Your car has already been towed. The tow yard is calling. Your insurer is “reviewing” the claim. Every hour you wait, the bill gets worse.

Most drivers treat towing and storage fees like a side issue. That's a mistake. In a total loss or diminished value claim, these charges can eat directly into what you recover. If you don't control them early, you weaken your position with the tow yard, and you give the insurance company an excuse to cut your payout.

You need to treat the tow yard invoice like claim evidence, not just a bill. That means moving fast, documenting everything, and refusing vague charges.

What Are Towing and Storage Fees and Why They Matter

The first invoice usually hits when you're still dealing with the accident itself. You're arranging a rental, talking to insurance, trying to figure out whether the car is repairable, and then a tow yard starts listing fees you never agreed to line by line.

Towing fees are the charges for moving your vehicle from the scene to a storage yard, impound lot, or repair shop. Storage fees are what the yard charges to keep the vehicle there until it's released, transferred, or picked up. On paper, that sounds simple. In practice, these charges are one of the fastest ways an accident claim gets more expensive.

What these fees look like in the real world

In major U.S. markets, towing and storage charges are often regulated rather than left entirely to whatever a yard wants to charge. Los Angeles is a good example. The city's Official Police Garages list a $220 first-hour towing charge for a standard vehicle, $109 for each additional half-hour, and a $68 daily storage rate for a standard vehicle. Heavier vehicles can jump much higher, including $400 for the first hour for an upright heavy-duty vehicle and $850 for an upright medium-duty motorhome, according to Los Angeles Official Police Garage rates.

That's the point you need to understand immediately. These aren't nuisance charges. They can become a serious part of your claim very quickly.

Practical rule: The tow bill starts as a logistics problem. It turns into a valuation problem the moment your insurer starts deciding what it will or won't reimburse.

Why they matter in an insurance claim

If your vehicle is a likely total loss, every avoidable day in storage gives the insurer another argument. They may say the charges were “excessive,” “avoidable,” or “not reasonably incurred.” Even when the other driver caused the accident, you still need to act fast.

If the car is repairable and you're pursuing diminished value, uncontrolled storage can still hurt you. It complicates the file, increases dispute points, and gives the carrier room to drag negotiations into side arguments that don't help you.

Here's the mindset shift I want you to make. Towing and storage fees are not background noise. They are a live financial threat to your settlement. Treat them that way from day one.

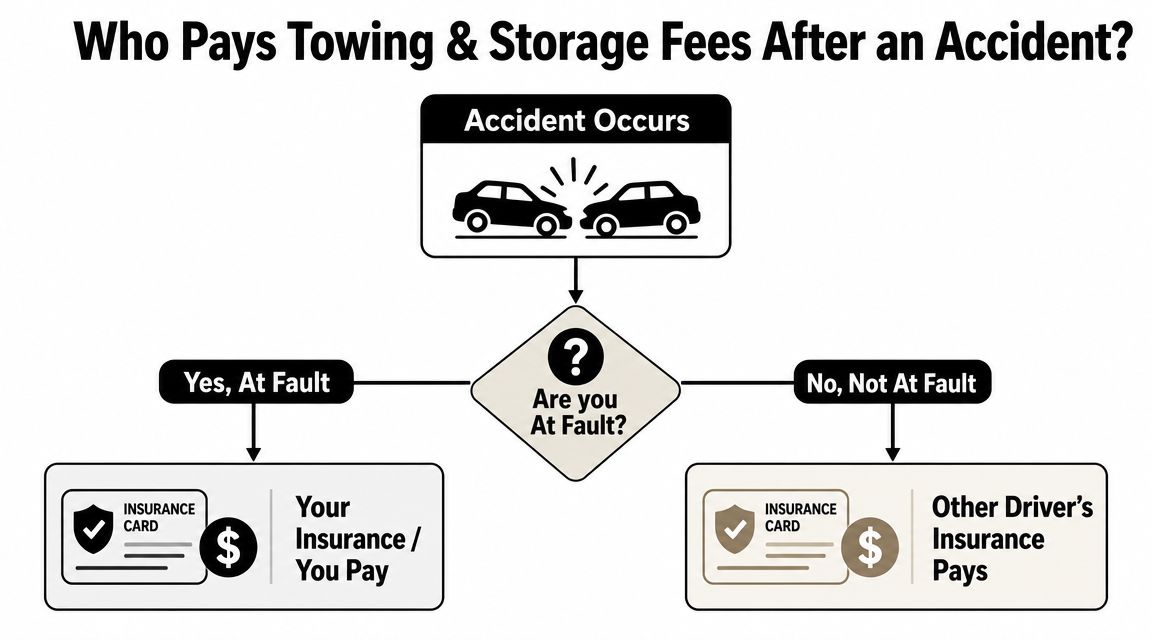

Who Pays Towing and Storage Fees After an Accident

Who pays depends less on what feels fair and more on claim posture, coverage, and how quickly you act. Don't wait for an adjuster to “sort it out.” You need to know where the bill should go and where the risk falls if the claim gets delayed.

The short version

If another driver is clearly at fault, their insurer is usually the target for reimbursement. If you're using your own collision coverage, your insurer may handle the immediate claim side first. If police ordered the tow, that doesn't mean police pay the bill. It usually just means the vehicle ended up in a yard you didn't choose.

None of that changes your immediate job. You still have to prevent the charges from ballooning.

A practical decision tree

Not at fault and filing a third-party claim: The at-fault driver's insurer is generally the party you'll pursue for towing and storage reimbursement. But if that insurer is slow, denies liability, or delays inspection, the yard won't wait. The yard expects payment or release arrangements.

Using your own collision coverage: Your insurer may be the fastest route to get the vehicle moved, inspected, or settled. That can be the smarter play if the storage clock is running.

Police tow or impound situation: The tow was initiated by law enforcement, but the fees still usually attach to the vehicle and owner. You need the exact yard location, release requirements, and daily storage terms immediately.

Disputed liability: This is where people get trapped. Each side points fingers while storage keeps accruing. In that situation, speed matters more than principle. Move the vehicle if you can, preserve documentation, and fight reimbursement afterward.

The right payer on paper doesn't help you if the vehicle sits for days while everyone “investigates.”

Why regulated fee schedules matter

One reason these disputes become manageable is that some states publish hard caps and fee rules. Texas provides a clean benchmark. As of the 2023 biennial adjustment, a vehicle storage facility may charge up to $272 to tow a vehicle weighing 10,000 lbs or less, $380 for 10,001–24,999 lbs, and $489 per unit or up to $978 for vehicles 25,000 lbs or more. Texas also caps daily storage at $22.85 per day for vehicles 25 feet or less and $39.99 per day for vehicles over 25 feet, sets an $22.85 impoundment fee, and prohibits extra charges such as environmental or notary fees under the Texas Department of Licensing and Regulation fee rules.

That doesn't mean every invoice is fair. It means there's a framework. And when a framework exists, you should demand the invoice match it.

Oregon and Washington drivers need to think about mitigation

If you're in Oregon or Washington, the legal fight often turns on reasonableness and mitigation. That means even when you didn't cause the crash, you're still expected to act sensibly to limit avoidable cost. You can't let the vehicle sit indefinitely and assume the insurer must cover every day.

That's not insurer-friendly spin. It's how claims are handled.

Use this standard:

- Call the yard the same day

- Confirm the daily storage charge

- Ask what documents are needed for release

- Tell the adjuster in writing where the vehicle is

- Push for inspection or transfer immediately

If the insurer delays, keep proof. If the yard blocks release without proper explanation, keep proof. If you can move the vehicle to your home, a body shop, or another lower-cost location, evaluate that fast.

The strongest claims aren't just valid. They're documented and disciplined.

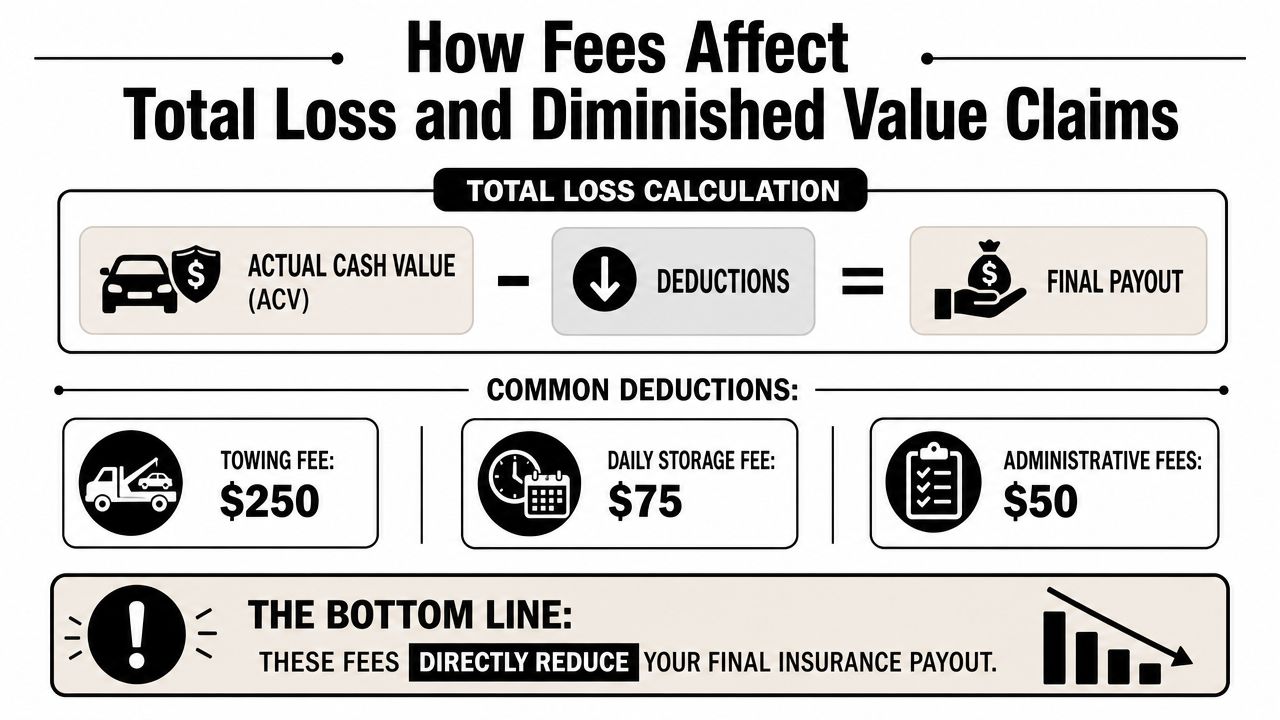

How Fees Affect Total Loss and Diminished Value Claims

Insurers love to separate issues. They'll talk about vehicle value over here, liability over there, and towing charges somewhere off to the side. Don't let them. These issues connect directly.

If your vehicle is a total loss, towing and storage fees can reduce the final amount you pocket. If your vehicle is repairable, storage delays and poor handling can complicate the condition story that supports diminished value.

Total loss claims get eroded two ways

First, the insurer may try to classify part of the storage bill as avoidable. Once they do that, they frame the excess as your problem, not theirs. The valuation number may look one way on paper, but the actual payout shrinks after deductions and disputes.

Second, delay gives the insurer an advantage. They can say they were still investigating, waiting for photos, waiting for authorization, or waiting on the yard. Meanwhile, the storage bill keeps growing and the pressure shifts to you to accept a weak settlement just to stop the bleeding.

If you haven't already, review what happens when your vehicle is totaled so you understand where these side charges fit into the broader settlement fight.

Storage timing is a money issue, not an admin issue

A lot of drivers assume partial-day storage should mean partial-day charges. That assumption gets expensive. Oklahoma's nonconsensual towing schedule states that “the rates are based on the calendar day” and that the maximum daily rate may be charged “for any towed vehicle which is stored for a portion of a twenty-four-hour period,” under the Oklahoma nonconsensual towing rate chart.

That rule matters even outside Oklahoma because it shows how these invoices work in practice. A missed release window, slow adjuster response, or holiday closure can trigger another full day rather than a prorated amount.

Diminished value can also take collateral damage

When a damaged vehicle sits in a storage yard, especially an open lot, the file can get messier. The vehicle may pick up dirt, weather exposure, dead battery issues, or disputes about when certain visible conditions occurred. That doesn't automatically destroy a diminished value claim, but it gives the insurer more room to argue about condition, causation, and post-loss handling.

If your car is repairable and you're trying to understand how value loss is argued after repairs, this explanation of a diminished value claim in Texas gives useful context on how these claims are framed.

If the insurer caused the delay, don't absorb the cost quietly. Put the timeline in writing and tie each storage day to their inaction.

The argument you should make

When storage increased because the insurer failed to inspect promptly, failed to communicate, or delayed authorization, say that plainly. Don't make a moral argument. Make a file-based argument.

List:

- the date of tow

- the date you notified the insurer

- each follow-up you made

- each response or non-response

- the date the vehicle became available for inspection

- the date the insurer acted

That timeline can decide who pays.

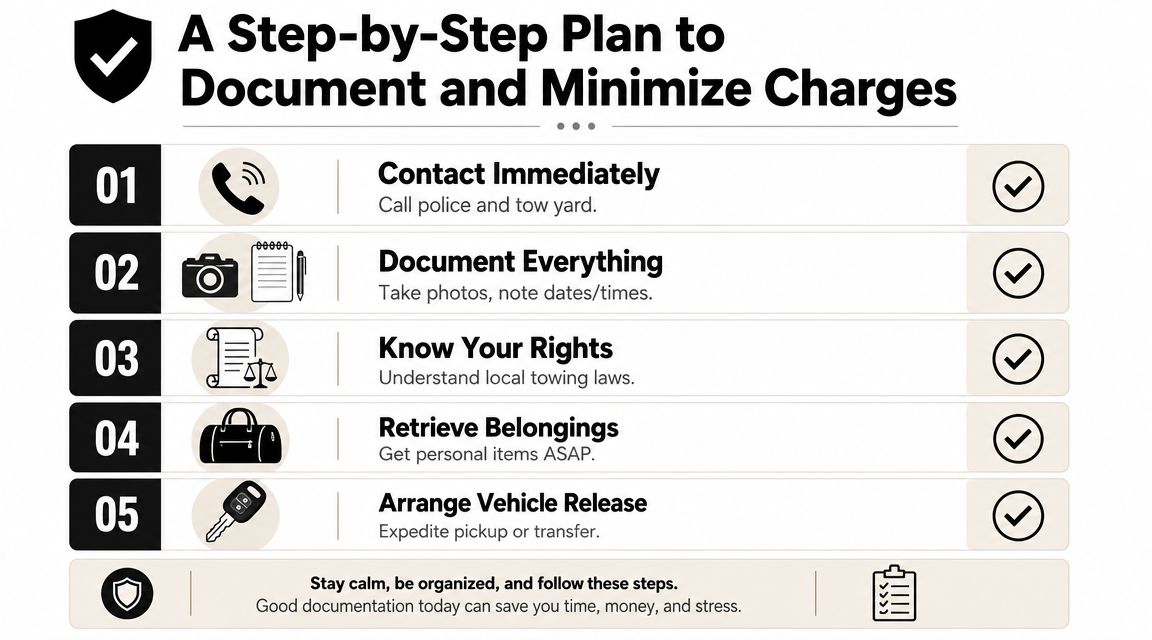

A Step-by-Step Plan to Document and Minimize Charges

This is the part that saves money. Not theory. Action.

Most bad towing and storage outcomes happen because the owner waits for the insurer to take control. Don't do that. The insurer is protecting its file. You need to protect your claim.

Step 1 Call the yard immediately

Call as soon as you know where the vehicle is. Ask for the exact facility name, address, hours, release requirements, accepted payment methods, and whether the vehicle is accruing daily storage right now.

Ask these questions plainly:

- What is the towing charge

- What is the daily storage charge

- When did storage start

- Is billing based on calendar day or another method

- Are there after-hours release rules

- What paperwork is required for release or transfer

Write down the name of the person you spoke with and the time of the call.

Step 2 Tell the insurer in writing on day one

Call if you want, but email is what protects you. Put the yard information in writing and ask for immediate inspection or transfer instructions.

Use direct language. “My vehicle is at [yard name]. Storage is accruing. Please confirm inspection timing and whether you authorize transfer to my home or repair facility.”

That email creates the timeline you may need later.

For broader accident triage, this guide for San Jose accident victims is a solid reminder of the immediate steps that matter after a crash, especially while details are still fresh.

Step 3 Move the vehicle out fast if you can

If the car is drivable enough to release and relocate, or if another tow to your home or preferred shop makes financial sense, evaluate that immediately. Every extra day in a high-cost yard increases pressure on your settlement.

Sometimes paying for a prompt secondary tow is the cheaper decision. Not always, but often enough that you should run the comparison quickly instead of assuming “insurance will handle it.”

Here's a useful overview if you want to hear a claims-focused perspective before you act:

Step 4 Demand an itemized invoice

Never accept a vague total. You want the towing charge, storage charge, any processing charge, release charge if applicable, and the exact dates and times used to compute them.

If they won't itemize, that's a dispute issue already.

“Send me the full itemized invoice with all charges, dates, and billing basis before I discuss payment.”

Step 5 Photograph the vehicle before release

Take clear photos of all sides, the interior if accessible, the odometer if visible, the VIN tag if accessible, and any additional damage or condition issues. If property is missing, note that immediately.

You're preserving two things at once:

- the vehicle's post-accident condition

- the fact that the yard had possession of it in that condition

Step 6 Keep a simple evidence file

Don't overcomplicate this. A folder on your phone and an email thread are enough if you're disciplined.

| Evidence Item | Why It's Important |

|---|---|

| Tow yard name, address, and phone number | Identifies the exact custodian of the vehicle and where charges originated |

| Date and time the vehicle was towed | Helps verify when towing and storage should have begun |

| Written confirmation of daily storage rate | Prevents later arguments that the rate was never disclosed |

| Itemized invoice | Shows whether charges were broken out or improperly bundled |

| Release requirements in writing | Documents whether the yard created avoidable delay |

| Emails to and from the insurer | Proves you gave notice and requested prompt action |

| Photos of the vehicle in storage | Preserves condition and helps defeat later damage disputes |

| Proof of transfer or pickup date | Establishes when storage should have stopped |

| Notes of phone calls with names and times | Fills in gaps when the other side claims confusion |

Step 7 Retrieve personal property without delay

Get your belongings out as soon as the yard allows it. Important documents, toll devices, chargers, work gear, child seats, and garage openers shouldn't stay with the vehicle longer than necessary.

Also check whether the title, registration, or insurance card is still in the car. Those items often become important when release paperwork starts.

Step 8 Don't let the file go silent

If the insurer doesn't respond, follow up again in writing. If the yard adds another day, update the insurer again in writing. Silence is expensive in towing and storage disputes.

Short, dated messages beat long emotional ones. Stay factual.

Disputing Unreasonable Towing and Storage Charges

A charge isn't reasonable just because it appears on an invoice. If the tow company can't show what was charged, when it began, and why it applies, you have a dispute worth making.

A lot of bad invoices rely on one thing. The owner feels overwhelmed and pays first.

What makes a charge suspect

Start with the paperwork. If the invoice lumps everything together, omits start times, or uses vague labels, challenge it.

Oklahoma's wrecker manual is useful here because it spells out a principle that applies broadly: “itemized charges” include total towing fees, total storage fees, total processing fees, and any other fee category under the Oklahoma wrecker manual. That matters because bundled invoices make it harder to verify whether the yard followed the rules.

Look for these problems:

- Bundled totals with no breakdown of towing, storage, and processing

- Missing timestamps for when tow service started or storage began

- Unclear day-count method so you can't tell how they calculated storage

- Undisclosed fees that appear only at release

- Charges for services not explained in any written notice or invoice detail

A direct letter to the tow company

Keep it short. You're not writing a legal brief. You're forcing clarity.

Sample dispute letter to the tow yard

I dispute the towing and storage charges currently claimed for my vehicle. Please provide a fully itemized invoice showing each fee category, the tow start time, the exact storage start time, the basis used to count storage days, and the written authority for any processing or release-related fee. Until I receive that documentation, I don't agree that the full amount claimed is valid or enforceable.

That letter does two things. It asks for specifics, and it signals that you're not treating a vague invoice as self-proving.

A stronger letter when the insurer caused delay

Insurers sometimes act like storage became your fault automatically after a certain point. That's wrong when their own delay drove the bill.

If they stalled inspection, delayed liability review, or failed to authorize movement after notice, say so in writing. If you need help framing that demand properly, this guide on an insurance demand letter is worth reviewing.

Use language like this:

I notified your office that the vehicle was in storage and accruing charges. I requested prompt inspection and direction regarding transfer or release. The additional storage that accrued after that notice resulted from claim handling delay, not from inaction on my part. I demand reimbursement for those charges and object to any deduction from my settlement based on delays outside my control.

Escalate with evidence, not outrage

Anger won't move the file. Documentation will.

Send:

- the itemized invoice or your request for one

- your email notice to the insurer

- your follow-up emails

- yard release terms

- proof of when the car could have been moved

- proof of when the insurer finally acted

If the tow yard still won't clarify charges, or the insurer keeps treating unsupported fees as your problem, escalate to the relevant regulator or consumer protection agency in your state. In Oregon and Washington, that often means using the state complaint channels that oversee unfair claim handling or regulated transport practices.

Your advantage stems from a clean timeline and a broken invoice. Build both.

When to Hire an Appraiser or Attorney

There's a point where self-help stops being efficient. You've reached it when the storage dispute starts distorting the value dispute.

Get professional help if the insurer says it will deduct disputed storage from a total loss offer, if the tow yard is threatening lien action, or if the combined charges are becoming a serious share of what the vehicle is worth. Those are not minor admin issues anymore.

An independent appraiser helps when the core dispute is over vehicle value and the carrier is using towing or storage chaos to pressure settlement. That matters in both total loss and diminished value claims. A proper appraisal gives you an evidence-based number that stands apart from the insurer's internal valuation process.

If you're not sure what that process involves, review what an appraisal for a car is and how it fits into a disputed claim.

Hire an attorney when the dispute has moved beyond valuation into legal exposure. Examples include lien threats, release refusals, bad-faith style insurer conduct, or serious disagreement over who caused the storage accumulation. At that point, you need someone who can force deadlines and protect your position formally.

Don't wait until the vehicle has sat too long and everyone has hardened their position. Early escalation is usually cheaper than late rescue.

If your total loss or diminished value claim is being dragged down by towing and storage fees, Total Loss Northwest can help you fight back with an independent appraisal that focuses on real market value, not insurer-friendly shortcuts. If you're in Oregon or Washington and you're being lowballed, or if storage disputes are eating into your settlement, get expert help before those charges take more than they should.