You've probably already had the same reaction most drivers have. The insurance company sends a total loss offer, you read the number once, then again, and it still doesn't make sense. Your car was clean, maintained, maybe upgraded, maybe hard to replace locally, and somehow the offer looks like it was generated for a stripped-down version of your vehicle.

That's because it usually was.

Results for a Car Appraiser Near Me often include generic valuation sites or local listing pages that tell users what a car might be worth in broad terms. That's not enough when you're fighting a claim. You need someone who can document value, challenge the insurer's number, and in the right situation invoke the Appraisal Clause so the insurance company's software doesn't get the last word.

Why Your Insurance Offer Is Just a Starting Point

The first number you get from the insurer is not sacred. It's an opening position.

I've seen the same pattern over and over. A driver gets hit, the carrier totals the vehicle, then sends a valuation report that misses options, ignores recent market realities, or treats custom parts like they barely exist. The owner assumes the company has already done the hard math and that arguing won't matter. That's the mistake.

What the insurance company is really doing

Most insurance valuations are built to process claims at scale. That means speed, templates, and software. It does not mean your vehicle got the kind of careful market review a buyer or dealer would use when pricing a replacement.

That gap matters most when your car had any of the following:

- Upgrades that add real value such as wheels, suspension work, camper equipment, or specialty trim

- Condition above average because you maintained it better than the typical comparable

- Limited local supply when replacing the same make, model, and package isn't simple

- Repair-related stigma if the car wasn't totaled but lost resale value after the accident

People regularly ask whether a Car Appraiser Near Me can legally use the Appraisal Clause to remove insurance software bias. That gap is real, and most local pages don't explain it. As noted by Auto Appraisal on the Appraisal Clause issue, many “near me” results focus on valuation services but don't clarify that certified independent appraisers can formally invoke the clause in the right dispute.

Practical rule: If the insurer created the number, the insurer can be wrong. Treat the offer like a draft, not a verdict.

Why the Appraisal Clause changes the fight

The Appraisal Clause is the part most drivers never hear about until they've already accepted too little. It's usually built into the policy and gives you a formal path to dispute value. That matters because it shifts the argument away from “please reconsider” and toward a structured valuation process.

A certified independent appraiser isn't there to guess. Their job is to determine fair market value using actual documentation and defend it. That's very different from an instant online estimate.

If your vehicle was an RV tow vehicle, a specialty rig, or part of a larger accident situation, you may also be juggling repairs on another unit. In that case, a practical next step is to get your RV collision damage fixed while you separately deal with the valuation dispute on the totaled or damaged vehicle.

The point is simple. You have an advantage, and most policyholders don't use it.

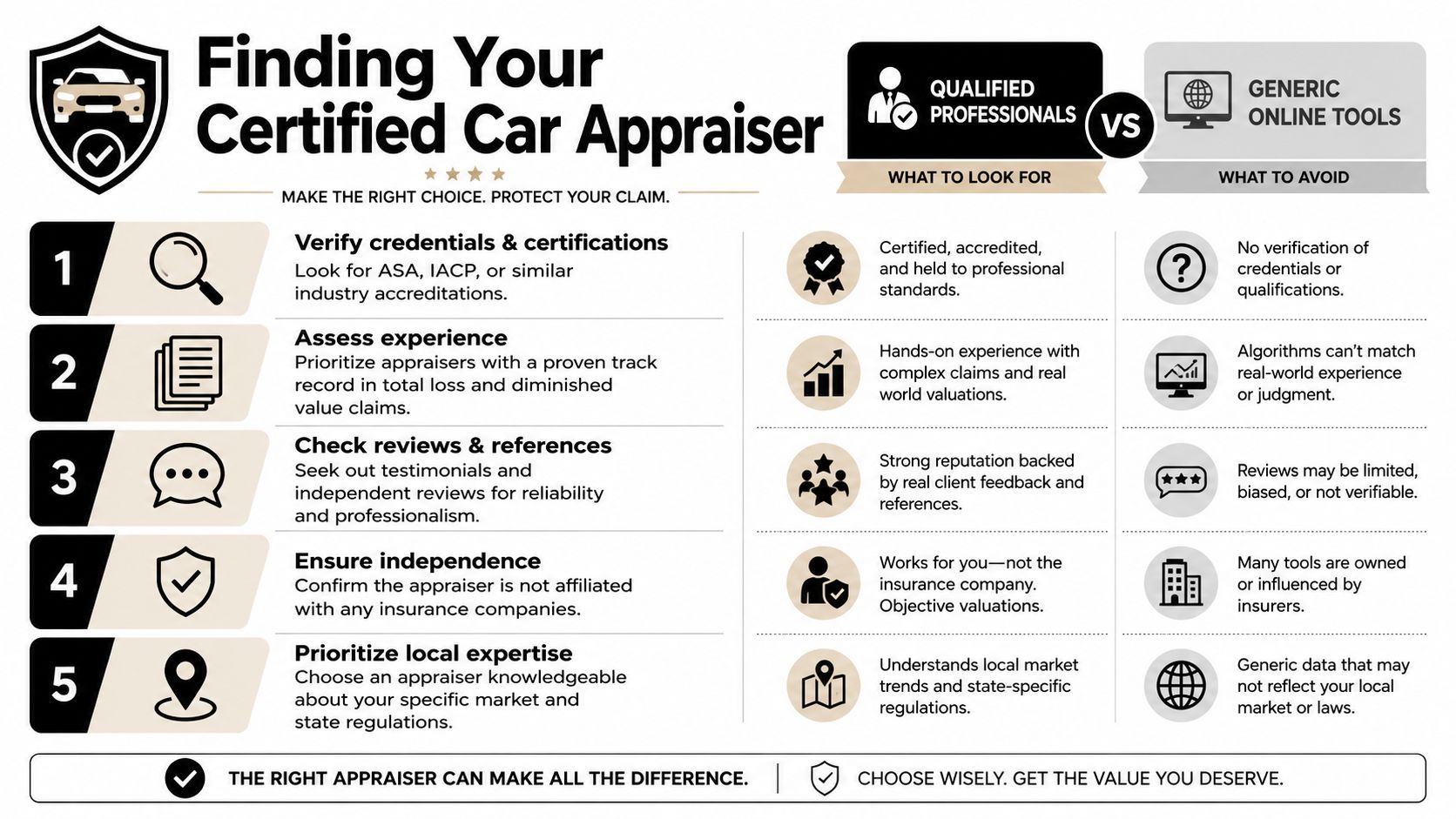

Finding a Certified Appraiser Not Just a Valuation Service

Typing Car Appraiser Near Me into a search bar is easy. Hiring the right person isn't.

A lot of results are junk for insurance disputes. Some are lead-gen directories. Some are instant pricing tools. Some are local shops that can tell you what they think a vehicle is worth but can't build a report that holds up when an adjuster pushes back. You need an appraiser whose work survives scrutiny.

What separates a real appraiser from a pricing website

A generic valuation site gives you a range. A certified independent appraiser gives you a documented opinion of value tied to your actual vehicle, your condition, and your market.

Use this quick comparison before you hire anyone:

| Option | Good for | Not good for |

|---|---|---|

| Online value tool | Rough ballpark pricing | Insurance disputes |

| Dealer trade estimate | Quick local opinion | Formal claim support |

| Body shop guess | Repair context | Total loss valuation arguments |

| Certified independent appraiser | Defensible total loss or diminished value report | Casual curiosity pricing |

If you're sorting options, one useful example of the kind of service you're looking for is an independent auto appraiser near you. The key isn't the phrase itself. It's whether the appraiser handles insurance disputes with formal reports and claim support.

Red flags I'd avoid immediately

Some appraisers talk a good game, then produce a flimsy report. That won't help you.

Watch for these problems:

- Formula-only reports. If they rely mostly on a canned equation, walk away.

- No inspection process. If they don't care about condition, options, or prior repairs, they're not valuing your vehicle properly.

- No discussion of comparable sales. A fair appraisal needs market evidence.

- Insurance relationships that sound too cozy. You want independence, not someone trying not to upset carriers.

- Vague deliverables. If they can't tell you what the report includes, don't hire them.

Appraisals based only on formulas like 17c get attacked for a reason. Certified Auto Appraisers explains that reports relying solely on mathematical formulas are routinely challenged because USPAP requires market evidence, not just computation. Thorough reports that document dealer quotes, inspection findings, and comparable analysis stand up much better.

If an appraiser says, “We just run the numbers,” that's not a strength. That's a warning.

What to ask before you hire

Don't overcomplicate the interview. Ask direct questions.

- Do you handle total loss disputes, diminished value claims, or both?

- Do you inspect the vehicle or repaired vehicle directly when needed?

- What market data do you use to support value?

- Can your report be used in negotiations or legal proceedings?

- Do you work independently from insurers?

- Can you help with the Appraisal Clause if my policy allows it?

A good appraiser should answer those without dancing around the question.

What a Proper Appraisal Report Should Contain

If you're paying for an appraisal, don't accept a one-page PDF with a number at the bottom. That's not a report. That's a receipt with opinions attached.

A proper appraisal is built to answer one question clearly. What was this vehicle worth in the market, in this condition, with these features, at the time of loss or after repair? Every part of the report should support that answer.

The core parts of a defensible report

A legitimate report should include a detailed description of the vehicle itself. That means year, make, model, trim, mileage, VIN details, options, package information, and relevant upgrades. If your insurer missed leather, tow packages, wheel packages, lift kits, performance parts, or specialty equipment, the report should document those items directly.

It should also include a condition analysis. Not a casual statement. A real analysis. Interior wear, exterior condition, prior damage history if relevant, tire condition, finish quality, and signs of unusually good or poor maintenance all matter.

Then comes the market work. Through this work, weak appraisals fall apart and strong ones win. The appraiser should compare your vehicle against real market indicators and explain why those comparables do or don't fit.

For diminished value claims, inspection matters more than people think

If your car was repaired and looks “fine,” that doesn't mean the value came back. A proper diminished value report needs evidence, not assumptions.

According to SnapClaim's overview of diminished value appraisal cost and methodology, a certified diminished value appraisal typically costs between $300 and $1,200, and the strongest methodology uses multiple sources such as NADA, KBB, Black Book, and auction results, plus a physical inspection, paint thickness measurements, and three or more dealer quotes with full accident disclosure.

That tells you two things. First, real appraisal work takes effort. Second, a formula-only shortcut isn't enough.

What you should expect to see in writing

Here's what I'd want in the report before I used it against an insurer:

- Vehicle identity and equipment with accurate trim, packages, and custom features

- Inspection findings with photos and notes tied to actual condition

- Market support from multiple recognized data points and comparable vehicles

- Adjustment logic explaining why mileage, condition, equipment, or local demand changed value

- Final value conclusion stated clearly and supported by the evidence

- Appraiser credentials and signature so the report has accountability behind it

A serious report shows its work. If you can't follow how the appraiser reached the number, the adjuster will attack it.

What a weak report looks like

Weak reports usually share the same flaws. They skip condition. They use broad database outputs without reconciling them. They don't explain local market realities. They don't address how the vehicle was equipped.

That's why the cheapest option often costs you the most. You're not paying for paper. You're paying for a report that can force a real response.

The Appraisal Process From Start to Finish

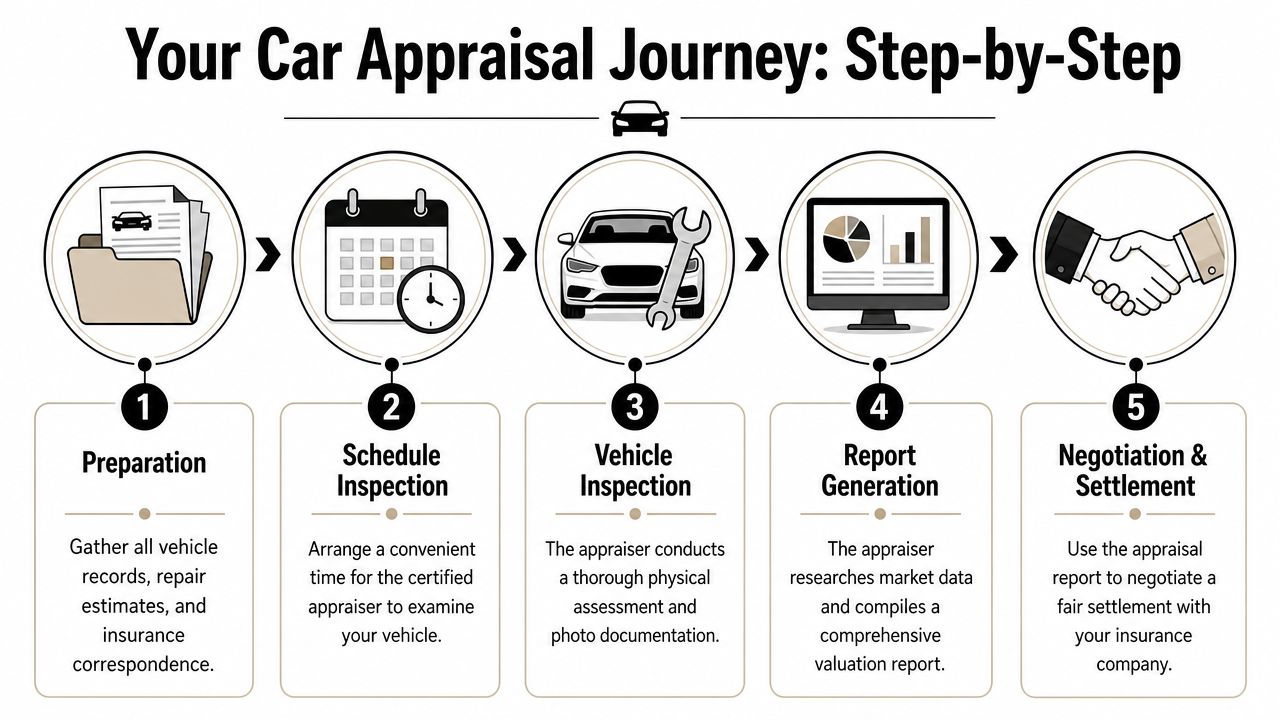

Most drivers delay getting help because they think the process will be messy. It's not. If you're organized, it's straightforward.

Start with your file. Pull together the insurance valuation report, the adjuster's written offer, photos of the vehicle, service records, receipts for upgrades, registration, title information if available, and any pre-loss photos that show condition. If it's a diminished value claim, gather repair invoices and the final repair estimate too.

Right after you have your documents, it helps to get your repair paperwork and shop communication organized in one place. If you've had trouble keeping that part straight, a workflow tool like FixyFlow for auto repair coordination can help you track estimates, records, and communication while the claim is still active.

Step one is choosing the right kind of help

Not every claim needs the same approach. A total loss dispute is different from a post-repair diminished value claim. Before you hire anyone, make sure they handle your exact situation.

If you're dealing with a total loss valuation dispute, this kind of car insurance appraisal service is the category to look for. What matters is that the appraiser works from market evidence and can support the claim through negotiation.

What happens during the appraisal

The appraiser reviews your documents, confirms the vehicle details, then inspects the vehicle when that's relevant and possible. For a repaired vehicle, inspection can be especially important because the report may need to document finish quality, panel work, or evidence of repairs that still affect resale value.

After inspection, the appraiser researches the market, selects and analyzes comparables, and writes the report. Then the report gets submitted to the insurer or used in a demand package, depending on the claim.

This video gives a helpful overview of how vehicle valuation disputes can play out:

Where the Appraisal Clause matters most

The negotiation stage is where people usually get emotional and lose ground. Don't do that. Let the report do the heavy lifting.

In Oregon, there's a major advantage here. The FD Auto appraisal clause FAQ for Oregon and Washington states that invoking the Appraisal Clause for total loss disputes in Oregon typically means the insurance company pays the independent appraiser's fee, making the service effectively free to the policyholder in most cases.

That changes the math for a lot of people. If you're in Oregon and the insurer's offer is low, there's even less reason to roll over.

Your job during the process

Your role is simple:

- Be complete. Give the appraiser every record that supports condition, maintenance, and equipment.

- Be accurate. Don't exaggerate condition or upgrades.

- Be responsive. Claims slow down when drivers disappear for days.

- Be disciplined. Don't accept a revised offer until the appraisal work is finished.

The fastest way to weaken your claim is to settle while the evidence is still being built.

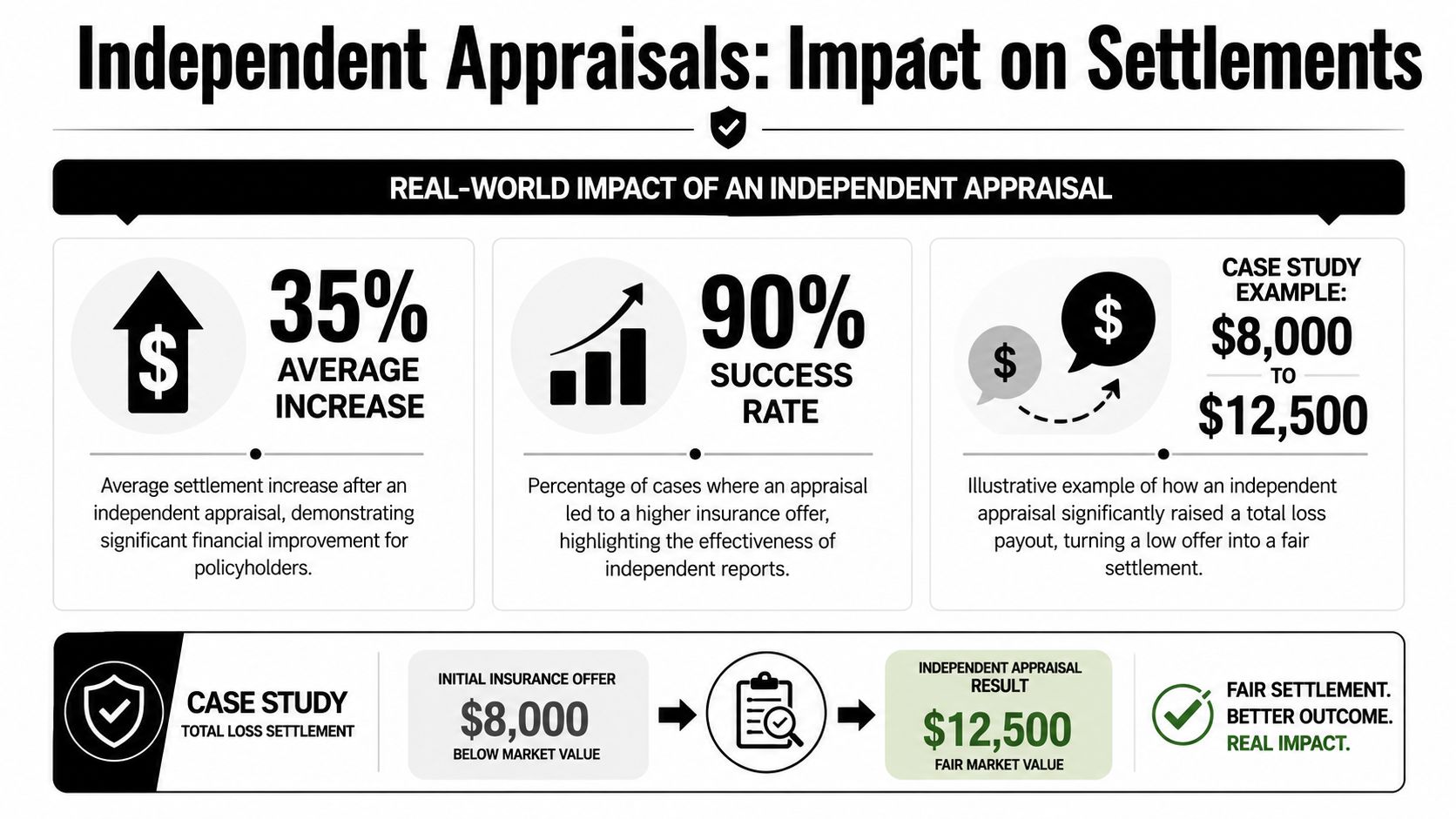

Real Results How Appraisals Impact Settlements

Your insurer offers $4,543 for a totaled car you could not replace for anywhere close to that amount. You argue. They point to their valuation system. That is the moment many drivers lose, because they keep debating the number instead of forcing a real valuation process.

A proper appraisal changes the settlement by replacing insurer software with documented market evidence. If your policy allows the Appraisal Clause, that evidence can force the carrier out of its internal pricing box and into a binding dispute process.

One documented Washington case shows the importance of this step. According to Total Loss NW, an insurance company initially offered $4,543 for a total loss. After an independent appraisal, the settlement increased to $12,626. That's an $8,083 increase and a 178% jump over the original offer. The same source states that Total Loss NW has helped clients achieve an average increase of +180% over original offers.

Why settlements rise after appraisal

Insurance valuations miss money in predictable ways. The software grabs weak comparables. The adjuster misses trim packages, options, service history, or specialty equipment. Local replacement cost gets flattened into a generic number.

A skilled appraiser corrects those errors with photos, comparable analysis, option verification, condition adjustments, and market support. Then the Appraisal Clause gives that report legal weight. That is the part drivers overlook, and it is why a real appraiser beats a basic online pricing printout.

Here's where the biggest changes usually show up:

| Claim type | What insurers often miss | What a strong appraisal adds |

|---|---|---|

| Total loss daily driver | Local replacement reality, options, condition | Better comparable selection and adjustments |

| Custom or enthusiast vehicle | Aftermarket parts and specialty demand | Equipment documentation and market support |

| Repaired vehicle with diminished value | Post-accident stigma despite clean repairs | Dealer input, inspection findings, market-backed resale loss |

Diminished value can cost you after repairs

A repaired car can still be worth less. Buyers, dealers, and lenders see the accident history and price the vehicle accordingly.

A search for a Car Appraiser Near Me after repairs often points to the wrong service. You do not need a replacement value dispute. You need proof of market stigma and resale loss. That is a different claim, and it calls for diminished value appraisals that focus on post-repair market impact.

The pattern is simple. Drivers who accept the first offer usually assume the insurer's number is final, or that fighting back will cost too much time and money. Insurers count on that.

The Washington case above shows what happens when someone stops arguing and invokes a formal valuation process backed by evidence. A low offer can move sharply when the claim is pushed out of insurer software and into appraisal. That is how you get paid based on the actual market, not the carrier's preferred number.

Your Next Steps and Questions to Ask

If you've been lowballed, don't waste time arguing from memory. Don't tell the adjuster you “feel” the car was worth more. That goes nowhere. Build the case properly.

Start by deciding what kind of claim you have. If the car was declared a total loss, you need a market-backed value dispute. If the car was repaired, ask whether you also have a diminished value claim. That second issue gets missed constantly.

A frequently overlooked problem is the repaired vehicle that looks spotless but still sells for less. JMK Classic Cars notes that diminished value affects 30% to 40% of repaired vehicles nationally, and even minor accidents can cause 10% to 20% permanent value loss due to market stigma. That's exactly why you shouldn't assume “looks like new” means “worth the same.”

Questions I'd ask any appraiser before signing

Use this checklist and keep it blunt:

- What types of claims do you handle most often? You want someone who regularly works total loss or diminished value claims, not general pricing.

- Do you use market evidence or mostly formulas? If the answer sounds formula-heavy, move on.

- Will your report document condition, comparables, and adjustments clearly? If not, it won't carry much weight.

- Have you worked with my insurer before? Prior experience helps, but independence matters more.

- Can you help invoke the Appraisal Clause when the policy allows it? If they dodge this question, that's a problem.

- What documents do you need from me right now? A competent appraiser will answer this instantly.

My recommendation

Pick the person who can do three things well. Identify the right claim. Build a report that can survive pushback. Use the Appraisal Clause when it's available and strategically useful.

If you're in Oregon or Washington, don't settle for a generic valuation service that just prints a number. You need someone handling insurance disputes as a core service, not a side offering.

You don't have to accept the insurer's first number, and you don't have to fight blind. Get the file together. Ask sharper questions. Hire someone who can prove value, not just talk about it.

If you want specialized help with a low total loss offer or a post-repair diminished value claim, Total Loss Northwest provides certified independent auto appraisals for drivers in Oregon and Washington and can invoke the Appraisal Clause in the right cases to challenge insurer valuations with market-backed reports.