Before we jump into the numbers and talk about the actual auto appraisal cost, let's first get a handle on why you’d ever need one in the first place. Think of it this way: a professional appraisal is your official, defensible proof of value. It carries far more weight than any free online estimate, especially when there's serious money at stake.

Why You Might Need a Professional Car Appraisal

A professional auto appraisal is a lot like a home appraisal, but for your car. It’s a formal, in-depth process where a certified expert meticulously inspects your vehicle, dives deep into market research, and prepares a comprehensive report. This document is your best leverage in any situation where a ballpark guess simply won’t do the job.

The most frequent reason people seek out an appraiser is for an insurance claim. Whether you’re staring down a frustratingly low offer for a totaled vehicle or fighting for diminished value after an accident, a certified appraisal provides the concrete evidence you need to push back against the insurance company's numbers.

Common Scenarios Requiring a Professional Auto Appraisal

While insurance disputes are common, they're far from the only reason to get a professional valuation. Several other high-stakes situations make an appraisal not just a good idea, but an absolute necessity.

The table below outlines some of the most frequent scenarios that call for an expert's opinion.

| Scenario | Primary Purpose of Appraisal | Who Typically Pays |

|---|---|---|

| Insurance Total Loss | To challenge a low settlement offer from the insurer. | The vehicle owner |

| Diminished Value Claim | To prove the vehicle's loss in value after accident repairs. | The vehicle owner (claimant) |

| Classic/Custom Car Sale | To establish and justify a high asking price for a unique vehicle. | The seller |

| Divorce/Estate Settlement | To determine a fair, unbiased value for asset division. | The estate or parties involved |

| Charitable Donation | To substantiate the vehicle's value for an IRS tax deduction. | The donor |

| Securing a Loan | To verify the vehicle's worth as collateral for a lender. | The borrower |

As you can see, the core purpose is always to establish a credible, documented value that can stand up to scrutiny, whether from an insurance adjuster, a potential buyer, or even the IRS.

Market Trends and the Growing Need for Appraisals

The current car market has made accurate appraisals more crucial than ever. We've all seen vehicle prices climb due to inflation and supply chain headaches. This has a strange side effect: even moderately damaged cars are now frequently declared total losses.

Why? Because modern vehicles are packed with expensive technology like cameras, sensors, and advanced driver-assistance systems. The cost to repair these complex components can easily surpass the car's (already inflated) market value. The auto appraisal cost has adapted to this new reality, as appraisers must now evaluate not just the sheet metal, but also the sophisticated tech inside. If you want to dig deeper, you can explore how market trends affect total loss appraisals to get a better sense of this shift.

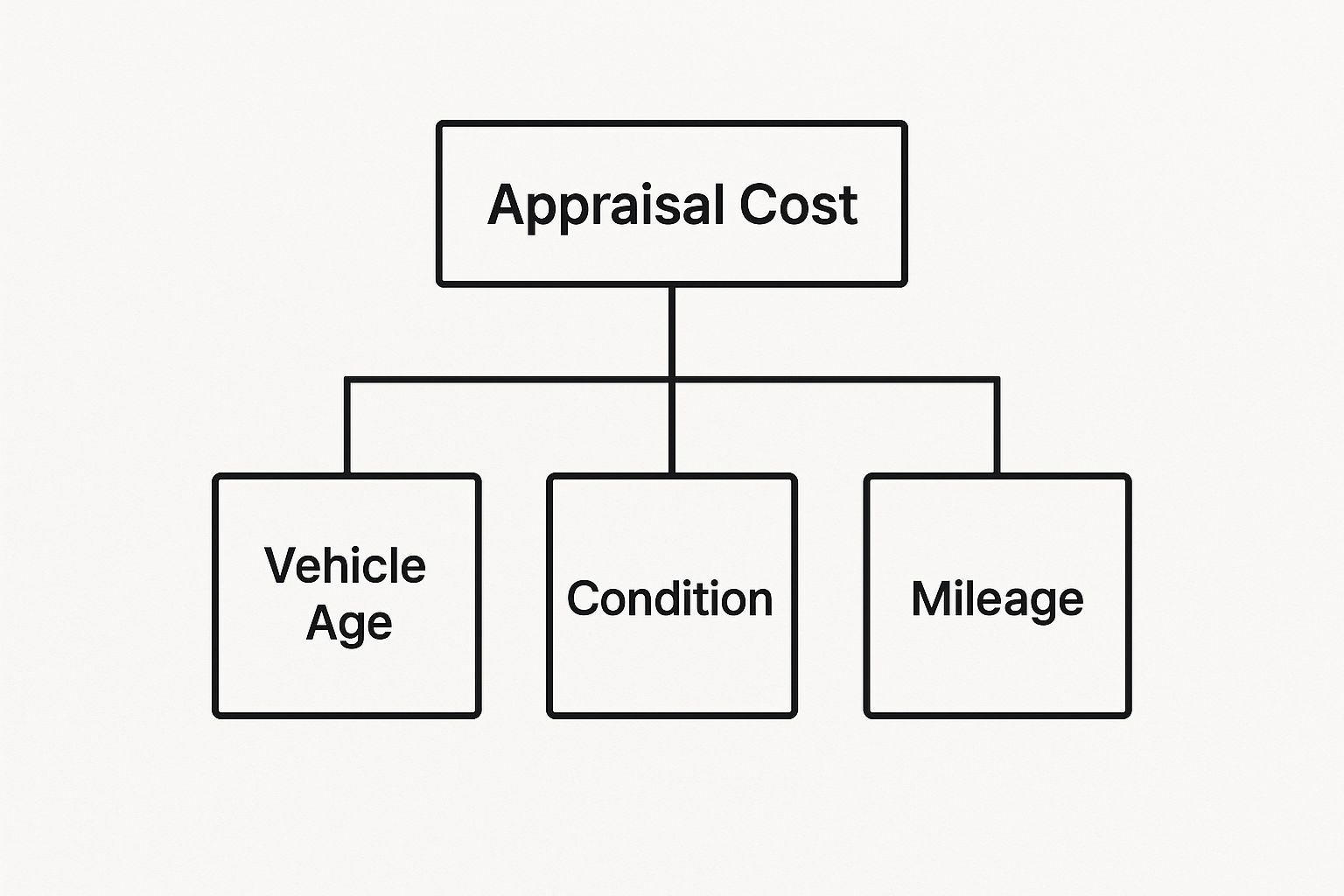

The Key Factors That Determine Appraisal Costs

Thinking about an auto appraisal cost as one single price is like asking a contractor for a quote without saying if you have a leaky faucet or need a new roof. The final bill really depends on the job at hand, and a few key things will determine just how much work is involved. There’s no simple, one-size-fits-all price tag because every car—and every situation—is different.

The biggest driver of the cost is the type of appraisal you actually need. A basic report for a common car involved in a total loss dispute is much simpler than a diminished value claim. The latter requires an appraiser to prove a very specific drop in market value after repairs, which takes more digging. Appraising a rare, numbers-matching classic car for an auction? That’s a whole other ballgame, demanding deep-dive historical research and authentication.

This image breaks down the core elements that directly affect an appraiser's workload and, ultimately, your cost.

As you can see, the vehicle's age, its overall condition, and the mileage on the odometer are the starting points for figuring out its value and how complex the appraisal will be.

Vehicle Complexity and Condition

Beyond just the purpose of the appraisal, the car itself is a huge factor. A stock 2022 Honda Accord is pretty straightforward; there's plenty of market data out there. But what about a heavily customized 1970 Ford Bronco with a modern engine swap, a lift kit, and a brand-new interior? That’s a much tougher puzzle to solve. Each of those custom parts has to be valued one by one.

The car's condition is just as critical. A pristine, show-quality vehicle needs a very different kind of inspection than one that's been wrecked. For a damaged car, the appraiser has to meticulously document every dent, scratch, and broken part. This step is essential when figuring out how much your totaled car is worth and backing up the final number.

Key Insight: The more unique, rare, or modified a vehicle is, the more time and expertise it takes to research the market and build a rock-solid report. That specialized labor is what you're paying for in the final appraisal cost.

Location and Appraiser Credentials

Finally, a couple of outside factors can nudge the price up or down:

- Geographic Location: Like any professional service, rates change depending on where you are. An appraisal in a big city like Seattle will likely cost more than one in a small, rural town, simply because of higher business costs.

- Appraiser Credentials: Experience costs money, and for good reason. A veteran, certified appraiser with credentials from an organization like the I-AAA (Independent Auto Appraisers Association) will probably charge more than someone new to the field. What you get for that higher fee is a more detailed, persuasive, and bulletproof report that insurance companies and courts take seriously. You're not just paying for a piece of paper; you're paying for their expertise and reputation.

What to Expect for Your Auto Appraisal Cost

Alright, now that we’ve covered the factors that can influence the price, let's get down to the real numbers. The auto appraisal cost isn't a simple, one-size-fits-all fee. It really depends on how much work is involved and what you need the report for. Knowing the typical price ranges helps you budget for the service and spot a fair deal when you see one.

Think of it like hiring a contractor for a home project. A simple paint job in one room is going to cost a lot less than a full kitchen remodel. In the same way, a basic appraisal for a common car is a different ballgame than a deep-dive report needed for a rare or custom vehicle. The time, research, and documentation required for each are worlds apart.

Standard and Total Loss Appraisals

For most people, the need for an appraisal pops up during an insurance claim, especially when their car has been declared a total loss. If your insurance company’s settlement offer feels insultingly low, a certified appraisal is your best bet for fighting back. This report is all about pinpointing your vehicle’s true market value right before the accident happened.

- Typical Cost Range: $300 to $650

- What It Includes: A hands-on inspection of the vehicle (or a detailed review of photos if you can't get to it), a careful look at the insurer's lowball valuation, and a thorough market analysis using real, comparable vehicle sales.

- Best For: Disputing an insurance settlement for your everyday car, truck, or SUV.

Getting an independent appraisal is usually the first move you’ll make when invoking the appraisal clause in your policy. This is the official step that gets the ball rolling. To get a better handle on this, you can learn more about how a total loss appraisal works to secure a fair settlement. In short, the report gives you the solid evidence needed to counter the insurer’s initial offer.

Diminished Value and Complex Reports

A diminished value appraisal is a more specialized beast. Its job is to calculate how much your car's market value has dropped after it's been in a wreck and repaired. This is trickier because the appraiser doesn't just need to know the car's value; they have to prove a specific financial loss caused by its accident history.

Likewise, appraising classic, custom, or exotic cars is in another league entirely. These valuations demand serious historical research, verifying original parts and aftermarket modifications, and digging into a niche market with far fewer comparable sales to go on.

Key Takeaway: The more research and justification an appraiser needs to prove a specific value—whether for a diminished value claim or a rare classic car—the more you can expect the appraisal fee to be.

To help you get a clearer picture, here’s a quick comparison of what to expect for your auto appraisal cost across different services.

Estimated Auto Appraisal Costs by Service Type

This table breaks down the typical price ranges for different types of auto appraisals, helping you understand what to expect based on your specific needs.

| Appraisal Type | Typical Cost Range | Best For |

|---|---|---|

| Standard / Total Loss | $300 – $650 | Daily driver insurance disputes. |

| Diminished Value | $400 – $850+ | Proving post-repair value loss. |

| Classic / Exotic / Custom | $600 – $1,500+ | Sales, insurance, or legal needs for unique vehicles. |

These price ranges should give you a solid baseline for what your auto appraisal cost might look like. No matter what, always ask for a detailed quote upfront. That way, you know exactly what you’re paying for and there are no surprises down the road.

How Your Vehicle’s Details Affect the Final Price

While the type of appraisal sets the baseline, the vehicle itself is easily the biggest factor driving the final auto appraisal cost. Every car has its own story, and its unique details dictate the amount of time, research, and expertise needed to nail down its true value. There's simply no such thing as a one-size-fits-all price in this line of work.

Think about it this way. Appraising a three-year-old family SUV is fairly straightforward. There’s plenty of market data, finding comparable sales is easy, and its features are all standard. That means the process is relatively quick and, as a result, less expensive.

Now, let's swap that SUV for a numbers-matching 1969 Chevrolet Camaro SS. This isn't just a car; it's a rolling piece of automotive history. An appraiser has to do some serious detective work: verifying engine and transmission serial numbers, digging into its specific production history, and hunting down auction results for other incredibly rare examples. This kind of deep dive takes a lot more time and specialized knowledge, which naturally pushes the cost up.

The Impact of Modifications and Condition

Customizations add another wrinkle. A simple lift kit on a truck or a set of aftermarket wheels means the appraiser needs to accurately value those specific parts. But what about a full engine swap or a completely custom-built interior? That vehicle is now a one-of-a-kind asset, demanding a far more detailed and time-consuming valuation.

A vehicle’s condition is just as important. A pristine, garage-kept classic ready for a car show needs a meticulous inspection focused on originality and perfection. On the flip side, a car that's been declared a total loss requires a different kind of detailed review. In that case, the appraiser has to document every single point of damage to firmly establish the pre-accident value and support the insurance company’s total loss decision.

The Rule of Thumb: The more unique, customized, rare, or damaged a vehicle is, the more labor-intensive the appraisal becomes. This specialized work is directly reflected in the final cost.

This is also where depreciation comes into play. For example, some full-size vans can depreciate by around 19.8% each year, whereas certain mid-size cars might only see a 9.4% drop. When an appraiser is assessing a total loss, a vehicle with a higher depreciation rate will have a lower pre-accident value, which can affect the complexity of the appraisal needed to justify a settlement. You can discover more insights about how depreciation rates affect valuations on diminishedvalueofgeorgia.com.

How to Find a Reputable Appraiser and Avoid Hidden Fees

Understanding the "what" and "why" behind appraisal costs is one thing, but finding the right professional is where the rubber really meets the road. Picking a qualified, trustworthy appraiser is the single most important step in making sure your auto appraisal cost is a smart investment, not just another bill to pay.

The whole point is to get a report that insurance companies, courts, or serious buyers will actually respect. After all, a poorly researched appraisal isn't worth the paper it’s printed on.

Vetting Your Potential Appraiser

First things first: look for credentials. A true professional will be certified by a recognized organization, which tells you they’re committed to high ethical and professional standards.

Think of it as a checklist for your peace of mind:

- Key Certifications: Are they affiliated with reputable groups? Look for names like the I-AAA (Independent Auto Appraisers Association) or the ASA (American Society of Appraisers).

- Relevant Experience: You don't want a classic car specialist for your totaled daily driver. Make sure they have direct experience with your specific situation (like total loss or diminished value) and your type of vehicle.

- Verifiable Reviews: Go beyond their website testimonials. Check independent reviews on Google or Yelp to see what real clients have to say, especially about how the appraiser handled tough negotiations with insurance companies.

Doing this homework upfront helps you weed out the amateurs and narrow your search to seasoned pros who can produce a solid, defensible report.

Uncovering Hidden Fees and Ensuring Transparency

Once you have a shortlist, it's time to talk numbers. Any ethical appraiser will be upfront about their fee structure, but it’s on you to ask the right questions to make sure there are no surprises down the line.

A clear, itemized quote is the hallmark of a professional. If an appraiser gets cagey about costs or won't put anything in writing, that’s a massive red flag.

Before you commit to anything, get clear answers to these questions:

- Is the quote all-inclusive? Ask them straight up: "Does this price cover the physical inspection, all the market research, and preparing the final report?"

- Are there travel expenses? If the appraiser needs to come to you, find out if that travel time is built into the quote or if it will be a separate line item on the invoice.

- What about extra fees? Ask about potential add-on charges. Things like appearing in court or spending significant time on the phone with an insurance adjuster often come at an extra hourly rate.

Knowing exactly what you're paying for is empowering. This is especially true when you're battling an insurance company. For a deeper dive into that process, check out our guide to a fair total loss appraisal. It’ll help you hire the right expert and understand every dollar you spend.

So, you've seen what goes into the cost of an auto appraisal. Now for the real question: is it actually worth the money?

It’s easy to get hung up on the upfront fee. But experienced owners know to look at it differently. An appraisal isn't just another bill; it's an investment in protecting your car's real, provable value. Think of it as your financial ace in the hole.

Shifting from Expense to Advantage

Here's a scenario that plays out all the time. Your insurance company offers you $16,000 after your car is declared a total loss. Your gut tells you that’s way too low, so you spend $500 on a certified appraisal. The appraiser dives deep, pulls the data, and builds a rock-solid report showing your car was actually worth $20,000 before the accident.

Just like that, your $500 investment put an extra $3,500 back in your pocket. Suddenly, that initial fee doesn't seem like a big deal at all.

The Payoff: A professional appraisal report is your best defense against a lowball offer. It changes the entire conversation, whether you're dealing with an insurance adjuster, a private buyer, or even arguing a case in court. It replaces emotional claims with hard facts.

The Power of Proof

This isn't about getting a simple second opinion. It's about showing up with a credible, documented case. An insurance adjuster can easily brush off what you feel your car is worth. What they can't ignore is a detailed report from a certified professional who has meticulously documented market data, comparable sales, and your vehicle's specific condition.

This kind of proof is more important than ever. The vehicle market is constantly shifting. For example, strong new-car sales often mean the used car market gets flooded with newer, higher-value models. This, along with increasingly complex vehicle technology, drives values up and makes appraisals even more nuanced. You can review recent automotive sales forecasts and their impact to see how these trends affect what cars are worth.

At the end of the day, an appraisal is about getting what you're rightfully owed. Whether you’re fighting for a fair total loss payout, proving diminished value after a wreck, or setting the price for a rare classic, that upfront cost is almost always a small price to pay for a much bigger financial win. It’s a smart, calculated move to make sure you don't leave money on the table.

Common Questions We Hear About Auto Appraisals

It's completely normal to have questions about getting your car appraised. Most people don't go through this process every day, so a little uncertainty is expected. Let's walk through some of the most common questions we get and give you clear, straightforward answers.

What's the Real Difference Between a Free Estimate and a Paid Appraisal?

Think of a free online estimate as a quick snapshot. It’s an automated guess based on very basic data—your car's make, model, year, and mileage. It's handy for getting a rough idea of what your car might be worth, but it won't hold up in a serious negotiation or legal dispute.

A paid, professional appraisal is a different beast entirely. It's a meticulous, legally defensible valuation. A real expert physically inspects your vehicle or pores over detailed photos, conducts deep research into actual comparable sales in your market, and then builds a comprehensive report. This is the document you need when you're challenging an insurance company's lowball offer or need to justify a specific price.

Key Difference: A free estimate is a suggestion. A paid appraisal is a substantiated, expert valuation designed to stand up to scrutiny. The auto appraisal cost is what pays for the expertise, research, and documentation needed to prove your vehicle's true worth.

Who Foots the Bill for the Appraisal in an Insurance Dispute?

This is a big point of confusion for many people. In nearly every situation, you, as the vehicle owner, are responsible for paying for your own independent appraisal. When you use the "appraisal clause" in your insurance policy, you hire your expert, and the insurance company hires theirs.

If those two appraisers can't reach an agreement on the value, they'll bring in a neutral third-party umpire to make the final call. The cost for that umpire is usually split between you and your insurer. But that initial investment in your own appraiser comes out of your pocket.

How Long Does a Professional Auto Appraisal Take?

The timeline can shift a bit depending on how complex your situation is, but here’s a general idea of what to expect from start to finish.

- The Inspection: The hands-on part, where the appraiser looks over your vehicle, typically takes about 30 to 60 minutes.

- The Research & Report: This is where the real work happens. The appraiser will spend several hours digging into comparable sales data and writing the detailed report. This part usually takes 2 to 5 business days.

- Final Delivery: All in, you should expect to have the final, comprehensive appraisal report in your hands within about a week of the initial inspection.

This schedule gives the appraiser the time they need to build a rock-solid, well-supported case for your vehicle's actual value.

When an insurance company's offer doesn't reflect your vehicle's true worth, you need an expert in your corner. At Total Loss Northwest, we provide certified, independent auto appraisals that stand up to scrutiny. We fight to get you the fair settlement you deserve. Don't leave money on the table—contact us today to protect your investment.