That dreaded phone call from the insurance adjuster… "I'm sorry, but your vehicle is a total loss."

For most people, those words kick off a wave of stress and uncertainty. What does that really mean? What happens next? You're not alone in feeling this way—it's a confusing process, and it's happening more often than ever before.

Your Car Is Totaled. Now What Happens Next?

So, what does it mean when your car is "totaled"? Simply put, the insurance company has run the numbers and decided it costs more to fix your car than what it was worth right before the accident. Instead of cutting a check to a body shop, they'll offer you a settlement for the vehicle's Actual Cash Value (ACV), minus your deductible. If you accept, you sign over the title, and they take the wrecked car off your hands.

Let's put this in a real-world context. Say you're driving your trusty SUV, worth about $18,000, when you get rear-ended. The damage looks bad, but you assume it's fixable. The adjuster, however, determines the repairs will cost $15,000. Because that repair bill is over 80% of the car's value, they declare it a total loss.

This isn't some rare event. In fact, nearly one in four cars involved in a crash today ends up being totaled. With the average car on U.S. roads now over 12 years old and even basic models packed with expensive sensors and safety tech, it doesn't take much for repair costs to spiral out of control. You can read more about the rising trends in total loss crashes to see just how common this has become.

The Initial Steps in a Total Loss Claim

The moment the insurer declares your car totaled, a new phase of your claim begins. It's no longer about repairs; it's about a financial settlement. This decision isn't based on whether you can still drive the car—it's a cold, hard calculation. If the cost of parts and labor crosses a certain percentage of the car's value (a threshold that varies by state and insurer), it's officially totaled.

Soon after, you'll get the first settlement offer. It is absolutely critical to remember that this is just that—an offer. Think of it as the opening bid in a negotiation. It's based on their valuation software and data, which may not accurately reflect the true, local market value of your specific vehicle with its unique history and condition.

Key Takeaway: An insurer’s first settlement offer is a starting point for negotiation, not a final, unchangeable number. Your immediate goal is to understand how they arrived at that figure and prepare to counter it with your own evidence.

What You Need to Do Immediately

The ball is now in your court. The decisions you make over the next few days can make a huge difference in your final payout. Here's a quick look at the immediate timeline and your first moves.

The first 24 to 72 hours after the "total loss" call are crucial. This is when you lay the groundwork for a successful negotiation. The table below breaks down what to expect and what to do.

Initial Total Loss Timeline At A Glance

| Phase | Key Action | What to Expect |

|---|---|---|

| Declaration (Day 1) | The adjuster informs you the vehicle is a total loss and provides an initial settlement offer. | The first offer will likely be verbal, followed by a written breakdown. It might feel low—don't panic. |

| Information Gathering (Day 1-3) | Immediately request a full copy of the insurer's valuation report (e.g., from CCC, Mitchell, or Audatex). | This report details the "comparable" vehicles they used to value your car. You need to review it for errors and inaccuracies. |

| Document Prep (Day 1-3) | Gather all your vehicle's records: maintenance history, receipts for new tires, upgrades, and recent repairs. | This documentation proves your vehicle's condition and value, giving you leverage to negotiate a higher settlement. |

| Hold Your Ground (Ongoing) | Do not sign any title release forms or other final paperwork. Do not accept the initial offer verbally. | The insurer may apply gentle pressure to close the claim quickly. Politely state you need time to review their offer. |

By taking these initial steps, you shift from being a passive victim to an active participant in the process. Your goal isn't to be difficult; it's to ensure you receive the fair market value you're owed for your totaled vehicle.

How Insurance Companies Calculate Your Car's Value

Once the insurance company has officially declared your vehicle a total loss, their next job is to figure out what it was worth right before the crash. This figure is called the Actual Cash Value (ACV), and it's the number that really matters—it's the basis for your settlement check.

But how do they land on that number? It's not as simple as looking up a price on Kelley Blue Book. Insurers rely on powerful, third-party valuation software to do the heavy lifting. Think of it as their secret weapon.

This software is essentially a "black box." The claims adjuster plugs in your vehicle's information—year, make, model, mileage—and out pops a detailed report with a specific dollar amount. The big players in this space are companies like CCC Intelligent Solutions, Mitchell, and Audatex. The problem is, the data these systems use can be full of holes, often leading to a lowball offer that doesn't come close to your car's true market value.

The Black Box and Its Flaws

The biggest issue with this "black box" approach is that you, the owner, have no idea what’s going on inside. The software scrapes data from all over to find so-called "comparable" vehicles to justify its price, but the quality of that data is often questionable at best.

Crucial Insight: The insurer's valuation report is just their side of the story, built on data that often conveniently supports a lower payout. It’s up to you to poke holes in their narrative and build a better one based on what’s actually happening in your local market.

Here are some of the most common shenanigans I see in these reports:

- Using Wholesale or Auction Prices: They might value your car based on what a dealer pays at a private auction, not the retail price you’d have to pay to replace it.

- Cherry-Picking "Comps": The report will often pull comparable vehicles from hundreds of miles away, in entirely different markets where cars sell for less.

- Outdated Listings: I've seen reports use "comps" that have been sitting on a dealer's lot for months. If a car hasn't sold, it's probably overpriced, not a good measure of market value.

- Unfair Condition Adjustments: An adjuster might knock your car's condition from "excellent" down to "average" for a few minor scuffs, shaving thousands off the value without real justification.

When an accident happens, insurers look at everything to determine a car's value, especially in complex cases like figuring out when frame damage equals total loss. This makes it absolutely critical to review every single line of their valuation report.

Key Factors in Your Vehicle's Valuation

A fair and accurate ACV needs to account for every little detail that made your car what it was. The insurer's software is supposed to do this, but key things often get missed or just plain wrong.

Here’s what a proper valuation has to cover:

- Base Vehicle Value: The starting point, making sure the year, make, and model are correct.

- Trim Level and Options: Is it the base LX model or the fully-loaded EX-L with the tech package? Missing a premium sound system, sunroof, or leather seats can easily cost you thousands.

- Mileage Adjustments: The software adjusts the value up if your mileage is low for its age, and down if it's high. You need to ensure this is calculated fairly.

- Condition Rating: This is where things get really subjective. The pre-accident condition of your car—excellent, very good, average—has a massive impact on the final number.

- Recent Upgrades: Did you just put on a brand-new set of tires? A new battery? These items add real value and absolutely should be part of the calculation.

Let's say your prized pickup truck gets T-boned. It wasn't your fault, but the insurance company totals it and offers you $22,500. You jump online and see that similar trucks in your area are selling for closer to $28,000. This happens all the time. With repair costs skyrocketing, total loss claims are hitting record highs, and insurers are feeling the pressure.

Your First Step is Scrutiny

Your very first move should be to demand a complete copy of the valuation report. Don't settle for a one-page summary; you need the entire, multi-page document. Once you have it, sit down and go through it line by line.

Look for obvious errors. Did they list your car as a base model when it’s a premium trim? Did they miss the factory navigation system? Is the condition rating fair? Every mistake you uncover is ammunition for negotiating a better settlement.

The key is to see their offer not as a final number, but as an opening bid—one that's based on data you have every right to challenge. For a deeper dive, check out our guide on calculating a total loss vehicle's value for more hands-on strategies.

So, What Are Your Rights and Options Now?

After the insurance company declares your car a total loss, the initial shock wears off, and you're left facing a series of decisions. It can feel like the insurer holds all the cards, but you actually have more say in this process than you might think. How you navigate these next steps will make all the difference in your financial outcome.

Most people simply follow the script the insurer provides. They accept the settlement offer, sign over the title to their wrecked car, and wait for the check to arrive. The insurer then takes the car and sells it at a salvage auction to recover a portion of what they paid out.

While that's the most common path, it's definitely not your only one. Before you put a pen to any paperwork, you need to understand your other options—especially if you suspect the settlement offer is too low or if you have a special connection to your vehicle.

You Can Actually Keep Your "Totaled" Car

One of the most powerful, and often overlooked, options is called owner retention, or what most people call a "buyback." This lets you keep your vehicle instead of handing it over to the insurance company. It's a great choice for people with classic cars, highly customized vehicles, or even just older, mechanically solid cars they know how to fix themselves.

So how does the money work out? It’s surprisingly simple. The insurer calculates the settlement like this:

Your Payout = Actual Cash Value (ACV) – Salvage Value

Basically, they figure out what your car was worth right before the crash (the ACV) and subtract what they would have gotten for it at a salvage auction. They cut you a check for the difference, and you get to keep the car.

For example, let's say your car's ACV is $15,000 and its salvage value is $3,000. The insurance company would pay you $12,000. You get the cash and you keep your car, giving you the freedom to repair it on your own schedule or even use it for parts.

What Happens to the Title?

Choosing to keep your car permanently changes its legal status. That clean title you had is gone for good, replaced by what’s known as a "branded title."

- Salvage Title: The moment you retain the vehicle, the DMV issues a salvage title. This is a big deal—it means the car is no longer street-legal. You can't register it, drive it, or get insurance for it until it's been professionally repaired and inspected.

- Rebuilt Title: After you've completed all the necessary repairs to make the car safe and roadworthy again, it has to pass a rigorous state inspection. If it passes, the DMV will issue a rebuilt title. This lets you legally register, drive, and insure the car, but that "rebuilt" brand is now a permanent part of its history, which will significantly lower its future resale value.

Keep in mind that states have their own specific rules. Both Oregon and Washington, for instance, have very strict inspection requirements to move a car from a salvage to a rebuilt title, all designed to make sure the vehicle is truly safe to be back on the road.

Your Secret Weapon: The Appraisal Clause

What if you and the insurer are at a complete stalemate over your car's value? You've sent them comps, you've argued your case, but they won't move an inch on their lowball offer. This is where your policy's most powerful tool comes into play: the Appraisal Clause.

Buried in the fine print of almost every auto insurance policy is a clause that gives you the right to demand an independent resolution when you disagree with the company's valuation. Invoking this clause takes the decision completely out of the insurer's hands.

It kicks off a formal process where you and the insurance company each hire your own certified, independent appraiser. Those two appraisers then negotiate to determine the vehicle's real value. If they can't come to an agreement, they bring in a neutral third appraiser (an umpire) to make the final call. This contractual right is your ultimate defense against an unfair valuation, ensuring the final number is based on objective, real-world data—not the insurer's self-serving software.

How to Dispute a Low Settlement Offer

When the insurance company slides a settlement offer across the table that feels downright insulting, it’s easy to feel frustrated and powerless. But don't be. That first offer is just that—an offer. It’s a starting point for a negotiation, not a final decree etched in stone.

The key is to remember that their number is based on their data, which often comes from valuation software that doesn't capture your vehicle's true story. Your job now is to build a counter-argument grounded in real-world facts. This means doing a little homework: find recent sales listings for cars just like yours in your area, pull together every maintenance receipt you have, and document any recent upgrades, whether it's brand-new tires or a recently replaced timing belt. Presenting this information clearly and calmly to the adjuster can often be enough to get them to bump up their offer.

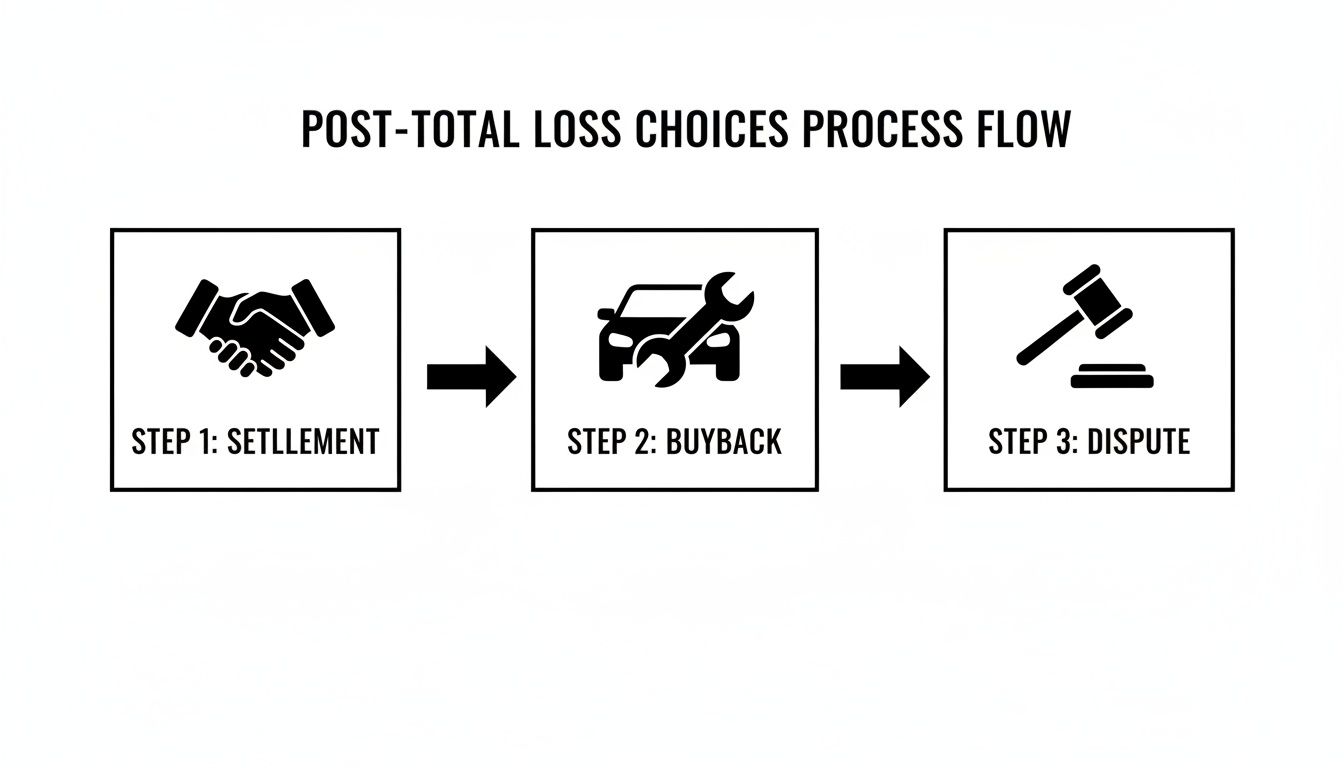

The flowchart below breaks down the three main paths you can take once your car is declared a total loss.

As you can see, while simply accepting the check or buying back the salvage are common choices, disputing the offer is a powerful third option every policyholder has.

Invoking the Appraisal Clause: Your Ultimate Right

So, what happens if you’ve laid out your evidence, but the insurer just won't budge? This is where you bring out the big gun: the Appraisal Clause.

It’s a provision tucked away in the fine print of almost every auto policy in states like Oregon and Washington, and it’s your contractual right to force a fair, independent review. Think of it as your escape hatch from the insurer’s one-sided process. By invoking it, you officially trigger a dispute resolution process that takes the valuation out of the insurance company’s hands and gives it to neutral, certified professionals. It’s your ultimate piece of leverage.

This isn't just a polite request; it's a formal demand your insurer is legally obligated to honor. Taking this step sends a clear message: you’re serious about getting what your car was truly worth, and you’re prepared to use the mechanisms in your own policy to do it.

The Step-by-Step Appraisal Process

Once you put your invocation in writing, a very specific sequence of events kicks off. It's a structured and binding process designed to land on an impartial and fair value for your totaled vehicle.

- Formal Written Notice: The first step is to officially notify your insurance company, in writing, that you are invoking the Appraisal Clause as outlined in your policy.

- Select Your Appraiser: You hire your own certified, independent auto appraiser to represent your interests. You’ll want someone with deep experience in total loss claims who knows how to build a rock-solid valuation.

- The Insurer Hires Their Appraiser: In response, your insurance company will hire its own appraiser to represent them.

- Negotiation Begins: The two appraisers then get to work. They’ll present their research and negotiate to come to an agreement on your vehicle’s Actual Cash Value (ACV). Crucially, they use real-world data like local comparable sales and condition reports, not the insurer's internal software.

- The Umpire Decides: If the two appraisers can't reach an agreement, they jointly select a neutral third-party appraiser, called an umpire. The umpire reviews both valuations and makes a final, binding decision.

This process is an absolute game-changer, especially for owners of classic, custom, or high-end vehicles. Standard insurance software completely misses the nuances that create value—like a low-mileage premium or the worth of specialty modifications—often leading to lowball offers that are thousands of dollars off. A skilled appraiser invoking the Appraisal Clause can often boost settlement payouts by 15-30% or more, simply by presenting evidence that holds up.

Key Takeaway: The Appraisal Clause is your contractual right to bypass the insurer's often-flawed valuation software and have independent experts determine your car's true market value.

Ultimately, this process forces a settlement that reflects what your vehicle was actually worth the moment before the accident. For a deeper dive into the tactics involved, our guide on how to negotiate a total loss settlement breaks it all down.

Finalizing Your Claim and Getting Paid

So, you’ve navigated the negotiations and finally agreed on a fair settlement figure. Great work! Now it’s time to cross the finish line, which involves some key paperwork and getting that check in your hand.

This last phase can feel a bit like running through a maze of forms, but knowing what's coming makes it much less intimidating. Let's break down exactly what happens next.

The first thing the insurance company will want is for you to sign over ownership of your wrecked vehicle. They'll send a packet of documents that usually includes a Bill of Sale, a Power of Attorney (so they can handle the title transfer), and a Release of All Claims.

Go through these documents carefully. Signing them is the final act that transfers the title and officially closes your claim.

Managing Paperwork and Your Title

Once you've settled on a number, the insurer needs your vehicle’s title to take possession.

If you own your car outright (no loan), it’s pretty simple. You’ll sign the physical title and hand it over. This is what allows the insurance company to legally sell the car for salvage.

But if you have a loan, your bank or credit union is the lienholder and they're the ones holding the title. In this case, the insurer will work directly with your lender to get the title. You'll just need to sign some authorization forms to get that ball rolling.

A Word of Warning: Do not sign anything—especially the title or a Release of All Claims form—until you are 100% satisfied with the settlement amount. Your signature is legally binding. Once you sign, there's no going back to ask for more.

What Happens If You Have an Auto Loan?

When there's a loan on your totaled car, things work a little differently. Your lender has a financial interest in the vehicle, which means they get paid first. This is standard practice.

The settlement check is often made out to both you and your lender. You'll endorse it, and the funds go straight to the financial institution to pay off your loan.

Here are the two ways this usually plays out:

- Positive Equity: Your settlement is more than your loan balance. If your settlement is $20,000 and you still owe $17,000, the lender gets their $17,000, and you get a check for the remaining $3,000.

- Negative Equity: Your settlement is less than what you owe. This is where it gets tricky. If the settlement is $20,000 but you owe $22,000, you are on the hook for that $2,000 difference. This is precisely the scenario where Guaranteed Asset Protection (GAP) insurance can be a real financial lifesaver.

Timeline for Receiving Your Payment

After you've signed on the dotted line and sent everything back, how long does it take to get paid?

It varies, but once the insurer has the signed title and release forms, the check is usually issued within a few days to a couple of weeks. Many states have "prompt payment" laws requiring insurers to pay within 30 days of reaching a settlement.

To keep things moving, check in with your adjuster to confirm they've received all the paperwork. A quick follow-up call can prevent unnecessary delays. For a deeper dive into what to expect, check out our guide on the typical auto accident settlement timeline. Following these final steps will help you close out your claim with confidence and get you back on the road.

Common Questions About Total Loss Claims

When your car is declared a total loss, it's like being thrown into a new world with its own confusing language and rules. A lot of questions pop up right away, and getting clear answers is the first step to taking control of the process. Let's walk through some of the most common things people ask.

Can I Keep My Rental Car After a Total Loss Is Declared?

This is usually the first panic-inducing question, and the answer isn't what most people expect. Your rental car coverage doesn't last until you buy a new car. Instead, it typically ends just a few days after the insurance company makes its first settlement offer.

Most policies give you a grace period, usually about three to five days, after that initial offer hits your inbox. If you're negotiating for a better settlement—and you should be—you can absolutely ask for an extension on your rental. It's not a guarantee, but adjusters often grant it if you're making a good-faith effort to settle the claim. Just be sure to get the exact end date in writing so you don't get hit with a surprise bill.

What if I Owe More on My Loan Than the Settlement?

Finding yourself "upside-down" on your loan is a tough spot to be in. It means the insurance company's settlement for your car's Actual Cash Value (ACV) is less than what you still owe the bank. You’re on the hook for the difference.

Imagine the insurer's final offer is $18,000, but your loan balance is $21,000. That leaves a $3,000 gap. The settlement check will be made out to both you and your lender, so they get paid first. You’ll have to come up with that remaining $3,000 out of pocket to officially close the loan.

This is exactly why Guaranteed Asset Protection (GAP) insurance exists. If you have a GAP policy, it steps in and pays that $3,000 shortfall for you, turning a potential financial disaster into a manageable situation.

Do I Have to Accept the First Settlement Offer?

No. Absolutely not. Let me say it again: you do not have to accept the first offer.

Think of the insurer's initial offer as their opening bid in a negotiation, not the final word. It’s generated by valuation software that often gets things wrong—like missing options, using the wrong trim package, or applying unfair condition adjustments.

You have the right to push back. Here's how:

- Demand a copy of their valuation report. Go through it line by line and look for errors.

- Do your own homework. Find real, local listings for cars that are a true match for yours in year, make, model, trim, options, and mileage.

- Build your case. Present your evidence to the adjuster and make a counteroffer based on real-world market data.

The insurance company’s job is to close claims as quickly and cheaply as possible. Your job is to make sure you get the full, fair market value you’re legally owed. If you hit a wall, invoking your policy's Appraisal Clause is the ultimate power move to force an independent, unbiased valuation.

Does Diminished Value Apply to a Total Loss?

This is a common point of confusion. Diminished Value is the loss in a vehicle’s resale value after it has been in a wreck and then repaired. The keyword there is "repaired."

Since a totaled vehicle isn't being repaired, a traditional diminished value claim doesn't apply. However, the goal is identical. A total loss settlement is supposed to give you the full pre-accident market value (ACV) of your vehicle. A proper, independent appraisal ensures you get that full value, which effectively makes you whole—the same financial outcome a diminished value claim aims for.

While accidents are common, other events can also lead to a total loss. For instance, electric car fire statistics show how certain types of catastrophic damage almost always result in a vehicle being written off, making a solid understanding of this process essential.

What Happens to My Personal Belongings in the Car?

Your auto insurance policy covers the car, not the stuff inside it. You'll need to schedule a time to go to the tow yard or storage facility and clean out your personal belongings. It’s best to do this quickly, as those storage lots start charging daily fees that can add up fast.

If items like a laptop, phone, or car seat were damaged in the crash, you might have coverage. Check your homeowners or renters insurance policy; you can often file a claim for those items there, though you'll have to pay your deductible.

Should I Continue Making My Car Payments?

Yes, without a doubt. Your loan agreement is with the bank, not the insurance company. Until that loan is officially paid in full, you are contractually required to keep making your payments on time.

Missing payments—even on a car that's a pile of metal in a tow yard—will get reported to the credit bureaus and will tank your credit score. Keep paying as scheduled while the claim is being processed. Once the lender receives the settlement check and closes the loan, they will refund any overpayments you made.

Navigating a total loss claim requires expertise and a commitment to ensuring you receive every dollar you are rightfully owed. If you believe your insurance company's offer is too low or the process feels overwhelming, Total Loss Northwest is here to help. We are certified independent appraisers who fight for vehicle owners in Oregon and Washington. We invoke the Appraisal Clause to ensure your settlement is based on true market value, not flawed software. Contact us today for a fair and accurate appraisal.