When an insurance adjuster declares your car a total loss, it means one simple thing: the cost to repair it is more than its Actual Cash Value (ACV). This isn't the final word, though. Your immediate next steps are to understand their settlement offer, gather your own evidence, and get ready to negotiate—the insurer's first number is rarely their best.

My Car Was Totaled—Now What?

Hearing the words "total loss" can feel like a final verdict, but it’s really just the opening move in a detailed process. An insurer makes this call based on a straightforward economic formula. When the estimated repair costs plus the car's scrap value exceed what it was worth moments before the crash, they'll "total" it.

This isn't an arbitrary decision about how wrecked the car looks; it's a financial one designed to limit the insurance company's losses. The key variable in this equation, however, is the car's pre-accident value, and this is where you have the most room to advocate for yourself.

That "totaled" declaration is just the start of the conversation. Here’s a quick rundown of your immediate priorities to make sure you stay in control of the process.

Immediate Actions After a Total Loss Declaration

| Action Item | Why It's Important | Key Tip |

|---|---|---|

| Request the Valuation Report | This document shows exactly how the insurer calculated your car's ACV. | Don't just accept the final number. Ask for the full report, which should list comparable vehicles ("comps") and adjustments. |

| Gather Your Own Comps | Find local listings for cars of the same year, make, model, and trim. | Focus on dealership listings, not private party sales. Screen-shot everything, including the VIN and mileage. |

| Collect All Documentation | Find receipts for recent major repairs, new tires, or significant upgrades. | Anything you've spent money on that adds value (e.g., a new transmission, not an oil change) can increase the settlement. |

| Understand Your Policy | Review your coverage, including any gap insurance or new car replacement clauses. | Know your rights before you speak to the adjuster again. Your policy is your contract. |

Once you've got this information in hand, you’re no longer just reacting to the insurance company—you're prepared to have an informed negotiation about what your vehicle was truly worth.

Why Are So Many Cars Being Totaled Lately?

If it feels like you’re hearing about more and more cars being written off after accidents, you're not imagining it. This trend is being fueled by a few powerful economic factors that are stacking the deck against your car's survival.

- Soaring Repair Costs: Modern cars are packed with complex sensors, cameras, and computers. A simple fender bender can damage delicate electronics, sending repair bills skyrocketing.

- Aging Vehicle Fleet: The average car on U.S. roads is older than ever. For these vehicles, even moderate damage can easily cost more to fix than their lower market value is worth.

- Fluctuating Used Car Values: When the used car market cools down, vehicle values drop. A lower ACV makes it much easier for repair estimates to cross that "total loss" line.

Recent industry data paints a clear picture. The total loss frequency is hitting record highs, climbing to 22.8% of all claims in recent quarters. A huge contributor is the age of the cars involved; over 72% of total loss valuations were for vehicles that were seven years old or older, where insurers are much less likely to approve expensive repairs. You can dig into these trends yourself in the latest Crash Course report from CCC Intelligent Solutions.

The insurance company's declaration is not the end of the story—it's the start of a negotiation. Your job is to ensure their valuation reflects the true market value of what you lost, not just the number most convenient for their bottom line.

Understanding these dynamics is your first step to getting a fair shake. It proves that the "total loss" label is less about the car's condition and more about the cold, hard numbers. This is your cue to shift from feeling like a victim of circumstance to becoming an active participant in determining a fair outcome.

Understanding the Insurance Settlement Offer

So, the insurance company has officially declared your car a total loss. Now comes the part that really matters: their settlement offer. This number isn't pulled out of thin air. It’s supposed to represent your car's Actual Cash Value (ACV)—basically, what it was worth in the moments right before the crash.

The adjuster uses special software to generate a detailed valuation report to come up with this number. This report is the single most important document you’ll receive, and you have every right to ask for a complete copy. Don't just glance at the final dollar amount. You need to dig into the details, because this is where you'll find the leverage you need to ensure you're getting a fair shake.

Cracking Open the Valuation Report

That report might look intimidatingly official, but I've seen hundreds of them, and they are frequently full of mistakes. The software works by pulling in data from "comparable" vehicles—or "comps"—that have sold recently. And that's usually where the trouble begins.

Often, the insurer's comps are just plain bad. They might use a vehicle from a completely different state, one with way more miles, or a lower trim package than yours. I once saw an adjuster try to compare a client's meticulously maintained, garage-kept sedan to a beat-up former rental car that sold at a wholesale auction 200 miles away. These kinds of comparisons are designed to do one thing: lower your payout.

An insurance company’s first settlement offer is just that—an offer. Think of it as their opening bid in a negotiation, not the final word. Your job is to poke holes in their valuation and build a stronger case for what your car was actually worth.

It's time to put on your detective hat. Go through every single "comp" they list. Is it really the same trim level? Does it have the same features? What was its condition? Even small differences can snowball into a settlement that's thousands of dollars too low. To get a better sense of the big picture, it helps to understand what a fair car accident settlement amount looks like in general.

Common Red Flags to Watch For

As you comb through the valuation report, a few things should jump out at you. These are the classic areas where adjusters make "adjustments" that conveniently reduce the value of your vehicle.

- Unfair Condition Adjustments: The report will almost certainly have deductions for pre-existing wear and tear. But did they ding you for a tiny door ding or normal tread wear on your tires? These adjustments are highly subjective and often blown way out of proportion.

- Missing Upgrades and Features: Did you just put on a new set of premium tires? Upgrade the stereo? A new battery? The standard valuation software won't know about these things unless you prove it.

- Incorrect Vehicle Trim or Package: There’s a huge price difference between a base model and a top-of-the-line version. Make absolutely sure they've identified your car’s exact trim (e.g., LX vs. EX-L) and any factory-installed packages it had.

Let's say you spent $1,200 on new Michelin tires a month before the accident. If that's not listed in the report, your offer is already $1,200 short, plain and simple. Start gathering receipts and bank statements for any major maintenance, repairs, or upgrades you've made in the past year or two. This is your evidence. For a deeper dive, you can learn more about https://totallossnw.com/calculating-total-loss-vehicle/ and see how all these pieces fit together.

The Power of Doing Your Own Homework

Never let the insurance company be the only one doing the research. The most effective thing you can do right now is build your own case by finding better, more accurate comps.

Start searching online for vehicles for sale that are the same make, model, year, and trim as yours. The key is to look at listings from local dealerships, preferably within a 50-75 mile radius. Private party sales are harder to use as a benchmark, so stick to reputable dealer inventory.

When you find good matches, take detailed screenshots. You need to capture the vehicle's asking price, VIN, mileage, features, and photos. If you can find three to five solid, local examples, you can completely reframe the negotiation. You're no longer arguing about their questionable data from another state; you're talking about the real-world cost to replace your exact car, right here, right now. This simple step transforms you from a victim into a well-informed negotiator.

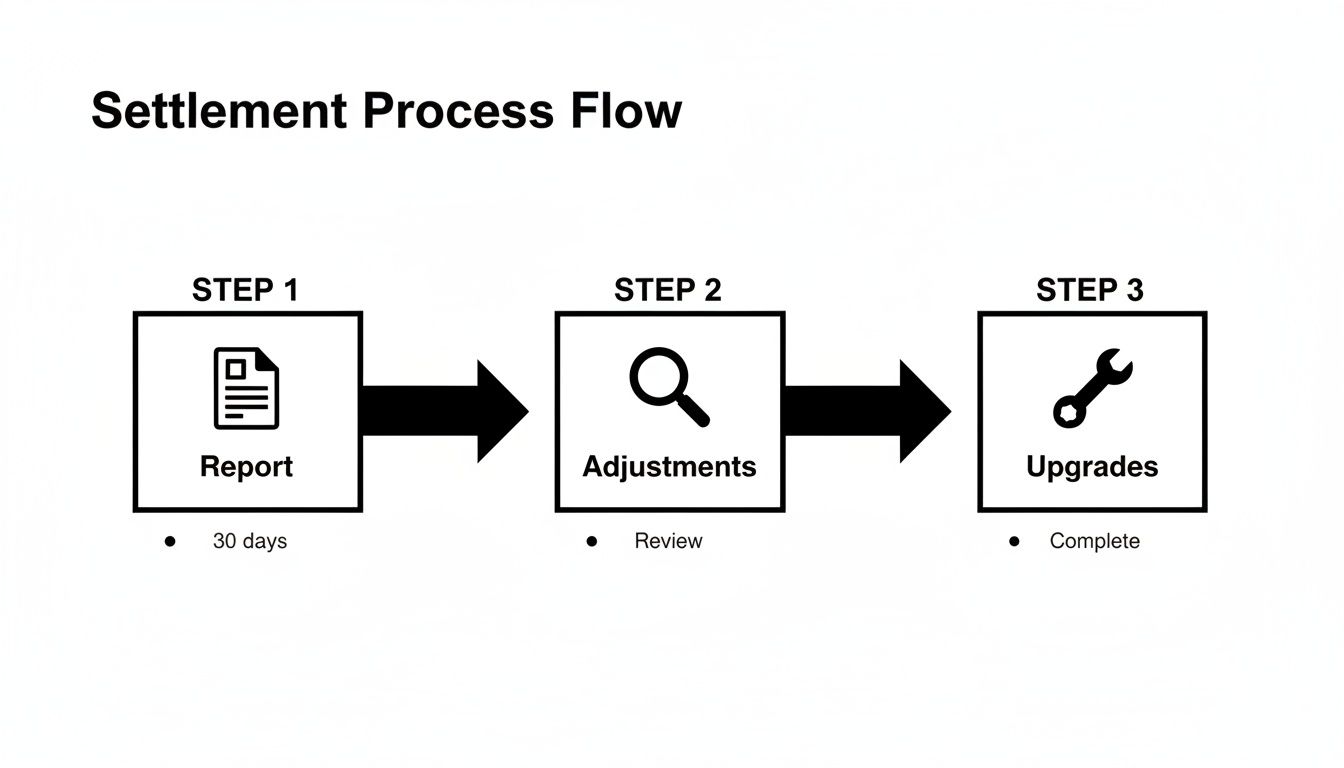

How to Dispute an Unfair Settlement

When the insurance adjuster's settlement offer finally lands in your inbox, it's easy to feel a sense of resignation. But if that number makes your stomach drop, trust your gut. An insurer's initial offer is rarely their best one; it's a starting point calculated by software that often misses the real-world value of a vehicle like yours.

You absolutely do not have to accept it. Here’s your playbook for fighting back.

The first move is to stop being a passive recipient of their lowball offer and become an active participant in your car's valuation. This means building a solid, evidence-based case for its true worth. Start by organizing the proof you've already gathered—those local comparable vehicle listings, receipts for the new tires or that recent brake job, and any documentation of special features or trim packages that made your car stand out.

This process is what separates a frustrating experience from a fair settlement. The infographic below breaks down the key elements you need to report and scrutinize to make sure the final number is accurate.

As this shows, the path to a fair settlement starts with your own reporting, moves through a sharp review of the insurer's adjustments, and ends with a strong argument for your vehicle's unique upgrades and value.

Build Your Counteroffer with Solid Evidence

Once your documentation is in order, it's time to draft a clear, professional counteroffer. This isn't the time for an angry email; think of it as a business communication backed by undeniable facts. Present your case logically and calmly.

Start by respectfully disagreeing with their proposed Actual Cash Value (ACV). Then, begin to systematically dismantle their valuation report by presenting your superior evidence.

Challenge Their Comps: List the comparable vehicles they used and explain exactly why they're a poor match. For example: "The 2018 Honda Accord you cited was a base LX model with 30,000 more miles, located 150 miles away. It is not a true comparable for my well-maintained EX-L model."

Present Your Comps: Now, introduce the local, dealership-listed vehicles you found. Include screenshots and links, pointing out how their trim, mileage, and condition are a much closer match to your car before the accident.

Itemize Your Upgrades: Clearly list any recent investments you made, like new brakes, tires, or a battery. Be sure to attach copies of the receipts as proof.

This methodical approach completely changes the conversation. You’re no longer just saying, "I think my car is worth more." You're proving it with market data they simply can't ignore.

The Ultimate Tool: The Appraisal Clause

So, what happens if the adjuster still won't budge? You have a powerful, but often overlooked, tool written directly into most auto insurance policies: the Appraisal Clause. Invoking this clause takes the decision out of the adjuster's hands entirely.

The process is refreshingly straightforward:

- You hire a certified, independent auto appraiser.

- The insurance company hires its own appraiser.

- The two appraisers review all the evidence and negotiate to agree on a value.

- If they can't agree, they select a neutral third appraiser (an umpire) to make a final, binding decision.

Taking this one step can be a complete game-changer. An independent appraiser works for you, not the insurance company. They conduct a thorough, unbiased evaluation based on real-world market conditions, not on the insurer’s cost-saving algorithms. Their detailed report becomes the new centerpiece of the negotiation, often forcing the insurer to significantly raise their offer.

It’s a critical tool, especially as modern vehicle complexity drives up repair costs and pushes more cars into the total loss category—a trend that has pushed the U.S. total loss frequency to a recent high of 22.6%. For many drivers, hiring an appraiser is the most effective way to reclaim value, as an insurer’s first offer is often 10-20% under market value. You can find more data on these industry shifts and explore the latest Crash Course report from CCCIS.

Invoking the Appraisal Clause is your right. It forces a fair, unbiased valuation and is often the fastest way to break a stalemate with a stubborn insurance adjuster.

Don't be intimidated by the process. While you are responsible for the cost of your appraiser, the return on that investment is frequently thousands of dollars in a higher settlement. When you're figuring out what to do with a totalled car, getting its full value is the most important financial step you can take. To better understand how this provision works, you can learn more about the insurance appraisal clause and how to use it to your advantage.

Deciding the Fate of Your Wrecked Car

Once you and the adjuster have finally settled on a fair number for your car, you’ve cleared a major hurdle. But now you’re facing another big decision: what actually happens to the vehicle itself?

You have two basic paths, and which one you take really boils down to your personal situation—your skills, your time, and what you hope to get out of this mess financially.

The most common, hassle-free option is to simply surrender the car to the insurance company. You sign the title over to them, they haul the wreck away, and you get a check for the full settlement amount. For most folks, this is the clean break they’re looking for. It’s simple, and it lets you move on.

The Owner Retention Option

Your other choice is to keep the car, which in industry terms is called owner retention.

If you go this route, the insurance company will figure out the car's salvage value—basically, what a scrap yard or auction house would pay for the wreck. They then subtract that amount from your settlement.

So, if your settlement was $15,000 and the salvage value is $2,000, you’d get a check for $13,000 and get to keep the car.

Be warned: The moment you choose owner retention, the DMV brands the vehicle with a salvage title. This is a permanent mark on its record, making it illegal to drive on public roads until it’s properly repaired and passes a series of stringent state inspections.

Hanging onto a totaled car is a serious commitment. It's not a decision to make on a whim, as it opens up a whole new can of worms you'll be responsible for.

Keeping vs. Surrendering Your Totalled Car

Deciding whether to keep the car or let the insurer take it can be tough. This table breaks down the key factors to help you weigh the pros and cons of each path.

| Consideration | Keeping the Car (Owner Retention) | Surrendering to Insurer |

|---|---|---|

| Settlement Payout | You receive the ACV minus the salvage value. | You receive the full Actual Cash Value (ACV). |

| Effort Required | High. You are responsible for all repairs, paperwork, and selling the car (or its parts). | Low. Sign the title, hand over the keys, and you're done. |

| Best For… | DIY mechanics, people parting out the car, or owners of rare/classic vehicles. | Anyone looking for the simplest, fastest, and most straightforward resolution. |

| Key Downside | The car gets a permanent salvage/rebuilt title, drastically lowering its future value. | You have no further claim to the vehicle or any of its parts. |

| Timeline | Can be very long, depending on repairs, inspections, and selling. | The process is usually completed within a few days of the settlement agreement. |

Ultimately, surrendering the car is the path of least resistance. But for those with the right skills or a specific type of vehicle, owner retention can sometimes put more money back in your pocket if you're willing to do the work.

When Keeping Your Car Makes Sense

So, why would anyone even want a totaled car? It’s definitely not the standard choice, but there are a few situations where it can be a smart move.

You might be a good candidate for owner retention if:

- You're a DIY Mechanic: If you have the garage, tools, and skills to do the repairs yourself, you can save thousands compared to what a professional shop would charge.

- You Plan to Sell it for Parts: A car is a collection of valuable components. The engine, transmission, infotainment system, and undamaged body panels can often be sold for more than the salvage value.

- It’s a Classic or Rare Car: For a special-interest vehicle, an insurer’s valuation might miss the mark. To an enthusiast, restoring a rare car might be a worthwhile passion project that also makes financial sense.

- The Damage is Mostly Cosmetic: Sometimes a vehicle is totaled because of something like widespread hail damage that makes it look terrible but doesn’t affect how it drives. If you can live with the dings, you can pocket the settlement money (minus salvage value) and keep driving a mechanically sound car.

The Long Road to a Rebuilt Title

If your plan is to fix the car and get it back on the road, you'll have to navigate the state’s process for getting a rebuilt title. This isn't just about bolting on a few new parts; it’s a bureaucratic process designed to ensure the car is safe.

While the specifics vary by state, you’ll generally have to:

- Document Everything: Keep a meticulous paper trail of all repairs, including receipts for every single part and any labor you paid for.

- Submit the Right Paperwork: You'll need to fill out and submit specific rebuilt title applications to your local DMV.

- Pass a Rigorous State Inspection: A certified state inspector will go over the vehicle with a fine-toothed comb, checking that the repairs are sound and all safety systems work correctly.

Only after you’ve passed that inspection can you legally register, plate, and insure the car again. And remember, that "rebuilt" brand on the title sticks with the car forever, which will always hurt its resale value. Make sure you weigh the costs and effort against what you’ll end up with.

How to Sell Your Totalled Car

So, you've gone through the settlement process and decided to keep your car. Now what? The focus shifts from getting a fair insurance payout to squeezing every last dollar out of that damaged vehicle. Selling a car with a salvage title isn't like a normal private sale, but with the right approach, you can definitely come out ahead.

You really have three main routes you can take. There’s the fast and simple path of selling it to a local salvage yard, the potentially more profitable but complex world of online auto auctions, and the high-effort, high-reward option of a private sale. Which one is best for you comes down to how much time and hassle you're willing to put in.

Option 1: Selling to a Local Salvage Yard

This is, hands down, the easiest and quickest way to get a totalled car off your hands. Salvage yards (you might know them as junk yards or auto wreckers) are in the business of buying wrecked cars to strip them for usable parts. They deal with this situation every day, so the process is usually very smooth.

To make sure you're getting a decent price, don't just call the first yard that pops up in a search. You need to shop around.

- Get multiple quotes. I always recommend calling at least three to five local yards. Give them the year, make, and model, and be upfront about the damage. Good, clear photos will get you a more accurate quote.

- Ask about towing. Any reputable yard should offer free towing for the car they're buying. Make sure you confirm this so you don't get hit with a surprise fee that wipes out your profit.

- Create some competition. Once you have a couple of offers, don't be afraid to play them against each other. Let Yard B know that Yard A offered you a bit more. A simple phone call like this can often add an extra $50 to $150 to your pocket.

You won't get top dollar this way, but it's a guaranteed sale with almost zero stress.

Option 2: Using an Online Auto Auction

If your car still has a lot of value—maybe it's a newer model with damage that could be repaired, or it has parts that are in high demand—an online auction could be your best bet. Websites that specialize in salvage vehicles open you up to a nationwide market of mechanics, rebuilders, and dealers who will often pay more than your local yard.

This route isn't without its own set of hurdles, though. Most of these platforms have listing fees, success fees, and other charges that come out of your final sale price. You’ll also need to put in the work to create a very detailed and honest listing, complete with high-quality photos and a full disclosure of the vehicle’s condition and salvage title. The upside is a higher sale price, but it demands more of your time and patience.

Pro Tip: When you're listing on an auction site, be brutally honest. Point out what's still in great shape (like an undamaged engine or transmission), but be completely transparent about the damage and the salvage title. This honesty builds trust and attracts serious buyers who know what they're looking at.

Option 3: Navigating a Private Sale

Selling a totalled car directly to another person can bring in the most money, but it also comes with the most risk and requires the most work on your part. Your target buyer is probably a hobby mechanic, someone looking for a project car, or a person who needs specific parts for their own vehicle.

Absolute transparency is key here. You are legally and ethically obligated to state clearly in any ad that the car has a salvage title and explain exactly what happened to it. Trying to hide this is a recipe for legal problems down the road.

Get ready for a lot of questions, some ridiculously low offers, and a few tire-kickers who don't quite grasp what a salvage title entails. You'll also be responsible for handling all the title transfer paperwork according to your state's specific rules. Plus, if you do find a buyer, you’ll likely need to arrange for specialized salvage towing services to get the vehicle to them, adding another logistical step.

In the end, selling a salvage vehicle is a trade-off between convenience and profit. By understanding these three paths, you can make an informed choice that fits your situation and turns that wrecked car into cash. Still not sure what your car is worth? Check out our guide on https://totallossnw.com/how-much-is-my-totaled-car-worth/ to get a clearer picture.

Your Top Total Loss Questions, Answered

When your car is declared a total loss, a whole new wave of questions and worries pops up. It's a confusing process, and most people have never been through it before. Feeling lost is completely normal.

Let's walk through some of the most common questions we hear from drivers, breaking down the answers so you can understand your options and move forward.

Can I Just Refuse to Let Them Total My Car?

This is probably the number one question people ask, and it comes from a place of frustration. But the short answer is no, you can't technically refuse the "total loss" label itself.

Once an insurance adjuster determines the cost to repair your car is more than its value (based on a percentage set by state law), they’re legally required to declare it a total loss. That triggers the process of issuing a salvage title.

But that doesn't mean you have no power. Your leverage isn't in fighting the declaration—it's in fighting the valuation. Pour your energy into proving their Actual Cash Value (ACV) offer is too low. That’s the part of the process where you can actually make a difference and get the money you're truly owed.

What If I Still Owe Money on the Loan?

This is where a total loss can go from bad to worse. If you have an auto loan, the insurance company isn't just going to cut you a check. That settlement money is made co-payable to you and your lender, and the bank always gets paid first.

The insurer sends the payment directly to your lender. If the settlement is more than your loan balance, you'll get a check for the leftover amount. But here’s the scary part: if you owe more on the loan than the car is worth (often called being "underwater" or "upside down"), you are on the hook for that remaining balance.

This is the exact scenario GAP (Guaranteed Asset Protection) insurance was invented for.

GAP insurance is a lifesaver. It’s designed to cover that "gap" between the insurance payout and what you still owe your lender. Without it, you could be stuck making monthly payments on a car that's sitting in a salvage yard.

How Long Is This Whole Process Going to Take?

A total loss claim is definitely not a quick affair. While you'll want it over with as soon as possible, it helps to have a realistic timeline in mind. From the day of the accident to getting the final check, you're typically looking at anywhere from a few weeks to over a month.

Here's a rough idea of the stages:

- Initial Review (1-2 weeks): This is when the adjuster inspects the vehicle, researches its value using their software, and officially declares it a total loss.

- Negotiation (1-3+ weeks): This is the biggest variable. If you take their first offer, it’s fast. But if you dispute their lowball number and start negotiating or have to invoke the appraisal clause, this can easily add several weeks to the clock.

- Finalizing Everything (1 week): Once you agree on a settlement number, it usually takes about a week to get all the paperwork signed, transfer the title over, and get the payment issued.

The best thing you can do to speed things up is to be hyper-organized and responsive. Get them any document they ask for immediately and check in regularly so your claim doesn't get buried on someone's desk.

Should I Keep Paying My Car Loan and Insurance?

Yes. 100% yes. Do not stop making payments.

Until the ink is dry, the title is transferred, and your lender confirms the loan is paid off, you absolutely must keep paying your car loan and your insurance premium.

If you stop paying your loan, you’ll get hit with late fees and wreck your credit score. If you let your insurance policy lapse, they could deny the claim entirely, leaving you with nothing. Keep everything current until you have written confirmation that the entire process is complete.

Fighting an insurance company over a lowball total loss offer is draining. You don't have to face it alone. At Total Loss Northwest, we are certified independent appraisers who step in to get you the true value of your vehicle. We invoke the Appraisal Clause in your policy, forcing a fair settlement based on real-world market data, not their internal software. Get the fair settlement you deserve by visiting us at https://totallossnw.com.