You open the claim summary, look at the number, and know right away it won't replace your vehicle. The trim is off. Options are missing. The insurer's comparables don't match what you owned. If it's a custom truck, a collector car, or a hard-to-find model in Oregon or Washington, the gap feels even worse because local inventory and real market value don't line up neatly with a canned valuation report.

That's the moment many owners either give up or start arguing with an adjuster who has already moved on to the next file.

There's a better path. If your policy includes an appraisal clause, you may be able to force the value dispute into a structured process where your appraiser, the insurer's appraiser, and, if needed, an appraisal clause umpire sort out the amount of loss. The umpire isn't there to debate fault or coverage. The umpire's job is to break a valuation deadlock with evidence, not pressure.

Your Insurance Offer Is Low Now What

A common pattern looks like this. Your car is declared a total loss. The carrier sends a report that looks polished and final. It includes adjustments, condition ratings, and comparables that make the offer seem objective. But when you try to shop for a replacement, the numbers don't work.

That frustration is justified.

Published claims data show why this process matters. In a set of 46 appraisal-clause outcomes, insurer settlement offers were reportedly off by an average of 45.86%, with an average shortfall of $5,312.46 before appraisal was invoked, and the final awards were often more than double the original offers, according to reported appraisal-clause outcome data.

What usually makes the offer feel wrong

Low offers often come from a handful of practical problems:

- Bad vehicle identity. Wrong trim, wrong drivetrain, or missing factory equipment.

- Weak comparables. Listings that aren't similar in condition, market, or configuration.

- Condition deductions. Adjustments that aren't supported by photos or prior records.

- Specialty market blind spots. Custom parts, collector demand, or limited regional inventory get flattened into generic value assumptions.

If you're trying to pressure-test the number yourself before escalating, start with a solid understanding of how to calculate fair market value.

If you can't buy a comparable replacement vehicle for the settlement amount, that's a signal to stop treating the insurer's first number as fixed.

The clause most owners miss

Many people never get told that their policy may already contain a process for this exact problem. The appraisal clause is usually there for a dispute over value, not over who caused the crash or whether coverage exists.

That distinction matters. If your dispute is about dollars, not liability, an appraisal demand can move the file out of endless back-and-forth and into a formal valuation track. For a lot of owners, that's the first point where the claim starts being judged on market evidence instead of settlement posture.

Understanding the Appraisal Clause Players and Process

Think of the appraisal process like two experienced mechanics disagreeing on a difficult diagnosis. They each inspect the same vehicle. They compare notes. If they still can't agree, they bring in a third specialist to resolve the specific points of disagreement. That third specialist is the umpire.

Who does what

The process is designed so each side chooses an appraiser first.

| Player | Role | What they should focus on |

|---|---|---|

| Your appraiser | Presents your valuation position | Vehicle identity, options, condition, local market support |

| Insurance appraiser | Presents the carrier's valuation position | The insurer's view of amount of loss |

| Umpire | Resolves only the disputed valuation items | Evidence, comparables, methodology |

The key point is simple. The umpire does not start as the main decision-maker. The two appraisers first try to agree on the amount of loss. Only unresolved differences go to the umpire, and the award becomes binding when any two of the three sign, as outlined in this explanation of how appraisal awards work.

What the umpire is not

Owners often assume the umpire is like a judge handling the whole claim. That's not how this process is built.

The umpire is usually a valuation tie-breaker, not a legal mediator. They don't decide fault. They don't rewrite your policy. They don't usually settle coverage questions. Their lane is the amount of loss.

That's why preparation matters more than emotion. If your appraiser brings clean comps, accurate build data, and a credible value theory, the umpire has something concrete to work with.

Why this feels different from adjuster negotiations

Adjusters negotiate claims every day. Most owners do this once. If you need a primer on handling that early stage before or alongside appraisal, this insurance adjuster negotiation guide is a useful background read.

For the appraisal track itself, the most helpful way to think about it is this: you're no longer asking the insurer to reconsider out of goodwill. You're invoking a contractual process. If you want a straightforward primer on the basics before you read your own policy, review what an appraisal for a car means.

The strongest appraisal files don't sound the most upset. They're the ones that document the dispute clearly and stay inside the valuation issue.

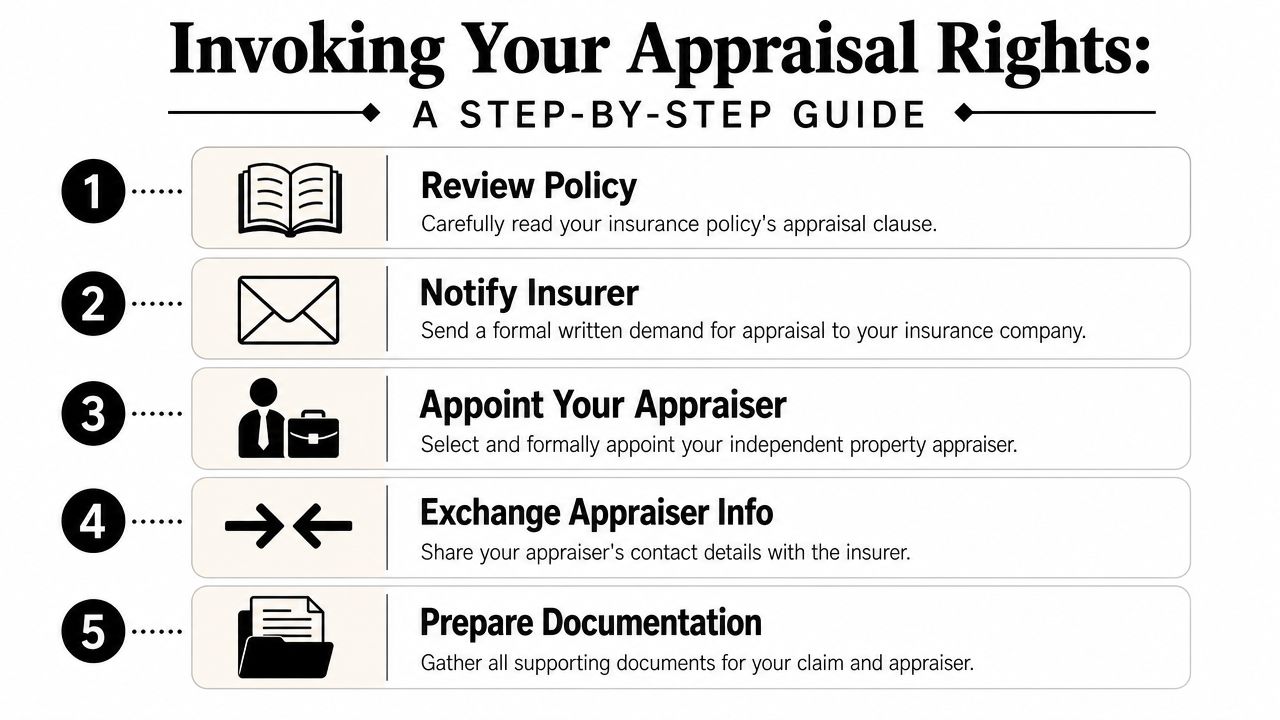

How to Formally Invoke Your Appraisal Rights

Most appraisal fights don't fail because the owner was wrong about value. They fail because the owner invoked the clause loosely, verbally, or without creating a record. If you want the process to move, make your demand clean, written, and specific.

What to find in your policy

Pull the declarations page and the full policy form. Search for the words appraisal, amount of loss, and umpire. You're looking for the paragraph that says either party may demand appraisal when there's disagreement over value.

Read that clause slowly. Don't skim it.

Different policies handle appointment language, timing, and award wording a little differently. Some clauses are straightforward. Others bury the trigger language in dense policy text. What matters is whether your dispute is framed as value and whether the policy gives either party the right to demand appraisal.

How to send the demand

Use written notice. Email is helpful for speed, but I prefer adding a hard-copy letter so there's no argument later about what was said or when it was sent.

Use this checklist:

- Identify the claim. Include claim number, date of loss, policy number, vehicle year, make, model, and VIN.

- State the dispute clearly. Say you dispute the insurer's valuation or amount of loss.

- Invoke the clause directly. Use the policy's own wording if possible.

- Name your appraiser if you already have one. If not, say you'll provide that information promptly.

- Request the insurer's appraiser information in writing.

- Keep every attachment. Save the valuation report, photos, receipts, option lists, and prior correspondence.

Sample demand letter

Re: Claim Number [insert claim number]

Policy Number [insert policy number]

Vehicle [year, make, model, VIN]

Date of Loss [insert date]I dispute the insurer's valuation of my vehicle and the amount of loss. Pursuant to the appraisal provision in my policy, I hereby make formal written demand for appraisal.

Please confirm in writing that this demand has been received and provide the name and contact information of the appraiser appointed on behalf of the insurer. My appraiser is [name and contact information], or I will provide that appointment in writing shortly.

Please direct future appraisal-related communication in writing so the parties can proceed efficiently.

Sincerely,

[Your name]

[Address]

[Email]

[Phone]

What to gather before your appraiser starts

Your appraiser will work faster and better if you hand them a complete file instead of dribbling out documents over a week.

- Vehicle proof. Window sticker, service records, photos, purchase docs, and upgrade receipts.

- Loss paperwork. Insurer valuation report, total loss notice, adjuster emails, and settlement offer.

- Market support. Similar listings, dealer inventory, auction references if available, and notes about local scarcity.

- Specialty documentation. Build sheets, restoration records, aftermarket invoices, or collector-market evidence for nonstandard vehicles.

Practical rule: Don't just tell your appraiser the offer is low. Show exactly why the insurer's number doesn't match the actual market for your vehicle.

Choosing Your Appraiser and Agreeing on an Umpire

This is the decision that most affects the outcome. Owners spend hours arguing about the insurer's report and only minutes vetting the person who will represent them in appraisal. That's backwards.

A good appraiser doesn't just know cars. They know how to build a valuation position that can survive scrutiny from another appraiser and, if needed, from an appraisal clause umpire.

What matters in an appraiser

You want someone who can work from evidence, not swagger. In a standard appraisal setup, the strongest submissions document market-supported comparables and separate agreed items from disputed ones. Guidance on useful awards also emphasizes that the umpire should be competent and disinterested and decide disputed valuation items based on the evidence presented by the appraisers, as described in this field guide to appraisal practice.

Ask practical questions:

- What vehicles do you handle most often. A daily-driver total loss is different from a custom Tacoma, a restored Bronco, or a collector Porsche.

- How do you support comparables. If the answer is vague, keep looking.

- Do you work appraisal-clause disputes regularly. Valuation knowledge alone isn't enough.

- How do you present disputed items to an umpire. Good appraisers can explain their method in plain English.

What matters even more in custom and specialty claims

If the vehicle is modified, rare, or unusually configured, generic valuation experience won't carry the day. You need somebody who understands the market where your vehicle lives.

That may mean knowing how buyers price documented upgrades, how local dealer inventory differs from national listings, or why a supposedly similar comparable isn't comparable at all.

One option in Oregon and Washington is Total Loss Northwest, which handles independent auto appraisals and appraisal clause disputes for total loss and diminished value claims. Whatever firm or individual you consider, ask for their process on custom vehicles before you hire them.

Here's a short walkthrough that helps owners understand the selection issues:

How to think about the umpire

The umpire should not feel like a compromise pick chosen because both sides got tired. The umpire should be someone both sides can defend if the process is later questioned.

Use this screen:

| Question | Why it matters |

|---|---|

| Does the umpire have valuation experience relevant to this vehicle type? | Specialty claims need specialty judgment |

| Is the umpire disinterested? | Prior business ties can create credibility problems |

| Can the umpire stay inside valuation issues? | Coverage arguments can derail the process |

| Will both appraisers respect the umpire's methodology? | A credible process is easier to finish and harder to attack |

If I'm reviewing an umpire candidate for a custom car case, I want to know whether they've dealt with thin-market valuations before. A neutral person who only knows high-volume commuter vehicles may still be honest, but honesty alone doesn't solve an expertise gap.

The Appraisal Process Costs and Timelines

Owners usually ask two questions right away. What will this cost me, and how long will I be stuck in it?

The cost structure is one of the clearer parts of the process. In a standard appraisal clause, each party pays its own appraiser, while the umpire's fee is shared equally. If the two appraisers can't agree on an umpire within a set period, often 15 days, a court may be asked to appoint one, according to this discussion of standard appraisal clause structure.

What that means in practice

That split-fee setup is supposed to reinforce neutrality. The umpire isn't your expert and isn't the carrier's expert. Both sides share that cost because the umpire serves the process, not one party.

The trade-off is straightforward. You do have to invest in your own appraiser. But if the dispute is large enough, especially on a total loss or specialty vehicle, the process can make more sense than prolonged negotiation that goes nowhere.

What usually slows things down

Most appraisal delays come from human bottlenecks, not from the clause itself.

- Appointment lag. One side takes too long to name its appraiser.

- Document gaps. The file is incomplete, so the appraisers spend time chasing basics.

- Umpire fights. The appraisers don't agree on a neutral person.

- Methodology disputes. The case involves unusual comparables or contested actual cash value inputs.

Expect movement when the paperwork is organized and the dispute is framed tightly. Expect delay when the parties mix valuation issues with every other claim complaint.

A realistic way to plan

Don't treat appraisal like instant relief, but don't assume it has to drag forever either. A straightforward file can move cleanly once both appraisers are engaged. A custom, collector, or disputed-condition claim usually takes more effort because the evidence has to be tighter.

Your best timeline lever is preparation. If your appraiser gets a complete file on day one, the process starts with analysis instead of cleanup.

Navigating Appraisal in Oregon and Washington

Owners in Oregon and Washington run into a practical problem that national articles usually miss. The hard part often isn't understanding the clause. The hard part is applying it to a Pacific Northwest market where inventory can be uneven, specialty vehicles are common, and replacement value may not track with generic valuation systems.

What local owners should pay attention to

In Oregon and Washington, I tell owners to focus less on broad internet averages and more on the actual replacement market that touches their vehicle. A late-model commuter car is one thing. A diesel truck with documented upgrades, a Subaru with trim-specific demand, or a collector vehicle with strong regional interest is another.

That's where appraisal work becomes local in a real sense.

If the insurer treats your vehicle like a generic unit and your replacement search shows otherwise, your file needs market evidence that reflects the region. Dealers, private-party listings, trim accuracy, option packages, and prior-condition support matter far more than arguing in circles about whether the insurer's software is fair in theory.

Constructive total loss issues

Some owners in this region also need to think beyond obvious total losses. The claim may involve a severe damage scenario where repair economics and post-loss value point toward a broader valuation dispute. If that sounds like your situation, it helps to understand how a constructive total loss works.

Where Oregon and Washington claims get sticky

These are the trouble spots I see most often:

- Local market mismatch. The valuation pulls from vehicles that don't reflect your buying area or your vehicle's real peer group.

- Weather and use profile differences. Prior condition assumptions can be overstated or unsupported.

- Outdoor and utility modifications. Racks, canopy systems, wheel packages, towing setup, and similar equipment may be undervalued or ignored.

- Specialty vehicles. Classic, custom, enthusiast, and limited-production vehicles need more than a mass-market pricing approach.

For Oregon and Washington owners, the practical answer is not to demand perfection from the insurer's first report. It's to build a file that can stand up in appraisal if negotiation stalls. The better your local evidence, the more useful the umpire stage becomes.

Common Pitfalls and Next Steps After the Award

The biggest mistake owners make is assuming appraisal will run on autopilot once they invoke it. It won't. The process still depends on participation, document exchange, and a real dispute being presented properly.

When the process stalls

A serious failure point appears when one appraiser stops participating or refuses to engage after appointment. Legal commentary warns that if an appraiser refuses to participate, there is “nothing in the policy giving the umpire the right to act in the absence of differences between the appraisers,” which means you may need legal intervention instead of assuming the umpire can finish the job alone, as discussed in this analysis of stalled appraisal proceedings.

That's an important limit. The umpire is a tie-breaker. No active disagreement between appraisers means no tie to break.

What works when things start slipping

When a claim starts bogging down, focus on process discipline.

- Keep communication written. Verbal updates disappear later.

- Pin down dates. Ask for clear deadlines for appraiser appointment, document exchange, and umpire proposals.

- Separate valuation from everything else. The more issues you pile into appraisal, the easier it is for progress to stall.

- Escalate appropriately. If participation breaks down, talk to counsel instead of waiting for the file to revive itself.

If the other side won't engage, patience stops being a strategy. At that point, procedure matters more than argument.

After the award

Once an award is signed by the required decision-makers under your policy, the claim usually shifts from valuation dispute to payment and implementation. At that stage, two outcomes are common.

| Outcome | What you do next |

|---|---|

| The insurer honors the award | Confirm payment details, deductible treatment, and any title or settlement paperwork |

| The insurer resists or delays | Preserve the signed award, document the noncompliance, and get legal advice on enforcement |

If the carrier pays, review the numbers carefully. Make sure the payment matches the award and that any salvage, deductible, or prior advance issues are handled correctly.

If the carrier doesn't pay or starts reframing the dispute after the award, that's no longer just a valuation problem. It becomes an enforcement problem. That's when owners should stop trying to solve everything through claims correspondence alone.

If you're in Oregon or Washington and your total loss offer doesn't reflect what your vehicle was worth, Total Loss Northwest can review the valuation dispute, help assess whether appraisal makes sense, and support owners dealing with low offers, specialty vehicles, and appraisal clause cases.