You open the claim email expecting a hard conversation. You don't expect an offer that makes no sense.

Your truck was clean before the crash. The mileage was reasonable. You kept it maintained. Maybe you added wheels, a canopy, premium audio, recent tires, or documented repairs that improved condition. Then the insurer sends a total loss valuation or diminished value offer that feels detached from your actual vehicle and your local market. The number isn't just disappointing. It feels careless.

That reaction matters. A low offer by itself doesn't automatically create a bad faith insurance claim, but it often marks the moment when owners realize the carrier may not be handling the file fairly. In auto claims, the fight usually isn't won by outrage. It's won by evidence, chronology, and a valuation record that exposes what the insurer did wrong.

As a practical matter, most vehicle owners don't need more legal jargon. They need to know what to look for in the report, what to save, what to request in writing, and when an independent appraisal changes the negotiating power. That's where this issue moves from frustration to strategy.

That Sinking Feeling Your Settlement is Unfair

The pattern is familiar. Your vehicle is declared a total loss. The adjuster sounds confident. They say the valuation is based on market data, approved methods, and comparable vehicles. Then you review the report and start spotting problems.

One comparable has higher mileage adjustments than you'd expect. Another is a different trim. A third isn't even equipped like your vehicle. Your recent maintenance isn't reflected. The condition rating looks generic. If this is a diminished value claim, the offer may feel even thinner, as if the accident history barely matters.

Why the offer feels personal

For most owners, a car isn't just a line item. It's a work vehicle, a family hauler, a carefully maintained asset, or a collector piece with features the software didn't capture. So when the settlement comes in low, the first instinct is often, “They're not listening.”

That instinct is sometimes right.

What drivers call “being lowballed” can come from several causes. Some are simple errors. Some are rushed file handling. Some involve an insurer leaning too heavily on valuation software, incomplete condition data, or weak comparable selection. And in the worst cases, it becomes more than a valuation dispute. It becomes a trust problem tied to how the claim was investigated, explained, and processed.

When the insurer can't clearly explain how it reached the number, you shouldn't assume the number is correct.

What this usually means in real life

A bad faith dispute rarely starts with dramatic language. It starts with ordinary moments:

- The unexplained offer that arrives with no useful breakdown.

- The repeated delay while your storage bill grows or your rental ends.

- The moving target where the adjuster gives one reason on Monday and another on Thursday.

- The dismissive response when you send better comparables or repair records.

That's why the right response is calm, organized, and detailed. If you feel wronged, don't argue from emotion alone. Build a file that shows what your vehicle was worth, what the insurer relied on, and where the handling stopped being reasonable.

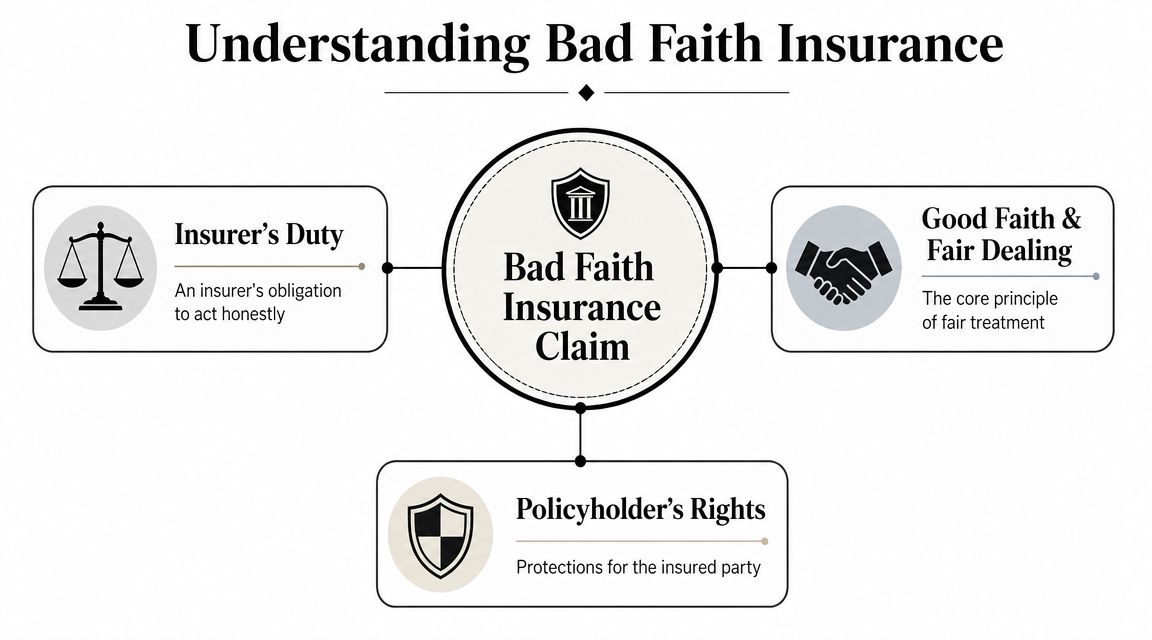

What Exactly Is a Bad Faith Insurance Claim

Insurance isn't just a payment arrangement. It carries a duty of good faith and fair dealing. In plain English, the insurer has to investigate, evaluate, and respond fairly and reasonably when a covered claim is presented. That doesn't mean they must agree with every owner's valuation. It means they can't handle the claim in a way that falls outside reasonable claims practice.

A key legal milestone changed how courts viewed that duty. A multi-state survey of bad faith law explains the historical shift from treating insurer misconduct mainly as a contract issue to recognizing a separate tort duty, noting the landmark 1959 California Supreme Court case Gruenberg v. Aetna Ins. Co. as part of the framework that established modern bad faith doctrine. That matters because bad faith became about unreasonable claim handling, not just failure to pay.

A simple way to think about it

Treat the policy like an agreement where both sides owe something. You pay premiums and cooperate with the claim. The insurer doesn't just process paperwork. It has to evaluate the loss fairly, explain its position, and avoid unreasonable delay or arbitrary denial.

That distinction matters because not every low number is bad faith.

A legitimate dispute can happen when two qualified people look at the same vehicle and disagree on trim, condition, prior damage, or market comparables. Bad faith starts to enter the picture when the carrier ignores known facts, refuses to reassess, withholds a real explanation, or leans on a process that no reasonable adjuster should trust without further review.

Disagreement versus unreasonable conduct

Here's the practical difference:

| Situation | More likely a valuation dispute | More likely bad faith concern |

|---|---|---|

| Comparable vehicles differ slightly | Yes | Not by itself |

| Condition adjustments are debatable | Yes | Not by itself |

| Insurer refuses to explain the valuation | Sometimes | Often a warning sign |

| Submitted records are ignored without response | No | Stronger concern |

| Delay continues after the insurer has enough information | No | Stronger concern |

If you're in Florida and want a legal overview of how these duties are described in practice, Oldham Law PLLC offers guidance on Florida bad faith insurance that helps frame the issue from the policyholder side.

Practical rule: A bad faith insurance claim usually turns on conduct, not just the final dollar amount.

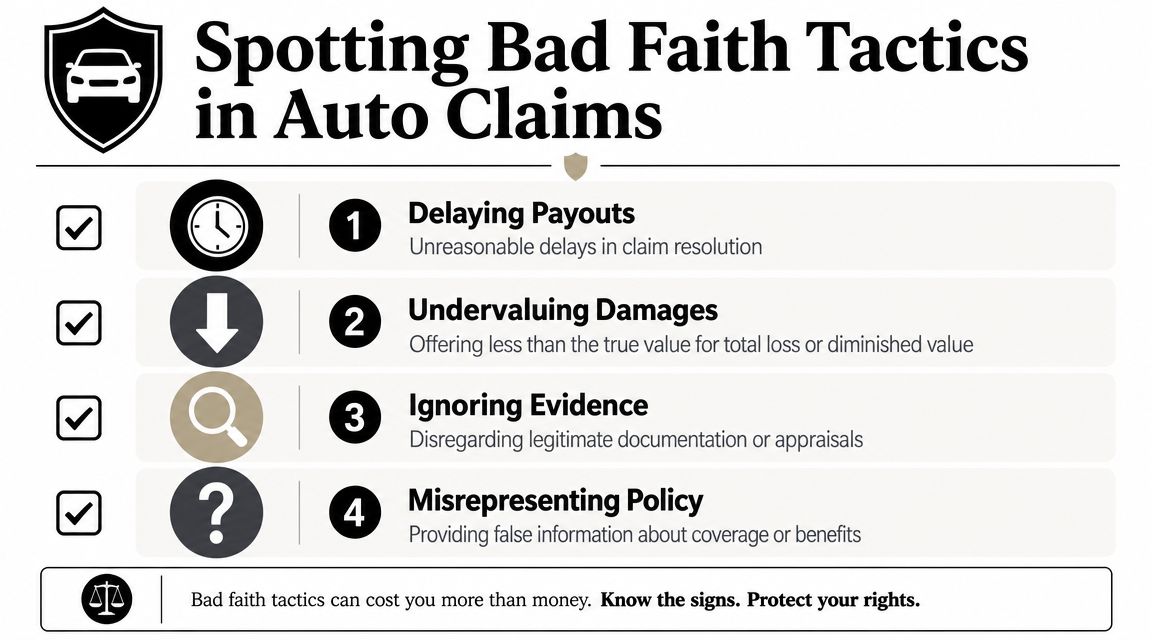

Common Bad Faith Tactics in Auto Claims

Most bad faith articles stay general. Auto claims are more specific. The pressure points usually show up inside the valuation report, the claim timeline, and the adjuster's response when you challenge either one.

Tactics that show up in total loss and diminished value files

Bad comparables: The insurer uses vehicles that don't match your trim, options, drivetrain, condition, or local market. A report can look polished and still be wrong at the comparison level.

Mechanical condition reduced to a template: Many reports apply broad condition ratings that don't reflect documented maintenance, recent parts, or above-average care.

Upgrades treated like they don't exist: Custom wheels, suspension work, audio equipment, bed caps, specialty accessories, or collector-grade details often get little attention unless the owner forces the issue with documentation.

No meaningful explanation for deductions: You'll sometimes see adjustments applied without a clear narrative tying them to actual facts about your vehicle.

Delay as leverage

Delay is one of the oldest tactics because it creates pressure without saying “accept less.” If you need transportation, storage charges are accruing, or a lender is waiting, the carrier knows time hurts you more than it hurts them.

In practice, that looks like repeated requests for documents they already have, slow responses after you send supporting records, or a promise to “review” the dispute with no clear deadline. Delay alone doesn't prove bad faith, but delay combined with a thin investigation is where problems deepen.

Software isn't neutral just because it's software

Insurers now rely heavily on automated tools for claim triage, vehicle valuation, and repair estimating. That changes how owners should look at the file. The issue isn't just whether the result is low. It's whether the method used to produce the result was reasonable and transparent.

A legal industry analysis from Wiley notes that regulators have focused on algorithmic transparency and that the NAIC adopted a model bulletin in 2024 on AI use in insurance, highlighting concerns about how automated systems can affect outcomes and how flawed comparable selection may reduce total loss payouts in particular (Wiley analysis of AI and bad faith issues).

That matters in auto claims because owners can challenge the methodology, not only the number.

What this looks like on the page

When I review insurer valuations, I look for patterns more than labels. A few examples:

- A “comparable” that is technically for sale but not meaningfully comparable.

- A condition adjustment that assumes average wear despite records showing recent work.

- A trim or package mismatch that drags value down.

- A total-loss methodology that depends so heavily on software output that no one appears to have sanity-checked the result.

If you want a deeper grounding in how insurers calculate vehicle value in these disputes, this explanation of actual cash value in auto insurance claims helps clarify where low offers often begin.

A low offer becomes more suspicious when the insurer can't defend the assumptions behind the software report.

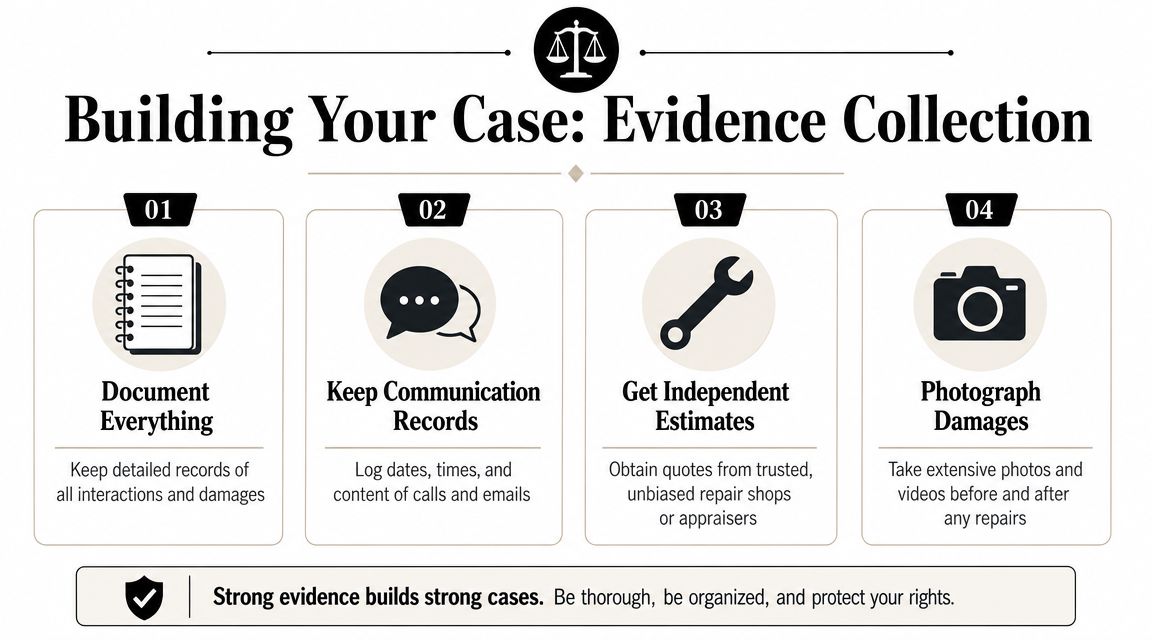

How to Build Your Evidence Against the Insurer

Bad faith cases are built backwards. People focus on the lowball number, but the stronger proof is usually the file trail that came before it.

The core issue in many first-party claims is whether the insurer lacked a reasonable basis for denial or delay. That's why documentation matters so much. A legal explainer on bad faith elements describes the strongest record as a closed-loop file containing the policy, proof of loss, emails, call logs, valuation materials, and other records showing the carrier had enough information to pay fairly but didn't (closed-loop file guidance for bad faith proof).

What to collect right now

Start with the file you control.

- Your policy documents: Save the declarations page and policy language, especially any section dealing with valuation disputes or appraisal.

- Every valuation report: Don't settle for a summary number. Request the full report, including comparables and adjustments.

- All communication records: Keep emails, letters, text messages, and voicemail screenshots.

- Call notes: Log the date, time, representative name, and what was said after every phone call.

- Vehicle proof: Gather maintenance invoices, option lists, photos before the loss if you have them, and receipts for recent parts or upgrades.

The timeline often wins the argument

Chronology gives context to everything else. If you sent maintenance records on one date, the adjuster acknowledged them on another, and the final valuation still ignored them, that sequence matters. If the carrier changed its explanation after you challenged a bad comparable, that matters too.

A short timeline can be more persuasive than a long complaint. Build one page that shows:

- when the loss happened,

- when the insurer inspected or valued the vehicle,

- when you requested the full report,

- when you sent supporting documents,

- when the insurer responded, or failed to.

Put verbal claims into writing

Many auto claim disputes get muddy because the most important statements were made by phone. Fix that immediately. After every call, send a short email confirming what you were told.

For example: “This email confirms our call today. You stated the insurer would review the comparable vehicle concerns and respond in writing.” That one sentence can become important later if the file starts drifting.

Keep asking for written explanations. Clear writing forces clearer claim handling.

Using an Independent Appraisal to Fight Back

When the valuation itself is the battleground, opinion alone won't move the claim. You need counter-evidence that is structured, documented, and hard to dismiss. That's what an independent appraisal does.

Why appraisals change the conversation

An insurer's valuation often starts with software and a rapid review process. A certified independent appraiser starts with the actual vehicle, its equipment, condition, market position, and the quality of the insurer's comparables. Those are not the same exercise.

A strong appraisal report does several things at once:

- identifies mismatched comparables,

- corrects trim, options, or condition errors,

- explains local market realities,

- documents supporting evidence in a format that can survive scrutiny.

That's why the appraisal is more than a second opinion. It becomes the working proof behind your dispute.

The appraisal clause matters

Many auto policies include an appraisal clause for value disputes. Owners often don't know it exists until the insurer has already framed the number as final. It usually gives each side the right to select an appraiser, with a process for resolving disagreements through an umpire if needed.

That matters because it shifts the dispute away from one-sided internal review. Instead of begging the carrier to “take another look,” you're invoking a policy-based mechanism built for valuation disagreements.

What works and what doesn't

A few practical contrasts help here:

| Approach | What usually happens |

|---|---|

| “This offer feels unfair” | The insurer notes your objection and often stays put |

| Sending random online listings | The adjuster may dismiss them as not comparable |

| Sending a certified appraisal report | The insurer has to answer actual valuation analysis |

| Invoking the appraisal clause properly | The dispute moves into a more structured process |

If you need that kind of valuation support, independent car appraiser services can help owners challenge a total loss or diminished value figure with a documented market-based report. One example is Total Loss Northwest, which works on total loss and diminished value disputes and invokes the appraisal clause in applicable cases.

The fastest way to lose leverage is to argue feelings against paperwork. The fastest way to regain it is to answer their paperwork with better paperwork.

Your Next Steps and State-Specific Remedies

Once you've identified the valuation problems and gathered your records, the next move should be deliberate. Don't scatter your effort. Escalate in sequence.

Start with a written dispute

Send a concise written challenge to the insurer. Identify the valuation errors, attach supporting documents, and ask for a written response. If your policy has an appraisal clause and the dispute is about value, consider invoking it clearly and formally.

Keep the tone controlled. You're creating a record, not venting.

Use the regulator when the process breaks down

If the insurer won't explain the offer, ignores submitted evidence, or drags the process out without a real basis, a complaint to your state's Department of Insurance may help. For Oregon and Washington owners, that can be a useful pressure point when communication has stalled or the file handling looks inconsistent.

A regulator complaint won't replace valuation evidence. It works best when you already have the timeline, correspondence, and disputed report organized.

Know when the issue is bigger than value

Some disputes stay in the lane of total loss or diminished value. Others move into broader bad faith territory. That is especially serious in third-party liability cases. Justia explains that when an insurer unreasonably fails to settle a covered claim within limits and an excess judgment follows, the insurer may face liability beyond the policy amount, making the paper trail central to proving what a reasonable insurer would have done (overview of failure-to-settle bad faith exposure).

That principle matters even if your own dispute is first-party. The lesson is the same. Documentation strengthens your position.

Consider mediation, arbitration, or counsel

Some cases need a lawyer, especially where the insurer refuses to honor the policy process, misrepresents coverage, or causes serious downstream harm. Others may benefit from alternative dispute resolution. If you want a plain-English look at that path, this article on exploring mediation and arbitration in Georgia is useful because it shows the practical trade-offs between formal litigation and negotiated resolution.

If your claim has been denied outright or the handling has shifted from undervaluation to broader refusal, guidance on what to do when insurance denies a claim can help you decide whether to keep pushing the valuation dispute, file a complaint, or bring in counsel.

Frequently Asked Questions About Bad Faith Claims

Is an independent appraisal worth paying for

If the insurer's number is materially wrong and the report has obvious weaknesses, an appraisal can be one of the few tools that changes the file. The value isn't just in the final number. It's in the written analysis, comparable review, and policy-based influence it creates.

Can the insurer punish me for disputing the offer

A carrier can disagree with you. It shouldn't retaliate because you asked for support, challenged bad comparables, or invoked a policy right. Keep your communication professional and documented so the record stays clean.

How long does the appraisal process take

That depends on how quickly each side appoints an appraiser, how much information is available, and whether an umpire becomes necessary. Some disputes move quickly once both sides engage. Others slow down when the insurer delays appointments or resists meaningful review.

Do I need a lawyer to pursue a bad faith insurance claim

Not always. If the dispute is about vehicle value, an appraisal-clause process may resolve it without litigation. If the insurer's conduct goes beyond valuation and starts involving refusal to investigate properly, repeated delay, policy misrepresentation, or larger financial harm, it may be time to speak with counsel.

What's the biggest mistake owners make

Accepting the insurer's report as if it were neutral. It may be usable. It may also be incomplete, poorly matched, or based on assumptions no one challenged. Always read the report line by line before deciding the fight isn't worth it.

If your total loss or diminished value offer doesn't match the market for your vehicle, Total Loss Northwest provides certified auto appraisals for owners in Oregon and Washington and diminished value support nationwide. A solid appraisal can give you the evidence you need to challenge the valuation, invoke the appraisal clause where available, and push the claim back onto defensible ground.