Your phone is buzzing. Your car is damaged. The other driver shrugs and says they don't have insurance, or they disappears and you find out later they weren't covered at all. Individuals often freeze right there. They assume they're stuck, their car is worth whatever the insurer says it's worth, and the process is just paperwork.

That's the mistake.

An uninsured motorist settlement can pay real money, but only if you treat the claim like a financial dispute, not a customer service interaction. Your insurer may be your carrier, but in a UM claim they're also the party deciding how little they can pay while still closing the file. If you don't document, value, and push back correctly, you'll leave money on the table.

The good news is you already bought the safety net. Now you need to use it well.

After the Crash What Happens Next

Right after the collision, most drivers focus on the obvious problems. Is anyone hurt? Can the car move? Who's calling the police? Then the second wave hits. The at-fault driver has no insurance, not enough insurance, or no intention of cooperating. That's when panic starts.

Slow down and get practical.

Uninsured motorist coverage exists for exactly this situation. You paid premiums for protection against irresponsible drivers. That means you may still have a path to recover for injuries, lost income, and in some cases damage-related losses tied to the claim. The claim doesn't become easy, but it does become manageable if you stop thinking like a victim and start thinking like a file-builder.

Practical rule: The first hours after the crash shape the entire value of your claim. Bad documentation creates cheap settlements.

You don't need to know every legal detail on day one. You do need to preserve evidence, notify the right people, and avoid casual statements that damage your case. Most low settlements start with small early mistakes. A weak police report, incomplete photos, delayed treatment, a recorded statement given too soon. Those are the gaps adjusters use.

The goal is simple. Prove fault. Prove damages. Prove the missing or inadequate insurance. Then make the carrier value your losses with real evidence, not shortcuts.

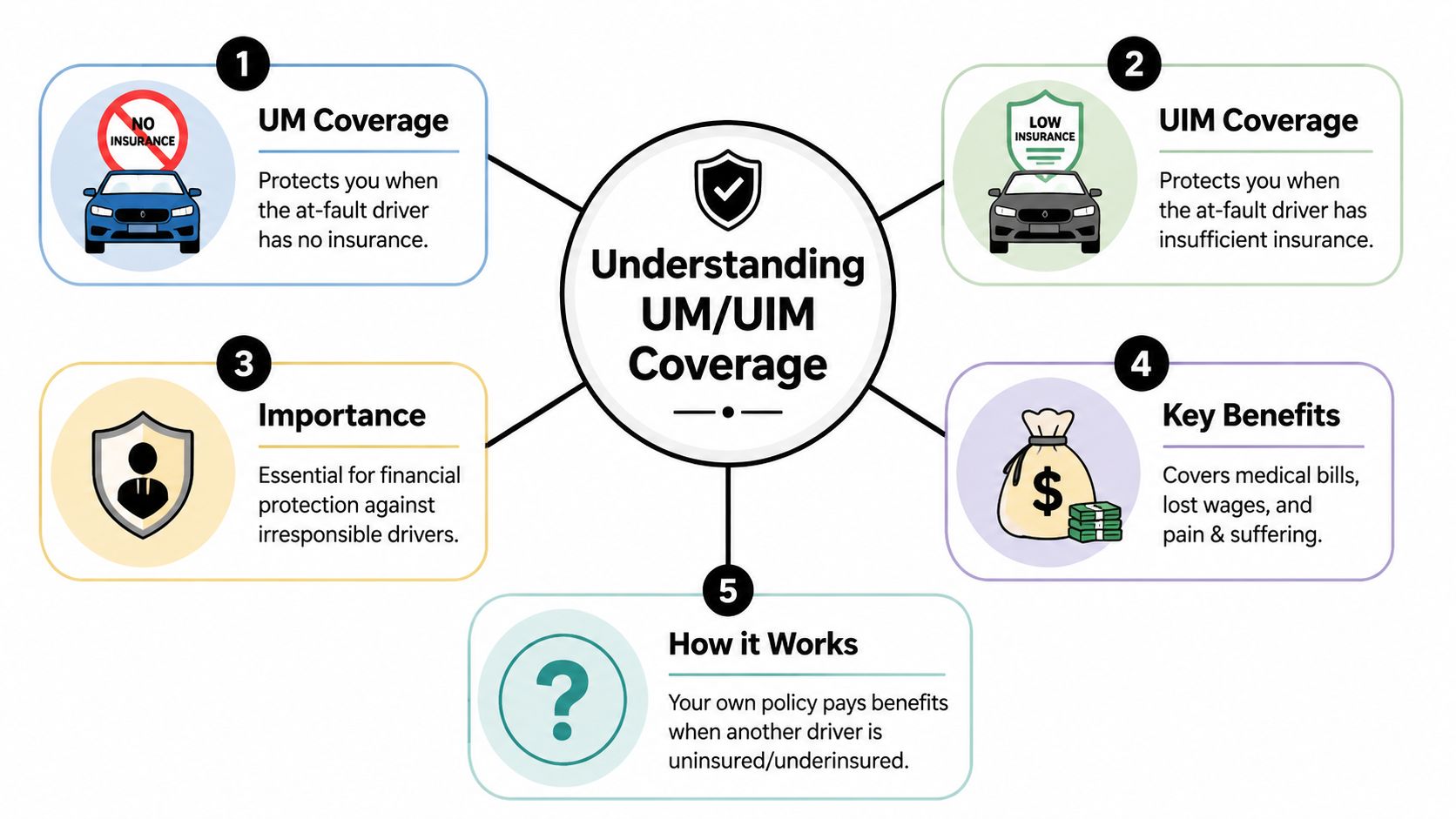

Understanding Your Uninsured Motorist Coverage

Most drivers carry UM or UIM coverage without understanding how it works until after a wreck. By then, the declarations page suddenly matters more than the premium ever did.

Think of UM and UIM as insurance for the other driver's failure. If the at-fault driver has no coverage, uninsured motorist coverage steps in. If the at-fault driver has coverage but not enough to pay for the harm they caused, underinsured motorist coverage may fill part of the gap.

If you want a cleaner breakdown of the basic policy language before digging into your own declarations page, this overview of uninsured motorist coverage is a good starting point.

What you have to prove

A UM claim is not automatic. To recover, you must establish three technical elements: the at-fault driver was legally liable, you suffered quantifiable damages, and the at-fault driver had no insurance or insufficient limits to cover those damages, as explained in this analysis of Alabama uninsured motorist coverage.

That matters because your own insurer doesn't just open the checkbook because you called. They step into an adversarial role and evaluate the file the way a liability carrier would. You're making a first-party claim under your policy, but you're still proving a third-party accident case.

UM versus UIM in plain English

Use this quick comparison to keep the terms straight:

| Coverage type | Trigger | Common purpose |

|---|---|---|

| UM | The at-fault driver has no insurance | Protects you when there's no liability policy to pursue |

| UIM | The at-fault driver has insurance, but not enough | Helps when damages exceed the at-fault driver's available limits |

That difference sounds simple, but carriers know the two are often blurred.

Bodily injury and property damage aren't the same claim

Your policy may split coverage into separate parts. The names vary by carrier, but the practical distinction is consistent:

- UM bodily injury: Covers personal losses such as medical bills, wage loss, and other injury-related damages if the policy applies.

- UM property damage: Applies to vehicle damage in some policies and states, but don't assume it's included.

- Collision coverage: Often handles repairs or total loss issues even when the other driver is uninsured.

Read the declarations page, then read the endorsements. Don't rely on what you think you bought.

Your declarations page is not a summary for convenience. It's the map to the money.

What your policy will not do

Even strong UM coverage has limits. It doesn't create unlimited recovery. It pays according to the contract you purchased, and the carrier will enforce every condition, deadline, and procedural requirement in that contract.

That means you need to know three things early:

- Your coverage limits

- Your notice requirements

- Your dispute resolution language, especially any appraisal or arbitration provisions

Those details determine your bargaining position later. If you don't know the policy, you can't negotiate from strength.

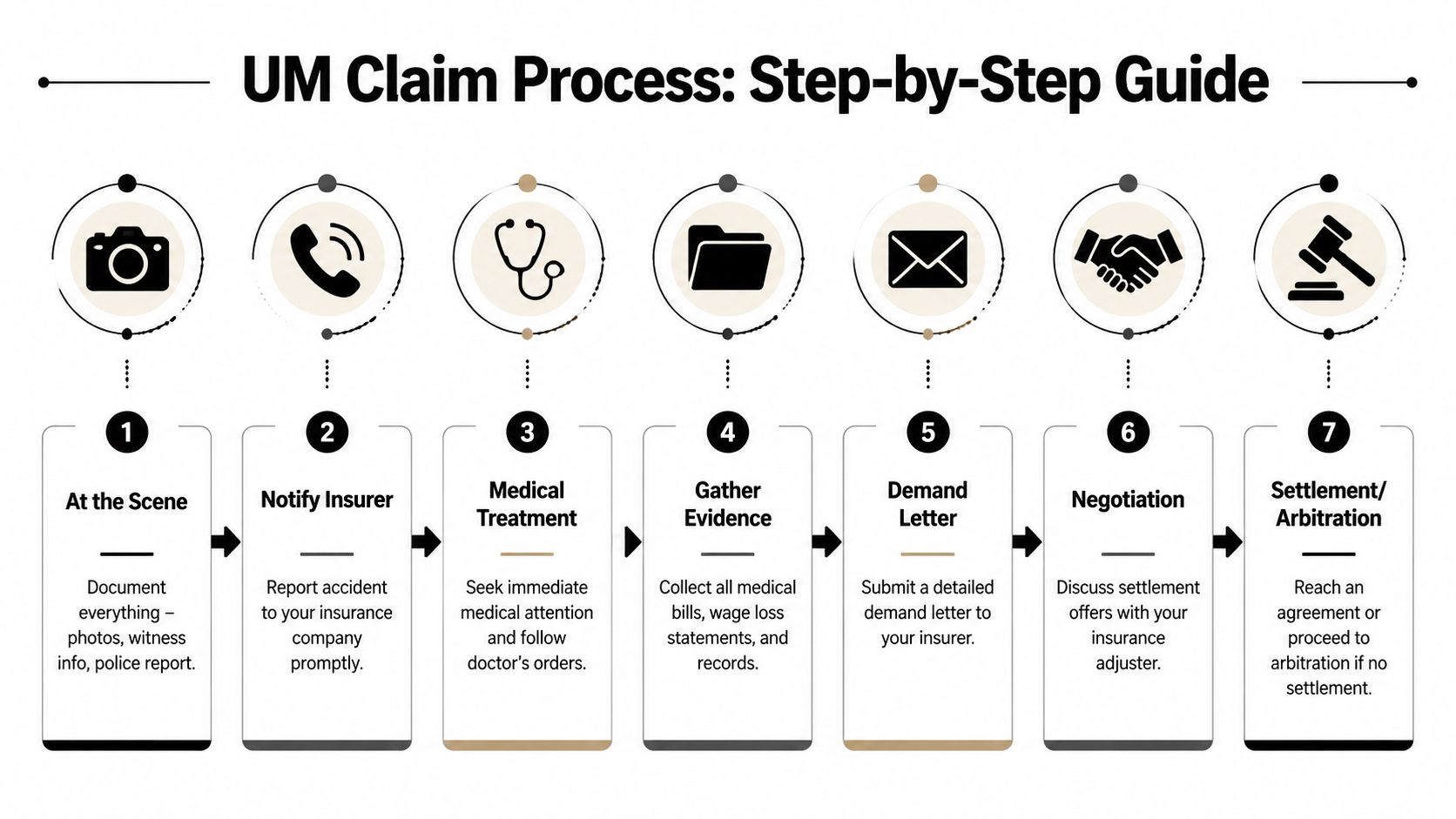

The UM Claim Process from Start to Finish

The claim starts at the crash scene, not when the adjuster calls. That's where many claimants get behind. They think the evidence can wait. It can't.

Start by securing the basics. Call the police. Get medical attention if you may be hurt. Photograph every angle of the vehicles, the roadway, debris, skid marks, weather, traffic controls, and the other driver's information if you can get it. If there are witnesses, get names and phone numbers before they leave.

If you need hands-on help organizing the claim file and communications, use professional insurance claim support. A messy file gives the insurer room to minimize your losses.

At the scene and in the first day

What you do immediately affects credibility later.

- Call law enforcement: A police report anchors the event in time and helps document fault, driver identity issues, and insurance problems.

- Take broad and close photos: Get the damage, but also get context. Lane position, intersection layout, impact points, glass, and paint transfer matter.

- Avoid casual blame-sharing: Don't say “I didn't see them” or “I might've been going a little fast.” Adjusters remember every loose statement.

- Get checked out: If you're injured, or think you might be, create the medical record now.

A short treatment gap can turn into a long argument.

Here's a useful walk-through if you want a visual summary before talking to the adjuster:

Opening the UM claim

Once you're safe and the initial evidence is preserved, report the loss to your insurer. Be prompt. Policies often require formal notice within a short window, and the same Burress Law analysis notes that failure to meet notice deadlines or contractual arbitration windows can forfeit coverage even when the general statutory period remains open.

When you report the claim, keep it simple and factual:

- date and location of loss

- vehicles involved

- known injuries

- police report status

- whether the other driver lacked insurance or appeared underinsured

Don't volunteer opinions. Don't guess about medical recovery. Don't accept fault framing from the first intake rep.

Build the file like you're going to have to prove everything

Most claimants underestimate how much paper wins these cases. You need a clean file that shows both liability and damages.

Create one folder, physical or digital, and keep:

- Medical records and bills

- Pay records and missed-work documentation

- Repair estimate, tow bill, storage bill, and rental records

- Photos and video

- Police report and witness contacts

- Every email and letter from the insurer

If it's not documented, the insurer treats it as negotiable or nonexistent.

Demand, response, and dispute

After treatment stabilizes and the losses are documented, you or your representative package the claim and demand payment. The adjuster reviews it, often asks for more records, then makes an offer.

That offer is not a verdict. It's a negotiating position.

The process usually moves through these stages:

- Initial claim notice

- Investigation

- Document exchange

- Demand package

- Offer and counteroffer

- Settlement, arbitration, or another contractual dispute process

Don't rush to close the file just because the insurer sounds cooperative. Friendly adjusters can still deliver weak valuations.

How to Properly Value Your Claim and Prove It

The biggest financial mistake in an uninsured motorist settlement is accepting the insurer's valuation as if it were objective. It isn't. It's an internal number built from their software, their assumptions, their comparables, and their preferred interpretation of your records.

You need your own valuation logic.

For the vehicle side of the claim, an independent fair market vehicle valuation gives you a much stronger foundation than reacting to the insurer's number.

Your claim has more than one bucket of value

A solid UM file separates losses into categories instead of throwing everything into one emotional demand.

| Damage category | What proves it |

|---|---|

| Medical expenses | Bills, records, treatment notes, provider recommendations |

| Lost income | Employer verification, pay stubs, tax records if applicable |

| Pain and suffering | Treatment history, daily limitations, consistent records |

| Vehicle loss | Repair documentation, condition evidence, market valuation, appraisals |

The more organized the categories, the harder it is for the adjuster to blur them together and shave them down.

Vehicle value is where insurers cut corners fast

When your car is repairable, the insurer will focus on the repair bill. That's incomplete. A properly repaired vehicle can still lose resale value because it's now an accident-history vehicle. That's diminished value, and many owners never claim it because nobody tells them to.

When your car is a total loss, the problem changes. The carrier may rely on valuation platforms such as CCC or similar tools that often miss real-world condition, options, upgrades, rarity, maintenance history, or the local market. If the comparables are weak, the offer will be weak.

Here is the practical divide:

- Repairable vehicle: Ask whether diminished value applies and what evidence will prove post-repair market stigma.

- Total loss vehicle: Challenge the actual cash value if the comparable vehicles are inferior, mis-equipped, distant, or badly adjusted.

Diminished value reports are leverage, not decoration

A diminished value report should do more than state that the car lost value. It should document why. Severity of damage, structural involvement, replaced panels, repaint work, prior condition, market desirability, and sales impact all matter.

That report gives you a basis to say, “Your repair payment didn't make me whole.” Without it, you're arguing from frustration. With it, you're arguing from market evidence.

A body shop invoice proves what was repaired. It doesn't prove what the vehicle is worth after the repair.

This matters even more for luxury vehicles, performance cars, newer models, collector vehicles, and customized vehicles. Buyers discount accident history. Insurers know that. They just hope you won't push the issue.

Total loss appraisals can dismantle a lowball offer

If the insurer declares the vehicle a total loss, don't look only at the top-line number. Inspect the valuation report line by line.

Check for these common problems:

- Wrong trim or options: Missing packages, upgraded wheels, ADAS features, premium audio, towing equipment

- Condition downgrades: Interior, exterior, tire, and mechanical condition marked lower than reality

- Bad comparables: Vehicles with more mileage, poorer condition, salvage history, or irrelevant geography

- Unsupported adjustments: Math that reduces value without a clear market reason

A certified independent appraisal can expose those flaws. Once you have a better-supported market value, the conversation changes. You're no longer saying the offer feels unfair. You're saying the offer is unsupported.

The appraisal clause is one of the strongest tools policyholders ignore

Many policies contain an Appraisal Clause for property value disputes. If the insurer and policyholder disagree on the amount of loss, that clause can force the valuation issue out of the adjuster's hands and into a formal appraisal process.

That matters because adjusters often hide behind software outputs. The appraisal clause shifts the fight to competing evidence and appraiser opinions. That's where a weak formula can lose to a strong file.

Use it when:

- the total loss offer is tied to bad comparables

- the insurer refuses to recognize real condition or options

- diminished value is being dismissed without real analysis

- negotiations stall because the adjuster repeats the initial number

This is not a magic wand. It is a contract tool. But contract tools work when people use them.

What a persuasive valuation package looks like

The strongest packages usually include a combination of the following:

- Vehicle photos from before and after the loss

- Maintenance records

- Window sticker or build sheet if available

- Independent market valuation

- Diminished value report for repaired vehicles

- Total loss appraisal for ACV disputes

- A concise written summary pointing out errors in the insurer's valuation

Short beats dramatic. Specific beats angry. A two-page rebuttal with clean exhibits often does more than a long emotional letter.

Negotiating Your Uninsured Motorist Settlement

Your own insurer isn't your ally in this phase. That's the hard truth many individuals resist, and it costs them money.

In a UM claim, the carrier has a direct financial reason to reduce what it pays. The file may sound polite. The adjuster may sound sympathetic. None of that changes the economics. They save money when you accept less.

Don't confuse responsiveness with fairness

Some adjusters move quickly because they want closure before the claim matures. Early treatment gaps, incomplete wage proof, and unresolved vehicle valuation issues all favor the insurer. A fast offer often means they think your file is still cheap.

A common point of confusion is policy limits. As discussed in this Reddit discussion on UM recovery limits, UM coverage pays up to the policyholder's purchased limits, not automatically the full amount of medical bills, lost wages, and pain and suffering, and recovery may also be reduced by comparative negligence principles.

That means two things are true at once. First, you should push hard for full value. Second, you need to understand where the contractual ceiling is so you don't negotiate blindly.

How to answer a low offer

Don't respond with outrage. Respond with structure.

Use a counter that does three jobs:

- Identify what they missed: wrong vehicle comps, omitted wage records, incomplete treatment review

- Attach proof: reports, records, photos, employer confirmation, valuation analysis

- State your number and why it changed: make the logic visible

A blunt but effective response sounds like this in substance: your offer doesn't account for the documented vehicle condition, the independent valuation, the completed treatment records, and the wage loss support already provided. Based on the enclosed documentation, the claim value is X within available limits.

That's negotiation. Not venting.

Leverage comes from evidence, not personality

If you're trying to improve your negotiation approach overall, this guide to better settlement outcomes is worth reviewing because it reinforces the same practical principle. Settlements improve when claimants present organized proof and refuse to let the first number anchor the entire discussion.

Here are the habits that usually move the file in your favor:

- Keep everything in writing: Confirm phone calls by email.

- Set response windows: Give the adjuster a reasonable deadline to respond to your package.

- Ask direct questions: Which records did you rely on? Which comparables support that number? What policy language are you using?

- Escalate when needed: If the adjuster is stuck, ask for a supervisor review or invoke the policy dispute process that applies.

Calm pressure beats emotional pressure almost every time.

When to stop negotiating and force the next step

There comes a point when repeated discussion is wasted effort. If the insurer keeps recycling the same unsupported number, stop feeding the loop.

Move to the next available mechanism if the policy supports it:

| Problem | Better response |

|---|---|

| Low total loss value | Independent appraisal and appraisal clause review |

| Ignored diminished value | Formal written rebuttal with report support |

| Injury value dispute | Arbitration prep or legal review |

| Delay tactics | Written demand for status and escalation |

Don't let a stale file sit. Insurance companies benefit from drift. You don't.

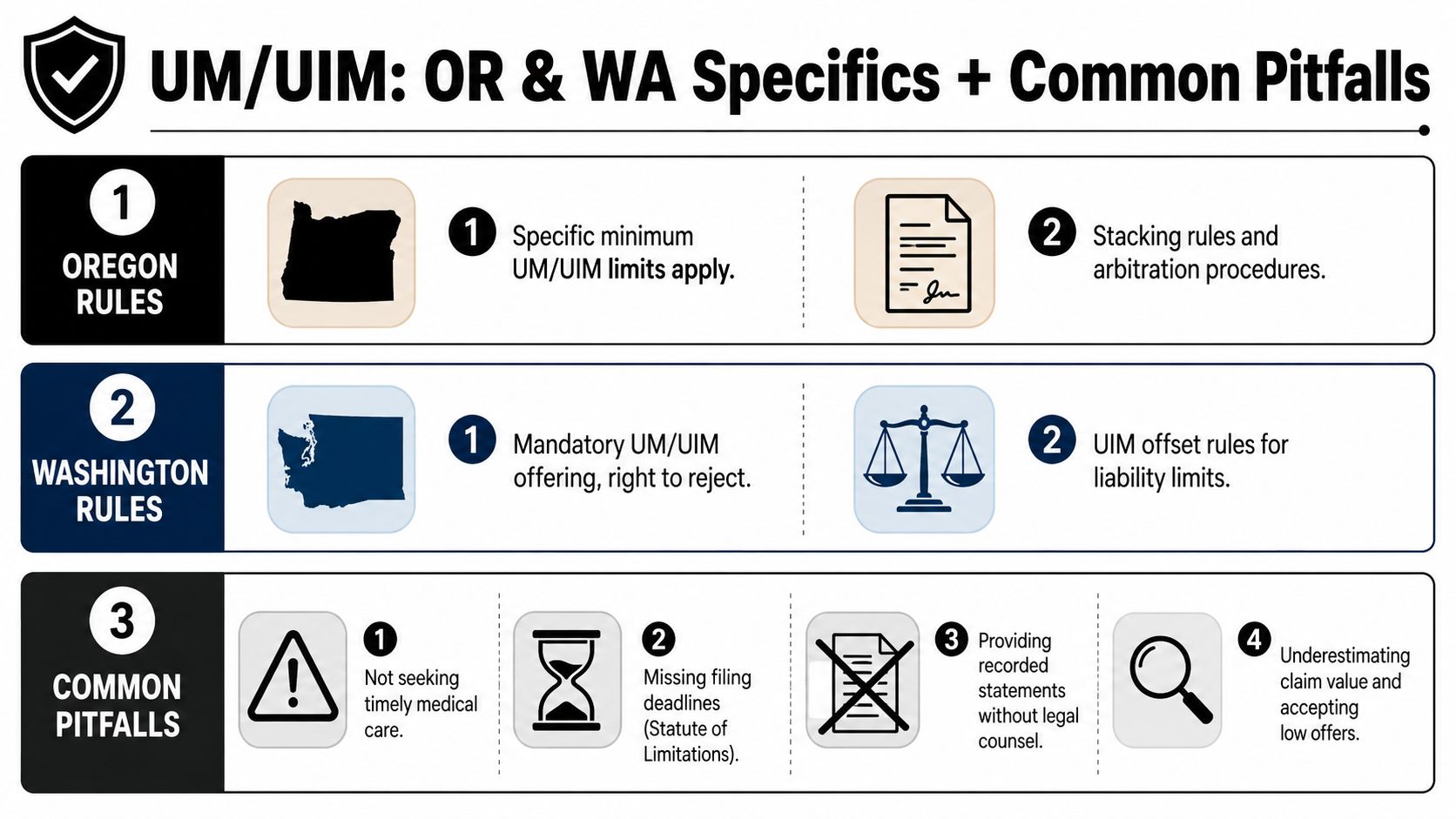

Critical Rules in Oregon and Washington and Common Pitfalls

Drivers in Oregon and Washington need to pay attention to policy language and state-specific rules, but the larger point is simpler. A good uninsured motorist settlement usually turns on details commonly overlooked until it's too late.

Oregon and Washington issues to check early

Don't assume your policy works the same way your neighbor's does. Read the endorsements and declarations page with these questions in mind:

- Was UM or UIM offered, accepted, or rejected clearly? Washington policies often involve a right to reject offered coverage, so the paperwork matters.

- Does the policy include PIP, MedPay, or both? Immediate injury payments and later offsets can affect strategy.

- Is stacking allowed or restricted? Multi-vehicle or multi-policy situations can change the amount available.

- What dispute language applies? Arbitration terms, notice provisions, and appraisal procedures can change how you fight back.

Those aren't technical side notes. They influence the negotiation.

Hit and run confusion causes real claim damage

One of the most misunderstood issues is the difference between UM and UIM in hit-and-run cases. The distinction matters because people often claim under the wrong theory or fail to gather the right evidence.

As explained in this California UM claims guide discussing hit-and-run eligibility, UM can apply in hit-and-run accidents involving physical contact, while UIM requires exhausted liability limits from a known at-fault party. That's a California-specific legal discussion, but the practical lesson travels well. If the driver is unidentified, don't casually assume UIM is the right lane.

For Oregon and Washington drivers, that means you should document the hit-and-run aggressively:

- Get the police report started immediately

- Photograph contact damage thoroughly

- Preserve dashcam and surveillance footage

- Identify witnesses before they disappear

If contact or identification becomes disputed later, you want a record created at the beginning, not a memory rebuilt later.

The most expensive mistakes I see

These errors show up again and again, and they all reduce value.

Giving a recorded statement too early

You don't have to fill every silence. Early recorded statements often lock people into incomplete facts before injuries develop or vehicle issues are understood. Give basic notice, then slow down and prepare.

Settling before the vehicle is valued correctly

This is a major one. Owners focus on repairs or the injury side and forget the actual market loss to the car. If the vehicle is repairable, diminished value may exist. If it's a total loss, the offer may be built on weak comparables. Once you sign off, your bargaining power vanishes.

Missing policy deadlines

The general legal deadline is not the only deadline that matters. Policies can impose notice requirements and arbitration windows. Miss one and you may hand the insurer a coverage defense.

Accepting the first offer because it feels official

Official doesn't mean accurate. It means written on company letterhead.

The first offer is often a test of how informed you are, not a statement of maximum value.

A final checklist before you agree to anything

Use this quick review before signing a release or accepting a total number:

- Have you confirmed all applicable coverages and limits?

- Have you finished or stabilized medical treatment enough to value the injury claim responsibly?

- Have you reviewed the vehicle valuation for errors in trim, options, mileage, and condition?

- Have you considered diminished value if the vehicle was repaired?

- Have you checked whether appraisal or arbitration rights apply?

- Have you kept the negotiation record in writing?

If any answer is no, you're probably not ready to settle.

A strong uninsured motorist settlement doesn't happen because the insurer decides to be generous. It happens because the claimant builds a better file, protects deadlines, proves loss, and pushes valuation disputes into a forum where evidence matters more than convenience.

If your carrier is lowballing a total loss or ignoring post-repair value loss, Total Loss Northwest can help you fight back with independent diminished value reports, total loss appraisals, and Appraisal Clause support across Oregon and Washington. When the insurer's number doesn't match the actual market, get a valuation that does.