It’s a frustrating reality for any car owner: even after the best body shop performs flawless repairs, your vehicle is worth less than it was a moment before the crash. Why? Because it now has an accident on its record.

This loss is called diminished value, and it represents the very real, provable difference between your car's market value before the accident and its new, lower value after. The good news is you are legally entitled to be compensated for this financial hit.

What Is Diminished Value and Why Does It Matter?

Let's try a quick thought experiment. You're in the market for a used SUV and you’ve narrowed it down to two identical options. They’re the same make, model, year, and have nearly the same mileage. One has a squeaky-clean vehicle history report, but the other shows it was in a major collision that was professionally repaired.

Which one are you buying? And more to the point, if you did consider the one with the accident history, you’d expect a steep discount, right?

That discount—that gap in price—is the core of what diminished value is all about. It's the market's natural reaction. A vehicle with a permanent blemish on its record is simply less desirable than one without. Even with state-of-the-art repairs that make it look and drive perfectly, the stigma of that accident is forever tied to the vehicle's history via its VIN.

The Three Types of Diminished Value

Diminished value isn't just one broad concept; it breaks down into three distinct categories. Understanding which type applies to your situation is key to building a strong claim.

Here's a simple breakdown of each type:

| Type of Diminished Value | What It Means for You |

|---|---|

| Immediate Diminished Value | This is the loss of value that happens the instant the collision occurs, even before any repairs have been made. It’s the difference between the car's pre-accident value and its post-accident, damaged value. |

| Repair-Related Diminished Value | This refers to any additional loss in value resulting from imperfect repairs. This could be anything from mismatched paint and poor part alignment to lingering mechanical issues. |

| Inherent Diminished Value | This is the most common and crucial type. It’s the automatic loss in resale value simply because the vehicle now has an accident history, even if the repairs were absolutely perfect. This is the value you’re typically claiming from the at-fault party's insurance. |

Most claims focus on inherent diminished value because it's a loss that exists no matter how great the repair job was. It’s the permanent financial damage you’ve suffered.

The Right to Be "Made Whole"

When another driver causes an accident, their insurance company is legally required to "make you whole." This principle isn't just about paying for the bodywork. It's about restoring you to the exact financial position you held moments before the crash.

Since the accident directly slashed your car's resale value, that loss is part of the damage you sustained.

At its heart, this is about fairness. You shouldn't be left financially worse off because of someone else's mistake. Being "made whole" means the at-fault party is responsible for both fixing the physical damage and compensating you for the drop in market value.

Why You'll Get Pushback From Insurance Companies

Despite this being a well-established legal concept, getting paid for diminished value is almost always a battle. Insurance adjusters are trained to minimize claim payouts, and their default response is often to deny it exists.

They might tell you they "don't pay for that" or claim that once the car is repaired, its value is fully restored. They're banking on the hope that you don't know your rights or won't bother to fight back.

Understanding that this pushback is part of their playbook is the first step. The financial loss from diminished value is real, and it can range from a few hundred dollars to tens of thousands depending on your car's value and the extent of the damage. For most people, walking away from this claim is like leaving a pile of your own cash on the table.

The Three Kinds of Diminished Value: What You're Really Losing

When you hear the term “diminished value,” it’s easy to think of it as one lump sum of money you’ve lost. But in reality, it’s more nuanced than that. The loss your car suffers breaks down into three specific types, and knowing the difference is your first step toward building a solid claim.

Think of it like a doctor figuring out what's wrong. They don't just say you're "sick"; they diagnose the specific issue to give you the right treatment. In the same way, pinpointing the exact type of diminished value you're dealing with helps you demand the right compensation from the insurance company.

Inherent Diminished Value: The Unavoidable Loss

This is the big one. Inherent Diminished Value (IDV) is the automatic drop in your car’s resale price just because it now has an accident on its record. It doesn't matter if the best body shop in the world made it look brand new—the stigma of being in a crash sticks.

Picture two identical cars for sale. One has a clean vehicle history report, but the other shows a "collision repair" entry. Which one do you think will sell for less? The one with the accident history, every single time. That difference in price is its inherent diminished value. It's a permanent financial scar that has nothing to do with the quality of the repairs.

This loss isn't trivial. A vehicle's value can drop by as much as 30% after an accident, even with flawless repairs, purely because of this market perception. This is a direct financial hit caused by the other driver's negligence.

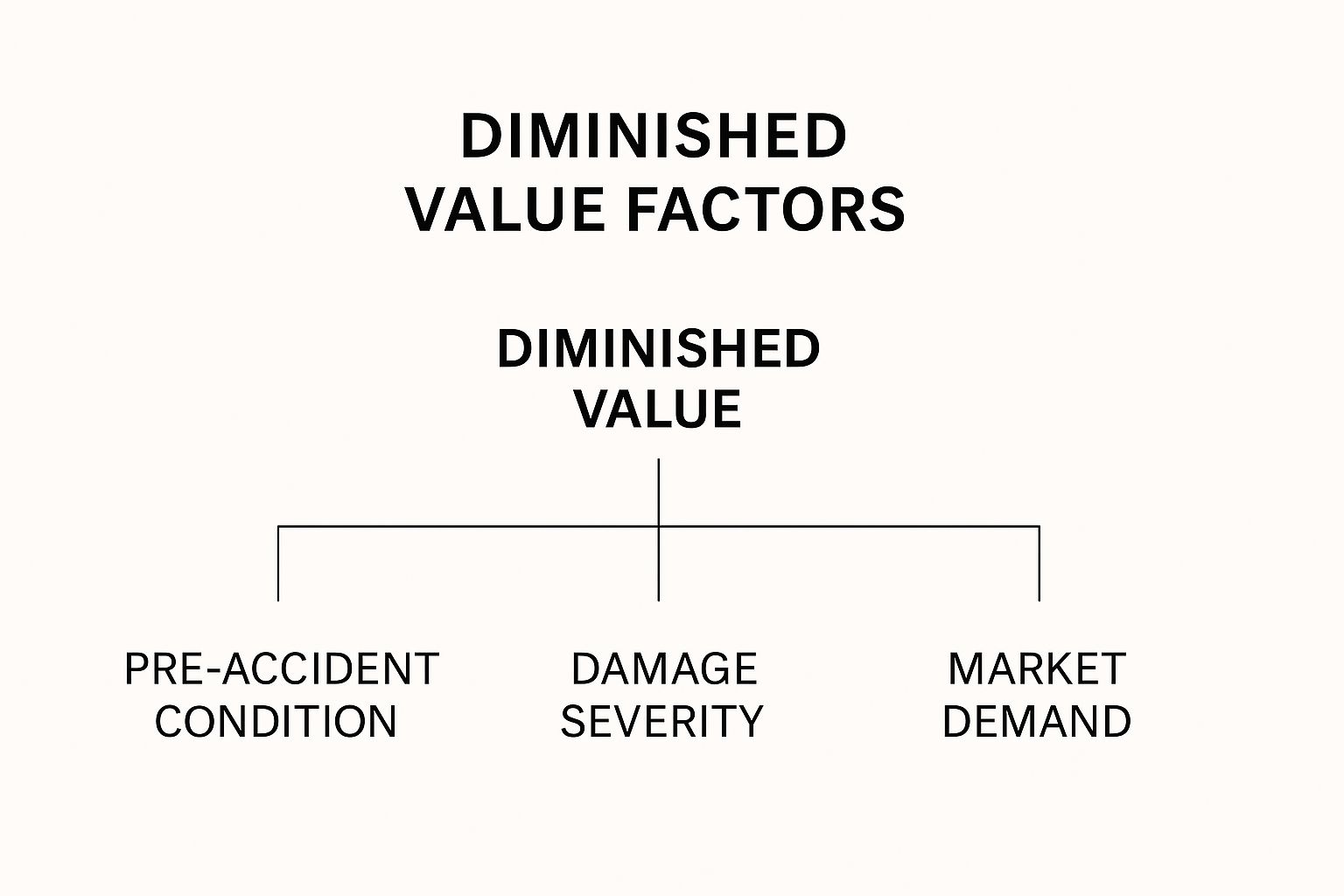

This image breaks down the main factors that go into calculating your vehicle's total diminished value.

As you can see, the final number isn't pulled out of thin air. It’s a careful calculation based on your car's condition before the crash, how bad the damage was, and how popular your specific model is on the open market.

Repair-Related Diminished Value: The Penalty for Shoddy Work

Next up is Repair-Related Diminished Value. This is an additional loss that happens when the repairs themselves are done poorly, making your car worth even less than it should be. It’s a direct result of bad workmanship.

You know you're dealing with this type of loss when you spot issues like:

- Mismatched Paint: The new paint is just a shade off from the factory original, and it’s obvious.

- Cheap Aftermarket Parts: The shop used non-OEM (Original Equipment Manufacturer) parts that don't fit or perform as well as the originals.

- Uneven Panel Gaps: The hood, doors, or trunk don't line up quite right, leaving weird spaces.

- Lingering Problems: You notice a new rattle, a slight pull to one side when you drive, or other mechanical gremlins that weren't there before the wreck.

This is a loss you absolutely shouldn't have to eat. You can—and should—hold the insurance company or their chosen body shop accountable for fixing these mistakes. For drivers in the Pacific Northwest, local rules can make a big difference, so it’s worth taking the time to learn more about filing a diminished value claim in Oregon specifically.

Immediate Diminished Value: The Pre-Repair Snapshot

Finally, there’s Immediate Diminished Value. This one is a bit more technical. It represents the loss in value right after the accident, before any repairs have started. It’s simply the difference between what your car was worth one minute before the crash and what it’s worth as a pile of wrecked metal right after.

The Bottom Line: While all three types of diminished value are real, the one you'll almost always be fighting for is Inherent Diminished Value. This is the core of your claim against the at-fault driver’s insurance and the foundation of any settlement negotiation.

Because immediate diminished value technically disappears once the car is repaired, it rarely comes up in a standard claim. Still, understanding all three types gives you a complete picture of what happened to your car's value and empowers you to argue your case with confidence.

How Vehicle Age and Type Affect Your Claim

When you're trying to figure out a car's diminished value after a wreck, it's crucial to understand that not all vehicles are created equal. The specific profile of your car—its age, make, model, and even its condition right before the accident—plays a huge part in what you can expect to recover.

Think of it like this: a minor fender bender on a brand-new Mercedes-Benz S-Class will cause a much bigger drop in value than the exact same damage on a 10-year-old Ford Focus. The person buying a luxury car is paying for perfection and prestige. An accident history shatters that illusion, resulting in a massive financial hit.

But this isn't just about six-figure supercars. The unique position of any vehicle in the market will shape its potential for a diminished value claim.

Why Newer Cars Suffer a Greater Loss

The vehicle's age is easily the most significant factor in any diminished value claim. It’s pretty straightforward: newer cars almost always see a bigger drop in value because they simply have more value to lose. A car that’s only a year or two old has barely depreciated from its original sticker price.

An accident puts a permanent black mark on its history report, instantly setting it apart from other pristine, accident-free cars on the lot. This is where the loss hits hardest. A potential buyer might look past a minor accident on an older car, but they're going to demand a steep discount for the same issue on a vehicle that's practically new.

Interestingly, the age of a car is a bit of a double-edged sword. The national vehicle fleet is getting older—in 2024, the average age of vehicles on U.S. roads hit a record 12.6 years. As repair costs climb, older cars are more likely to be totaled out after an accident. This means diminished value claims are most often pursued for newer, repairable vehicles. You can read more about how vehicle age impacts insurance claims and total loss trends.

The Impact of Make and Model

Is your car a hot commodity known for holding its value, like a Toyota Tacoma or a Porsche 911? Or is it a more common sedan with an average resale history? An insurance adjuster will look very closely at the make and model, and you should too.

-

Luxury and Exotic Vehicles: These cars take the biggest hit, hands down. Buyers in this high-end market expect perfection and a clean vehicle history. An accident, no matter how well it was repaired, creates a stigma that can slash tens of thousands of dollars from the car's price tag.

-

High-Resale-Value Models: Popular trucks and SUVs known for their rock-solid reliability also see a significant drop. A huge part of their appeal is their proven long-term value, which is directly undermined by an accident record.

-

Standard Sedans and Economy Cars: While the total dollar amount of the loss might be smaller, the percentage can still be substantial. A $2,000 loss on a $15,000 car is a serious financial blow for any owner.

Your vehicle's desirability on the open market is a key part of your argument. If your car is a popular model that buyers actively seek out, its accident history becomes a much bigger deal during a sale, justifying a higher diminished value claim.

Pre-Accident Condition and Mileage Matter

Finally, don’t overlook your car’s condition and mileage right before the crash. A low-mileage, garage-kept vehicle in mint condition will have a much higher pre-accident value than an identical car with high mileage and obvious wear and tear.

To build the strongest possible case, you need to document everything that proves your car was in superior condition. Gather things like:

- Maintenance Records: Show a history of regular oil changes and scheduled service.

- Recent Upgrades: Did you just put on new tires or replace the battery?

- Pre-Accident Photos: If you happen to have them, they are golden for establishing the car’s pristine state.

This information helps your appraiser lock in the highest possible pre-accident value, which is the baseline for calculating your total loss. The bigger the gap between its "before" and "after" value, the stronger your diminished value claim becomes.

Proving Your Claim with a Professional Appraisal

So, the accident happened, the repairs are done, and now the at-fault driver's insurance adjuster is on the phone with an offer. Don't be too quick to accept it. That first number is almost always a lowball starting point for a negotiation, not the final word.

Insurance adjusters often lean on generic, one-size-fits-all formulas to calculate your payout. The most notorious of these is the “17c” method, a calculation designed from the ground up to produce the lowest possible diminished value figure.

Letting them dictate the value based on their internal math is like letting the opposing team's coach referee the championship game. It’s just not in your best interest. To counter their low offer, you need undeniable, expert-backed proof of your car’s actual loss in value. This is where a professional, independent appraisal becomes your most powerful tool.

Why the Insurance Company's Math Is Flawed

Let's be blunt: insurance companies are businesses, and their biggest expense is paying out claims. The formulas they use are intentionally vague and built to minimize those payouts. They rarely account for the truly important factors that determine your car's value.

Things like your vehicle's specific make and model, its pristine pre-accident condition, or the high demand for it in your local market are often ignored. An adjuster’s quick calculation from a worksheet simply isn't a credible assessment of what your car is worth now. To get a fair settlement, you have to bring a detailed, professional report to the table that they can't easily brush aside.

A professional appraisal isn't just a second opinion. It's a meticulously researched document that serves as the bedrock of your entire diminished value claim, replacing the insurer's biased numbers with a fair market valuation.

A certified appraisal provides the hard evidence needed to shift the conversation from their flawed formula to the real-world facts of your financial loss. It also sends a clear signal to the adjuster: you know your rights, you're serious about your claim, and you’re prepared to fight for what you're owed.

What Makes a Diminished Value Appraisal Report Compelling

A truly great appraisal is more than a number on a page; it's a comprehensive document that builds an airtight case for your vehicle's lost value. An experienced appraiser digs into multiple data points to create a report that can withstand the intense scrutiny of any insurance adjuster.

A compelling report will always include these critical components:

- Pre-Accident and Post-Repair Values: It establishes your car's fair market value the moment before the crash and its new, lower value after repairs are complete.

- Local Market Comparables: The appraiser researches recent sales of similar vehicles in your area—both with and without accident histories—to provide real-world proof of the value drop.

- Detailed Damage and Repair Analysis: The report should list the exact damages and repairs, explaining how these factors hurt the car’s long-term integrity and make it less desirable to future buyers.

- Appraiser's Credentials and Certification: The report must feature the appraiser's qualifications, certifications (like I-CAR or ASE), and experience to establish them as an undeniable expert.

This level of detail transforms your claim from a simple request into a well-supported demand. Remember, even with perfect repairs, an accident history report permanently scars a vehicle's value.

Finding a Reputable and Certified Appraiser

The strength of your claim rests entirely on the credibility of your appraiser. You need an expert who isn't just certified but also has a proven track record of writing reports that insurance companies have to take seriously. Most importantly, find someone who is truly independent and has no financial ties to insurance companies.

When looking for the right professional, here's what to do:

- Check for Certifications: Make sure they hold recognized industry certifications. This proves they've met strict standards for knowledge and ethics.

- Ask for Sample Reports: A good appraiser will have no problem showing you redacted examples of their past work. This lets you see firsthand the level of detail and professionalism you'll get.

- Read Reviews and Testimonials: See what other car owners in your shoes have said about their experience. A history of positive feedback is a strong sign of success.

Taking the time to find an independent auto appraiser near you is a critical investment in your claim's outcome. It’s your best defense against an insurer's attempt to undervalue your loss and the key to getting the fair settlement you deserve.

A Step-by-Step Guide to Filing Your Claim

Once you have a professional appraisal, you're in a much stronger position. You're not just asking for money anymore; you're presenting a documented, evidence-backed demand. Now, it’s time to officially file your claim. This part takes a bit of organization and a clear head, but you can absolutely handle it by following a few key steps.

The first move is always yours. You have to formally tell the at-fault driver's insurance company that you intend to file for the diminished value after your car accident. A quick phone call gets the ball rolling, but always follow up with an email or even a certified letter. Having a paper trail is just smart business.

Assembling Your Evidence Package

Your appraisal report is the centerpiece of your claim, but it needs solid backup. Think of yourself as building a case file. The cleaner and more complete your documentation is, the more weight your claim will carry with the insurance adjuster.

Before you even think about sending your demand, get all your ducks in a row. This collection of documents will be the backbone of your request.

- The Police Report: This is crucial because it officially establishes who was at fault.

- Repair Invoices: You'll need the final, itemized bill from the body shop. It proves the extent and cost of the work done.

- Pre-Accident Records: Gather any maintenance logs or photos you have that show your car was in great shape before the wreck.

- Your Independent Appraisal: This is your expert evidence, clearly stating the dollar amount of value your car has lost.

Drafting a Powerful Demand Letter

Your demand letter is your formal, written request for payment. Keep it professional, concise, and direct. This isn't the time for a long, emotional story—it's a straightforward business letter that presents the cold, hard facts.

The letter needs to identify who you are, provide the key details of the accident (date, location, and claim number), and state the exact amount you are demanding based on your appraiser’s findings. Make sure you attach copies of your appraisal and all your supporting documents. This package presents a logical, undeniable argument for why you are owed this money.

A strong demand letter accomplishes three things: it clearly lays out the facts, provides irrefutable proof, and signals to the insurer that you've done your homework and are serious about getting a fair settlement.

Navigating Negotiations with the Adjuster

Once you send your demand, the real work begins: negotiation. Remember, the adjuster's goal is to close the claim for as little money as possible. You can expect them to come back with a lowball offer, challenge your appraisal, or try to find weak spots in your case.

This is where you need to stay calm and professional. Don't let them rattle you. Keep bringing the conversation back to your appraisal and the facts. When they give you a low number, explain why it’s not enough by referencing specific examples and market data from your appraiser’s report. Knowing how to negotiate a diminished value claim is a learned skill that comes down to persistence and sticking to the evidence.

If you hit a wall and feel the insurance company isn't negotiating in good faith, it might be time to escalate. You can file a formal complaint with your state's department of insurance or speak with an attorney who handles these types of claims. Often, the possibility of escalation is enough to make a fair offer suddenly appear.

Got Questions About Diminished Value? We've Got Answers.

After a wreck, your head is probably swimming with questions about getting your car fixed and getting your life back to normal. One of the biggest—and often most confusing—is the idea of a diminished value claim. It can feel like a maze, but let's clear up some of the most common questions we hear every day.

First up, a big one: can you file a claim if the accident was your fault?

Almost always, the answer is no. Think of a diminished value claim as something you file against the person who caused the accident. It's part of a third-party claim against their insurance. Your own policy is set up to pay for repairs, not to compensate you for the car's drop in market value.

People also worry they've waited too long. Is there a deadline?

What's the Time Limit on Filing My Claim?

Yes, and this is critical. Every state has a legal deadline for property damage claims, known as the statute of limitations. This isn't a flexible guideline; it's a hard cutoff.

The time you have can vary wildly depending on where you live, from just a single year in some states to several years in others. The best advice? Don't wait. To be safe, you should start the diminished value process right after your car repairs are finished. This ensures you don’t accidentally miss your chance to get paid what you're owed.

Can I Still File a Claim if My Car is Leased or Financed?

Not only can you, but you absolutely should. In these situations, a diminished value claim is one of your most important financial safeguards.

- If you lease your car: When your lease is up, the leasing company will assess its value. They can—and often will—charge you for the value lost due to the accident history. A successful DV claim gives you the cash to cover that charge.

- If you have a car loan: A major accident can sink your car's resale value, potentially leaving you "upside down." That's a scary spot where you owe more on your loan than the car is actually worth.

Winning a diminished value settlement protects you from these financial hits. It makes sure that another driver's mistake doesn't send your own finances into a tailspin.

Trying to get a fair shake from an insurance company can be a real headache, but you don't have to go it alone. Total Loss Northwest provides the certified, professional appraisals that make insurers pay attention to your car's true loss in value.

Get the expert help you need for a fair settlement. Find out more at the Total Loss Northwest website.