When your insurance company declares your car a "total loss," they'll make you a settlement offer. If that number feels disappointingly low, you're not stuck. You have the right to get an independent, second opinion on your car's real value, and this process is called a total loss appraisal.

Often referred to as "invoking the appraisal clause," this is your single most powerful tool for challenging a lowball offer. It ensures the payout you receive is based on your vehicle's actual market worth right before the accident, not just what the insurance company's software says it's worth.

What a Total Loss Appraisal Actually Means for You

It's a gut-wrenching moment that thousands of drivers face every year. After an accident, your insurer says your vehicle is a total loss, and their settlement offer won't even come close to buying a similar replacement. This is precisely when a total loss appraisal becomes your best move.

Think of it like selling a house. You wouldn't automatically accept the first low offer that comes in. You'd get a professional home appraisal to prove its true market value. A total loss appraisal works the exact same way for your vehicle. It’s an official, evidence-backed valuation conducted by a certified, unbiased expert who works for you, not the insurance company.

This simple step completely changes the dynamic. Instead of being stuck with a figure from the insurer’s system—which is often designed to minimize their costs—you bring an objective, expert assessment to the negotiating table.

The Power of an Independent Second Opinion

The whole point of invoking your policy's appraisal clause is to secure a fair and accurate valuation. Insurance companies typically rely on large-scale, automated valuation services that can easily miss what made your specific car special.

An independent appraiser's sole job is to find the true value that the insurer overlooked. They dive deep into your local market, account for recent upgrades, and analyze your vehicle's specific features to build a rock-solid case for its real, pre-accident worth.

Your appraiser’s report gives you the factual ammunition you need to push back against the initial low offer. It turns a "take-it-or-leave-it" ultimatum into a structured negotiation backed by hard evidence.

Insurer Valuation vs Independent Appraisal

The gap between the insurance company's first offer and an independent appraisal can be surprisingly wide. Seeing where these differences come from really highlights the value of getting your own expert involved.

Here’s a breakdown of the two approaches:

| Valuation Aspect | The Insurer's Initial Offer | Your Independent Appraisal |

|---|---|---|

| Data Source | Relies on huge, national databases and automated software. | Focuses on hyper-local market research, quotes from local dealers, and real sale listings. |

| Vehicle Condition | Often uses generic, standardized condition ratings like "average" or "clean." | Based on a detailed physical inspection and a thorough review of your maintenance history. |

| Upgrades & Options | Frequently misses or undervalues recent investments like new tires or aftermarket stereo systems. | Specifically documents and assigns value to all recent maintenance, upgrades, and desirable features. |

| Market Adjustments | May not reflect recent spikes in demand for your specific model in your geographic area. | Directly investigates and documents regional market factors that are driving your car's value up. |

Ultimately, a total loss appraisal is about making sure the final settlement reflects what it would actually cost you to go out and buy a comparable replacement car in your local market today. It's a formal process built right into your policy to protect your financial interests and make you whole again after a loss. By demanding an appraisal, you are simply using the rights you've been paying for all along.

How Insurers Decide Your Car Is a Total Loss

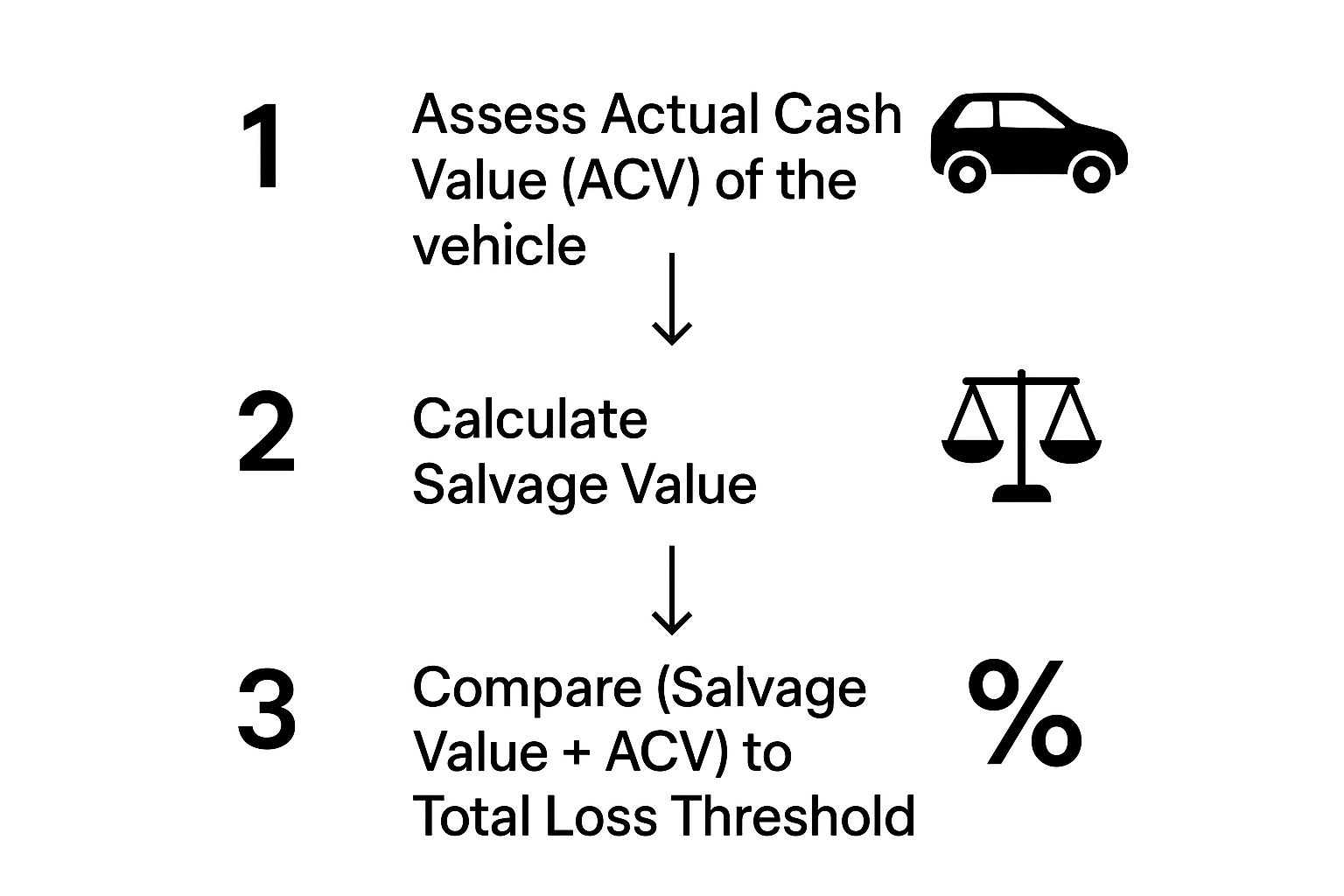

If you want to successfully challenge an insurance company's settlement offer, you first have to understand their playbook. The decision to "total" a car isn't random. It comes down to a specific financial calculation called the total loss formula.

Think of it as a simple cost-benefit analysis. The insurer compares the estimated cost to repair your vehicle to its Actual Cash Value (ACV)—what your car was worth on the open market just moments before the crash.

If the repair costs climb past a certain percentage of the ACV, the car is declared a total loss. This tipping point is called the total loss threshold, and it's dictated by state law or the insurance company's own internal guidelines.

The Key Factors in Their Calculation

The insurer’s decision isn't based on one body shop quote alone. They look at several moving parts to get a complete financial picture of your claim.

Here’s what they’re looking at:

- Estimated Repair Costs: This isn't just a ballpark figure. It includes the cost of parts, materials, and the going labor rates for body shops in your area.

- Actual Cash Value (ACV): To figure this out, they analyze your car’s make, model, year, mileage, options, and its overall condition right before the accident.

- Salvage Value: This is a big one. It's the money the insurance company expects to recoup by selling your wrecked car to a salvage yard. This potential income reduces their total payout, so it’s a critical piece of their math.

The insurer will add the repair estimate to the car's projected salvage value. If that number is higher than the ACV, it’s a clear business decision for them to total the vehicle and cut you a check. It simply costs them less. If you believe their valuation is off, you should know that the appraisal clause in your auto insurance policy gives you a powerful tool to dispute it.

How Technology and Market Trends Change the Game

Have you noticed that more cars seem to be getting totaled these days, even for what looks like fixable damage? You're not imagining things. Major shifts in automotive technology and the used car market are fundamentally changing the total loss equation.

While many insurers now use photo-based AI for quick initial estimates, the real story is economic.

In the first three quarters of 2022, total loss claims accounted for nearly 27% of all collision claims. Experts say this isn't because of AI estimating tools, but because soaring new and used vehicle prices have completely upended the value equation for repairs.

When the market value of used cars skyrockets, the math changes. A car that would have been repaired just a few years ago is now a prime candidate for a total loss because its higher ACV makes the repair-cost-to-value ratio much tighter. Understanding this gives you a crucial insight into the insurer's mindset and helps you build a stronger case for a fair settlement.

Your Step-by-Step Guide to Demanding an Appraisal

So, you've looked at your insurance company's total loss settlement offer and know it's too low. It's time to act. This doesn't mean getting into a shouting match over the phone; it means formally using a powerful tool built right into your insurance policy—the appraisal clause. This process takes the decision out of the hands of the insurer's adjuster and puts it into the hands of neutral experts.

Feeling a bit lost? Don't be. We're going to walk through the entire process in four straightforward, manageable steps. Think of this as your game plan for challenging a lowball offer and getting the fair value you're actually owed.

Step 1: Formally Notify Your Insurer in Writing

First things first, you have to make it official. You must tell your insurance company, in writing, that you dispute their valuation and are formally demanding an appraisal as outlined in your policy. A simple phone call just won't cut it.

Putting it in writing creates a legal paper trail and officially gets the ball rolling. Your letter should be professional and straight to the point.

Expert Tip: Don't just say you disagree. Your letter needs to use specific language. Explicitly state that you "dispute the Actual Cash Value" and are "invoking the appraisal clause" or "demanding an appraisal." This specific phrasing triggers their contractual obligation to move forward.

Make sure you send this letter via certified mail with a return receipt requested. This gives you undeniable proof of the date they received your demand, which is critical for holding them to the timelines in this process.

Step 2: Select Your Independent Appraiser

Now, you need to find your expert. The next move is to hire a qualified, unbiased, and independent appraiser who will represent your side of the dispute. This is probably the single most important decision you'll make.

Your appraiser’s job is to dig deep and conduct a thorough, evidence-based valuation of your vehicle to determine what it was truly worth right before the accident. They will build the factual case that dismantles the insurer's low offer.

So, what makes a great appraiser?

- Credentials and Experience: Look for professionals with recognized certifications and a proven history of handling total loss and diminished value claims specifically.

- Local Market Knowledge: An appraiser who knows your local area inside and out will find much more accurate and relevant "comps" (comparable vehicles for sale).

- No Conflicts of Interest: Make absolutely sure they work for policyholders, not for insurance companies. You need someone who is 100% on your team.

Step 3: Navigate the Exchange of Reports

Once you've hired your appraiser, they'll get to work. They will meticulously inspect your vehicle (if possible), review all your documentation, research your local market, and compile a detailed valuation report. This report is your key piece of evidence.

Your appraiser then sends this report over to the insurance company's appraiser. The two experts will look over each other’s work, compare their data, and start negotiating to land on a fair value. A seasoned appraiser knows exactly how to defend their numbers and poke holes in the insurer's often flawed assessment.

The image below gives you a simplified look at how the value is assessed—the very process at the heart of the appraisal dispute.

This flowchart shows the basic financial logic your insurer uses. Your appraiser's job is to challenge it with more accurate, real-world data from your specific market.

Step 4: Understand the Role of an Umpire

But what if the two appraisers—yours and the insurer's—just can't see eye to eye on a final number? This is where the last piece of the puzzle, a neutral umpire, comes into play.

An umpire is an impartial, third-party appraiser brought in specifically to break the deadlock. Both your appraiser and the insurer's appraiser will present their reports and make their case to the umpire.

The umpire then reviews all the evidence and makes a final call. The process is designed for resolution: if any two of the three parties (your appraiser, the insurer's appraiser, or the umpire) agree on a value, that amount becomes the final, binding settlement. This structured system prevents an endless stalemate and ensures your claim reaches a fair conclusion.

Uncovering Your Vehicle’s Hidden Value

An insurance company’s valuation report often just scratches the surface. It’s built on generic data from a database that can't possibly capture the unique story and condition of your specific vehicle. If you want a fair settlement, you have to prove what your car was truly worth right before the accident. That means digging into the details the insurer almost always overlooks.

A professional total loss appraisal goes way beyond the basic make, model, year, and mileage. It's an investigation into your car’s hidden value—the kind of value that only comes from dedicated ownership, meticulous care, and smart investments.

Think of it like this: two identical houses on the same street can have wildly different sale prices. One might be a bit run-down, while the other has a brand-new kitchen, a recently replaced roof, and perfect landscaping. It’s the same exact principle with your car. Your appraiser’s job is to find and document your vehicle’s "new kitchen" and "landscaping."

Beyond the Basics: What Appraisers Look For

An independent appraiser’s report is built on a foundation of solid proof. They meticulously analyze every single element that contributes to your car’s pre-accident Actual Cash Value (ACV). This detailed approach is what gives you the leverage you need to counter the insurer's low offer.

Here are the key areas where that hidden value is most often found:

- Detailed Maintenance History: A thick folder of receipts showing consistent oil changes, scheduled services, and preventative maintenance is powerful evidence. It proves your car was in superior mechanical condition, which directly increases its value over a similar car with no service history.

- Recent Upgrades and Repairs: Did you install new tires three months ago? What about a new battery, brakes, or a high-end stereo system? These are real, dollars-and-cents investments that add quantifiable value, and they absolutely must be accounted for.

- Desirable Factory Options: Premium packages, a sunroof, upgraded wheels, or a high-performance engine all make your car more valuable than a base model. Appraisers ensure these features are properly identified and valued, not just lumped into a standard trim level.

A common mistake is thinking only major upgrades matter. The truth is, even small, recent investments add up. A car with $1,500 in new tires and brakes is demonstrably worth more than an identical one that needs those items replaced.

The Impact of Modern Technology and Market Forces

The automotive world is changing fast, and these shifts have a direct impact on your total loss appraisal. Recent global trends have driven the price of used cars sky-high, while new technologies have made even basic repairs far more expensive.

Supply chain disruptions and inflation have increased the market value of most used cars, and that higher value should be reflected in your settlement. At the same time, the complex sensors, cameras, and computers in Advanced Driver Assistance Systems (ADAS) make even minor fender-benders incredibly costly to fix. This is pushing more vehicles past the total loss threshold.

This reality makes an accurate pre-accident valuation more important than ever. If your car was in excellent shape, that high standard of condition is a critical factor in determining its true worth. You can get a clearer picture of this by exploring our guide on how to figure out what your totaled car is worth.

Proving Your Car’s Superior Condition

Your appraiser will build the case, but you’re the one who provides the initial evidence. The more documentation you can hand over, the stronger your claim will be.

Start gathering this information as soon as you can:

- Service Records: Collect every receipt you can find, from oil changes and tire rotations to major scheduled services.

- Repair Invoices: Dig up receipts for any recent work, like new brakes, a new alternator, or transmission service.

- Purchase Receipts for Upgrades: Did you add a remote starter, a new sound system, or custom wheels? Find those receipts.

- Original Window Sticker: If you still have it, the window sticker is the best proof of all the factory-installed options your car came with.

By focusing on these hidden value factors, you and your appraiser can build an undeniable, evidence-based report. This shifts the negotiation from being about the insurer’s lowball estimate to a factual discussion about your vehicle’s real, pre-accident market value.

Strategies to Maximize Your Settlement Offer

Knowing your car’s true value is one thing; getting the insurance company to actually pay it is another. To turn that knowledge into a bigger check, you need to get organized and be proactive. You can't just tell the adjuster your car was in fantastic shape—you have to prove it with hard evidence they can't ignore.

This is where you shift from being a passive recipient of their offer to building a rock-solid case for what your vehicle was really worth. By gathering the right paperwork and doing a little homework on your local market, you can confidently push back against their initial lowball number and take the reins of the negotiation.

Create Your Vehicle’s "Brag Book"

Your single most effective tool is a complete and detailed record of your car's life. I like to call this a "brag book"—a file that showcases every dollar and every bit of care you invested in that vehicle. This file will become the undeniable foundation of your independent total loss appraisal.

Your mission is to gather every receipt and invoice related to your car’s maintenance and upgrades.

- Maintenance Receipts: Every oil change, tire rotation, and fluid flush demonstrates meticulous upkeep.

- Major Repairs: Got receipts for new brakes, a timing belt replacement, or a rebuilt transmission? These are proof of major value you’ve recently added.

- Recent Upgrades: Did you install new tires six months ago? What about a new battery, premium sound system, or a remote starter? These all have a direct, provable cash value.

Putting this documentation together transforms your claim from a simple opinion ("My car was in great shape!") into a factual, evidence-based argument ("My car was worth more, and here are the receipts to prove it.").

The insurance company's valuation software has no idea you spent $1,200 on top-of-the-line all-season tires last fall. Your brag book makes that hidden value impossible to overlook.

Find Your Own Comparable Vehicles

The insurance company will send you a list of "comparable" vehicles, or "comps," that they claim justify their valuation. Don't just accept it. More often than not, these comps are located hundreds of miles away, are in visibly worse condition, or are base models that lack your car's desirable features. Your job is to fight back with your own, more accurate market research.

Get online and search for vehicles for sale that are genuinely like-for-like in your local area. You’re looking for listings that match your car’s:

- Exact Year, Make, and Model: No substitutions here.

- Trim Level and Options: An EX-L is worth more than an LX. Make sure the comps reflect your car's specific package.

- Mileage: Find examples with mileage as close to yours as possible.

- Local Market: Stick to listings within a 50-75 mile radius. Car values in Seattle are different from those in rural Idaho.

When you present these real-world listings to the insurance adjuster or your appraiser, you’re providing a powerful counter-narrative to their lowball comps. This is an absolutely essential step in any successful total loss settlement negotiation.

Avoid These Common and Costly Mistakes

In the chaos following an accident, it’s all too easy to make a simple mistake that can cost you thousands. Stay sharp and watch out for these common traps.

First and foremost, do not cash the check the insurance company initially sends you. Cashing or depositing that first check is often legally considered an acceptance of their offer, which could close your claim for good.

Second, be extremely cautious about giving a recorded statement. You're not required to give one on the spot. It's always better to take your time, speak with your appraiser first, and be fully prepared before you agree to have your conversation recorded.

Finally, never assume an older car has little value. This is more true today than ever. The average age of vehicles on U.S. roads has hit a record 12.6 years, and market values for total loss vehicles are running about 8.5% higher than historical trends. This data proves that well-maintained older cars hold significant value—a powerful fact you can use to your advantage if you have the documents to back up its condition.

Navigating the Final Stages of Your Appraisal

https://www.youtube.com/embed/Qsm3ue3sS58

You’ve done the hard part. You've officially challenged the insurance company's lowball offer and hired an independent appraiser who has submitted a thorough valuation report. This is the endgame, where all that careful documentation and standing your ground really starts to pay off.

Now, your appraiser and the one hired by the insurance company will exchange their reports and the real negotiations begin. This is where you'll see the value of having a seasoned professional in your corner. They'll go to bat for their valuation, systematically dismantling the insurer's assessment and pushing for a fair, agreeable settlement.

In most cases, this back-and-forth between the two experts is all it takes. They find common ground, land on a new, higher value for your vehicle, and the claim moves toward a final payment.

How the Process Concludes

But what if they can't agree? The appraisal process has a built-in "tie-breaker" to prevent your claim from getting stuck in an endless loop. This final stage typically unfolds in one of three ways, guaranteeing a resolution.

Here are the most common paths to a final settlement:

-

Direct Agreement: This is the best-case scenario and the most frequent outcome. Your appraiser and the insurer's appraiser negotiate a final, binding settlement amount. It's the cleanest and quickest way to wrap things up.

-

Umpire Decision: If the two appraisers hit a brick wall and just can't agree, they bring in a neutral, third-party umpire. The umpire reviews both appraisal reports and makes an independent decision. Once any two of the three parties—your appraiser, the insurer's appraiser, or the umpire—agree on a value, that number becomes the binding settlement.

-

Finalizing the Settlement: As soon as a binding value is set, whether through direct agreement or an umpire's decision, the claim is officially finalized. This isn't just a suggestion; it's the final amount the insurance company is legally obligated to pay.

This structured process is your safety net. It takes away the insurance company's power to just say "no" and forces a conclusion based on evidence and the judgment of qualified experts. It's designed to level the playing field.

Understanding the Final Payout

Once that settlement value is locked in, the insurance company will issue the payment. It’s crucial to know how this money is handled, particularly if you still have a loan on the vehicle.

The process is pretty straightforward. First, the insurance company pays off your lender to clear the remaining balance on your auto loan.

After the lender is paid in full, any leftover funds from the settlement are sent directly to you. For example, if the final settlement is $25,000 and you still owe $10,000 on your car loan, the lender gets their $10,000, and you get a check for the remaining $15,000.

Frequently Asked Questions About Total Loss

Even when you know the steps, navigating a total loss claim can feel like walking through a minefield. You're bound to have questions pop up along the way. I've gathered some of the most common ones I hear from policyholders to give you clear, straightforward answers so you can challenge your insurer’s offer with confidence.

How Much Does an Independent Appraiser Cost?

You can expect to pay between $300 and $600 to hire a qualified independent appraiser for a total loss claim. The exact cost often depends on a few things, like their years of experience, how complex your vehicle's valuation is, and even where you're located.

It’s easy to hesitate at an upfront cost, but it's better to think of it as an investment. Paying a few hundred dollars to potentially get thousands more in your final settlement is a smart move. It stops you from leaving money on the table that is rightfully yours.

Can I Demand an Appraisal if I Was At Fault?

Yes, absolutely. The right to demand an appraisal is baked into your insurance policy. It's a contractual right that applies to claims you make against your own collision or comprehensive coverage.

Fault has nothing to do with it. The appraisal clause is purely about determining the Actual Cash Value (ACV) of your vehicle. It’s a mechanism to ensure you get paid what your car was worth, based on the policy you’ve been paying for.

This protection exists to guarantee a fair valuation, no matter who caused the accident. The entire focus is on getting the numbers right for your property.

What if the Appraisal Value Is Lower Than the Offer?

Honestly, this is extremely rare if you've done your homework and hired a reputable appraiser who only works for policyholders, not insurance companies. A true professional's entire job is to dig into the data and find the evidence that supports your car's real market value.

Most good appraisers will look over your case first and tell you upfront if they don't think they can get you more money. But it's important to know that in most states, the final appraisal award is binding on both you and the insurance company.

This is exactly why choosing the right appraiser is so important. A good one won't take your case unless they're confident they can build a rock-solid argument for a higher settlement, which makes a lower valuation a very unlikely outcome.

Are you dealing with a lowball total loss offer in Washington or Oregon? Don't accept a settlement that doesn't reflect your vehicle's true worth. The certified experts at Total Loss Northwest are here to fight for you. We invoke the appraisal clause on your behalf to secure the fair, accurate settlement you deserve. Get a professional on your side by visiting totallossnw.com today.