When you hear an insurance adjuster talk about "Actual Cash Value," or ACV, they're really just talking about what your property is worth today—not what you originally paid for it. It’s a lot like how a car loses value. The second you drive a new car off the dealer's lot, it starts to depreciate. ACV works the same way for your insured belongings, whether it's your laptop, your roof, or your living room sofa.

Breaking Down Actual Cash Value in Simple Terms

This concept is the bedrock of most standard home and auto insurance policies. It’s the method insurers turn to when they need to figure out how much to pay you for an item that's been damaged or destroyed. While the calculation itself looks simple on the surface, the two main ingredients—replacement cost and depreciation—are where things can get a bit tricky.

At its heart, your insurance payout is determined by a straightforward formula.

The ACV Formula: Replacement Cost (RC) – Depreciation = Actual Cash Value (ACV)

Let’s unpack those terms with an example you can relate to.

The Two Main Ingredients of an ACV Calculation

Imagine a kitchen fire ruins your five-year-old refrigerator. To figure out its ACV, your insurance adjuster will first find out what a new, similar fridge costs today, and then they'll subtract a certain amount for the years of use it already had.

-

Replacement Cost (RC): This is simply the price of buying a brand new refrigerator of similar kind and quality today. If a comparable new model costs $1,500, that's the starting number.

-

Depreciation: This is the value your fridge lost over the five years you owned it. It accounts for normal wear and tear, age, and the fact that newer, better models are now available. If the adjuster figures it lost $700 in value over that time, that's your depreciation.

Plugging those numbers into the formula, your ACV payout would be $800 ($1,500 – $700). This $800 represents the fair market value of your used fridge right before it was damaged.

It’s also important to know that many insurance policies use a mix of valuation methods. For example, your policy might cover the physical structure of your house at its replacement cost but cover your personal belongings inside at their actual cash value. This is a very common approach, and you can learn more about these standard insurance practices and how different valuation types are combined.

How Insurers Figure Out Depreciation on Your Property

Depreciation is almost always the most contentious part of an actual cash value (ACV) claim. Why? Because it’s the number that directly shrinks your insurance check. It represents the value your property lost over time from normal aging, use, and general wear and tear.

While the final number might feel like a judgment call, insurers don't just pull it out of thin air. They have standard methods for putting a price tag on that loss in value.

Think of it this way: a brand-new item is like a fully charged battery at 100%. As years go by and you use it, that charge—its value—slowly drains. Depreciation is just a measurement of how much charge it lost. The ACV payment you receive is for the value that was left right before the incident happened.

What Goes into the Depreciation Calculation?

An adjuster’s job is to blend hard data with the real-world specifics of your property. They aren’t just guessing; they’re analyzing a few key things to land on a fair depreciation amount.

Here are the main ingredients they look at:

- Expected Lifespan: Everything has an estimated shelf life. Industry data gives adjusters a baseline—a standard architectural shingle roof is expected to last 20-30 years, while a laptop is usually good for about 5 years.

- Age: This one's simple. The older something is, the more value it has likely lost. An eight-year-old appliance has seen more action than a two-year-old one.

- Pre-Loss Condition: This is where your maintenance habits really pay off. A five-year-old sofa that looks brand new because you cared for it will be depreciated far less than another five-year-old sofa with stains, saggy cushions, and a broken spring.

- Market and Obsolescence: Sometimes, an item loses value simply because something better came along. A top-of-the-line plasma TV from 2012 might still be in perfect condition, but it's lost a ton of value because 4K and 8K TVs are now the standard.

Seeing Depreciation in Action

So how does this all come together in a real claim? Let's walk through it. The go-to method for most insurers is straight-line depreciation, which is a fancy way of saying an item loses value evenly each year.

Example 1: A Five-Year-Old Roof

A hailstorm wrecks your roof. It’s made of 30-year architectural shingles and you had it installed five years ago. A contractor quotes you $15,000 for a full replacement today.

- Lifespan: 30 years

- Age: 5 years

- Depreciation Rate: 1/30, which is about 3.33% per year.

- Total Depreciation: 5 years x 3.33% = 16.65%

- Depreciation Amount: $15,000 x 0.1665 = $2,497.50

- ACV Payout: $15,000 – $2,497.50 = $12,502.50

The adjuster systematically breaks it down to find the roof’s current value. The same logic works for your personal belongings inside the house.

Example 2: A Three-Year-Old Laptop

Your laptop gets fried in a power surge. You bought it three years ago, and a comparable new one costs $1,200. Laptops like yours typically have a five-year lifespan.

- Lifespan: 5 years

- Age: 3 years

- Depreciation Rate: 1/5, or a straight 20% per year.

- Total Depreciation: 3 years x 20% = 60%

- Depreciation Amount: $1,200 x 0.60 = $720

- ACV Payout: $1,200 – $720 = $480

Once you understand this math, you’re in a much better position to review the insurance company’s settlement offer. If you have photos showing your property was in pristine condition, or manufacturer specs suggesting a longer lifespan, you have a solid foundation to negotiate a better payout.

How Actual Cash Value Works in Homeowners Insurance

When you're dealing with a homeowners insurance claim, you’ll quickly discover that not everything is treated equally. Most standard policies draw a clear line between your house itself—the physical structure—and all the personal belongings you keep inside it.

Understanding this distinction is crucial because it directly impacts the payout you receive after a covered loss. It’s very common for policies to cover the structure for its Replacement Cost Value (RCV) but only cover your personal property for its Actual Cash Value (ACV).

This means if a fire guts your living room, your insurance will likely pay to rebuild the walls and floors with brand-new materials (RCV). But when it comes to your couch, TV, and rugs, they’ll only pay what those items were worth the moment before the fire, after accounting for wear and tear (ACV). This "mixed" coverage helps keep premiums down, but it can also create a major financial gap when you're trying to replace everything.

For instance, many basic policies default to ACV for both the home and its contents unless you specifically upgrade. With residential buildings depreciating at an average rate of 3.6% annually, a home you bought for $300,000 could have an ACV of just $272,000 only three years later. You can get a better sense of how home depreciation impacts your policy and see why this matters for your financial security.

A Practical Scenario: The Kitchen Fire

Let's walk through a real-world example. Imagine a fire breaks out and destroys your kitchen. You lose your beautiful ten-year-old custom oak cabinets and your five-year-old stainless steel appliances.

Here’s a breakdown of how a typical insurance policy would handle it:

-

The Cabinets (Part of the Structure): Assuming your dwelling coverage is RCV, the insurance company will pay the cost to install brand-new cabinets of similar kind and quality, minus your deductible. They’re focused on making that part of your home whole again.

-

The Appliances (Personal Property): Your stove, fridge, and microwave are considered personal belongings. Under ACV coverage, the adjuster won't look at what you originally paid for them. Instead, they'll calculate their current, used value by subtracting five years of depreciation. The check you get will almost certainly not be enough to go out and buy new models.

This simple scenario makes it crystal clear why you need to know exactly what your policy says. The gap between RCV and ACV can easily add up to thousands of dollars you'll have to pay out-of-pocket.

Upgrading Your Coverage With Endorsements

The good news? You aren't necessarily stuck with basic ACV coverage for your belongings.

Most insurers offer add-ons, called endorsements or riders, that let you upgrade your personal property coverage from ACV to full RCV.

An endorsement is simply an amendment that changes the original terms of your insurance contract. For homeowners, adding a Replacement Cost Value endorsement for personal property is one of the smartest and most common upgrades you can make.

By adding this rider, you’re buying peace of mind. It ensures that if your five-year-old appliances are ruined, you get enough money to buy new ones. Yes, it will raise your premium slightly, but the financial protection it offers during a crisis is often worth every extra penny. Take a look at your policy’s declaration page—it will tell you exactly what coverage you have right now.

Navigating Actual Cash Value for Your Car

When your car is declared a total loss, one number suddenly matters more than any other: its Actual Cash Value (ACV). This is the figure your insurance company will pay out, and it represents your car's market value the instant before the crash happened. It's not what you originally paid, and it's definitely not what you might still owe on your loan.

This is a tough pill to swallow for many drivers. You might have bought your car for $30,000 just a couple of years ago, but depreciation is a harsh reality. A car's value starts to drop the moment you drive it off the lot, and that steep decline is a key part of how insurers calculate ACV. For a deeper dive, you can learn more about the factors that determine your car's value in these situations.

How Insurers Determine Your Car's ACV

So, how do insurance companies land on that specific dollar amount? It's not a random guess. Adjusters lean on specialized third-party data and a checklist of concrete factors to build a detailed valuation report. While you can get a great overview in our guide on how ACV is determined for a car, the process boils down to a few key areas:

- Mileage: More miles on the odometer almost always means a lower ACV. It’s a direct indicator of wear and tear on the engine and other critical parts.

- Pre-Accident Condition: The adjuster will account for any dings, scratches, interior stains, or mechanical issues your car had before the accident. A meticulously maintained vehicle will naturally command a higher value.

- Recent Sales Data: This is a big one. They look at what comparable cars—the same make, model, year, and trim—have actually sold for in your local area.

- Options and Trim Level: A top-tier model with all the bells and whistles is worth more than a bare-bones base model.

The Dreaded Coverage Gap

This is where the math can become painful. What happens if the ACV check from your insurer is less than what you still owe on your car loan? That shortfall is known as the "coverage gap."

For example: Let's say you still owe $18,000 on your auto loan. After the accident, the insurance company determines your car's ACV is only $15,000. They'll send that check to your lender, but you're still on the hook for the remaining $3,000 balance—for a car you can't even drive anymore.

This isn't a rare scenario; it’s incredibly common, especially if you had a small down payment or a long loan term. This is precisely why gap insurance was created. This optional coverage steps in to pay off that remaining loan balance, bridging the financial gap so you aren't stuck paying for a totaled vehicle out of pocket.

ACV vs RCV vs Fair Market Value

When you're dealing with an insurance claim, a few terms get thrown around that can sound confusingly similar: Actual Cash Value (ACV), Replacement Cost Value (RCV), and Fair Market Value (FMV). It's crucial to know the difference, as it can mean a swing of thousands of dollars in your final payout.

Think of it this way: ACV and RCV are insurance-specific languages for figuring out how much they owe you. Fair Market Value, on the other hand, is the language of the open market—what something would sell for between a willing buyer and seller, like on a car lot or in a real estate deal.

The Core Differences

The real heart of the matter boils down to a single, powerful concept: depreciation. How an insurance policy handles depreciation is what separates these valuation methods.

-

Actual Cash Value (ACV): This is what your property is worth in its current, used condition. The insurance company starts with the cost of a brand-new replacement and then subtracts a dollar amount for every year of age, wear, and tear. ACV policies are cheaper, but the payout won't be enough to buy a brand-new replacement.

-

Replacement Cost Value (RCV): This is the gold standard for coverage. RCV policies pay the full amount needed to replace your damaged item with a new one of similar quality—no deduction for depreciation. You get more protection, but you'll pay a higher premium for it.

-

Fair Market Value (FMV): This is the price your property would fetch on the open market right before it was damaged. While it sounds a lot like ACV, especially with vehicles, they aren't always the same. An insurer's ACV calculation might be more rigid and less generous than the true market price. You can learn more about this in our guide on what is fair market value.

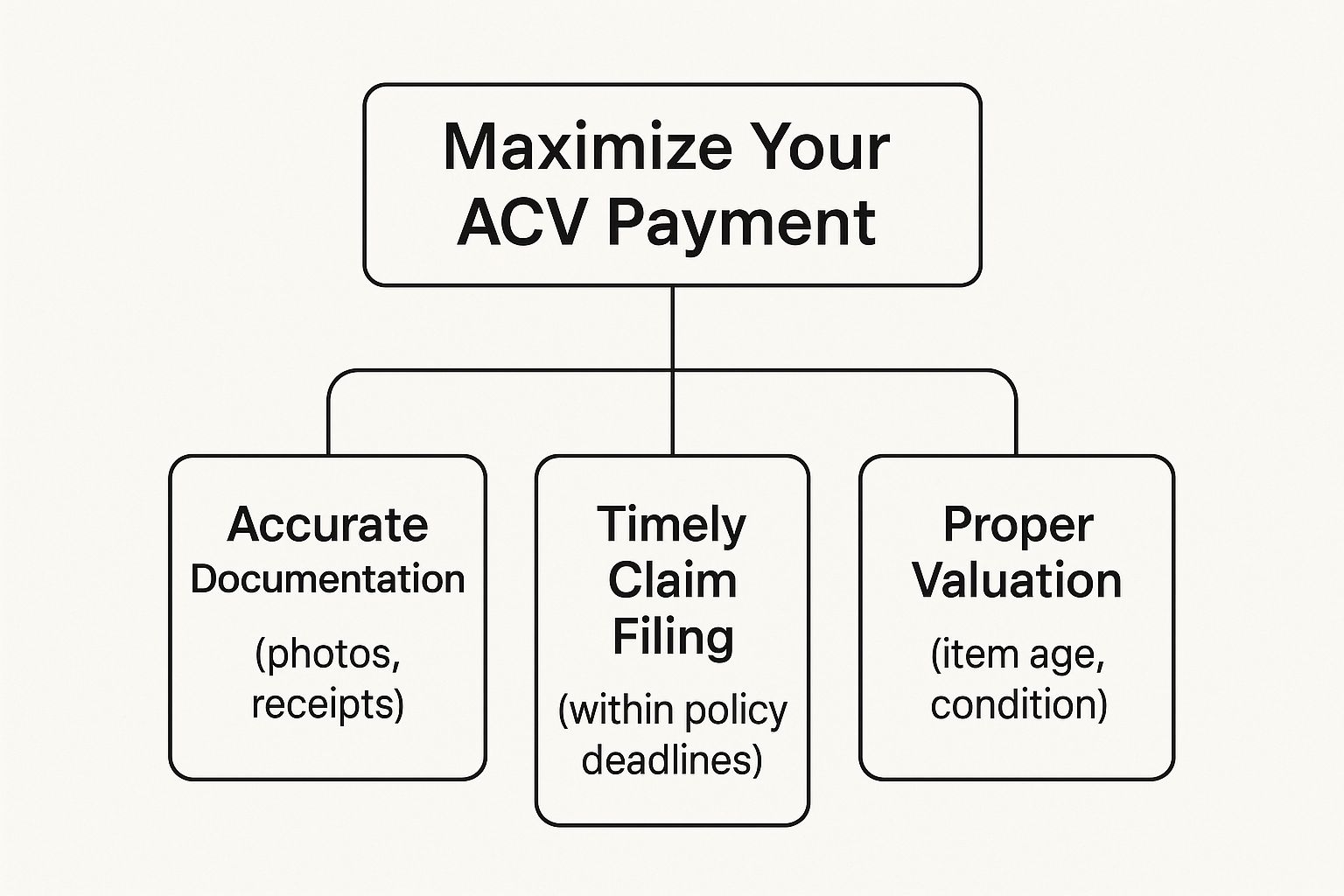

This chart breaks down the key steps to securing a fair ACV settlement, emphasizing the importance of documentation and proper valuation.

As you can see, getting the payout you deserve often comes down to providing solid proof of your item's pre-loss condition and value.

To make these distinctions even clearer, here’s a quick comparison table.

Valuation Method Breakdown

| Valuation Method | What It Covers | Best For | Typical Premium Cost |

|---|---|---|---|

| Actual Cash Value (ACV) | The cost of a new item minus depreciation. | Keeping premium costs low; insuring older items. | Lower |

| Replacement Cost (RCV) | The full cost to buy a brand-new replacement. | Ensuring you can fully recover from a loss. | Higher |

| Fair Market Value (FMV) | The price an item would sell for in its current condition. | Real estate, vehicle sales, and legal valuations. | N/A (Market-driven) |

The table really highlights how RCV is designed to make you whole again, while ACV provides a more budget-friendly but partial reimbursement.

Seeing It in Action

Let’s put this into a real-world scenario. Imagine a hailstorm totals your 10-year-old roof.

-

With an ACV policy, the insurer would calculate the cost of a new roof today and then subtract 10 years' worth of depreciation. You’d get a check for a fraction of the replacement cost, leaving you to pay the rest out of pocket.

-

With an RCV policy, you'd get a check for the full amount it costs to install a brand-new roof of similar quality. It's a much better financial outcome.

-

The Fair Market Value of the roof itself is essentially zero before the storm—no one buys a used roof. However, its condition would have been factored into the overall FMV of your home if you were selling it. For more on how these values play out in high-stakes markets, it's worth understanding car market prices and how they are determined.

Ultimately, digging into your policy documents to see whether you have ACV or RCV coverage is one of the smartest things you can do before you ever have to file a claim. It sets your expectations and tells you exactly what to prepare for financially.

What to Do When Your ACV Offer Seems Too Low

It’s a sinking feeling—you get the settlement offer from your insurance company, and the number just feels wrong. It’s a common and deeply frustrating moment, but here’s the good news: their first offer is just that, an offer. It's not the final word.

You absolutely have the right to question their math and push for the true value of your property. Don't just accept the initial figure. Your first move is to formally ask for the insurer’s complete valuation report. This document is the key, as it breaks down exactly how they landed on their number, showing the comps they used and the depreciation they calculated.

Building Your Counter-Argument

With their report in hand, it's time to build your own case. Your mission is to gather concrete proof that your property's pre-loss condition and value were better than the adjuster's assessment. The more solid documentation you can provide, the stronger your negotiating position becomes.

Start digging for any evidence that supports your claim's value:

- Original receipts are gold. They establish what you paid and when you bought the item.

- Photos and videos from before the loss can vividly demonstrate the item was in excellent shape.

- Maintenance records for vehicles, appliances, or roofing prove you took great care of your property, which slows depreciation.

- Online listings for identical or very similar used items are perfect for challenging the lowball comparables the insurer might have used.

By presenting a well-documented counter-offer, you shift the conversation from their opinion to your facts. This approach demonstrates that you've done your research and are serious about receiving a fair settlement for your property.

If you’re dealing with a totaled car, learning how to negotiate a total loss settlement is crucial. For bigger, more complex claims—like significant damage to your home—don't be afraid to bring in a professional.

Hiring a certified independent appraiser or a public adjuster can be a game-changer. They provide an unbiased, expert valuation that gives you the leverage you need to get the money you're truly owed.

Answering Your Top Questions About ACV

Let's tackle some of the most common questions that pop up when dealing with Actual Cash Value. These are the sticking points we see time and time again, so let's clear them up.

Is Actual Cash Value the Same As Fair Market Value?

It’s a common mix-up, but no, they aren't quite the same. Think of it this way: Fair Market Value (FMV) is the real-world price a willing buyer would pay for something today. It’s what your car would sell for on Craigslist or at a dealership.

Actual Cash Value (ACV), on the other hand, is an insurance industry formula: Replacement Cost minus Depreciation. While they can be very close, especially for vehicles, an insurer's strict ACV calculation can sometimes produce a lower number than what the car is truly worth on the open market.

Can I Dispute the Insurer's ACV Calculation?

Yes, you can and you absolutely should if the number feels wrong. The first offer from an insurance company is just that—an offer. It's a starting point for a conversation, not a final, take-it-or-leave-it declaration.

The secret to successfully challenging a low ACV is documentation. You need to build your own case with hard evidence. Pull together original purchase receipts, detailed maintenance records, and—most importantly—local listings for comparable vehicles to prove what yours was really worth.

How Does Salvage Value Affect My Payout?

This comes into play when your car is declared a total loss. The insurer determines its pre-accident ACV, and that’s the baseline for your settlement.

But what if you want to keep the wrecked vehicle? In that case, the insurer will deduct the car's salvage value—what the damaged shell and its parts are worth—from your payout.

For instance, if your car's ACV was $10,000 and the wreck is worth $1,500 for salvage, your check would be for $8,500 if you decide to keep the car.

Handling a total loss claim is tricky, and a low ACV offer can force you to dig into your own savings to get back on the road. At Total Loss Northwest, our certified independent appraisers work for you, not the insurance company, to secure the fair settlement you’re entitled to. We invoke the Appraisal Clause in your policy, forcing a valuation based on real market data, not just their internal software. Don't let them undervalue your vehicle—contact us for a fair and accurate appraisal.