists for the exact moment when the offer misses the pre-loss value of your vehicle or understates the financial hit you took. Used correctly, it turns a lopsided argument into a structured valuation process with rules, deadlines, and decision-makers outside the insurer's internal chain.

When to Stop Arguing and Invoke the Clause

The adjuster sends a polished report. The number is still wrong. You reply with better comps, point out the bad trim match, explain the mileage problem, and get another version of the same answer in different packaging.

That is the moment to change tactics.

In Washington claims, appraisal is not the first move. It is the right move after you have identified a real value dispute, made your objections clear in writing, and confirmed the carrier is defending a weak valuation instead of fixing it. If the insurer keeps "reviewing" without correcting obvious errors, stop treating the process like a debate you can win through persistence.

Signs you are done negotiating

Focus on the valuation report itself. That is where lowball claims show their hand.

The comparable vehicles do not match your vehicle

Wrong trim, wrong drivetrain, missing options, inflated condition adjustments, or listings pulled from markets that do not reflect your real selling area.Mileage and condition adjustments do not make sense

A lower-mileage vehicle should not be valued against tired, high-mileage comps without a credible adjustment. The same goes for prior condition. If the report glosses over it, the number is suspect.Diminished value is treated like a paperwork exercise

Buyers discount accident history. If the carrier acts like a repaired vehicle with a damage record sells the same as a clean-history vehicle, the valuation is detached from the real market.The insurer keeps delaying instead of answering

Repeated "we're reviewing it" responses usually mean the carrier has no good answer and hopes you get tired first.You are arguing about judgment, not a typo

If the dispute is over valuation methodology, comparable selection, condition, or market area, appraisal is usually the cleaner path.

One practical benchmark matters more than any canned timeline. If you have sent one organized rebuttal and the insurer still stands on a flawed report, you have enough information to act.

Do not wait for the carrier to be reasonable

Clients often ask me how long they should keep pushing the adjuster. My answer is simple. Stop after one serious rebuttal unless the carrier makes real corrections.

Insurance companies are built around process control. Appraisal takes value away from that internal loop and puts it in the hands of people who have to support a number with market evidence. If you want to understand what happens when the two appraisers cannot agree, read this guide on the insurance appraisal umpire process in Washington.

Industry standards for fair documentation and timely claim handling are discussed in this insurance claims processing guide. Use that as a frame, but do not confuse a documented process with a fair valuation. Carriers can follow procedure and still underpay the claim.

My recommendation

Use this rule.

Audit the insurer's report line by line.

Check trim, options, mileage, condition, prior damage, market area, and every comp used to support the number.Send one tight written rebuttal.

Identify the defects clearly. Attach better comps or photos if they strengthen your position.Measure the response, not the tone.

A polite email with bad analysis is still bad analysis. Look for corrected comps, revised adjustments, and a materially better number.Invoke appraisal if the defects remain.

That is where you stop asking the insurer to reconsider and start enforcing your rights under the policy.

Lowball offers do real damage because they pressure people to settle while they are stressed, busy, and unsure of the rules. Do not stay in that trap. Once the carrier shows you it will not voluntarily fix a bad value, invoke the clause and move the dispute where evidence matters.

The Appraisal Clause Process Step by Step

Once you decide to use the clause, the goal is simple. Be formal, be organized, and stop talking like you're asking permission.

A lot of drivers make appraisal harder than it needs to be because they stay casual. They call instead of writing. They rely on vague conversations. They accept delays that should've been challenged. Don't do that.

Step 1 formally demand appraisal

Read the appraisal language in your policy first. Then send a written demand.

Keep it short. You are not writing a novel. You are invoking a contractual right.

I dispute the insurer's valuation of my vehicle and hereby demand appraisal under the appraisal provision of my policy. Please confirm your designated appraiser and all next steps required under the policy.

Send it by email and keep a clean paper trail. If the insurer has a claim portal, upload it there too.

Step 2 choose your appraiser carefully

Outcomes are subject to swings.

Your appraiser should know total loss valuation, diminished value methodology, market-based comps, policy language, and the Washington claim environment. You want someone who can write a report that stands up under scrutiny, not somebody who just throws out a higher number.

If you want to understand the umpire side of the process before you get there, this overview on how an appraisal clause umpire works helps explain why neutral tie-breakers matter in disputed valuations.

Step 3 let the insurer appoint theirs

The carrier picks its own appraiser. That's expected. Don't panic because the insurer's appraiser is insurer-friendly. The process assumes each side chooses someone aligned with their position.

Your job is not to make the insurer play fair out of goodwill. Your job is to make sure your appraiser is thorough, credible, and ready for a contested file.

Step 4 the appraisers exchange evidence and negotiate

This is the heart of the process.

Both appraisers review the vehicle details, loss documents, condition, market evidence, valuation sources, and repair history if diminished value is involved. They try to reach agreement on the amount of loss.

That means the report quality matters. Good appraisers don't submit unsupported opinions. They build a case.

A broader insurance claims processing guide is helpful if you want context for how claims normally move through insurer systems. Appraisal matters because it interrupts that one-sided workflow and creates a structured valuation dispute process.

Step 5 select an umpire if the appraisers don't agree

If the two appraisers remain apart, they select an umpire. The umpire doesn't redo the whole claim from scratch. The umpire reviews the disputed valuation issues and helps resolve the deadlock.

This is why professionalism matters from the start. Sloppy submissions don't suddenly become persuasive because an umpire enters the picture.

Step 6 the decision becomes binding and payment follows

When two members of the appraisal panel agree, typically the two appraisers or one appraiser plus the umpire, that decision is binding as to the amount of loss. At that point, the insurer should issue payment based on the award, subject to policy terms.

Settlement process comparison

| Stage | Standard Insurance Process | Appraisal Clause Process |

|---|---|---|

| Initial valuation | Insurer values the claim internally | Each side retains an appraiser |

| Dispute handling | Adjuster review or supervisor review | Formal appraisal demand triggers contract process |

| Evidence review | Insurer decides what to accept | Independent appraisers analyze market evidence |

| Deadlock | Claim can stall in internal review | Umpire resolves unresolved valuation disputes |

| Outcome | Insurer may hold to its number | Binding amount of loss is determined through appraisal |

This walkthrough helps if you want to hear the process discussed in a more conversational format.

What clients get wrong most often

They wait too long

Delay gives the insurer time to control the narrative and wear you down.They talk too much by phone

Phone calls disappear. Written demands and written objections don't.They treat appraisal like a bluff

Don't threaten it unless you're prepared to carry it through.

Appraisal works best when you invoke it cleanly, document everything, and choose an appraiser who can defend the number with evidence.

How to Choose a Winning Independent Appraiser

Invoking appraisal is the strategic move. Choosing the right appraiser is the execution.

Plenty of people call themselves appraisers. That doesn't mean they know how to build a defensible total loss file, challenge bad insurer comps, or present a diminished value analysis that survives pushback. You need a specialist, not a generalist.

What to look for first

Start with competence that matches your claim.

Claim-specific experience

Total loss and diminished value are not the same assignment. Ask which kind of file they handle regularly.Washington familiarity

You want someone who understands Washington claim practice and can work inside that environment without getting lost in generic national advice.A report, not just a number

If all they promise is “I'll get you more,” keep looking. You need methodology, support, and documentation.

If you're vetting local options, this directory for finding an independent auto appraiser near me is a practical place to start comparing specialists.

Questions I'd ask before hiring anyone

Don't ask whether they're “good.” Everyone says yes. Ask sharper questions.

How do you select comparable vehicles?

Listen for trim accuracy, option matching, mileage adjustments, and local market awareness.How do you document pre-loss condition?

A serious appraiser wants service records, photos, prior listings, and repair history where relevant.What does your final report include?

It should include the basis for the valuation, not just a conclusion.How do you handle disagreement with the insurer's appraiser?

You want someone who can negotiate professionally and, if needed, present a file that an umpire can follow.

Warning signs

A weak appraiser usually reveals themselves quickly.

- They guarantee an outcome

No honest appraiser can promise a specific award. - They can't explain their method in plain English

If they hide behind jargon, that's a problem. - They seem unfamiliar with insurer valuation reports

If they can't dissect CCC-style or market-based insurer reports, they'll struggle in a contested appraisal.

The right appraiser doesn't just disagree with the insurer. They prove why the insurer's value is wrong.

That's the standard.

Common Pitfalls and Insurance Company Tactics

Appraisal is powerful, but it isn't foolproof. Drivers still make avoidable mistakes, and insurers still use pressure points to keep control.

The biggest misconception is that once you invoke the clause, everything turns fair and smooth. It doesn't. The process gets better, but only if you handle it carefully.

Mistakes drivers make

Cashing a check too casually

Before you deposit or endorse anything, understand what the payment represents and whether it could be argued as acceptance of the insurer's position.Using a friend instead of a specialist

A “car guy” is not the same thing as an appraisal professional who can support a disputed insurance valuation.Relying on phone conversations

If it isn't documented, it's fragile. Confirm important conversations by email.

Tactics insurers use

Some tactics are subtle. Some aren't.

Delay through endless review

They ask for one more document, one more internal review, one more callback. Delay is often a strategy, not an accident.Muddying a value dispute with other issues

When the number is hard to defend, some carriers try to blur the line between valuation and unrelated claim questions.Influencing process choices

Be careful if the insurer pushes hard on who should serve as umpire or tries to steer the process before your appraiser is in place.

How to respond without getting sidetracked

Use a disciplined approach.

| Problem | Smart response |

|---|---|

| Vague phone statement from adjuster | Ask for written confirmation |

| Repeated “review” with no fix | Set a deadline, then invoke appraisal |

| Pressure to move informally | Stick to policy language and written communication |

Keep your file clean. Save valuation reports, emails, photos, window stickers if available, maintenance records, and any evidence of upgrades or exceptional condition. Strong documentation makes weak insurer tactics less effective.

The insurer's process is designed to close claims. Your job is to make sure they don't close yours at the wrong number.

Washington Appraisal Clause FAQs

Who pays for the appraisers and the umpire

You generally pay for your appraiser, the insurer pays for theirs, and the cost of the umpire is usually split between both sides. Check your policy language to confirm the exact wording.

How long does the appraisal clause process take in Washington

It often takes 30 to 60 days from demand to decision, depending on how quickly the appraisers are appointed, how organized the claim file is, and whether an umpire is needed.

Is the umpire's decision final and binding

In practical terms, yes. The appraisal award is generally binding on the amount of loss when the required members of the panel agree. That's why the choice of appraiser matters so much. A weak file can carry all the way through to a binding result.

Can I invoke the clause if I was at fault for the accident

Yes, if you're making a first-party claim through your own collision coverage. Fault for the accident doesn't automatically eliminate your right to dispute the amount of loss under your own policy's appraisal provision.

Should I hire help or do this myself

You can invoke the clause yourself, but most drivers underestimate how technical the valuation fight becomes once the process starts. If the vehicle is high-value, customized, unusually clean, recently repaired, or subject to a diminished value dispute, professional help usually makes the process far more effective.

If your insurer lowballed your total loss or diminished value claim, don't sit in endless “review” status. Total Loss Northwest helps Washington drivers fight bad valuations with certified independent appraisals and appraisal clause support built for real-world insurance disputes.