You open the envelope, see the settlement check, and your first reaction isn't relief. It's suspicion. Do I owe the IRS part of this?

That question comes up all the time after a crash, especially when your car is declared a total loss or you receive money for diminished value after repairs. Most drivers aren't trying to game the tax system. They just want to know whether this payment is reimbursement for what they lost, or income the government will treat like a gain.

The easiest way to think about insurance settlement taxes is this: the IRS usually cares less about where the money came from and more about what the money is replacing. If the payment is restoring something you lost, the tax result is often different than if the payment gives you something extra, like interest or compensation that stands in for wages.

That distinction matters most in auto claims because one settlement can contain several pieces. Part may be for the vehicle. Part may be for medical treatment. Part may be for lost time from work. Part may be interest added because payment took a while. Those pieces don't always get the same tax treatment.

If you're dealing with a totaled car, a low valuation, or a diminished value claim after repairs, this guide will walk through the rules in plain English and keep the focus on everyday auto settlements.

Is Your Insurance Settlement Check Taxable?

The short answer is sometimes.

The longer answer is more useful. A settlement check after a car accident isn't automatically taxable just because it looks like income. In many cases, it is replacing value you already had before the wreck. Your car had value on Monday. Someone hit it on Tuesday. The insurer paid you on Friday. That payment may just be restoring what was taken away.

What the IRS is really asking

A practical way to frame it is this:

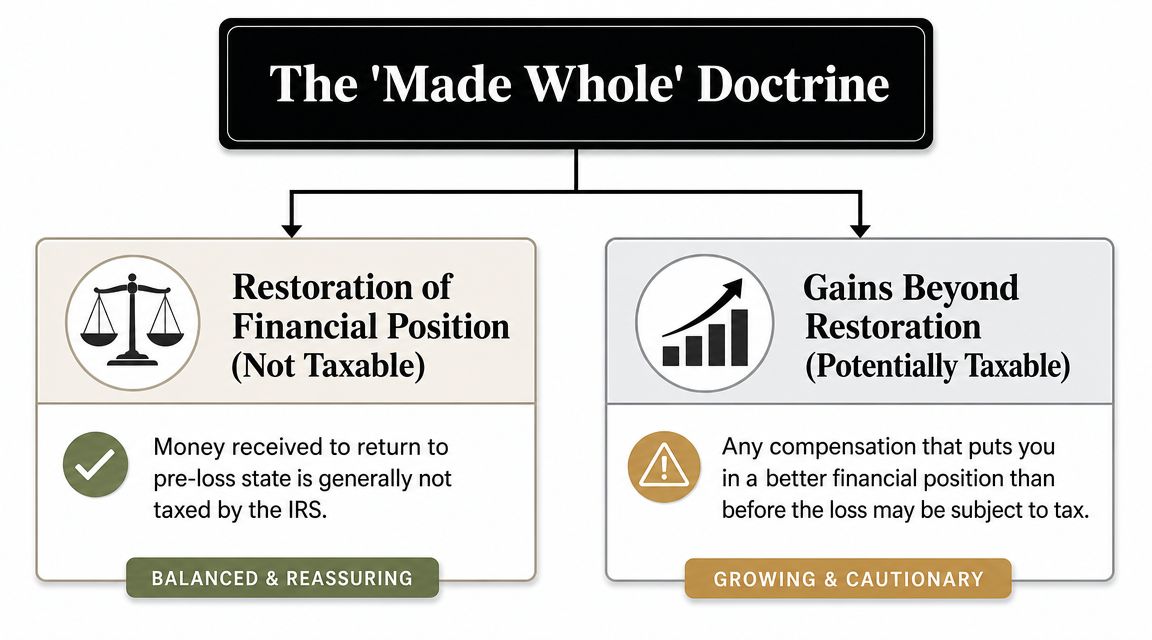

- If the payment makes you whole, it's often treated differently than taxable income.

- If the payment goes beyond making you whole, that extra amount is where tax questions usually start.

- If the settlement includes mixed categories, you may have both taxable and non-taxable parts in the same claim.

For vehicle owners, this shows up most often in two situations.

First, a total loss claim. The insurer says your vehicle is worth a certain amount and sends payment instead of paying for repairs. If you want a clearer picture of how insurers reach that value, this explanation of actual cash value in auto insurance helps connect the valuation process to the tax question.

Second, a diminished value claim. Your car gets repaired, but the market still sees it as worth less because it now has an accident history. That payment is usually aimed at restoring part of the value you lost, not creating new income.

Practical rule: Don't ask, "Was this an insurance payment?" Ask, "What loss was this payment meant to cover?"

Why people get confused

Drivers often assume all accident settlements are tax-free. Others assume every check from an insurer has to be reported. Both views are too broad.

Confusion usually starts because settlement paperwork doesn't always separate the pieces clearly. A check can look like one lump sum even when it really covers several categories. If you're not careful, you can miss the fact that one part may be treated differently from another.

That is why the paperwork matters almost as much as the payment itself.

Understanding the Made Whole Doctrine

The clearest mental model for insurance settlement taxes is the made whole idea. Imagine replacing a broken window. If someone hands you enough money to put the same window back in place, you haven't come out ahead. You've just returned to where you started.

That basic logic sits underneath a lot of accident-settlement tax treatment.

Restoration versus gain

If a driver receives money for physical injuries from a crash, federal tax law starts with a major rule in Internal Revenue Code Section 104. The IRS says damages received “on account of personal physical injuries or physical sickness” are excluded from gross income, and it also explains that the modern rule was narrowed by the 1996 tax law change so that mental and emotional distress is excludable only when it arises from physical injury or physical sickness, as described in the IRS guidance on tax implications of settlements and judgments.

That same logic helps drivers understand property claims. The tax line usually isn't about whether the money came from an insurer. It's about whether the payment is replacing a loss or creating a financial gain.

A simple car-claim analogy

Suppose your vehicle was worth one amount before the crash and the collision reduced that value. If the settlement fills that hole, the payment is acting like reimbursement.

Now compare that with money added because payment was delayed. That extra amount isn't restoring your car. It's extra compensation tied to time. The IRS often treats that differently.

Or take lost wages after an injury. That part isn't replacing vehicle value. It's standing in for income you would have earned. Again, different purpose, different tax treatment.

When you sort a settlement by purpose instead of by check size, the tax rules make a lot more sense.

Where drivers trip up

The made-whole idea is simple, but applying it can get messy fast. People mix up three different questions:

- What was damaged

- What the insurer paid for

- Whether the payment replaced loss or added gain

A total loss payment may feel like a windfall if the check is large, but size alone doesn't decide tax treatment. The same goes for diminished value. A smaller payment isn't automatically non-taxable just because it seems modest. Purpose matters more than appearance.

That is why clear claim language, appraisal support, and settlement breakdowns matter. They help show whether the money restored prior value or compensated you for something else.

Taxable vs Non-Taxable Settlement Components

A single accident claim can contain parts that are treated differently for tax purposes. Due to this, many drivers make mistakes. They look at the check as one item when the IRS may look at it as several.

A practical benchmark is that interest is taxable as ordinary income, lost income is typically taxable because it replaces wages, and previously deducted medical expenses can become taxable to the extent you already received a prior tax benefit, while reimbursement for bodily injury-related medical costs is usually excluded when it restores out-of-pocket loss, as explained in this discussion of why a car accident settlement might be taxable.

Tax treatment of common settlement components

| Settlement Component | Generally Taxable? | Reason |

|---|---|---|

| Vehicle repair or replacement payment | Usually no | It typically reimburses property loss rather than creating new income |

| Diminished value payment | Usually no | It generally compensates for lost market value after the crash |

| Medical reimbursement tied to bodily injury | Usually no | It usually restores out-of-pocket loss connected to physical injury |

| Pain and suffering tied to physical injury | Often no | It is generally treated under the physical injury framework described earlier |

| Interest on the settlement | Generally yes | Interest is typically treated as ordinary income |

| Lost wages or lost income | Generally yes | It replaces earnings that would normally be taxable |

| Punitive damages | Typically yes | It goes beyond making you whole and is generally treated as taxable |

| Reimbursement for medical expenses you already deducted and benefited from | Potentially yes | Prior tax benefit can make that portion taxable |

How to read your own settlement

Don't focus only on the final number. Focus on the labels and support documents.

Look for these clues:

- Settlement agreement language: If it separates property damage, medical payments, interest, and wage loss, that helps.

- Claim correspondence: Emails and letters often describe what the insurer believed it was paying.

- Check stubs and payment summaries: These sometimes break out categories even when the front of the check doesn't.

- Appraisal reports: In total loss and diminished value disputes, valuation documents help show the payment was tied to vehicle value.

The part that surprises people

The same case can produce two different tax answers.

For example, a driver might receive money for bodily injury treatment and also receive interest because the case took time to resolve. One portion may be excluded while the interest portion is taxable. Another driver may get property damage reimbursement and a separate amount for lost wages. Again, different treatment inside one settlement.

Key takeaway: A settlement isn't one tax category. It's a bundle of categories.

This is also why a vague lump-sum agreement can create headaches later. If the paperwork never shows what each portion was for, you may have a harder time defending the tax treatment you claim on your return.

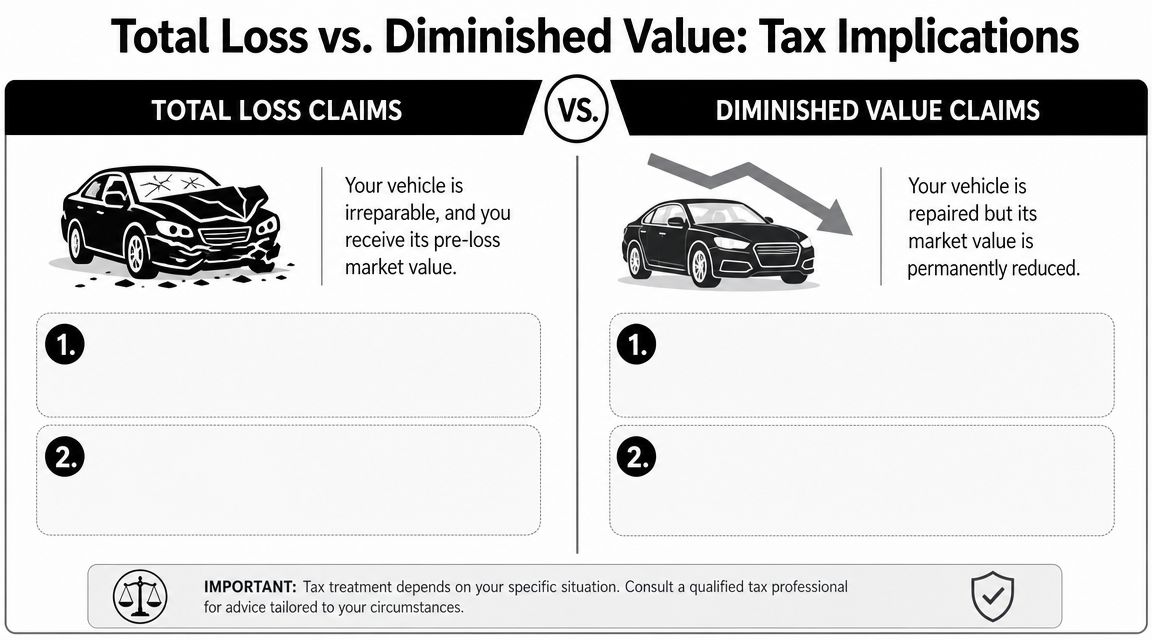

How Taxes Apply to Total Loss and Diminished Value

Here's how the rule applies in practice. Total loss claims and diminished value claims feel similar because both arise from the same accident, but they don't work the same way.

A total loss payment is usually meant to compensate you for the vehicle's pre-loss value. A diminished value payment is usually meant to cover the drop in market value that remains after repairs. If you need a closer look at how a post-repair claim works, this page on automobile diminished value gives useful background.

Example one with a total loss claim

Start with a simple framework. Ask two questions:

- What was your basis in the vehicle?

- How much did you receive for the loss?

Your basis is usually what you paid for the vehicle, adjusted for major changes that affect value in a tax sense. For everyday drivers, the useful point isn't advanced tax accounting. It's keeping proof of what the vehicle cost you and what the insurer paid.

Here is the math in plain form:

- If settlement is less than or equal to your basis, you're usually being reimbursed for loss.

- If settlement exceeds your basis, the excess may raise a tax issue.

Say you bought a car for one amount and after the accident the insurer pays an amount that does not exceed what you had invested in that vehicle. In that situation, the payment generally looks like restoration, not gain.

Now change the facts. Suppose your basis in the vehicle is lower than the settlement amount because of prior circumstances in your tax records. The amount above basis may be treated differently. That is one of the few total-loss situations where a personal vehicle claim can turn into a real tax question.

Example two with a diminished value claim

Diminished value usually lands closer to reimbursement.

Your car is repaired, but buyers often won't value it the same way they would a comparable car with a clean history. A diminished value payment is meant to compensate for that lost market value. In plain English, the insurer is trying to pay for the dent left in your car's resale position, even after the bodywork is done.

That usually fits the made-whole idea better than a gain idea. You had a car with one market position before the wreck. After the wreck and repair, the market position dropped. The payment is intended to fill that gap.

Why appraisals matter in both situations

Tax treatment often depends on being able to show what the payment was really for.

For a total loss dispute, a proper valuation report helps document the vehicle's fair market position before the accident. For diminished value, an appraisal supports the argument that the payment reflected a measurable loss in resale value rather than extra income.

That documentation matters if the insurer's breakdown is thin or if you ever need to explain the claim later.

The cleanest way to think about both claims

Use this quick comparison:

- Total loss claim: You are being paid for the car itself because it can't reasonably return to its prior condition.

- Diminished value claim: You still have the car, but you lost part of its market value because the accident history stays with it.

- Tax concern in either case: The issue is whether the payment restored prior value or exceeded it in a way that created a gain.

For most everyday auto claims, that distinction points back to reimbursement. But if your facts are unusual, especially if the numbers around basis and settlement don't line up cleanly, don't guess.

Filing Your Taxes After a Settlement

Once tax season arrives, most drivers want a straightforward answer: Do I report this or not?

In many routine car-accident situations, the non-taxable portion of a settlement isn't something you report as income. The harder part is not filing more. It's filing correctly when one part of the payment was taxable and another part wasn't.

A good first move is to organize the claim before you open your tax software.

Your record-keeping checklist

Save every document connected to the loss and settlement:

- Settlement agreement: This is the best evidence of what the payment covered.

- Insurance letters and emails: They often show whether amounts were for property damage, interest, or wage replacement.

- Repair invoices and photos: Useful for diminished value and for showing what happened to the vehicle.

- Purchase records for the car: Keep the bill of sale, financing paperwork, and any records that help establish basis.

- Appraisal or valuation reports: These support total loss value and diminished value calculations.

- Tax documents received later: If any reporting form arrives, don't ignore it.

If you struggle to keep these papers organized, even a simple digital worksheet can help you automate data entry for finances and keep claim-related records in one place.

Reporting when a taxable portion exists

If part of the settlement is taxable, the reporting method depends on what that part represents. Interest is commonly handled as income. A gain tied to property can raise different reporting questions. Some taxpayers may encounter forms such as Schedule D (Form 1040) or Form 4797, depending on the nature of the transaction and how the property is classified.

That doesn't mean every accident claimant needs those forms. It means you shouldn't assume a single reporting path fits every case.

Here is a short explainer if you want a visual overview before sorting your documents:

What not to do

Don't report the full settlement as income just because you received a check. And don't ignore a payment category that was clearly taxable because you assumed all insurance money is exempt.

Keep the paper trail stronger than your memory. Months later, the documents will be more reliable than your recollection of what the adjuster said on the phone.

If your paperwork is unclear, fix that before you file. Waiting until after the return is submitted makes everything harder.

Do State Insurance Settlement Taxes Apply?

Federal rules usually drive the conversation, but state taxes can still matter.

Many states use their own income tax systems and often track the federal approach in broad strokes. That means a payment treated as non-taxable reimbursement at the federal level is often handled similarly at the state level. Still, "often" is not the same as "always."

What drivers in the Pacific Northwest should know

For drivers in Washington and Oregon, the practical starting point is usually the federal treatment. Those states generally don't create a completely separate theory for auto settlement payments that overturns the basic reimbursement-versus-gain analysis.

That said, state tax treatment can still depend on your specific facts, the character of the payment, and whether your settlement includes elements such as interest or income replacement.

A safe way to think about it

Use a two-layer check:

- Federal first: Identify whether each piece looks like reimbursement or taxable income.

- State second: Confirm whether your state follows that treatment or has its own reporting wrinkle.

If you moved during the year, run a business from your vehicle, or have a mixed personal and business use situation, the state side can get more complicated.

The key point is simple. Don't stop at the IRS question if your state has an income tax system that may also apply.

When to Consult a Tax Professional or Appraiser

Most routine property-damage settlements don't require a full legal team and a stack of memos. But some claims deserve professional help right away because the risk of getting the tax treatment wrong is higher.

The biggest red flags are easy to spot once you know what to look for.

Call a tax professional when these issues show up

- Lost wages are part of the settlement: That piece often needs separate treatment because it stands in for taxable earnings.

- Interest was added: Even when the main settlement is non-taxable, interest can change the filing picture.

- Punitive damages appear in the paperwork: That is a clear sign not to rely on guesswork.

- The settlement may exceed your vehicle basis: This is one of the main ways a property claim can move from reimbursement into possible gain territory.

- You receive tax forms you didn't expect: Never assume a form is wrong just because the claim felt non-taxable.

If your situation spills into a legal gray area, outside help can save time and stress. For more complex disputes or allocation questions, some drivers benefit from expert tax attorney guidance instead of trying to interpret settlement language alone.

Why an appraiser belongs in the conversation

An appraiser doesn't replace a tax professional. The roles are different.

A tax professional interprets the tax consequences. An appraiser helps establish what the vehicle was worth, what it lost in value, and whether the insurer's position is supported by the market. That matters because tax treatment often depends on proving the payment was tied to actual loss.

If you're not sure what that process involves, this overview of what an appraisal for a car is is a useful starting point.

Where documentation and valuation meet

A strong appraisal can do two jobs at once:

- support your settlement position with the insurer

- create a clear record showing the payment related to vehicle value

That is especially useful in total loss and diminished value disputes, where the insurer's internal valuation may not explain the market as clearly as an independent report. In those situations, a firm such as Total Loss Northwest can provide appraisal documentation for total loss and diminished value claims, while a CPA, enrolled agent, or tax attorney handles the return itself.

A tax preparer can tell you how to report a number. An appraiser helps prove why that number was justified in the first place.

If your settlement paperwork is clean, your records are complete, and the payment clearly looks like reimbursement, you may never need to escalate. If the claim includes mixed categories, unclear allocations, or unusual property-basis issues, professional help is money well spent.

If you're dealing with a low total loss offer or trying to document diminished value after an accident, Total Loss Northwest provides independent auto appraisals that can help clarify your vehicle's market value and support the records you keep for settlement and tax purposes.