The call usually goes the same way. The adjuster is polite, says your vehicle is a total loss, then gives you a number that makes no sense. You start checking listings for a replacement and realize the offer won't put you back where you were before the crash.

That's the moment most drivers in Washington make the wrong move. They assume the insurer's number is fixed, sign the paperwork, and move on frustrated. It isn't fixed. If the valuation is wrong, you can challenge it, and you should.

A low total loss offer is often a valuation problem, not a coverage problem. The insurer may have used weak comparables, ignored options, missed condition details, or leaned too heavily on software. Washington Total Loss Experts exist to correct that. Their job is simple: document the actual cash value of your vehicle with real market support and force the discussion back onto evidence.

Your Car Is Totaled Now What

You're probably staring at a settlement letter, an email from the adjuster, or a valuation report full of line items that don't reflect your car. Maybe the mileage is off. Maybe the comparables are stripped-down versions of your trim. Maybe they valued your upgraded truck like a basic fleet model.

That reaction you're having is valid. Vehicle owners often understand their car's value, having purchased vehicles in the past. When the insurer's number feels disconnected from the actual replacement market, it usually is.

What not to do first

Don't accept the first offer just because the adjuster sounds confident. Don't sign a release. Don't hand over title until you understand whether the valuation is accurate.

If you need a practical overview of the immediate basics, review what to do when your car is totaled. Then come back to the valuation issue, because that's where most of the money is won or lost.

If the insurer's offer doesn't buy a comparable replacement in your market, treat the valuation as disputed until proven otherwise.

What actually matters right now

Your next step isn't arguing emotionally with the adjuster. It's getting the valuation reviewed by someone who works from market evidence instead of insurer software. That changes the conversation.

A Washington total loss expert looks at the vehicle the way a buyer, dealer, or appraiser would. They ask the questions that matter. What was the pre-loss condition? What options did it have? What local comparables are equivalent? Was the insurer's report complete and defensible?

You don't need to become an insurance expert overnight. You need a clear process and a qualified advocate.

Who Are Total Loss Experts and What Do They Do

A total loss expert is an independent auto appraiser. Not the insurer's adjuster. Not the software vendor behind the insurer's report. An independent appraiser works for the vehicle owner and builds a valuation from actual market support.

That distinction matters. The insurer's adjuster is handling the claim for the carrier. An independent appraiser is there to test the carrier's number and challenge it if it's wrong.

Their real job

In a total loss claim, the appraiser's job is to determine the vehicle's Actual Cash Value, usually called ACV, before the accident. In plain language, that means what your vehicle was worth in the open market right before the loss.

That work usually includes:

- Reviewing the insurer's report to spot bad comparables, missing options, mileage errors, and unsupported deductions.

- Researching the local market for vehicles that match yours in trim, features, condition, and use.

- Documenting pre-loss value in a form that can stand up during negotiation or appraisal.

- Handling the dispute process when the carrier won't correct a low valuation voluntarily.

Why people hire them

The biggest benefit isn't just the report. It's your advantage.

Washington drivers often hit a wall when they try to dispute a value on their own. The adjuster repeats the software result. The owner sends screenshots from car-shopping sites. Nothing moves. A certified appraiser changes the tone because the dispute stops being opinion versus opinion.

In Washington, certified total loss appraisers at TotalLossNW offer 48 to 72 hour turnaround for market-supported reports, and the company describes itself as a family-owned independent appraisal business focused on replacing automated insurance estimates with real market data across the state, as noted on its Washington total loss appraisal page.

Which claims they help with

Often, the focus is only on totaled vehicles, but the same type of expert can also help with diminished value when a repaired vehicle is worth less after an accident history shows up.

Practical rule: If the insurer's valuation depends on a formula you can't inspect clearly, you need an appraiser who can show the evidence line by line.

Washington Total Loss Experts are most useful in three situations:

The offer is obviously low

You can't find a comparable replacement anywhere near the carrier's number.The vehicle is unusual

Collector, custom, modified, rare-trim, and high-value vehicles often get mishandled by generic valuation systems.You want a clean dispute process

Instead of arguing with the carrier yourself, you want a professional valuation that gives you a structured way to challenge it.

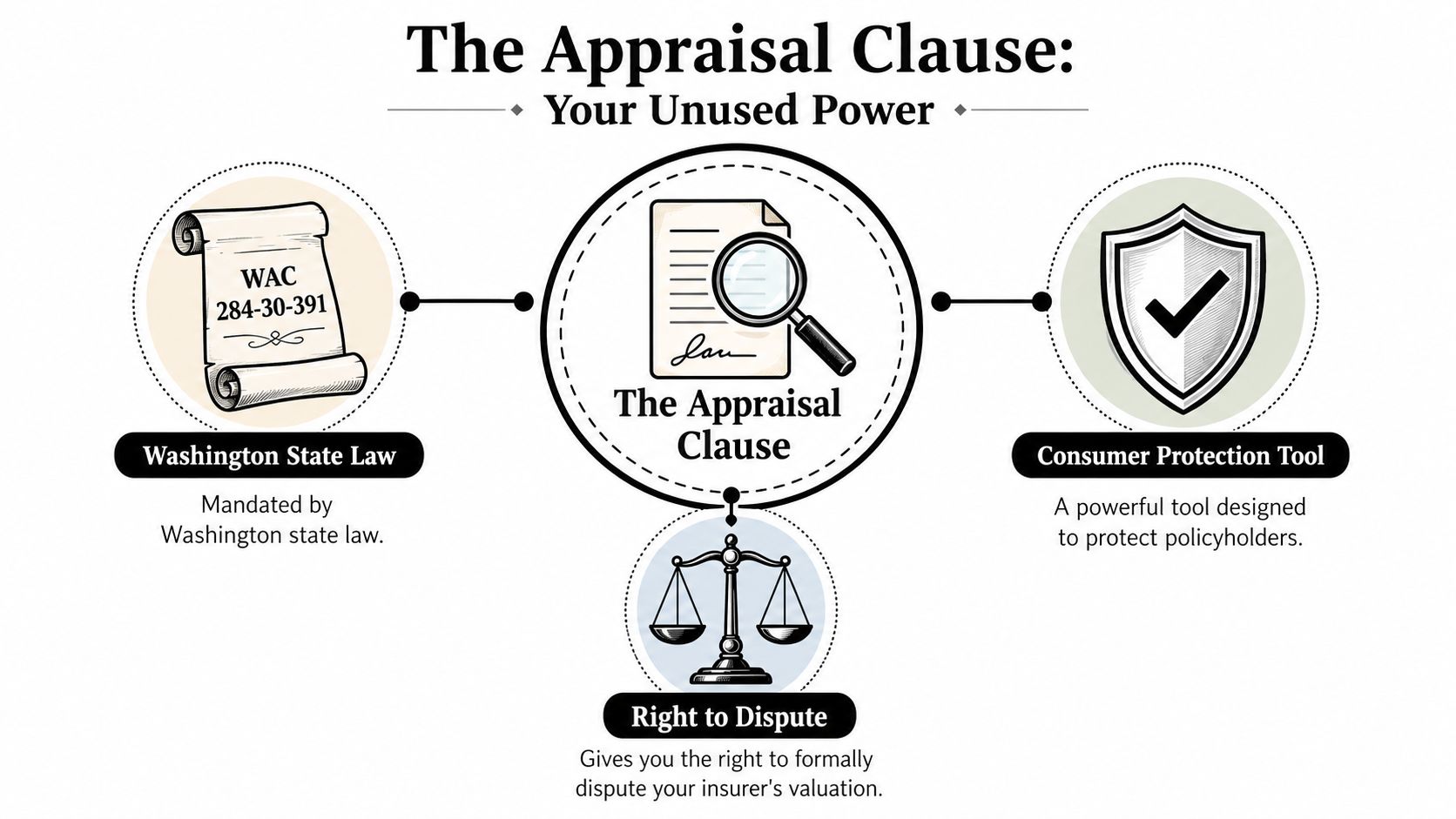

The Appraisal Clause Your Insurer Hopes You Ignore

Most policyholders don't realize they already have a built-in way to challenge a bad valuation. It's called the Appraisal Clause, and it's one of the most important protections in a Washington total loss case.

When you and the insurer disagree on ACV, Washington law allows the claimant to invoke the appraisal clause in the policy. Each side selects an independent appraiser. If those appraisers can't agree, an umpire can be brought in, and the insurer must pay the final award within 15 days under WAC 284-30-391.

Why this clause matters

Think of the appraisal clause as a forced reset. It takes the valuation fight out of the insurer's ordinary claims routine and moves it into a defined dispute process with independent valuation professionals.

That matters because many bad offers survive for one reason. The carrier controls the paper, the software, and the workflow. The appraisal clause interrupts that control.

If you want a practical explanation of how that process is used in real claims, read how the insurance appraisal clause works.

How the process usually unfolds

Once invoked, the process is more structured than most drivers expect.

You choose your appraiser

This should be someone who understands total loss valuation and can defend their report.The insurer chooses its appraiser

That appraiser reviews the claim from the carrier's side.The two appraisers compare evidence

They examine condition, equipment, mileage, comparables, and valuation method.If they still disagree, an umpire can decide

The umpire breaks the deadlock based on the evidence presented.

Here's a quick explainer that helps many clients understand the mechanics before they invoke it:

Why insurers prefer you never use it

The appraisal clause removes the comfort of an uncontested file. Once invoked, the insurer has to defend its valuation against someone who knows how vehicle markets work and can identify weak comps fast.

That's especially important for owners of custom and collector vehicles. Broad valuation systems often flatten those vehicles into generic categories. Appraisal doesn't.

A low offer feels final only until someone forces the insurer to prove how they got there.

Your Step-by-Step Plan After a Total Loss Declaration

When a vehicle is declared a total loss, speed matters. Not because you should rush into accepting the offer, but because you need to lock down the valuation record before the file hardens around the insurer's number.

Step 1. Pause the claim before you sign anything

Tell the adjuster you're reviewing the valuation. Keep it short and professional. You don't need to argue yet.

Do not sign a release. Do not send title just because you want the process over with. Once you accept and finalize the settlement, your negotiating power diminishes significantly.

Step 2. Request the full valuation report

You need the paperwork behind the number. In Washington, when an insurer provides a total loss valuation report, it must include the data from the initial vehicle inspection, the method used to determine ACV, and the comparable vehicles used for that ACV calculation. If the insurer relies on a computerized source, the report must also document that source and the data validation process under Washington Administrative Code 284-30-392.

That requirement is useful because it gives you something concrete to inspect. If the comparables are weak or the methodology is vague, you've found the problem.

Step 3. Gather your vehicle-specific evidence

Build the file the insurer should have built in the first place.

Bring together:

- Photos before the loss if you have them, especially showing condition, wheels, interior, or upgrades.

- Maintenance and repair records for major recent work that supported the car's market value.

- Option and package details such as trim level, factory packages, towing equipment, tech packages, or premium audio.

- Upgrade documentation for custom or collector vehicles, including receipts and build details where available.

Step 4. Hire an independent appraiser early

This is the move that changes the outcome. The appraiser reviews the insurer's report, identifies bad assumptions, and prepares a proper valuation.

Washington residents often hesitate here because they worry they'll spend money and still get nowhere. That concern is real. In Washington, appraisal fees generally aren't reimbursed by the insurer. That's why flat-fee structures matter. They turn an uncertain cost into a defined decision.

Step 5. Let the appraiser handle the dispute

Once the file is organized, your appraiser can challenge the valuation directly and, if needed, invoke appraisal. That takes the burden off you.

Instead of repeating yourself to an adjuster, you now have a professional dealing with comparables, methodology, and policy procedure. Your role becomes simple: respond quickly when documents are requested and don't undermine the process by accepting a side offer too early.

Step 6. Review the final settlement carefully

When the valuation is corrected, make sure the final paperwork matches the agreed number and any related claim terms. If you have a loan or lease, confirm how the payoff is being applied.

A better valuation doesn't just improve the check amount. It can reduce the odds that you'll still owe money on a vehicle you no longer have.

How Fair Market Value Is Really Calculated in Washington

Most low total loss offers come from one basic problem. The insurer says it calculated market value, but the report often reflects a software output rather than a real market analysis.

That difference is where many claims turn.

What the insurer often does

Insurers commonly rely on automated valuation tools. Those systems can be useful for volume processing, but they aren't neutral just because they look technical.

For modified and collector vehicles, automated systems like CCC ONE often undervalue the vehicle by 20 to 35 percent because they rely on non-equivalent comparisons, according to The Auto Mediator's discussion of total loss valuation problems. That's exactly why custom, rare, and enthusiast-owned vehicles get shortchanged.

What an independent appraiser does differently

A certified appraiser builds a transparent, supportable opinion of value. That means using actual market data, examining comparable vehicles critically, and adjusting for the things that affect price in market conditions.

If you want to see the basics of that process from the owner's side, review how fair market value is calculated.

| Valuation Factor | Insurer's Method (e.g., CCC ONE) | Independent Appraiser's Method (USPAP Compliant) |

|---|---|---|

| Comparable vehicles | May include non-equivalent vehicles | Filters for truly comparable vehicles |

| Vehicle condition | Often reduced to standard adjustment fields | Evaluates actual pre-loss condition with support |

| Options and trim | Can miss or flatten equipment differences | Verifies packages, features, and trim impact |

| Local market relevance | May pull broad or weak market matches | Focuses on defensible market data |

| Custom or collector value | Often undervalued by generic categories | Uses niche market data where appropriate |

| Transparency | Summary-style output | Detailed report with documented reasoning |

Why transparency wins disputes

A strong appraisal report doesn't just give a higher number. It shows how that number was reached. That's what makes it useful in negotiation and appraisal.

Software can generate a figure. A qualified appraiser can defend one.

For standard daily drivers, that may mean correcting trim, mileage, and condition. For collector or modified vehicles, it often means proving value from markets the insurer's software never measured properly in the first place.

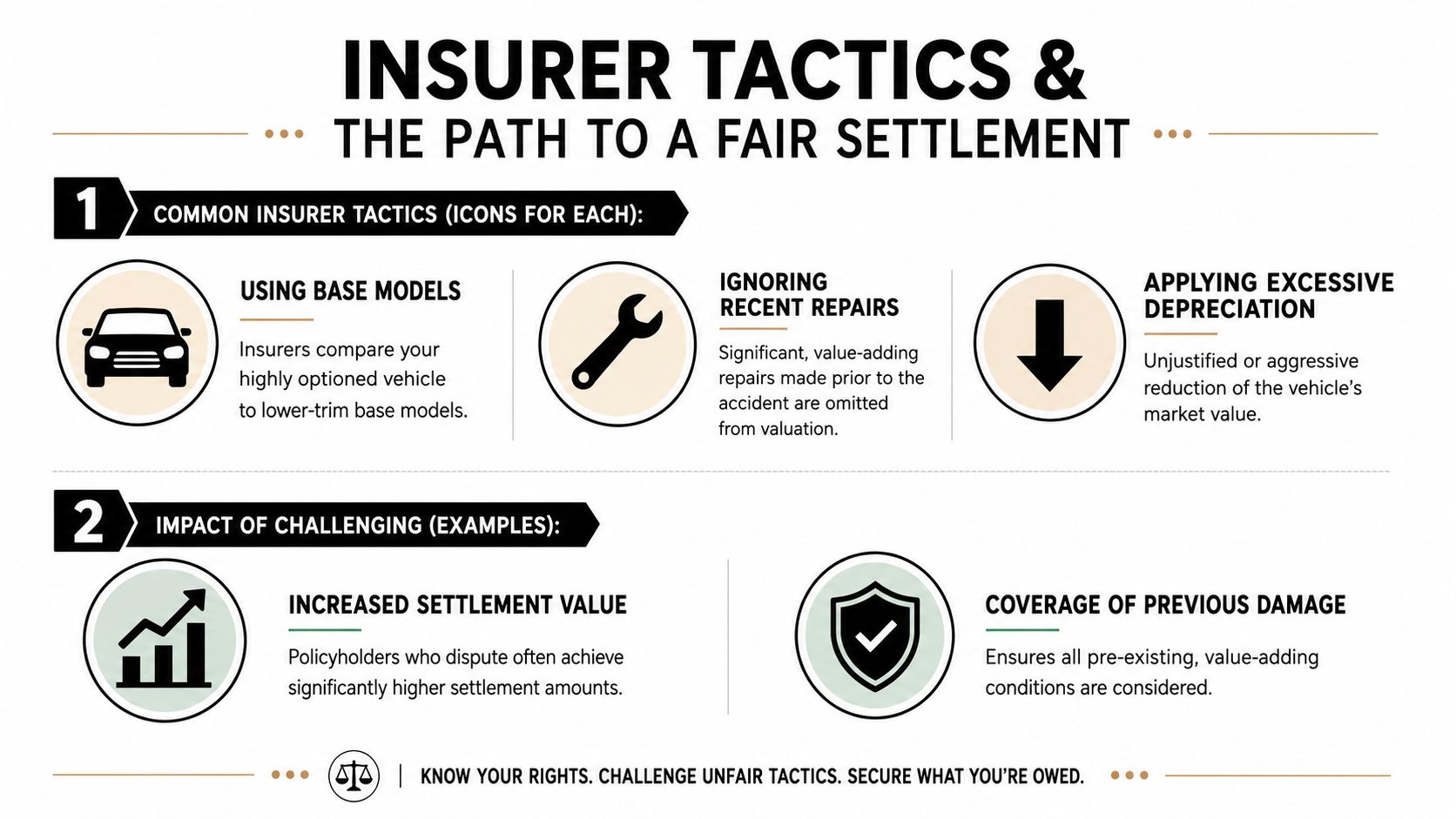

Common Insurer Tactics and Real Settlement Increases

Insurers don't usually say, “We're lowballing you.” They do it indirectly. They build a report that looks official, then count on you to assume it's accurate.

The tactics are familiar.

How low offers get built

Base-model comparisons

Your vehicle had premium trim, options, or packages, but the report leans on lower-spec vehicles.Missing recent work

Valuable maintenance or recent condition-improving repairs never make it into the valuation logic.Aggressive condition deductions

The report applies downward adjustments that don't match how your vehicle presented before the loss.Weak market matching

The comps are technically vehicles for sale, but not genuine equivalents.

What happens when drivers push back properly

The practical impact of hiring an expert becomes clear. Industry data from a licensed appraiser serving the Washington market shows that independent appraisers achieve an average settlement increase of $5,768.19, representing 44.78% of a vehicle's pre-accident market value, as reported on this Washington total loss appraisal resource.

That number matters because it reflects a practical result. Not a legal theory. Not a motivational slogan. Money recovered because someone challenged the insurer's valuation with evidence.

My recommendation

If the insurer's report has obvious errors, don't waste energy trying to negotiate from screenshots and frustration. Move directly to a professional valuation review.

The strongest disputes are boring. Clean documents. Good comparables. Clear adjustments. A report the other side has to answer. That's how you turn a weak first offer into a settlement that reflects your vehicle.

Washington Total Loss FAQs

Is it expensive to hire an appraiser in Washington

This is the main hesitation, and it's a fair one. Washington insurers generally do not reimburse appraisal fees, which means the cost concern lands on the vehicle owner. That's why flat-fee models matter so much in this state.

The practical answer is simple. If you're considering appraisal, look for a provider using a flat fee and, where offered, a guarantee structure that reduces your downside. The financial risk is the barrier most drivers focus on first, and firms built around fixed pricing are trying to remove exactly that barrier, as noted in this discussion of total loss appraisal fees and guarantees.

What if I still owe money on the car

Then valuation matters even more. The lienholder gets paid first from the settlement. If the carrier undervalues the car, you can end up still owing on a vehicle you no longer have.

A corrected settlement can reduce that gap or eliminate it. Don't treat this as a small negotiating point if you have a loan or lease.

Can an appraiser help if my car wasn't totaled but lost value after repairs

Yes. That's a diminished value issue, not a total loss issue. If your repaired car now carries an accident history and buyers would pay less for it, that lost market value may be claimable depending on the circumstances.

What should I ask before hiring someone

Ask four direct questions:

- Do you handle total loss appraisal disputes in Washington

- Do you work on a flat fee

- Will you review the insurer's valuation report

- Will you invoke the appraisal clause if the facts support it

One option in this space is Total Loss Northwest, which handles Washington total loss appraisal disputes and appraisal clause cases for vehicle owners. What matters most is that whoever you hire can document value properly and explain the process clearly.

What's the biggest mistake drivers make

Accepting the first number because they're tired.

That's what insurers count on. If the valuation is wrong, challenge it before you sign away your bargaining power.

If you're dealing with a total loss offer that doesn't reflect the market, contact Total Loss Northwest and get the valuation reviewed before you accept anything. A short review now can save you from locking in a bad settlement that you can't unwind later.