You open the claim email, scan the valuation, and feel your stomach drop. The insurer's number may look tidy on paper, but it doesn't look anything like what it would cost to replace your vehicle in Portland. That reaction is usually justified.

I see this problem most often after a total loss decision or after a major repair on a newer vehicle. The insurance carrier presents a figure built from software, comparable listings, condition adjustments, and internal rules. It may be technically defensible. But “defensible” and “enough to make you whole” are not the same thing, especially when you drive a late-model EV, a higher-end trim, a modified vehicle, or anything the local market values differently than a generic database does.

That's where a Portland auto appraiser matters. The job is not to complain louder than the insurance company. The job is to document why the number is wrong, where the replacement gap exists, and what evidence will hold up in a real dispute.

That Lowball Offer Is Not the Final Word

You review the insurer's offer, pull up a few local listings, and the gap is obvious. On paper, their number may pass an internal review. In Portland, it still may not buy the same vehicle again, especially if you owned a newer EV, a premium trim, or a car with options the market values.

By the time people call a Portland auto appraiser, they have usually already done the reasonable things. They sent service records. They corrected the trim level. They pointed out mileage, tires, condition, charging package, driver-assist features, or recent work. The carrier may adjust a line item or two and still leave them short of what replacement really costs.

That is a valuation dispute, and the financial problem is usually larger than the insurer admits at first.

The first offer is often a starting position built to be defendable, not a number designed to put you back in an equivalent vehicle.

I see this most often in three situations. A total loss on a late-model car. A repaired vehicle that now carries accident history. A specialty or high-value vehicle that does not fit neatly inside standard valuation software. In each case, the insurer can produce paperwork that looks orderly while the owner is left trying to solve a real cash shortfall.

This distinction is important: many claim fights are not about whether a car had damage. They are about what it will cost you, in Portland, to replace the vehicle or absorb the loss in market value after repair.

A low offer usually creates one of these problems:

- Total loss shortfall: The carrier pays actual cash value, but the figure may not be enough to buy a comparable replacement locally.

- Diminished value loss: The car is repaired, yet its accident history still reduces what buyers will pay.

- Specialty valuation gap: EVs, luxury vehicles, classics, modified cars, and uncommon trims often get flattened into generic comparisons that miss real market value.

That is why owners bring in an independent appraiser. The job is to examine the vehicle, the market, and the insurer's reasoning, then document a number that can stand up in a dispute. If you want a plain-language overview first, this guide on what an appraisal for a car involves explains the basic process.

If the offer leaves you unable to replace the vehicle you had, the discussion should not end with “that's what the system produced.” It should move to evidence.

What a Portland Auto Appraiser Really Does

A Portland auto appraiser does more than put a price on a car. Their primary job is to build a valuation that can survive scrutiny.

Consider it similar to hiring a private home inspector before buying a house. You don't hire that person for a casual opinion. You hire them to identify facts, document conditions, and give you something credible enough to act on. Auto appraisal works the same way in claim disputes. The appraiser is an independent third party working from inspection, market data, valuation standards, and written support.

The work behind the number

A proper appraisal usually includes several layers of analysis:

- Vehicle identification: Exact trim, options, mileage, prior condition, modifications, and pre-loss market position.

- Damage context: Whether the issue is a total loss, a repaired vehicle with stigma, or a specialty valuation problem.

- Market comparison: Real comparables and reasoned adjustments, not just a software printout.

- Written support: A report built for negotiation, policy dispute, and sometimes legal review.

If you're new to the process, this overview of what an appraisal for a car involves is a useful starting point.

Why certification matters

Not every person who “knows cars” is qualified to write a report that carries weight in an insurance dispute.

Certified appraisers affiliated with ASCAA complete a 5-course certification program covering USPAP ethics, vehicle inspection methodology, and valuation standards, according to the Portland appraiser certification overview. That matters because the insurer doesn't have to care about opinions. It does have to deal with a documented appraisal grounded in recognized methods.

Practical rule: If the report won't stand up to pushback, it won't move the claim.

Different assignments require different thinking

A seasoned appraiser adjusts the approach based on the claim type:

| Claim type | What the appraiser is evaluating |

|---|---|

| Total loss | Pre-accident value and whether the insurer's figure reflects a real comparable replacement |

| Diminished value | How much value the repaired vehicle lost in the market because of accident history |

| Classic or collectible | Rarity, condition, originality, and market nuance that software often misses |

| Pre-loss or fair market value | Baseline value for planning, negotiation, or dispute support |

This is why a Portland auto appraiser is not just a car person. The appraiser is a dispute professional who translates vehicle facts into support for a claim.

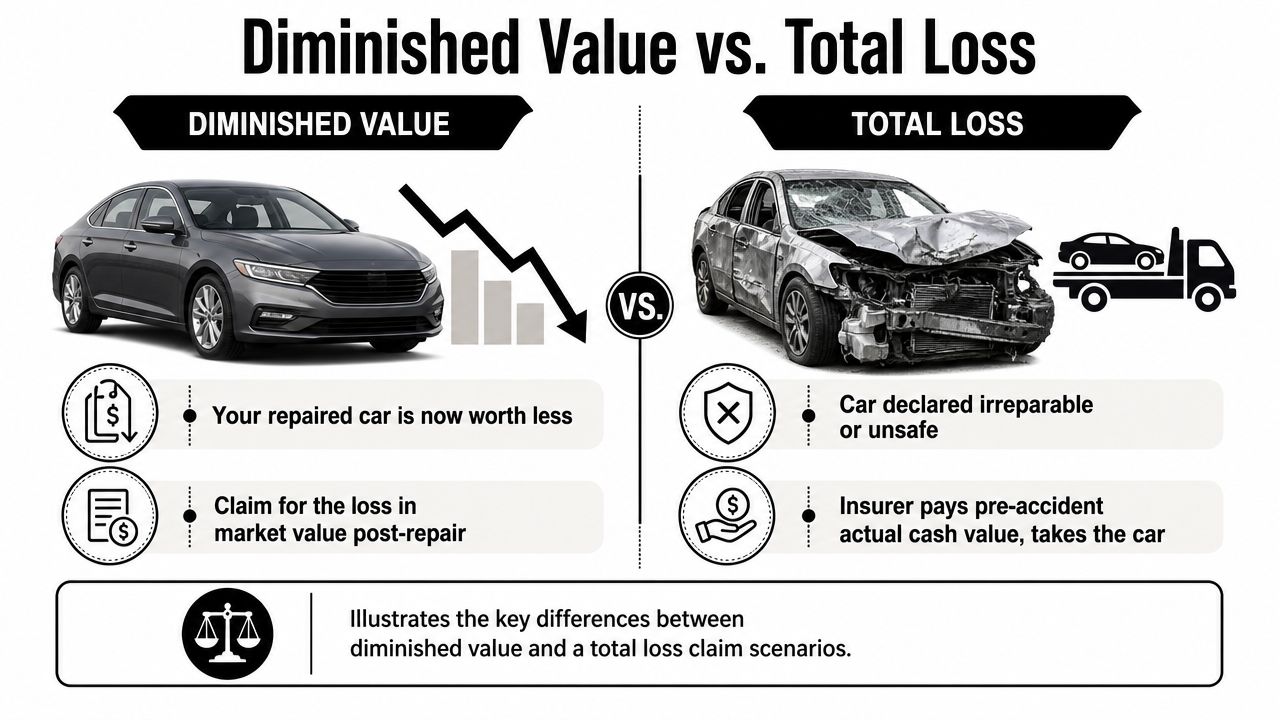

Diminished Value Versus a Total Loss Claim

These two claims get mixed together all the time, but they are not the same.

A diminished value claim means your car was repaired and returned to you, yet the market now sees it as less desirable because it has an accident history. A total loss claim means the insurer has decided to pay the vehicle's pre-accident value rather than repair it.

The simplest way to tell them apart

Use this mental shortcut:

- Diminished value: You keep the car, but it's worth less than it was before the crash.

- Total loss: You lose the car, and the fight is over what the payout should be.

That distinction sounds basic, but it changes the entire strategy. In a diminished value case, the question is how the accident history affects resale. In a total loss case, the question is whether the insurer's number would let you buy a comparable vehicle again.

If you want a consumer-friendly explanation of understanding vehicle depreciation after a crash, that resource helps clarify why repaired vehicles can still suffer a market penalty.

Where the real money gap shows up

The hardest claims are often the ones where the insurer's valuation is not obviously ridiculous. The report may be neatly assembled. The comparable vehicles may look close enough. The math may check out internally.

But there's a bigger question. Can you replace your vehicle with that amount in Portland?

A key issue in this market is the gap between a “technically defensible” valuation and the actual cost of buying a comparable replacement. Portland-focused appraisal analysis notes that Cox Automotive data shows continued volatility in used-vehicle pricing into 2025, which means a fair market value figure can still leave you under-indemnified in practical terms, especially after adding tax, title, and licensing, as discussed in this review of replacement cost pressure in Portland auto claims.

That problem hits several owners especially hard:

- EV owners: Repair complexity can distort the repair-versus-total-loss decision.

- Luxury owners: Small option differences create large real-world pricing gaps.

- High-demand everyday drivers: A paper valuation can lag behind what local inventory costs.

- Modified or specialty owners: Generic comparables often erase value that buyers do recognize.

For diminished value support, a more detailed look at automobile diminished value claims can help you decide whether the claim belongs in a post-repair negotiation or whether the total-loss issue is the bigger financial fight.

A claim can be “supported” on paper and still leave you short at the dealership.

How to Invoke the Appraisal Clause in Oregon

You receive a total loss offer, search Portland listings, and realize the problem fast. The insurer's number may be defensible inside its report, but it still may not buy the same vehicle here, especially if you drive an EV, a late-model SUV with option packages, or a higher-end car where trim and condition change value in a hurry.

The appraisal clause gives you a contract-based way to challenge that gap. It does not decide coverage. It does not fix repair delays. It addresses one issue: the amount of loss.

Step one through step three

Read your policy carefully

Find the appraisal language and confirm how your policy describes a value dispute. Oregon policies vary in wording, deadlines, and procedure. Small language differences matter.Put the dispute in writing

Send a short letter or email stating that you disagree with the insurer's valuation and are invoking the appraisal clause under the policy. Include the claim number, VIN, date of loss, and the amount being disputed. Keep the tone professional. You are building a record.Choose your appraiser

You select an independent appraiser. The insurer selects its own appraiser. If you want a plain-English explanation of how that process works, this guide on the insurance appraisal clause is a useful starting point.

A practical point matters here. Appraisal works best when the dispute is about value. If the primary dispute is coverage, liability, or whether certain damage is related to the loss, the clause may not solve that problem.

What happens next

Once both appraisers are named, they review the file and try to reach an agreement on value. If they cannot agree, they choose an umpire. The umpire decides the remaining disputed points.

That changes the posture of the claim. You are no longer asking the same adjuster to rerun the same valuation system. You are using a process the policy already allows, with deadlines, written positions, and a neutral tie-breaker if needed.

For Portland owners, that shift can have real financial consequences. A small paper difference can become a large out-of-pocket problem once you try to replace the vehicle locally and account for taxes, title, registration, equipment differences, battery concerns on EVs, or option packages that generic comps miss.

Later in the process, many drivers find it helpful to watch a quick walk-through before sending formal notice:

What works and what doesn't

The policy clause helps. Your documentation still decides how strong your position is.

What works

- Clear written notice: Short, firm, and tied to the policy language.

- Vehicle-specific proof: Photos, option lists, service records, receipts, prior condition evidence, and market support for comparable replacements.

- A focused valuation argument: Explain why the insurer's comps are off on trim, mileage, condition, equipment, or local availability.

What doesn't

- Arguing only that the offer feels low: The number needs support.

- Using random listings that do not match your vehicle: Wrong trim, branded title history, distant markets, or missing features weaken the file.

- Waiting until the claim file goes stale: Delay makes condition, options, and market timing harder to prove.

Treat appraisal like evidence work. The stronger your file, the harder it is for a technically defensible number to stand in for your real replacement cost.

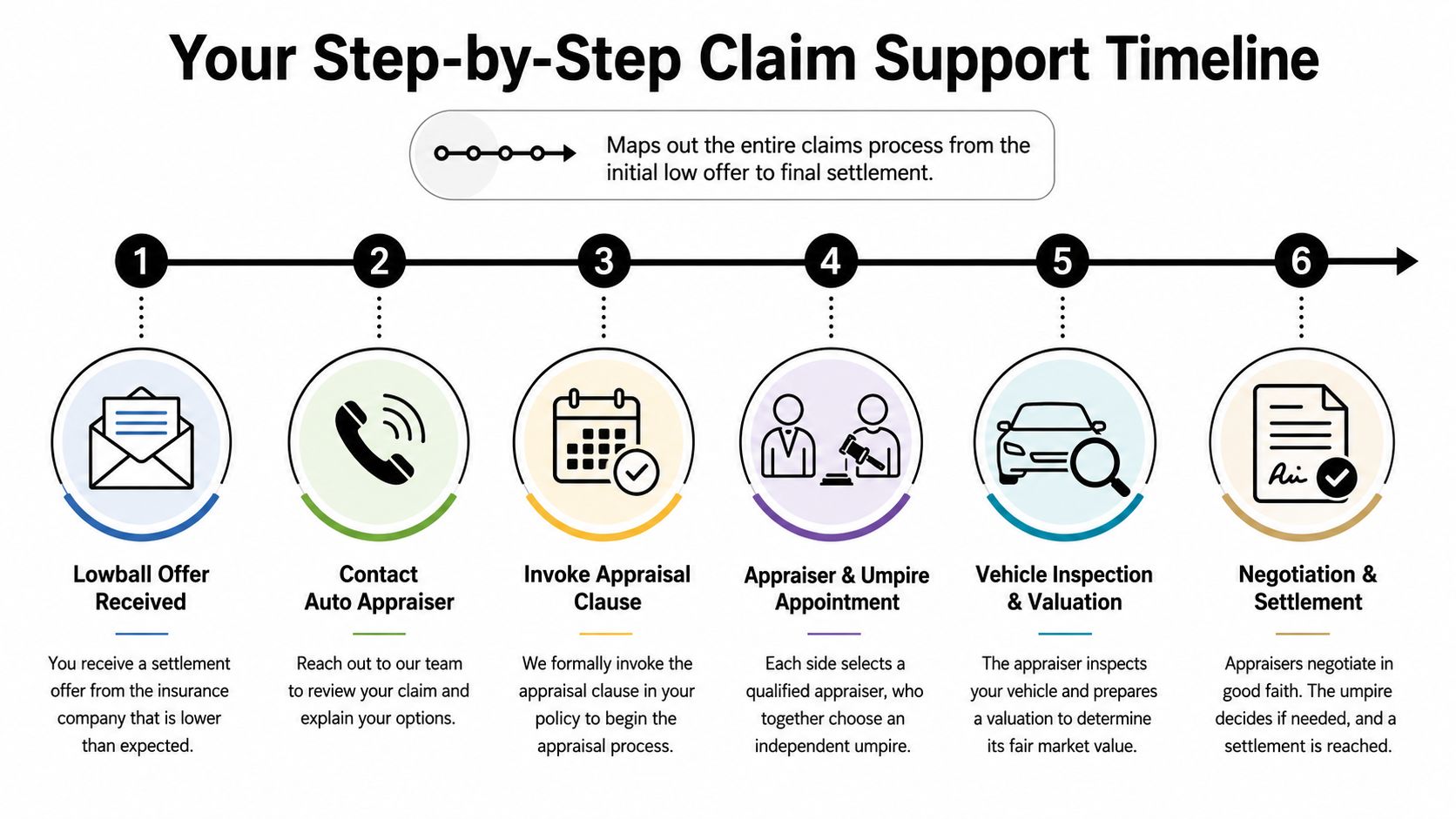

Your Step by Step Claim Support Timeline

The process feels less intimidating when you know what comes next. Most claims follow a recognizable path, even when the details vary by carrier, vehicle type, and whether the dispute is over total loss or diminished value.

Use this timeline as the practical version of what usually happens after the low offer lands.

The first few days

You receive the insurer's valuation and realize the numbers don't line up with replacement reality. Before arguing on the phone, gather the basics.

Start with:

- Claim documents: The valuation report, settlement letter, and any total-loss or repair paperwork.

- Vehicle records: Window sticker if available, service history, upgrade receipts, and recent photos.

- Damage file: Collision photos, repair estimate, and body shop documentation.

At this stage, a lot of people call an independent appraiser. One option in Oregon and Washington is Total Loss Northwest, which handles certified independent appraisals for total loss disputes and appraisal clause matters.

Inspection and report stage

Once the appraiser has the file, the work shifts from complaint to documentation. The appraiser reviews the condition, trim, market position, repair context, and comparable vehicles, then prepares a written report designed for negotiation or appraisal-clause use.

This part usually feels slow to clients because it's not visible. But it's the core of the case. A rushed report often creates more problems than it solves.

The strongest claim files are organized before the insurer asks for anything else.

Submission and dispute resolution

After the report is ready, it goes to the insurer or into the appraisal process, depending on the path you're taking. Sometimes the carrier revises its position after seeing a defensible valuation. Sometimes it digs in, and the dispute moves to appraiser-to-appraiser discussion or to an umpire.

A typical progression looks like this:

| Stage | What you should be doing |

|---|---|

| Offer received | Do not accept before reviewing the valuation details |

| File assembly | Organize documents, photos, options, and condition evidence |

| Appraiser engagement | Provide records quickly and answer factual questions |

| Report submission | Let the written valuation do the work |

| Negotiation or appraisal clause | Stay responsive, but avoid repeating unhelpful phone arguments |

| Settlement | Review final numbers carefully, including replacement-cost realities |

Most of the stress comes from uncertainty, not just the dispute itself. Once the process is organized, clients usually stop feeling trapped and start making decisions from a stronger position.

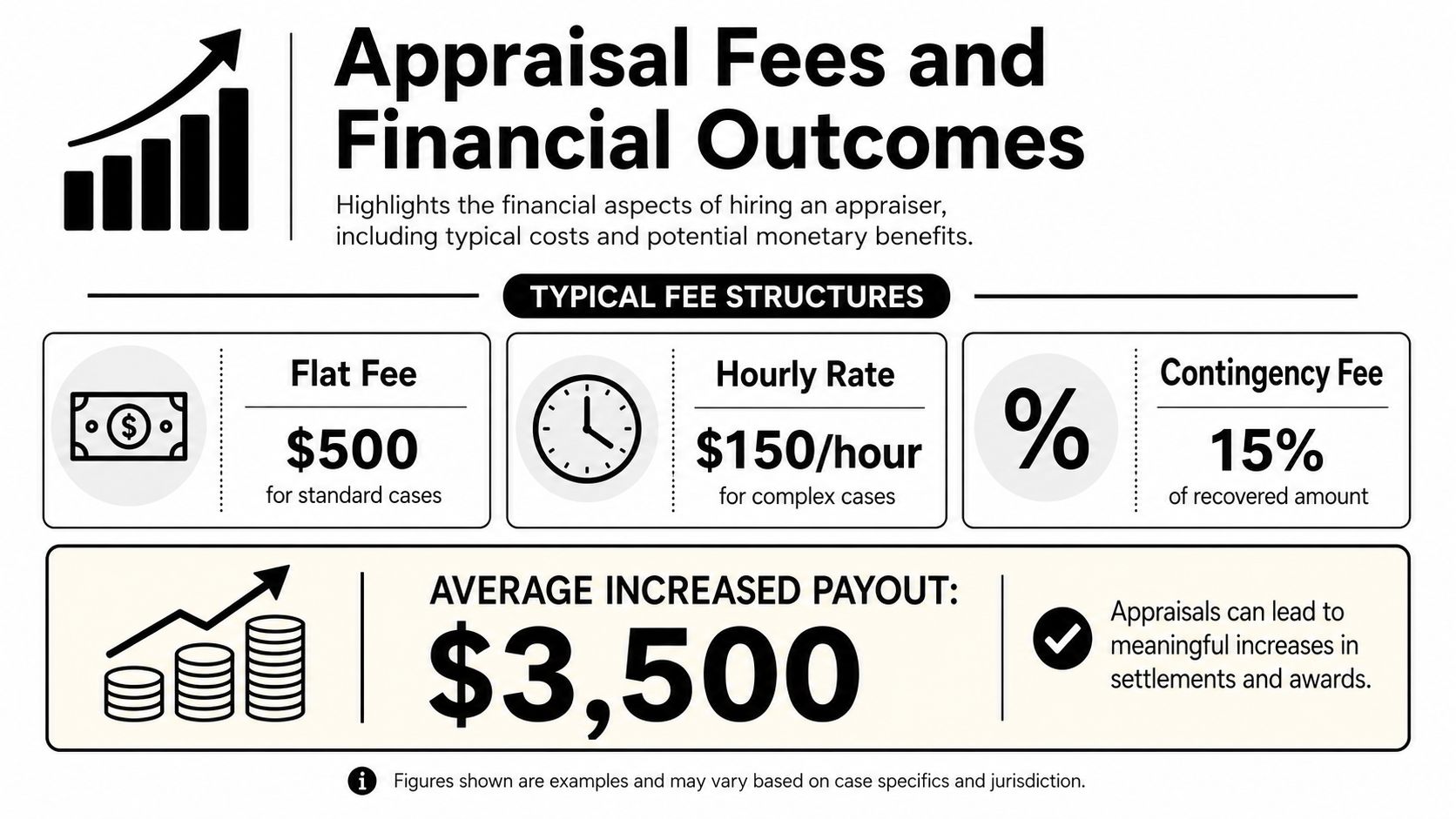

Appraisal Fees and Financial Outcomes

The first question most drivers ask is simple. Is hiring an appraiser worth it?

That depends on the size of the valuation gap, the type of vehicle, and how weak the insurer's number is. In practice, the fee question should be framed against the financial downside of accepting the wrong settlement too early. If the carrier is only off by a minor amount, the economics may be different. If the carrier is missing the mark by a meaningful margin, the appraisal can pay for itself quickly.

This visual covers the cost-benefit issue at a glance:

I'm not going to invent “typical” fees, because fee structures vary by appraiser, claim type, and whether the file involves a report only or full appraisal-clause representation. Ask directly how the appraiser charges, what the fee covers, and whether there are separate costs if the matter goes to an umpire.

What the documented outcomes show

There is public Oregon claim data showing that independent appraisal work can materially change the final settlement.

According to publicly posted Oregon total-loss case results, one Portland claim increased by $32,917, which was a 27% increase, and another Oregon case in Rogue River increased by $13,207, equal to an 18% increase.

Those are not small corrections. They show that, in some cases, the valuation issue is large enough to affect whether the owner can replace the vehicle properly or must absorb the shortfall personally.

A practical cost test

Ask three questions before deciding:

- How far apart are the numbers? If the insurer's offer obviously won't replace the vehicle, the appraisal has more room to matter.

- How nuanced is the vehicle? EVs, luxury trims, collector cars, and modified vehicles often justify deeper valuation work.

- How strong is your evidence without help? If your file is weak, a professional report may be the difference between a stalled complaint and a changed outcome.

A Portland auto appraiser isn't automatically worth hiring in every claim. But when the financial gap is real, the cost of doing nothing can be much higher than the appraisal fee.

Portland Auto Appraiser FAQs

Is diminished value worth pursuing on a newer EV or luxury vehicle

Often, yes. But not automatically.

Portland-focused appraisal guidance notes that a major question today is whether diminished value makes sense for modern EVs and late-model luxury vehicles, because those vehicles often involve higher repair costs, more severe claims, and more complicated post-repair valuation issues tied to ADAS, battery, and calibration work, as discussed in this review of EV and luxury diminished value issues in Portland. In plain terms, complex repairs can leave a stronger market stigma than many insurer tools account for.

What if the insurance company ignores my appraiser's report

That doesn't mean the report failed. It may mean the insurer is forcing the dispute into the next stage.

A solid appraisal report becomes most useful when it is part of a formal process, especially if your policy gives you appraisal rights. If the carrier won't negotiate reasonably, you may need to escalate beyond informal back-and-forth and force the value dispute into the contractual mechanism available under the policy.

How long does the process usually take

There's no honest one-size-fits-all answer.

Simple disputes can move quickly when the documentation is clean and the carrier is responsive. Complex files take longer, especially when the vehicle has unusual options, repair complexity, or a large gap between the insurer's number and the replacement reality. The fastest way to slow a claim down is incomplete paperwork and sloppy evidence.

What should I do before I accept the settlement

Pause and review the valuation line by line.

Check trim, mileage, condition, options, prior service, and whether the comparables resemble your vehicle. Then ask the question that matters most in Portland. Could you replace this vehicle, in similar condition, without paying the difference yourself? If the answer is no, the claim deserves a second look.

If your insurer's number looks neat but still leaves you short, talk to Total Loss Northwest. They provide certified independent appraisals for total loss and diminished value disputes in Oregon and Washington, and they can help you evaluate whether your claim has a real replacement-cost gap worth challenging.