When you hear the word "totaled" after a car wreck, you probably picture a twisted heap of metal. But that’s not always the case. More often than not, it's a constructive total loss, which is an insurance term that has everything to do with money and almost nothing to do with how the car looks.

It’s a financial call, pure and simple. Even if your car seems fixable, the insurance company has decided that paying to repair it is a bad investment.

Understanding the Financial Side of a Total Loss

Let's use an analogy. Imagine your trusty old laptop, worth about $500 on the used market, suddenly dies. You take it to a repair shop, and they quote you $600 to fix the motherboard. Does it make any sense to spend $600 fixing something that’s only worth $500? Of course not. You'd just buy another one.

Insurance companies think the exact same way about your car. A constructive total loss happens when the cost to properly repair your vehicle, plus what they can get for it as scrap (its salvage value), adds up to more than the car’s market value right before the crash.

It all boils down to a business decision based on one straightforward formula.

The Core Calculation

The entire decision to total your car rests on this single equation:

Cost of Repairs + Salvage Value ≥ Actual Cash Value (ACV)

If the numbers on the left are the same or bigger than the number on the right (your car’s pre-accident value), the insurer will declare it a constructive total loss. This is their way of cutting their losses and avoiding a situation where they sink more money into a car than it's actually worth.

To make this crystal clear, here’s a quick breakdown of how a constructive total loss differs from a vehicle that's physically beyond saving.

Actual vs Constructive Total Loss at a Glance

| Attribute | Actual Total Loss | Constructive Total Loss |

|---|---|---|

| Primary Cause | Extreme physical destruction (e.g., fire, flood, severe impact) | The cost to repair is economically unfeasible |

| Vehicle Condition | Unrepairable; often unrecognizable as a vehicle | Damaged but may appear repairable to the naked eye |

| The "Why" | It's physically impossible to fix | It's financially impractical to fix |

| Key Factor | The extent of the physical damage | The cost of repairs vs. the car's pre-accident value |

This table highlights the key point: an actual total loss means the car is gone for good, while a constructive loss is a judgment call made with a calculator.

Why This Matters to You

Getting a handle on this concept is the first, most important step toward getting a fair settlement. So many drivers are shocked when their car, with what looks like moderate damage, gets totaled. It happens all the time because modern cars are packed with expensive sensors, cameras, and structural components that can send repair costs through the roof.

Hidden frame damage or a single deployed airbag can easily add thousands to a repair bill.

The main takeaway here is that the adjuster isn't just looking at the dents you can see. They're running a cost-benefit analysis. Knowing this gives you insight into their process and puts you in a much better position to question their valuation if it seems low. For a deeper dive into the specific factors that push a car over the edge, take a look at our detailed guide on what makes a car totaled.

How Insurers Decide to Total Your Car

When an insurance adjuster looks at your wrecked vehicle, they’re not just seeing the damage. They’re running a business calculation to see if it’s cheaper to pay for repairs or to just cut you a check and sell the wreck for scrap. This is where the term constructive total loss comes into play.

It’s not some big secret; it's a straightforward formula. Knowing how they get their numbers is your first line of defense against a lowball settlement offer that leaves you short.

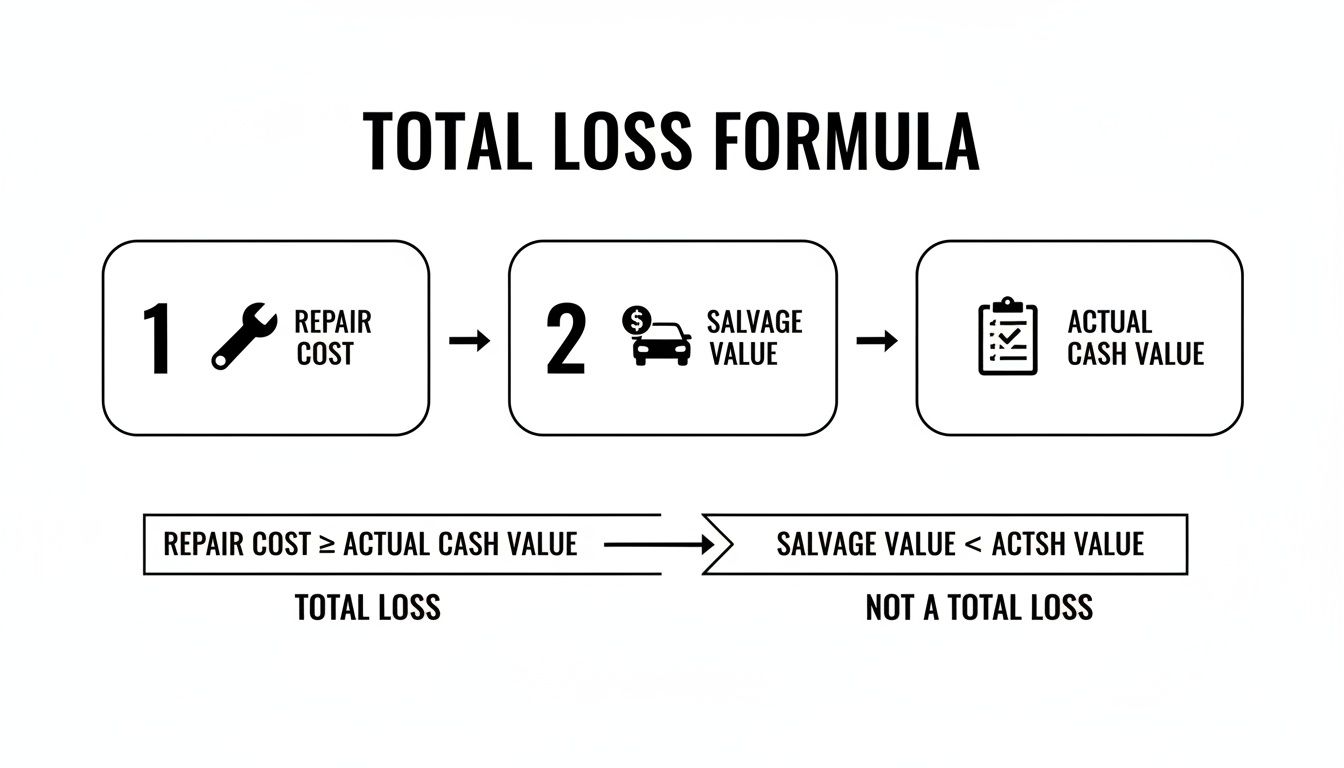

This diagram breaks down the three key pieces of the puzzle that insurers use.

As you can see, when the cost to fix your car plus its value as scrap metal adds up to more than what it was worth before the crash, the insurer will total it out. It’s a simple cost-benefit analysis for them.

The Total Loss Formula in Plain English

At its heart, the decision boils down to one simple equation that every single insurance carrier uses:

Repair Costs + Salvage Value ≥ Actual Cash Value (ACV)

If the first two numbers added together are equal to or more than the third, your car is officially a constructive total loss. Let’s pull back the curtain on how the insurer calculates each of these critical figures.

Repair Costs: This is the shop's estimate to bring your vehicle back to its pre-accident condition. Insurers often lean on their own adjusters or body shops in their "direct repair program" who give them discounted rates. This can create a real conflict of interest, as these initial estimates might miss hidden damage or rely on cheaper, aftermarket parts to keep the repair bill artificially low.

Salvage Value: This is what the insurance company thinks they can get for your wrecked car at a salvage auction. They look at what similar damaged vehicles have sold for recently and use that data to project a price. A car with a high salvage value is much more likely to be declared a total loss.

Actual Cash Value (ACV): This is where most of the fights happen. ACV is supposed to be your car’s fair market value the second before the accident. It’s not what it costs to buy a new one. Insurers use third-party valuation software like CCC ONE or Audatex, which often pull data from a massive (and sometimes questionable) pool of vehicle listings to generate an ACV—and it's almost always on the low side.

A Real-World Ford F-150 Example

Let's walk through how this plays out in a common scenario. Say your 2019 Ford F-150 gets into a pretty serious collision.

- The Insurer's ACV: Their software churns through the data and spits out a pre-accident ACV of $30,000 for your truck.

- The Repair Estimate: An adjuster at one of their preferred shops comes back with a repair estimate of $22,000. At first glance, it seems like the truck is repairable.

- The Salvage Value: But then, the insurer checks recent salvage auction results. They see that even a banged-up F-150 like yours can fetch around $9,000 for parts and scrap.

Now, they do the math: $22,000 (Repairs) + $9,000 (Salvage) = $31,000.

Because that $31,000 total is higher than the $30,000 ACV, your truck gets branded a constructive total loss. You can dive deeper into these variables by exploring https://totallossnw.com/calculating-total-loss-vehicle/.

This calculation shows you exactly where you can fight back. If the repair estimate is inflated or—much more likely—the ACV is unfairly low, the whole equation can flip in your favor. Sometimes an insurer will even try to use non-OEM parts to keep repair costs down; it's worth understanding what makes CAPA certified parts a valid point of negotiation in these estimates. Challenging the ACV with your own evidence is almost always the most effective way to get the fair settlement you deserve.

Crossing State Lines: How Washington and Oregon Handle Total Loss Claims

While the core idea behind a constructive total loss is universal, the specific math that triggers it can change the second you drive from one state to another. For anyone in the Pacific Northwest, it's essential to know the different playbooks for Washington and Oregon.

These aren't just minor differences in paperwork; state laws set the official line that determines if your car gets fixed or if you get a check. Knowing exactly where that line is drawn is your first and best defense against a lowball settlement offer. Insurance companies have to play by these rules, and so should you.

Washington's Total Loss Formula: A Game of Numbers

In Washington State, the rules are spelled out in the Washington Administrative Code (WAC). Think of it as the official rulebook for insurance claims. When it comes to totaling a car, the law gives insurers a clear, formula-based decision.

They have to total your car if the repair bill is more than the car was worth right before the crash. But the real action happens in the gray area where they have a choice.

Under WAC 284-30-391, your insurance company can call your vehicle a total loss if the repair cost combined with its scrap value is more than its Actual Cash Value (ACV). This gives them some wiggle room, but it also gives you an opening to push back.

This is the classic Total Loss Formula (TLF) in action: Repair Costs + Salvage Value ≥ ACV. If the insurer’s math tips the scale, they're almost certainly going to declare it totaled. It’s a pure business decision for them—which path costs less?

Your Rights as a Consumer in Washington

Washington law doesn't just set the formula; it also builds in some key protections to keep the process fair and transparent. You're not just a bystander in this process.

- Timely Updates: Insurers can't ghost you. They must acknowledge your claim within 10 working days and answer any of your questions within that same timeframe.

- Honest Valuation: They can't just cherry-pick the lowest comparable vehicle to set your car's value. The ACV has to be based on credible, local market data.

- Full Disclosure: You have a legal right to see the valuation report they used. This is your most powerful tool—get that report and go through it with a fine-tooth comb to find errors.

Oregon's Bright-Line Rule: The 80% Threshold

Oregon throws a bit of a curveball by using a different system. Instead of the flexible formula used in Washington, Oregon law establishes a hard-and-fast percentage.

This is called a Total Loss Threshold (TLT), and it removes much of the insurer's discretion.

In Oregon, a car is officially a total loss once the estimated repair cost climbs above 80% of its retail market value. This is a crucial difference, as it sets a very clear line in the sand.

Here’s what that looks like in the real world:

- Let’s say your car had a retail market value of $20,000 before the accident.

- The total loss threshold in Oregon is 80% of that, which comes out to $16,000.

- If the body shop’s estimate is $16,001 or higher, your car must be declared a total loss by law.

This percentage rule can sometimes be a double-edged sword. It might save a car with high-cost, low-impact damage from being totaled. On the other hand, a car you feel is unsafe could get repaired if the costs come in just shy of that 80% mark. Either way, knowing that magic number is key to planning your next move.

Your Three Options After a Total Loss Offer

When the adjuster calls with the news that your car is a constructive total loss, their settlement offer can feel like an ultimatum. It’s easy to think your only move is to sign the paperwork and take the check.

But that first offer isn't the final word. It's the opening move in a negotiation, and you have three very different paths you can take. Understanding these choices is what separates a passive claimant from a proactive owner who gets paid what they're truly owed. Let's break down each option.

Option 1: Accept the Insurer's Settlement Offer

This is the path of least resistance. You accept the insurance company’s offer for the Actual Cash Value (ACV), sign over your car’s title, and they send you a check. The insurer then takes your damaged vehicle and sells it for scrap or parts at a salvage auction.

While it’s the fastest way to close the claim, it's often the worst financial decision you can make. Insurance companies are businesses, and their goal is to minimize claim payouts. Their initial offers are frequently based on valuation reports that are full of errors and undervalue your vehicle. If you accept it without doing your homework, you could be leaving thousands of dollars behind.

Honestly, this route only makes sense if you’ve done your own research and confirmed their number is a fair market value for a car like yours in your area.

Option 2: Retain the Salvage Through an Owner Buyback

Your second choice is to keep your damaged car, a move called "owner retention" or "salvage retention." If you go this route, the insurance company still pays you the ACV, but they subtract what they would have gotten for the car at a salvage auction.

For example, if your car's ACV is $15,000 and its salvage value is $3,000, you’d get a check for $12,000 and keep the car. This can be a smart move in a few specific situations:

- You're Attached: It might be a classic, heavily customized, or a car with too much sentimental value to let go.

- You're a Mechanic: If you have the skills and tools, you might be able to fix it for far less than the body shop's estimate.

- You See Value in the Parts: The car might be worth more if you sell off its valuable components individually.

Be warned, though—this isn't an easy path. The DMV will brand the car with a salvage title, a permanent black mark. You’ll find it nearly impossible to get full insurance coverage again, and its resale value will be next to nothing. It's a choice that requires a very careful cost-benefit analysis.

Option 3: Dispute the Valuation and Negotiate

This is where you can really take control of the outcome. If that settlement offer feels low, you have every right to challenge it. You are not required to accept a valuation based on flawed data from the insurer's software. This is where you switch from being a victim of circumstance to an active negotiator.

The key to winning this fight is bringing solid proof to the table. You can't just say, "That's not enough." You have to prove it with comparable vehicle listings from your local market, detailed maintenance records, and a clear breakdown of why their valuation is wrong. If you get a lowball offer or run into a wall, knowing how to appeal a denied insurance claim gives you a playbook for fighting back.

But your most powerful weapon is probably already in your hands, hidden in the fine print of your policy: the Appraisal Clause. This clause gives you the right to hire your own certified, independent appraiser to establish your vehicle's true value.

When you invoke the Appraisal Clause, you force the insurer to deal with facts from an unbiased expert, not just their own computer-generated numbers. It completely levels the playing field and is your single best tool for getting the money you need to actually replace what you lost.

Using an Independent Appraisal to Get Fair Market Value

When an insurance company declares your vehicle a constructive total loss, the settlement they offer can often feel like a punch to the gut. This isn't by accident. It's the direct result of a valuation process built for their own efficiency, not for your benefit.

Insurers lean on third-party software programs like CCC ONE or Audatex. These platforms are designed to generate a quick Actual Cash Value (ACV) by crunching data from massive, often nationwide, databases. They're fast and cheap, but they frequently miss the mark.

The problem is that these algorithms often pull data from distant markets, gloss over your vehicle's specific condition and features, and fail to account for what similar cars are actually selling for in your local area. The result is an ACV that protects the insurer's bottom line, leaving you shortchanged.

But here’s the good news: you don't have to just accept their number. Hiring a certified, independent auto appraiser is the single most powerful step you can take to challenge a lowball offer and prove your vehicle's true fair market value.

The Appraiser’s Method vs. The Insurer’s Algorithm

An independent appraiser’s work is less like running a computer program and more like conducting a detailed investigation. Their process is hands-on, specific to your market, and focused entirely on one question: what was your car worth in your area the moment before the accident?

This meticulous approach results in a valuation that is far more accurate and, critically, defensible. If you're facing a low offer, it’s worth understanding exactly what a certified appraisal involves. You can learn more about how auto insurance appraisals level the playing field and empower you during your claim.

The difference between the two approaches is night and day, and it has a direct impact on your final settlement.

Insurer Valuation vs Independent Appraisal

This table breaks down the fundamental differences between how an insurer’s software calculates a value and how a real-world appraiser does it.

| Factor | Insurer's Valuation Method (e.g., CCC) | Independent Appraiser's Method |

|---|---|---|

| Data Source | Large, often national, databases of vehicle listings and auction results. | Local dealerships, private seller listings, and recent sales in your specific market. |

| Condition Adjustments | Relies on standardized, often generic, deductions and additions. | A hands-on inspection of your vehicle's actual condition, mileage, and features. |

| Comparables | May use "comparable" vehicles from hundreds of miles away to find lower prices. | Finds real, currently available vehicles for sale within a relevant geographic radius. |

| Customizations | Often ignores aftermarket upgrades, custom work, or unique features. | Documents and assigns value to all modifications, from custom wheels to performance parts. |

| Goal | To generate a quick, low-cost, and algorithmically justified ACV. | To determine the true, evidence-based fair market value to make you whole. |

As you can see, an independent appraisal replaces a generic, computer-generated number with a valuation rooted in documented, real-world market evidence.

What a Comprehensive Appraisal Report Includes

A professional appraisal isn’t just a new number—it’s a powerful evidence package. When you hire an expert, you get a detailed report that methodically breaks down your car’s value, leaving the insurance company very little room to argue.

A quality report will always include:

- Detailed Vehicle Inspection: A thorough analysis of your car’s pre-accident condition, noting everything from the paint quality to the tire tread.

- Documentation of Options: A complete list of all factory and aftermarket options, packages, and custom upgrades that contribute to its value.

- Local Market Comparables: A list of several similar vehicles currently for sale at dealerships in your area, complete with photos, VINs, and asking prices.

- Value Adjustments: A clear explanation of how the appraiser adjusted the value based on differences in mileage, condition, and options between your car and the comparables.

- Final Value Conclusion: A certified, defensible Actual Cash Value based on concrete evidence from your local market.

This document is your best negotiating tool.

A Real-World Example of the Difference an Appraisal Makes

Let's look at a real-world case involving a meticulously maintained 2018 Subaru Outback. After a collision, the owner's insurance company declared it a constructive total loss and offered a settlement of $18,500, a figure generated by their software.

The owner knew their car was worth more. It had low mileage, a premium trim package, and a brand-new set of tires. They decided to hire an independent appraiser.

The appraiser conducted a full inspection and did the local market research the insurer skipped. They found three comparable Outbacks for sale within a 75-mile radius, all priced between $23,000 and $24,500. After adjusting for mileage and condition, the appraiser established a fair market value of $23,200.

Armed with this rock-solid report, the owner invoked the appraisal clause in their policy. Faced with indisputable market evidence, the insurance company had no choice but to agree to a higher settlement.

The final payout was $23,200—a $4,700 increase over the initial offer. This isn't just a lucky break; it's what happens when real-world facts go up against an algorithm.

Common Questions About Constructive Total Loss Claims

When your car is badly damaged, the last thing you need is a bunch of confusing insurance jargon. The term “constructive total loss” can be especially baffling, and it’s normal to have a lot of questions.

Let's cut through the noise. Here are some straightforward answers to the questions I hear most often from drivers, designed to help you understand what’s happening and what you can do about it.

Can I Keep My Car if It’s a Constructive Total Loss?

Yes, in almost every case, you have the option to keep your car. The official term for this is "owner retention" or "salvage retention."

Here’s how it works: the insurance company calculates your car’s Actual Cash Value (ACV), then subtracts what they would have gotten for it at a salvage auction. You get a check for the difference, and the car stays with you.

But you need to know what you're getting into.

Once you retain the vehicle, the state DMV will brand its title as "salvage." This is a permanent mark that craters the car's resale value and makes getting full coverage insurance again incredibly difficult, if not impossible.

So, when does it make sense? It's really only a good idea in a few specific situations:

- Unique or Classic Cars: The car has sentimental value that money can't replace.

- DIY Repairs: You’re a skilled mechanic and can fix it yourself for a fraction of what a shop would charge.

- Parting Out: You plan to dismantle the car and sell its components, which are worth more separately than the car as a whole.

For most people with a daily driver, keeping a totaled car is a financial headache waiting to happen.

How Long Does an Insurer Have to Settle My Claim?

There isn't one single deadline for all claims, but insurance companies can't just leave you hanging. Both Washington and Oregon have "prompt payment" laws to protect consumers from unreasonable delays.

Take Washington, for instance. WAC 284-30-370 says an insurer has to get back to you within 15 working days after you’ve sent them everything they need. If you've done your part and all you hear is silence, or they keep giving you the runaround, that’s a major red flag.

Stalling tactics could even be a sign of bad faith. This is often where a solid, independent appraisal can break the logjam. It gives the insurer clear, undeniable evidence of your vehicle's value, forcing them to stop dragging their feet and settle your claim fairly.

What if My Insurer Uses Comps from Hundreds of Miles Away?

This is a classic trick, and frankly, it’s not fair. Insurers often use valuation software, like CCC ONE, that pulls "comparable" vehicles from distant cities or even other states just because they’re cheaper.

But your car's value is local. Think about it: a 4×4 truck in rural Eastern Oregon is going to command a very different price than the exact same one in downtown Seattle.

A professional, independent appraiser grounds their report in reality. They find real-world comps from dealerships in your local area. This gives you powerful leverage to dispute a lowball offer because it reflects what it would actually cost you to replace your car here.

You're owed enough to buy a similar vehicle in your own market, not one from a place you’d need a road trip to get to.

Do I Have to Use the Insurer's Recommended Body Shop?

Absolutely not. It's your car, and it's your choice. Both Washington and Oregon law guarantee your right to take your vehicle to any repair shop you trust.

Insurance companies have networks of "Direct Repair Program" (DRP) shops that agree to their labor rates and procedures. They can suggest these shops, but they can't force you to use them. These programs are set up to control costs for the insurer, which doesn't always translate to the best possible repair for your car. Getting an estimate from an independent shop you trust is always a smart first step.

When you're facing a lowball settlement on your total loss claim, you don't have to accept it. Total Loss Northwest specializes in independent auto appraisals that force insurance companies to pay what you're truly owed. We use real, local market data to prove your vehicle's value, leveling the playing field and putting you back in control. Visit us at https://totallossnw.com to get the fair settlement you deserve.