It's a gut-wrenching moment: the phone call where you learn your car is a "total loss." For most of us, that means the vehicle we depend on every day is gone, and we're left wondering what comes next.

In the simplest terms, an insurance company "totals" a car when they decide it costs more to fix than it's actually worth. But it's not just about a crumpled fender or a deployed airbag; it's a cold, hard financial calculation.

Decoding the "Total Loss" Decision

When an adjuster says your car is a total loss, they aren't commenting on how well you maintained it or how much you love it. They're making a purely economic call.

Think of it this way: if a contractor told you it would cost $400,000 to repair a foundation issue on a house worth $350,000, you wouldn't do it. You'd cut your losses. That's exactly what the insurance company is doing. They've run the numbers and concluded it's cheaper to write you a check for your car's value and sell the wreck for parts than it is to pay a body shop to put it all back together.

This entire decision pivots on a single, crucial number: your car’s Actual Cash Value (ACV). This isn't what you paid for the car or what a brand-new one costs. It’s what your exact car—with its specific mileage, condition, and features—was worth on the open market a moment before the crash.

The insurer's process isn't a mystery. They follow a specific formula using a few key ingredients to decide your car's fate. Understanding these elements is the first step to making sure you get a fair shake.

Here’s a look at the main components that go into the insurance company's total loss calculation.

| Factor | What It Means for Your Claim |

|---|---|

| Repair Estimates | An adjuster or body shop creates a line-by-line estimate of what it will take to fix the damage, including all parts and labor. |

| Actual Cash Value (ACV) | This is the insurer's determination of your car's pre-accident market value, based on its age, mileage, condition, and recent sales of similar cars. |

| Salvage Value | This is the amount the insurance company expects to get back by selling your damaged car to a salvage or scrap yard. |

| State Regulations | Each state has its own rules. In places like Oregon and Washington, a specific formula or percentage threshold legally defines what qualifies as a total loss. |

Ultimately, these factors are plugged into a formula to see which option costs the insurer less money.

At its core, a total loss declaration is a business decision, not a personal one. The insurance company's job is to close your claim for the lowest possible amount. That’s why their first offer for your car's value is just that—an offer. It's the beginning of a negotiation, not the final word.

Navigating this process means understanding how these pieces fit together. While the insurance company has its own data and adjusters, you have the right to challenge their math—especially their valuation of your vehicle. This is where getting an independent appraiser involved can be a game-changer, giving you the leverage you need to get the settlement you deserve.

Understanding the Total Loss Formula

At the heart of every total loss decision is a surprisingly simple calculation. When an insurance adjuster surveys your damaged car, they aren't just looking at the twisted metal. They're weighing two numbers against each other: how much it would cost to fix it, and what your car was worth just a moment before the crash.

That pre-accident value has a specific name: Actual Cash Value (ACV).

Think of the ACV as a snapshot of your car's fair market price. It’s not the sticker price from the dealership or what you still owe on your loan. It’s what someone would have reasonably paid for your specific car—considering its make, model, year, mileage, and overall condition—right before the accident happened. This single number is the bedrock of the entire total loss equation.

Once the insurer pins down the ACV, they compare it to the repair estimate. But they don't just total the car if the repairs cost a dollar more than the ACV. Instead, they use a benchmark called the Total Loss Threshold (TLT).

The Role of the Total Loss Threshold

A Total Loss Threshold is simply a percentage. It’s the line in the sand, set by state law or the insurance company’s own rules, that determines when a car is officially a goner.

Some states make this mandatory. For example, if a state has a 75% TLT, any vehicle with repair costs that climb past 75% of its ACV is legally required to be totaled. Other states, like Washington, use a slightly different approach called the Total Loss Formula (TLF), which we’ll get into next.

Even without a state mandate, the industry has its own standards. Most insurance companies will declare a vehicle a total loss when repair estimates hit 70-80% of its ACV. So, if your truck has an ACV of $25,000, a repair bill anywhere from $17,500 to $20,000 will likely push it into total loss territory. This is happening more and more often; by Q2 2025, a staggering 22.6% of all collision claims ended in a total loss. You can explore the data for yourself in the Crash Course 2025 report.

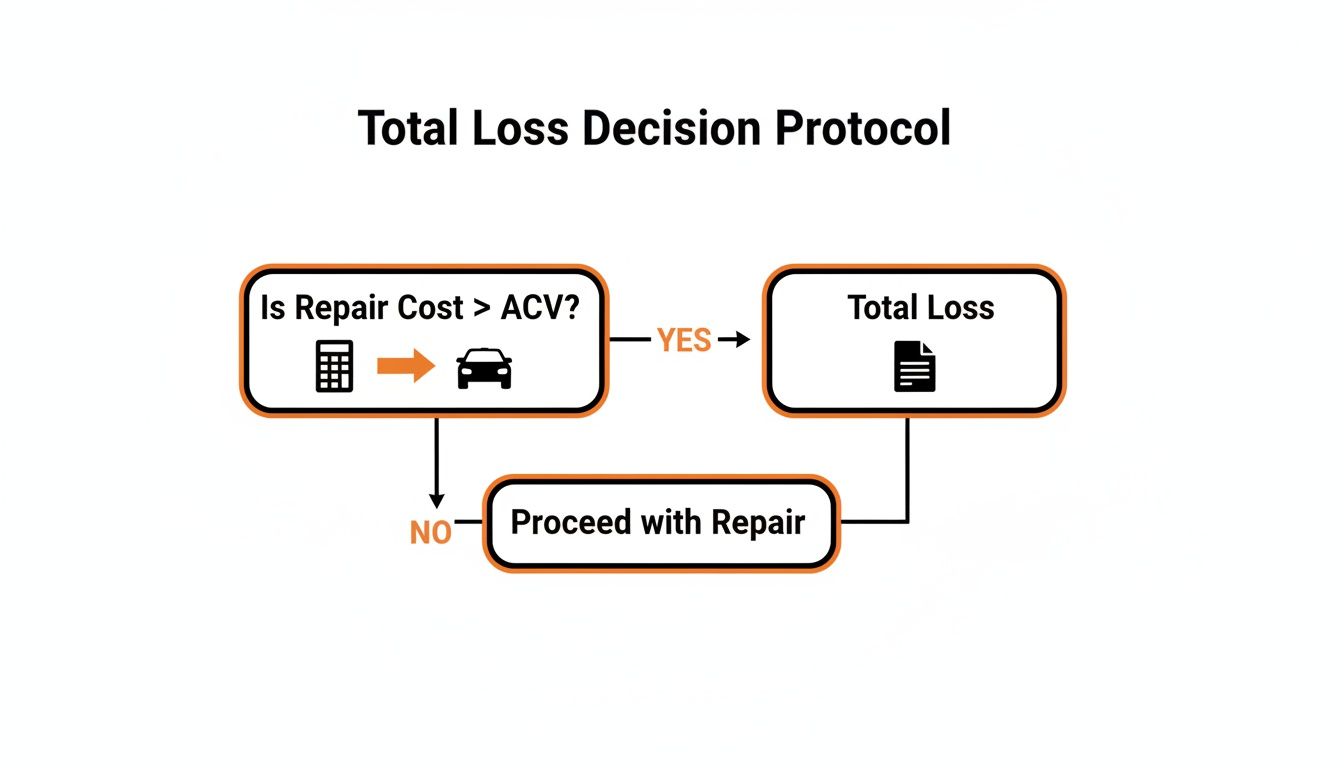

This decision process basically boils down to a simple flowchart.

As you can see, the insurer's primary calculation is a straightforward comparison: repair estimate vs. pre-accident value.

Seeing the Formula in Action

Let’s make this real. Imagine your car has an ACV of $20,000, but the outcome depends entirely on where the accident happened.

-

Scenario A: High Threshold State

- ACV: $20,000

- Repair Estimate: $16,500

- State TLT: 85% (which is $17,000)

- Result: The $16,500 repair bill is under the $17,000 threshold. The insurance company will almost certainly choose to repair your car.

-

Scenario B: Lower Threshold State

- ACV: $20,000

- Repair Estimate: $16,500

- State TLT: 75% (which is $15,000)

- Result: Now, that same $16,500 estimate is over the $15,000 threshold. The insurer is now required to declare it a total loss.

It's the same car, same damage, but two completely different outcomes. This is exactly why knowing your state’s rules is so critical.

Because your entire settlement is based on the ACV, this is often where the fights start. An unfairly low ACV can cost you thousands of dollars, making it impossible to replace what you lost. That’s why you have to scrutinize the insurer's valuation report. If the numbers feel off, getting a professional total loss estimate from an independent expert gives you the leverage you need to challenge their offer and get paid what your vehicle was actually worth.

Oregon vs. Washington: How State Law Decides if Your Car is Totaled

Where your accident happened can be just as important as how it happened. That’s because the rules that force an insurance company to declare a car a total loss aren't the same everywhere—they change from state to state. If you’re a driver in the Pacific Northwest, getting a handle on the specific laws for Oregon and Washington is your first, best defense against a lowball offer.

These state-specific rules create a legal formula for when a car must be totaled. It takes the decision out of the insurance adjuster's hands and replaces it with a clear, mathematical trigger. Knowing how your state’s formula works gives you the power to hold the insurer accountable and make sure their math lines up with the law.

Washington: The Total Loss Formula

Washington doesn't use a simple percentage like many states. Instead, it relies on something called the Total Loss Formula (TLF). This approach gives insurers a bit more wiggle room, but it’s still based on a straightforward economic principle.

Under Washington state law (WAC 284-30-391), your car is officially a total loss if the cost of repairs plus its leftover scrap value is equal to or more than its pre-accident value.

Here’s a simple breakdown of the terms:

- Repair Costs: The total estimated price to bring the vehicle back to its pre-accident condition.

- Salvage Value: What the insurance company expects to get by selling your wrecked car to a salvage yard.

- Actual Cash Value (ACV): The fair market value of your vehicle a moment before the crash.

The Formula: If (Repair Costs + Salvage Value) ≥ ACV, it's a total loss.

Let's look at a real-world example. Say a family SUV in Seattle gets into a serious collision.

- ACV: $28,000

- Repair Estimate: $22,000

- Salvage Value: $7,000

First, we add the repair costs to the salvage value: $22,000 + $7,000 = $29,000. Because that $29,000 sum is greater than the car's $28,000 ACV, Washington law defines this vehicle as a total loss. End of story.

Oregon: A Straightforward Percentage Threshold

Oregon’s approach is much more direct. The state uses a clear, non-negotiable percentage threshold to decide when a car is totaled, which helps remove a lot of the gray area from the process.

Under Oregon Revised Statute 801.527, a vehicle is deemed totaled if the repair costs climb above 80% of its Actual Cash Value. This is a hard-and-fast rule for any vehicle that’s six years old or newer.

For older vehicles (seven years or more), Oregon law gives the insurer a little more discretion. Even then, they still have to prove that fixing the car just doesn't make financial sense.

Let’s apply this to a typical commuter car in Portland.

- Vehicle: A four-year-old sedan.

- ACV: $19,000

- Repair Estimate: $15,500

To find Oregon's total-loss trigger, we calculate 80% of the car's value: $19,000 x 0.80 = $15,200. Since the repair shop’s estimate of $15,500 is higher than the $15,200 legal threshold, the insurance company is required by law to total the vehicle.

Why You Need to Know These Local Laws

Knowing your state's specific rule is the legal ground you stand on. When an adjuster comes to you with an offer or a repair decision, you can check their work against the actual law.

This knowledge completely changes the conversation. It’s no longer just their opinion versus yours. It becomes a discussion based on established state regulations, giving you a huge advantage in pushing for a fair settlement that reflects your vehicle's true worth.

Why More Cars Are Being Totaled Today

If it feels like you're hearing about more "totaled" cars than ever before, you're not imagining things. The days when a total loss was reserved for catastrophic, twisted-metal wrecks are long gone. Today, what looks like a minor fender-bender can easily push a modern vehicle over the financial cliff.

The main reason? Our cars have become incredibly complex. What used to be a simple plastic bumper is now a sophisticated hub of technology. A minor bump can damage a hidden network of sensors, cameras, and wiring that are astonishingly expensive to replace and recalibrate.

This isn't just a gut feeling; the numbers back it up. By mid-2025, total loss declarations were already accounting for 27-30% of all collision claims in the United States. It's a perfect storm of advancing tech, skyrocketing repair costs, and the simple fact that our cars are getting older. You can see more data on how small changes are leading to big results in total loss claims from industry analysts.

The High Cost of Modern Repairs

Think about all the features that make new cars so safe and convenient. Every one of those systems adds another layer of cost to what used to be a straightforward fix. That simple bumper replacement is anything but simple when it’s packed with sensors for parking assist, blind-spot monitoring, and automatic emergency braking.

Here’s a quick look at what’s driving up repair bills:

- Advanced Driver-Assistance Systems (ADAS): We're talking about the cameras in your windshield, radar sensors in your bumpers, and lidar units. Even a slight misalignment after an accident means they need a specialized, costly recalibration to work properly.

- Complex Materials: Cars are now built with a mix of high-strength steel, aluminum, and carbon fiber to save weight and boost safety. Fixing these materials isn't like banging out a dent in an old steel fender; it requires special training and equipment that not every body shop has.

- Specialized Labor: The technicians fixing your car today need to be part IT specialist, part mechanic. Finding people with the skills to work on these high-tech systems is tough, and that shortage drives up labor rates.

A windshield replacement that used to be a few hundred bucks can now easily top $1,500 if it has a camera for your lane-keeping system that needs to be perfectly recalibrated. For an older car, that single repair could be enough to get it declared a total loss.

Economic Forces Tipping the Scales

It's not just what's happening in the repair bay. Broader economic trends are also making it more common for insurers to write that check instead of authorizing repairs. It’s a classic case of rising costs colliding with fluctuating values.

The decision to total a vehicle is a purely financial calculation made by the insurer. It has nothing to do with how well you maintained your car or how much you love it.

This cold, hard math is heavily influenced by a few key market forces:

- Supply Chain Headaches: The global supply chain for car parts is still a mess. If a single sensor or control module is on backorder, your car could sit at the shop for months. All the while, the insurer is paying for your rental car, making a quick total-loss payout look a lot more appealing.

- Soaring Parts Inflation: The cost of the parts themselves has gone through the roof. Everything from microchips to the little plastic clips that hold a bumper on costs more, directly pumping up the "repair" side of the total loss equation.

- Volatile Used Car Values: While used car prices soared for a while, they've started to come back down. As a car's Actual Cash Value (ACV) drops, it takes a much smaller repair bill to cross the total loss threshold. A $10,000 repair on a car worth $15,000 is far more likely to be totaled than the same repair on a car worth $25,000.

When you combine technologically complex cars, expensive repairs, and a shaky used car market, you get the perfect recipe for an explosion in total loss claims. That’s why it’s more critical than ever for you, the owner, to be ready to defend your car’s true value if an accident happens.

Your Action Plan After a Total Loss Declaration

The moment an insurance adjuster says the words "total loss," the game changes. It can feel like you’ve been thrown into the deep end, but having a clear plan of action puts you back in the driver's seat. The first rule is simple: do not immediately accept the insurance company's first offer.

Think of their initial number as an opening bid, not the final word. Your very next move should be to ask for a complete copy of their valuation report. This document breaks down how they arrived at their number, and trust me, it’s often full of errors that can cost you thousands.

Scrutinize the Insurer's Valuation Report

Once you get that report, it’s time to go through it with a fine-tooth comb. Insurers use third-party services that pull data on "comparable" vehicles to determine your car’s value, but the software they use is far from perfect. You're looking for mistakes—big and small—that drag down your car’s Actual Cash Value (ACV).

Go through every single line item. Pay special attention to these common weak spots:

- Incorrect Vehicle Options: Did they list your car as the base model when you actually had the premium trim with a sunroof, leather seats, and an upgraded stereo? Those options add real value.

- Inaccurate Mileage: A simple typo can make a huge difference. A car with 50,000 miles is worth quite a bit more than the same one with 80,000 miles.

- Unfair Condition Rating: Adjusters often slap an "average" or "fair" condition rating on a vehicle without a second thought. If your car was immaculate, you need to prove it with maintenance records, recent receipts, or photos.

- Bad "Comps": Look at the comparable vehicles they used for their valuation. Are they actually from your local market? It’s a common tactic to pull comps from hundreds of miles away where car values are lower.

Every single discrepancy you find gives you leverage to challenge their offer. Each error, no matter how small it seems, is a talking point to negotiate a higher, fairer settlement. You can find more strategies in our complete guide on what to do when your car is totaled.

Remember, the insurer’s valuation report is their argument for what your car is worth. Your job is to build a counter-argument with facts, records, and solid evidence to prove what it was truly worth right before the accident.

Invoke the Appraisal Clause in Your Policy

So what happens when you’ve pointed out all the mistakes, presented your evidence, and the insurance company just won't budge? This is where a powerful, but often overlooked, tool in your policy comes into play: the Appraisal Clause.

The Appraisal Clause is a provision baked into most auto insurance policies that outlines a specific process for settling valuation disputes. It’s essentially a tie-breaker that takes the final decision out of the insurance company’s hands.

Here’s a quick rundown of how it usually works:

- You hire your own certified, independent appraiser. This is a crucial step—this expert works for you, not the insurer.

- The insurance company hires its own appraiser.

- The two appraisers negotiate. They’ll review all the evidence and try to come to an agreement on your vehicle's fair value.

- An Umpire Steps In (If Needed): If the two appraisers can't agree, they select a neutral third-party umpire. A final value agreed upon by any two of the three parties becomes binding.

Invoking this clause completely levels the playing field. It forces the insurer to defend its lowball number against a certified expert whose only goal is to find your car's true market value. Taking this step is often the key to getting the fair settlement you’re entitled to. Of course, part of the process also involves paperwork, so it can be helpful to understand what’s required for transferring a car title in your state.

How to Challenge a Low Settlement Offer

When that settlement offer from your insurance company lands in your inbox, it's easy to feel defeated. It often looks like a final, take-it-or-leave-it number. But here's the truth from someone who's seen this play out countless times: that offer is just their opening move. It's the start of a negotiation, not the end.

To successfully challenge their valuation, you first have to understand their game. Insurers typically lean on valuation software that pulls "comparable" vehicles from hundreds of miles away, where car values might be significantly lower. They might also misclassify your car's trim package or completely ignore its optional features. Your best defense is a strong offense, armed with your own undeniable proof of value.

The Power of an Independent Appraisal

Your single most effective tool in this fight is a certified, independent appraisal. Think of it this way: the insurer's report was built to protect their bottom line. An independent appraisal is a detailed, evidence-based argument built to protect you.

A professional appraisal is so much more than a quick Kelley Blue Book search. A good appraiser will:

- Dig into Your Local Market: They’ll research what cars like yours have actually sold for recently right here in your area, whether it's Portland, Seattle, or a smaller town.

- Find True "Comps": They locate legitimate, apples-to-apples comparable vehicles, matching the correct year, make, model, trim, and mileage.

- Make Fair Adjustments: The appraiser will add value for your vehicle’s pristine condition, recent upgrades like new tires, and desirable features the insurance software completely overlooked.

This detailed report becomes your negotiating leverage. For a deeper look at the process, check out our guide on auto insurance appraisals and see how they can be the key to a fair settlement.

A lowball offer isn't a final verdict; it's an invitation to negotiate. An independent appraisal is your evidence-backed RSVP, showing you've come prepared to demand your vehicle’s true market value.

Understanding the Insurer's Motivation

It helps to remember what's happening on their end. Insurance companies are businesses, and they're under enormous financial pressure to control claim payouts. When used car prices shot up by over 40% in 2021, major insurers felt the squeeze.

State Farm's loss ratio hit 72.2%, GEICO's parent company reached 75.0%, and Allstate's jumped to 67.3%. This kind of financial pressure naturally leads them to manage payouts as tightly as possible, which often means lower initial ACV offers for customers like you.

A Real-World Example of Success

Let me tell you about a client with a meticulously maintained SUV here in Washington. The insurance company came in with an offer of $24,500. Their report was a classic example—it used comps from a rural market over 150 miles away and listed the vehicle's condition as just "average."

The owner knew their SUV was worth more and hired us. Our appraisal documented all the premium features, included receipts for recent major service, and found three solid comparable sales right in the owner's zip code. Our final appraised value was $29,000.

Armed with that professional report, the owner went back to the insurer and successfully settled for $28,750. That’s an extra $4,250 in their pocket. This just goes to show you don't have to accept that first number and leave thousands of dollars on the table.

Common Questions About Total Loss Claims

Dealing with a serious accident is stressful enough. When your insurance company starts talking about "totaling" your car, it can open up a whole new can of worms and a lot of urgent questions. Let's walk through some of the most common things people worry about during this process.

Can I Keep My Car if It Is Totaled?

The short answer is yes, most of the time you can. This is officially called “owner retention.”

If you decide to keep your wrecked vehicle, the insurance company will calculate your settlement differently. They’ll pay you the car’s Actual Cash Value (ACV) but subtract what they would have gotten for it at a salvage auction. That leftover amount is what you get.

Just be prepared for what comes next. The state will brand your car with a "salvage title," which is a huge red flag. Getting insurance, registering it for the road, or ever selling it again becomes incredibly difficult. On top of that, you're now solely responsible for getting it repaired and paying for everything out of pocket.

What if I Owe More Than the Settlement?

This is a tough spot to be in, and it happens more often than you'd think. It's known as being "upside down" on your loan. The insurance company's payout is based on what your car was worth right before the crash, not what you owe the bank. You’re still on the hook for the rest of that loan.

This is exactly what GAP (Guaranteed Asset Protection) insurance is for. If you have a GAP policy, it steps in to pay off that remaining loan balance. Without it, the difference has to come straight from you.

How Long Does the Total Loss Process Take?

There's no single answer here, but you should probably plan on it taking anywhere from a few weeks to over a month. It’s rarely a quick process.

Several things can slow it down or speed it up:

- How busy your insurance adjuster is and how quickly they move.

- How complicated the accident was to investigate.

- Whether you accept their first offer or decide to negotiate for a better one.

Fighting for a fair settlement by using the appraisal clause will definitely add some time to the clock, but it’s often the only way to get the money you're truly owed.

If you're facing a lowball offer and need to prove your vehicle's true worth, Total Loss Northwest can help. Our certified, independent appraisals give you the evidence you need to challenge the insurer and get the fair settlement you deserve. Learn more at https://totallossnw.com.