Yes, auto insurance companies can drop you, and it usually happens for specific reasons like nonpayment, too many claims, accidents, or tickets. It typically happens in one of two ways: a mid-term cancellation or a non-renewal at the end of your policy period.

For most drivers, the letter shows up at the worst possible time. You've already dealt with the accident, the repair estimate or total loss call, maybe a rental issue, maybe missed work, and now your insurer is telling you the policy is ending too.

That creates two separate problems. The first is obvious. You need replacement coverage fast so you don't end up uninsured. The second is the one most articles ignore. If your claim is still open, the same company that no longer wants your risk may also be deciding what your vehicle was worth, whether it's a total loss, and how much to offer for diminished value.

That combination matters more than people realize. When a carrier is tightening underwriting, pushing problem accounts out, or reacting to affordability pressure across the market, your open claim can become one more file they want resolved cheaply and quickly. If you've been dropped after an accident, you should pay close attention not just to the notice, but also to the valuation behind your settlement.

Your Insurer Sent a Notice Now What

The usual scene is simple. You open the mail or your email and see words like “cancellation,” “non-renewal,” or “coverage ending.” Many policyholders read the effective date first, then panic.

That reaction makes sense. Insurance is one of those things you don't think about until the moment you need it. If you're in the middle of a claim, the fear gets sharper because now you're wondering whether the company can still deny, delay, or squeeze your settlement while also cutting ties with you.

What the notice usually means

In practice, these notices often come after a payment issue, a claims pattern, a serious driving event, or a broader underwriting decision. Affordability is a real factor for many households. Fifteen percent of drivers have let their car insurance lapse, and among those who let coverage lapse, 30% said they could not pay, according to AutoInsurance.com's summary of the TransUnion-related report. The same source notes that if a customer misses payments past the grace period, carriers often cancel or non-renew the policy.

If that's your situation, don't treat the notice as just an administrative problem. Treat it as a financial risk event.

Practical rule: If your policy is ending and your claim is still open, separate the coverage problem from the claim-value problem. They overlap, but they aren't the same fight.

The first decisions to make

Start with the paper itself. Read the effective date, the stated reason, and whether the policy is ending now or only at expiration. Then gather every claim document you already have, including the valuation report, repair estimate, photos, adjuster emails, and any payment history.

If the letter arrived after a denial or dispute, it helps to review a grounded checklist for what to do when insurance denies a claim. The steps are similar because both situations require documentation, timing, and a clear record of what the insurer said and when they said it.

A lot of drivers disadvantage themselves by making rushed phone calls and keeping no paper trail. Slow down enough to document everything. Speed matters for replacement coverage. Accuracy matters for the open claim.

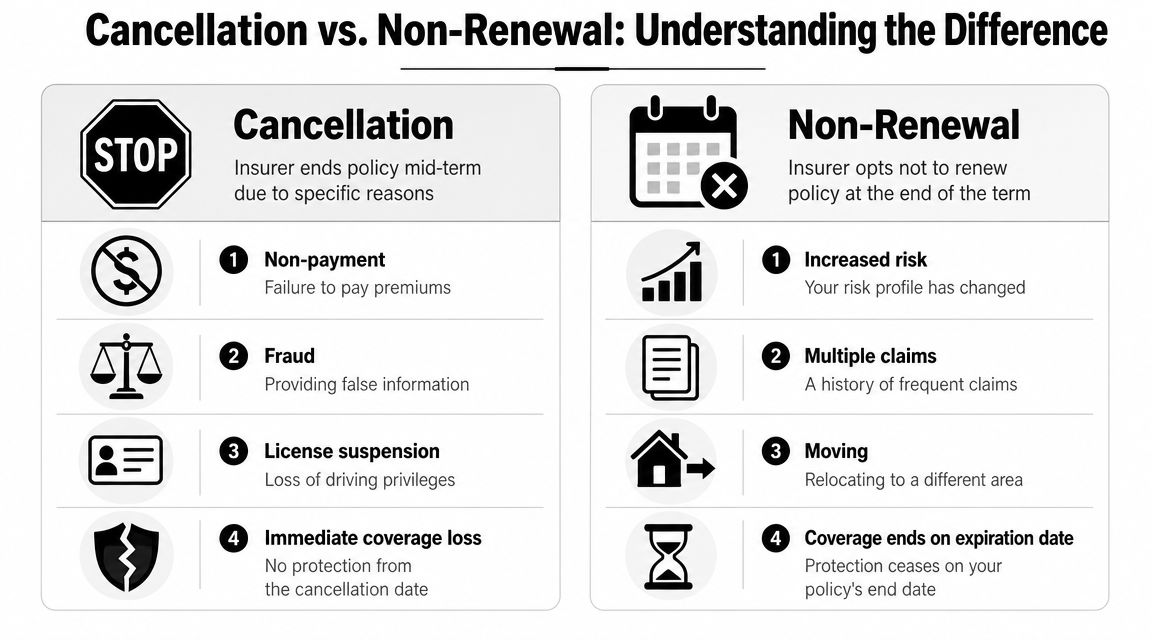

Cancellation vs Non-Renewal Understanding the Difference

A cancellation is the insurer ending the policy before the policy term is over. A non-renewal means the insurer lets the current term run out, then declines to continue coverage.

One is like being removed from a project in the middle of the work. The other is a contract that won't be extended after the current term ends.

Why the distinction matters

The wording changes your timeline, your options, and sometimes your rights under state law. A cancellation often signals something the carrier considers immediate and serious, such as nonpayment or a problem discovered during the policy term. A non-renewal often reflects the insurer's decision that they don't want to keep the account going forward.

For claim handling, that difference matters because a cancellation can create urgency overnight, while a non-renewal can give you at least some time to plan your replacement coverage and organize your claim file.

Cancellation vs. Non-Renewal at a Glance

| Attribute | Cancellation | Non-Renewal |

|---|---|---|

| When it happens | Before the policy term ends | At the end of the policy term |

| Typical trigger | Immediate issue the insurer says justifies ending coverage early | Insurer chooses not to continue the relationship |

| Driver impact | Coverage can stop mid-term | Coverage continues until expiration date |

| Common response | Fix the issue fast if possible and secure replacement coverage | Shop early and compare new offers before expiration |

| Claim concern | Higher urgency if an accident claim is still active | Watch for low settlement pressure as the file closes |

What to look for in the notice

Read the notice like evidence, not junk mail.

- Reason given: Is it specific, or is it vague?

- Effective date: Does coverage end immediately, or at the policy expiration?

- Delivery method: Was it sent the way your state and your policy require?

- Related endorsements or conditions: Did the insurer offer a changed policy, an excluded driver, or some other limited option?

A vague notice is a warning sign. If the insurer can't clearly explain why it's ending coverage, you should be cautious about everything else attached to that file, including valuation decisions.

A lot of people ask, “can auto insurance companies drop you after one accident?” Sometimes the better question is, “what exactly did they send me, and when does it take effect?” That answer controls what you do next.

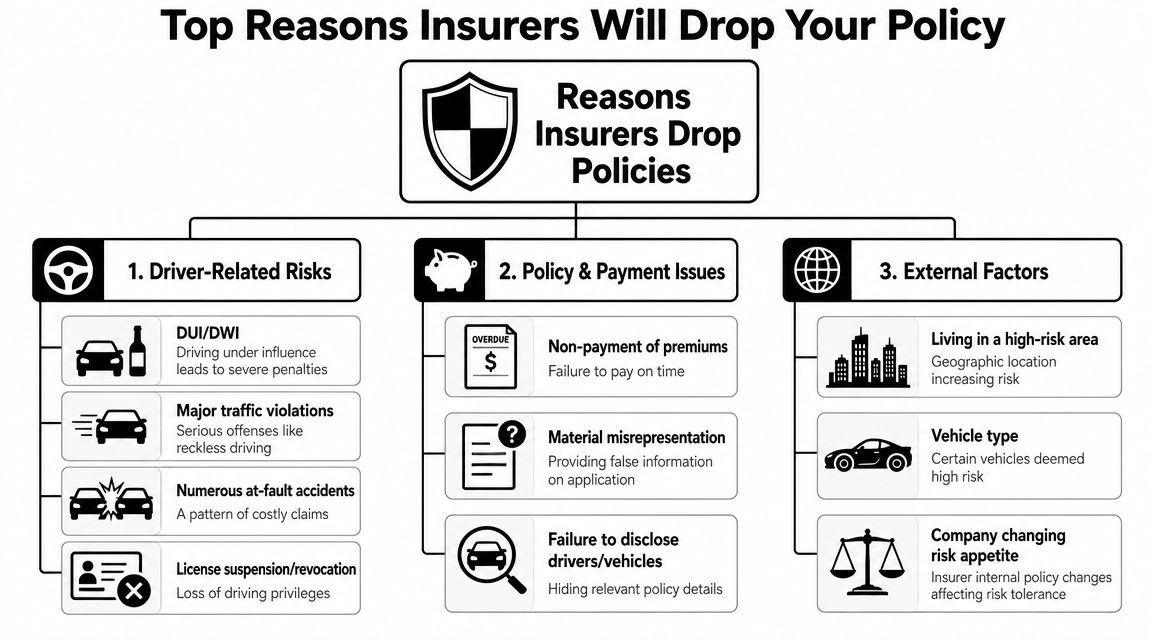

Top Reasons Insurers Will Drop Your Policy

Insurers usually don't end policies randomly. They make risk decisions. Some are obvious. Some now come from data streams drivers never see.

The classic triggers

Accidents, tickets, DUIs, and missed payments are often the first things that come to mind. That's still where many cancellations and non-renewals start.

Common examples include:

- Nonpayment: Missing premiums past the grace period is one of the most straightforward reasons a carrier will end coverage.

- Too many losses: A pattern of claims can move a driver out of a preferred tier, then out of standard-market eligibility.

- Serious violations: DUI, reckless driving, or a suspended license can trigger swift underwriting action.

- Application problems: If the insurer believes key details were omitted or misstated, it may decide the policy shouldn't continue.

If you're trying to understand the premium side of that risk shift, a practical consumer-facing explanation of premiums after an at-fault accident helps show why insurers react so aggressively when they think future losses will cost more.

The modern trigger people miss

Usage-based insurance and telematics programs changed the picture. In usage-based auto insurance, carriers can materially change renewal pricing or even terminate eligibility based on telematics-derived risk scores built from variables that include miles driven, time of day, and phone use, as noted by Consumer Reports on car insurance telematics.

That matters because some drivers think these programs can only help them. That isn't always true. Some programs operate as discount tools. Others can reprice risk upward if the data paints a worse picture than the driver expected.

Data you didn't know could matter

Connected-vehicle data adds another layer. A driver may be claim-free and still look undesirable to an insurer if the broader data profile suggests higher exposure, inconsistent driving habits, or a risk pattern the carrier doesn't like.

Here's what tends to work against consumers:

- Passive consent: Drivers enroll in an app or connected-service feature without understanding how the data may be used later.

- Incomplete review: They check the premium change, but not the program rules for renewal or eligibility.

- Assuming no accident means no problem: Underwriting doesn't always wait for a crash. Sometimes it reacts to predicted exposure.

What doesn't work is arguing only from your own experience. “I haven't filed a claim” may be true and still not answer the insurer's underlying concern.

If your insurer says your driving data affected eligibility, ask what program you were in, what data was considered, and whether the action was a pricing change, a tier change, or a non-renewal decision.

How State Laws Protect You from Unfair Cancellation

Insurers have room to manage risk, but they don't have unlimited freedom. State law usually controls how and when they can cancel or refuse to renew a personal auto policy, and those rules often include notice requirements, permitted grounds, and complaint procedures.

That matters more in a strained market. The U.S. Treasury's analysis of the auto insurance market reported that between 2015 and 2022, personal auto insurers generally experienced underwriting losses and rising premiums became a significant budget burden for consumers. Treasury also noted broader pressure in pricing and underwriting during that period. When carriers are under stress, they tend to tighten standards. That doesn't erase your rights.

What protections usually look like

State protections vary, but drivers commonly have the right to know:

- Why the policy is ending

- When the action takes effect

- How to challenge an error

- Where to file a complaint with the state regulator

Some states also restrict carriers from using certain reasons or from taking action without proper notice. Others distinguish sharply between mid-term cancellation and end-of-term non-renewal.

Where drivers make mistakes

The biggest mistake is assuming that if the insurer sent a notice, the notice must be valid. Not necessarily. The second mistake is focusing only on getting new coverage and ignoring whether the original carrier followed the rules.

Use a simple review standard:

| Question | Why it matters |

|---|---|

| Did the notice state a clear reason? | You need to know whether the action is legally and factually supportable. |

| Did it give enough time? | Timing affects your ability to replace coverage and challenge errors. |

| Is the stated reason accurate? | Wrong claims history, wrong driver information, or wrong payment data can be challenged. |

| Did the insurer follow your state complaint process? | If not, you may have grounds to contest the action. |

The insurer's financial pressure is real. Your legal protections are real too. Don't let the first one convince you the second one doesn't exist.

If the notice contains a factual error, dispute the error in writing. If the notice appears improper, contact your state department of insurance. Do both while you shop for replacement coverage. One protects your rights. The other protects your ability to keep driving legally.

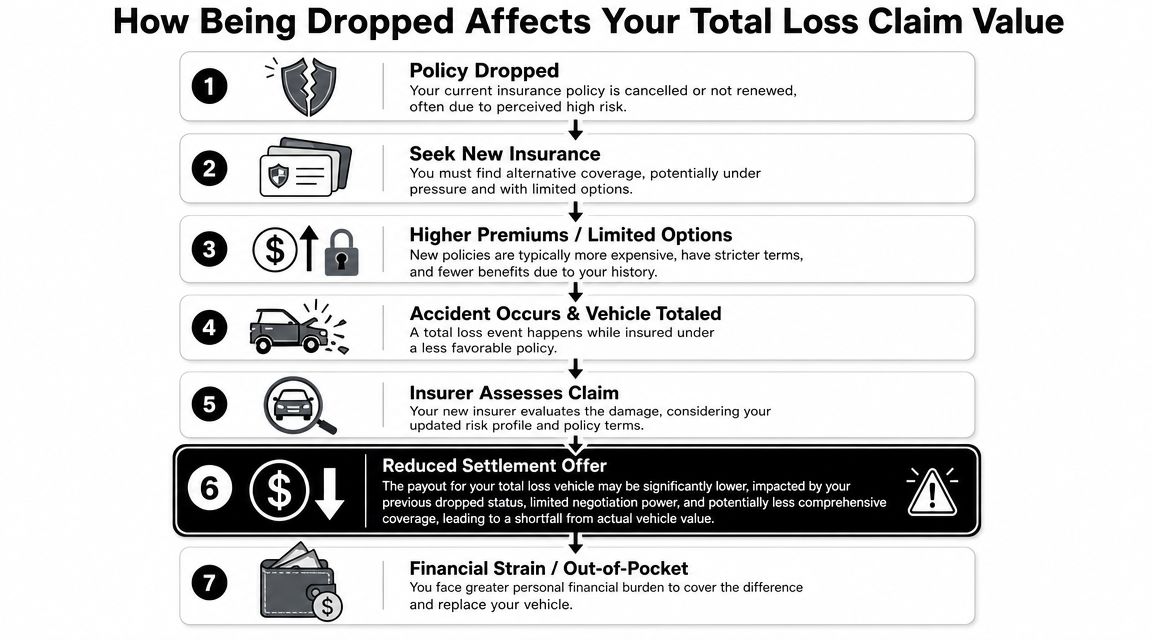

The Critical Link Between Being Dropped and Your Claim Value

This is the part most drivers never get warned about.

A policy-ending notice doesn't automatically prove the insurer will undervalue your claim. But when a carrier is both closing out the relationship and evaluating your vehicle's value, the risk of a weak settlement offer becomes more serious. That's especially true in total loss and diminished value claims, where the number often depends on valuation methods, condition adjustments, comparable vehicles, and software-driven assumptions.

Why the risk goes up during an open claim

A major gap in most consumer content is that it rarely addresses what happens to the value of the vehicle and the claim outcome when a driver is dropped after an accident, including how cancellation can affect a pending valuation dispute or the use of appraisal clause protections, as noted in Progressive's discussion of whether car insurance can drop you.

In plain terms, the incentive problem is obvious. If the insurer has already decided you're not a customer it wants to keep, there's less relationship value to preserve. That can show up in very practical ways:

- Thin comparable selections

- Condition adjustments that lean low

- Overreliance on valuation software

- Resistance to owner-supplied market evidence

- Pressure to settle before you review the basis of value

What to watch for in a total loss or diminished value file

Look closely if any of these happen around the same time as a cancellation or non-renewal notice:

- The valuation arrives fast, but the support is weak

- Your local market listings are dismissed without much review

- The adjuster won't explain mileage, options, or condition adjustments

- The carrier pushes a release before answering value questions

That doesn't mean every low offer is bad faith. It does mean you should treat the valuation as a technical document that deserves independent scrutiny.

When the insurer says the number is “market value,” ask which market, which vehicles, what adjustments, and why those adjustments were used.

If you're already getting pushback from an adjuster, this guide on how to fight an insurance adjuster gives a useful framework for documenting the dispute and forcing clarity.

The appraisal clause is often the pressure point

For many policyholders, the strongest tool isn't arguing louder. It's moving the value dispute into the appraisal clause process when the policy allows it. That changes the conversation from “accept our number” to “show the evidence and let competing appraisers test it.”

In real claim work, that's often what separates frustration from an advantage.

Your Action Plan After a Cancellation or Non-Renewal

When the notice lands, don't try to solve everything in one call. Work the problem in order. Coverage first. Documentation second. Claim value third. Then circle back if you need to challenge the insurer's stated reason.

A simple checklist helps because this situation creates panic, and panic makes people miss deadlines.

The first moves to make

Read the notice word for word

Don't rely on memory. Confirm whether it says cancellation or non-renewal, and note the exact effective date.Ask for the reason in writing if it isn't clear

A phone rep summary isn't enough. You want the insurer's stated basis in a form you can keep.Start shopping for replacement coverage immediately

Even if you plan to dispute the insurer's action, don't gamble on driving uninsured.Pull your claim file together

Keep the valuation report, adjuster emails, vehicle photos, estimates, and any market comps in one folder.

The video below gives a general consumer overview that can help you stay organized while you move quickly.

Protect your claim while you replace coverage

A technical issue many people miss is how telematics and connected-vehicle data can flow through third parties and create a second-order underwriting signal. Smartcar's discussion of data-driven car insurance notes that a claim-free driver can still be flagged if the data profile suggests higher exposure, which can contribute to non-renewal.

That means your action plan should include data review, not just quote shopping.

- Check enrolled apps and connected services: If you joined a driving-score or connected-car program, review what data access you granted.

- Request underwriting clarity: Ask whether telematics, third-party data, or connected-vehicle data played any role in the action.

- Don't let claim deadlines slide: A policy dispute can distract you from a low total loss or diminished value offer.

- Escalate denial issues separately: If your open file starts turning into a denial fight, these steps to appeal a denied claim give a practical legal roadmap.

Keep two timelines on paper: one for replacing coverage, one for preserving claim rights. Mixing them together is how drivers miss something important.

When to file a complaint

If the notice is vague, factually wrong, or appears inconsistent with your state's rules, file a complaint with your department of insurance. Do it with attachments. Include the notice, your policy page, relevant emails, and a short chronology.

Complaints don't always reverse the decision. They do force a documented response, and that record can matter.

Finding New Coverage and Rebuilding Your Insurability

Once the immediate fire is under control, focus on the next policy and the record you're building from this point forward. Some drivers will still qualify for standard-market coverage. Others may need a specialty or high-risk carrier for a while.

The key is continuity. Keep coverage in force, pay on time, and avoid giving the next insurer a fresh reason to worry. If the prior policy ended after an accident, also watch the details of the new policy. Deductibles, valuation language, endorsements, and optional coverages matter more when you've already seen how hard a claim can become.

If your vehicle has unusual history, rebuilt status, or a title issue, practical consumer guidance on expert guidance on category vehicle cover is useful because it shows how underwriting can change when a vehicle falls outside the easiest risk box. Different market, same lesson. The more unusual the vehicle or risk profile, the more carefully you need to read the policy.

If you're changing insurers by choice or necessity, this walkthrough on how to switch car insurance companies can help you avoid a gap while you rebuild.

Recovery takes time, but it's manageable. Clean payments, a stable coverage history, and fewer underwriting surprises are what gradually move you back into better options.

If you're dealing with a non-renewal or cancellation while a total loss or diminished value claim is still open, Total Loss Northwest can help you focus on the number that matters most: your vehicle's actual value. They provide independent total loss and diminished value appraisals and can invoke the Appraisal Clause to challenge low insurance valuations with market-based evidence.