The insurance letter is sitting on your counter, and the offer inside feels wrong. Maybe the adjuster called it “fair market value.” Maybe they paid for repairs but ignored what the accident did to the vehicle's resale value. Either way, you're stuck with a familiar question at this point: How do you write a demand letter that an insurer has to take seriously?

A good demand letter isn't a rant. It isn't a threat. It's a clean, documented argument that makes it harder for the carrier to dismiss you with a form response. Most bad letters fail for the same reason. They rely on emotion, skip proof, and bury the actual ask.

Most guides are also behind the times. They still assume certified mail alone is enough. It isn't. Insurers increasingly route claims through digital workflows, and if your demand only arrives on paper, it may sit longer than it should. The modern version of how to write a demand letter includes the writing, the evidence, and the delivery method.

Why Your First Demand Letter Matters

The first real mistake many claimants make is treating the insurer's first offer as the center of the discussion. It isn't. It's a starting position. If you answer with a scattered email or an angry voicemail, the adjuster still controls the frame. If you answer with a focused demand letter, you take that control back.

What the letter actually does

A demand letter does three jobs at once:

- States the dispute clearly so the adjuster can't pretend your complaint is vague

- Shows your evidence in a logical order, rather than as a pile of attachments

- Sets terms for response so the claim moves on your timeline, not only theirs

That matters because insurance files are handled by people under pressure. If your file is easy to dismiss, it often gets dismissed. If your file is organized, specific, and tied to documents, it usually gets escalated or answered more carefully.

Practical rule: The strongest demand letters read like a professional summary, not a personal diary.

Power shifts when the facts are organized

Say you were not at fault, your vehicle was repaired, and the insurer says the matter is closed. You know the car isn't worth what it was before the accident. A weak response says, “I disagree and want more money.” A strong response says, “Here is the incident date, claim number, repair history, appraisal support, and the amount demanded to resolve the loss.”

That shift matters. You stop sounding frustrated and start sounding prepared.

A first demand letter also becomes the record everyone will refer back to later. If negotiations continue, the adjuster reviews it. If a supervisor gets involved, they review it. If the claim moves toward appraisal, mediation, or attorney review, your letter becomes the starting document.

That's why learning how to write demand letter material the right way isn't about sounding legal. It's about making your position easy to understand and hard to brush aside.

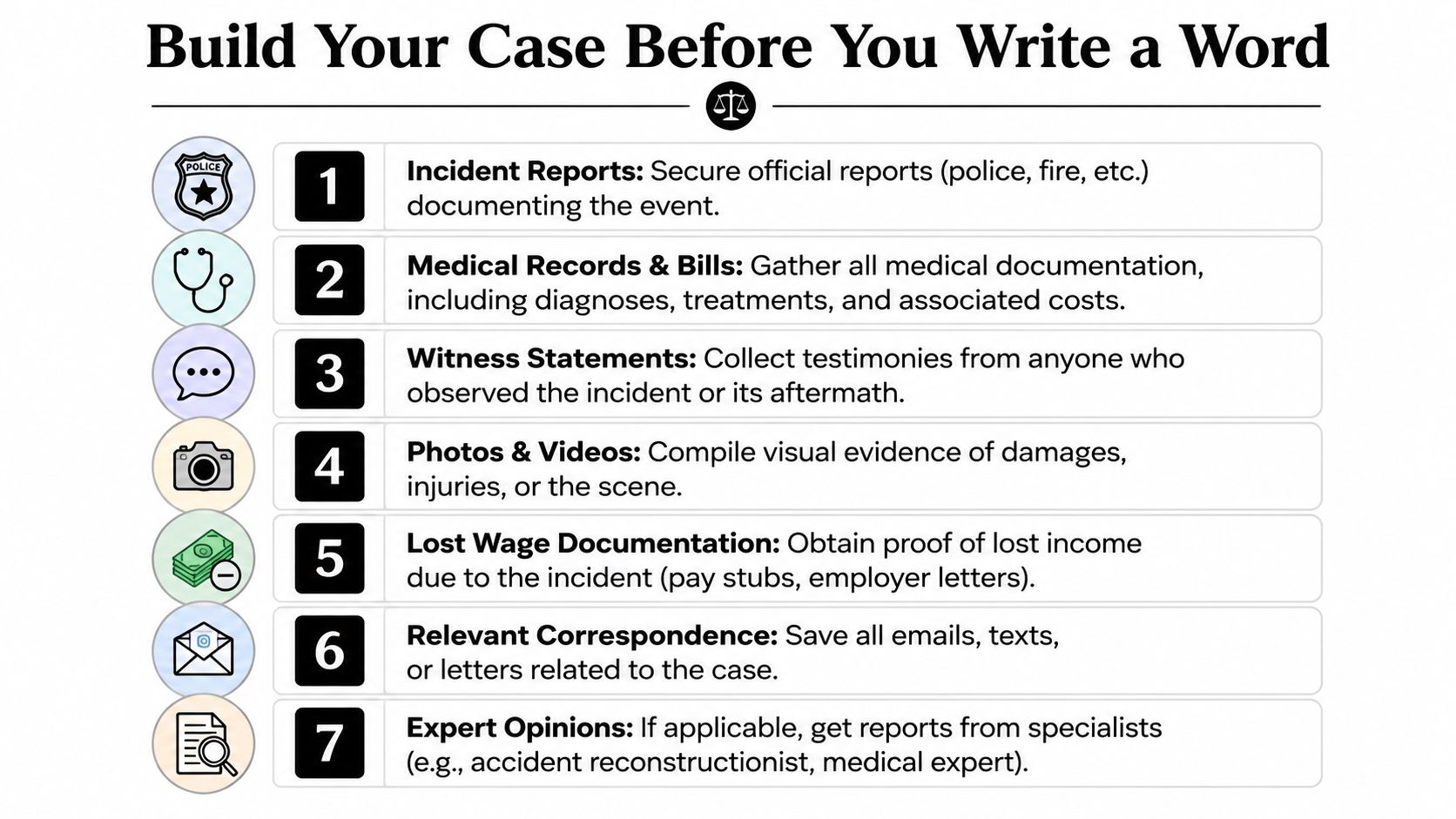

Build Your Case Before You Write a Word

A demand letter without proof is just a conclusion. Before you draft anything, build a file that supports every point you plan to make. If you can't point to a document, photo, estimate, or appraisal, leave the claim out of the letter until you can.

The core file every claimant needs

Start with the basics. These are the records that usually matter in either a diminished value claim or a total loss dispute:

- Claim identifiers. Keep the claim number, adjuster name, policy details, and date of loss in one place.

- Incident records. Police report, exchange of information, towing receipt, and any written admission or coverage notice.

- Visual proof. Save clear pre-loss and post-loss photos if you have them. Photos help show condition, trim, options, and damage severity.

- Repair records. Include the final repair invoice, parts list, and any supplements. For a total loss dispute, include the insurer's valuation report and settlement breakdown.

- Correspondence. Save every email, portal message, text, and letter. A clean communication trail often matters more than people expect.

If you want a practical checklist for organizing that material, this auto claim documentation guide is useful because it shows what to gather before you start arguing value.

What matters for diminished value

A diminished value claim rises or falls on one point: the car may be repaired, but the market still treats it as worth less after an accident history.

For that type of demand, focus on these items:

- Repair invoice and damage scope. This shows what was hit, what was replaced, and whether structural or major panel work occurred.

- Vehicle details. VIN, mileage, trim, options, service condition, and any upgrades that affect market perception.

- Pre-accident condition evidence. Maintenance records and clean-condition photos help show the vehicle had real value before the crash.

- Independent appraisal report. This is the anchor. Without it, your number looks self-generated.

The insurer may have its own formula or internal worksheet. That doesn't mean you should accept it. A third-party valuation gives you something concrete to attach and cite.

What matters for total loss disputes

A total loss fight is different. Here, the issue isn't post-repair stigma. It's whether the insurer's valuation reflects your vehicle's market value.

Build around these records:

| Item | Why it matters |

|---|---|

| Insurer valuation report | Shows the comps, adjustments, and condition assumptions they used |

| Vehicle options list | Carriers often miss trim packages, tech, wheel packages, towing equipment, or specialty upgrades |

| Recent photos | Helps prove actual condition before the loss |

| Maintenance and improvement records | Supports better condition and helps rebut low-condition adjustments |

| Independent appraisal | Gives an outside market-based opinion to challenge weak or mismatched comparables |

A lot of clients think the letter itself does the heavy lifting. It doesn't. The file does.

If your documents are thin, your demand sounds negotiable before anyone even reads the number.

Organization beats volume

Don't attach everything in random order. Label files clearly. Use names that make sense, such as “Repair Invoice Final,” “Valuation Report Carrier,” or “Photos Pre-Loss Exterior.” If you're working with a lawyer or a firm that handles large case volume, the process looks a lot like the intake discipline described in this guide to large law firm CRM. The point isn't the software. The point is that organized claims get handled faster and argued better.

You don't need fancy tools. A clean folder structure and a numbered exhibit list are enough. But you do need to know where every supporting document is before you write your first sentence.

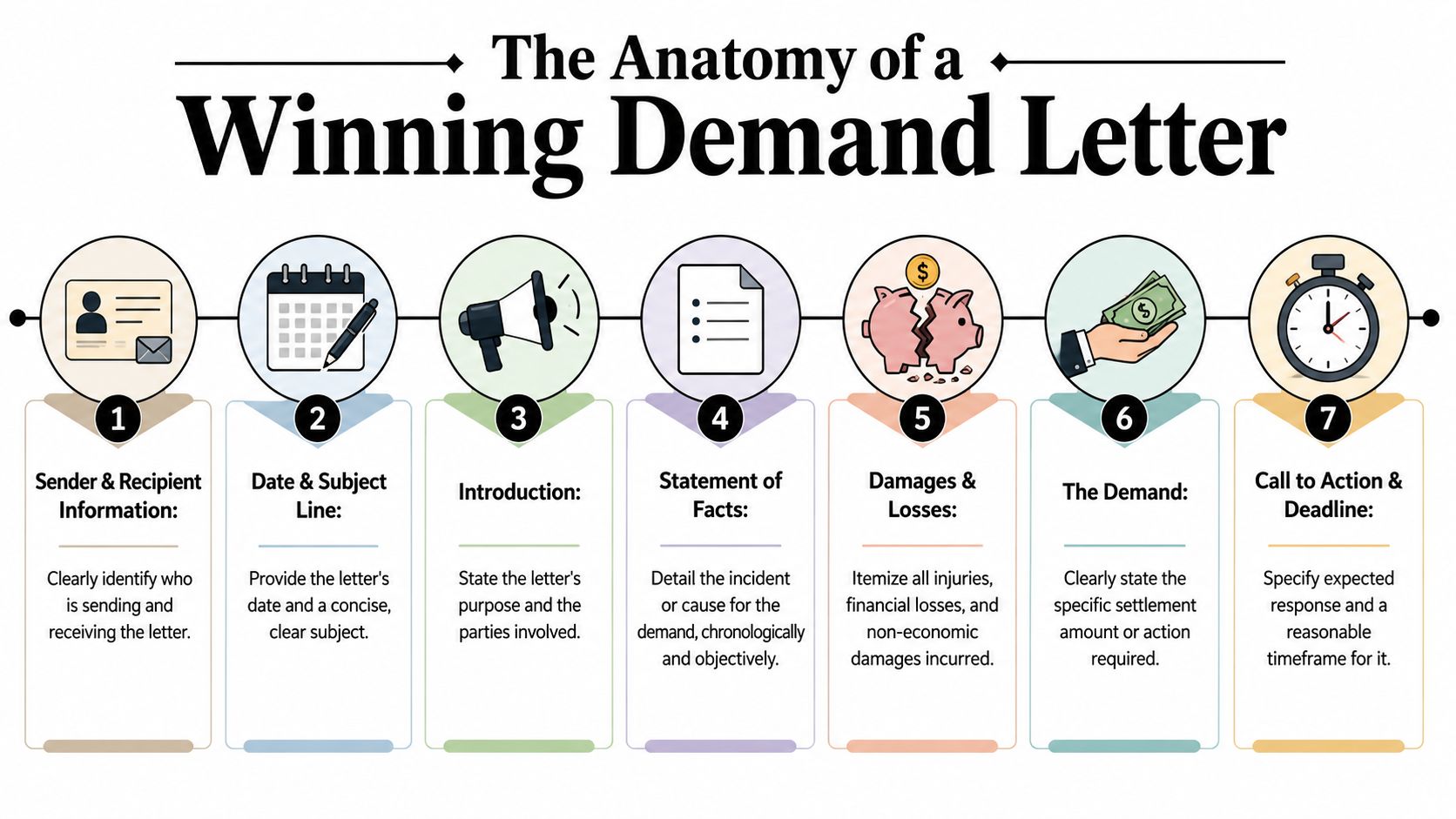

The Anatomy of a Winning Demand Letter

Structure matters because adjusters scan before they read. If your letter is easy to follow, your position lands faster. If it's bloated, emotional, or vague, the adjuster hunts for the number, ignores half the rest, and moves on.

The seven parts that should always be there

Header

Put your full name, address, email, phone number, and the date at the top. Then list the adjuster's name, company, and mailing address.

Subject line

Include the claimant name, date of loss, claim number, and vehicle information if relevant.

Re: Demand for settlement, claim number, date of loss, vehicle year make model

Opening paragraph

State why you're writing in one short paragraph.

I am submitting this demand for payment arising from the collision on [date]. This letter concerns my claim for [diminished value / total loss settlement dispute] involving my [vehicle].

Statement of facts

Keep this chronological and calm. Say what happened, who was involved, and why the other driver or carrier is responsible. Don't crowd this section with opinion.

Damages and support

Connect the loss to documents. Mention the repair invoice, valuation report, photos, and appraisal in plain language.

The demand

Ask for a specific amount or specific corrective action. Don't hedge.

Based on the enclosed documentation, I demand payment in the amount of [amount] to resolve this claim.

Deadline and delivery instructions

Tell them when and how to respond. Make it simple.

A plain-English model works better

A lot of people think a demand letter should sound like a lawsuit. That usually backfires. Adjusters respond better to writing that is direct, readable, and tied to records. If you need help stripping legal clutter out of your draft, HireParalegals' legal writing guide is a solid reference for writing in plain English without losing authority.

Here's a useful flow to follow:

Start with identification

Make sure the adjuster can route the letter without guessing.

- Your details. Full legal name and current contact information.

- Their details. Adjuster name, claims office, and any department identifier.

- Claim details. Claim number, date of loss, and vehicle description.

Tell the facts without argument

Many first drafts go off course. People over-explain, accuse, or editorialize. Keep it restrained.

On [date], your insured struck my vehicle. Liability has already been established under the claim. My vehicle then required repairs as documented in the enclosed records.

That's enough. You're setting context, not reliving the collision.

A short video can also help if you want to see how professionals frame demands in practice.

Show the loss in a way they can answer

This part should track your evidence. For example:

- For diminished value. Explain that despite completed repairs, the vehicle now carries accident history that affects market perception and resale.

- For total loss. Explain that the insurer's valuation does not reflect the actual vehicle configuration, condition, or comparable market data.

Make the ask clean

Don't write three alternative demands in the same letter. Pick one path.

| Weak phrasing | Better phrasing |

|---|---|

| I think I deserve more | I demand payment in the amount of [amount] |

| Please reconsider your offer | Please review the enclosed records and issue revised payment |

| This is unfair | The current valuation does not reflect the vehicle's documented condition and features |

Close with your signature and list the exhibits you're enclosing. That exhibit list matters. It tells the adjuster this wasn't dashed off in frustration. It was assembled.

Two Real-World Demand Letter Examples

Templates help, but only if you understand why the wording works. These examples are short enough to adapt and strong enough to use as a model. Replace the bracketed details with your actual facts and documents.

Example one for diminished value

[Your Name]

[Address]

[Email]

[Phone]

[Date]

Claims Adjuster Name

[Insurance Company]

[Address]

Re: Diminished Value Demand

Claim No. [Claim Number]

Date of Loss [Date]

Vehicle [Year Make Model VIN]

Dear [Adjuster Name],

I am submitting this demand for diminished value arising from the collision on [date]. Your insured caused damage to my [year make model], and the vehicle required repairs as documented in the enclosed repair records.

Before the loss, the vehicle was in [brief condition description], with approximately [mileage] miles and no prior accident history to my knowledge. After the collision, the vehicle underwent repair. Even with completed repairs, the market does not treat an accident-involved vehicle the same as a similar vehicle with a clean history.

I have enclosed the repair documentation, photographs, and an independent appraisal evaluating the vehicle's loss in market value after the accident. Those records support my position that the vehicle has sustained measurable diminished value beyond the cost of repair.

Based on the enclosed documentation, I demand payment in the amount of [demand amount] to resolve this claim. Please provide your written response by [date].

Sincerely,

[Your Name]

Enclosures:

Repair invoice

Photographs

Independent appraisal

Relevant correspondence

The second paragraph matters because it establishes pre-loss condition without over-claiming. Don't say “mint” unless you can prove it. Credibility is worth more than dramatic wording.

Notice what this sample avoids. It doesn't threaten suit in every line. It doesn't accuse the adjuster of bad faith. It doesn't wander into pain and suffering or unrelated complaints. It stays on one issue: post-accident loss in value.

Example two for total loss

[Your Name]

[Address]

[Email]

[Phone]

[Date]

Claims Adjuster Name

[Insurance Company]

[Address]

Re: Total Loss Settlement Demand

Claim No. [Claim Number]

Date of Loss [Date]

Vehicle [Year Make Model VIN]

Dear [Adjuster Name],

I am writing to dispute the current total loss valuation for my [year make model]. The settlement amount offered does not reflect the vehicle's actual market value, condition, and equipment at the time of loss.

The valuation provided by your company appears to rely on comparables and adjustments that do not accurately match my vehicle. My vehicle included [key options or features], and it was in [brief condition description] before the loss. I have enclosed supporting photographs, maintenance records, the insurer's valuation report, and an independent appraisal for review.

The enclosed appraisal identifies the vehicle's market value based on appropriate comparable vehicles and documented condition. For that reason, I reject the current settlement figure and demand payment in the amount of [demand amount].

Please respond in writing by [date]. If you need confirmation of any enclosed record, I'm prepared to provide it promptly.

Sincerely,

[Your Name]

Enclosures:

Carrier valuation report

Photos

Maintenance records

Independent appraisal

Option or feature documentation

A total loss letter works best when you attack the valuation method, not the adjuster personally. Focus on bad comparables, missing options, and unsupported condition adjustments.

Why these examples work

Both letters share the same strengths:

- They identify the dispute fast

- They tie the claim to enclosures

- They state a clear demand

- They set a written response expectation

What they don't do is just as important. They don't bluff. They don't use legal jargon for effect. And they don't bury the actual ask under a page of anger.

If you're learning how to write demand letter drafts for the first time, this is the tone to copy. Firm. Documented. Easy to answer.

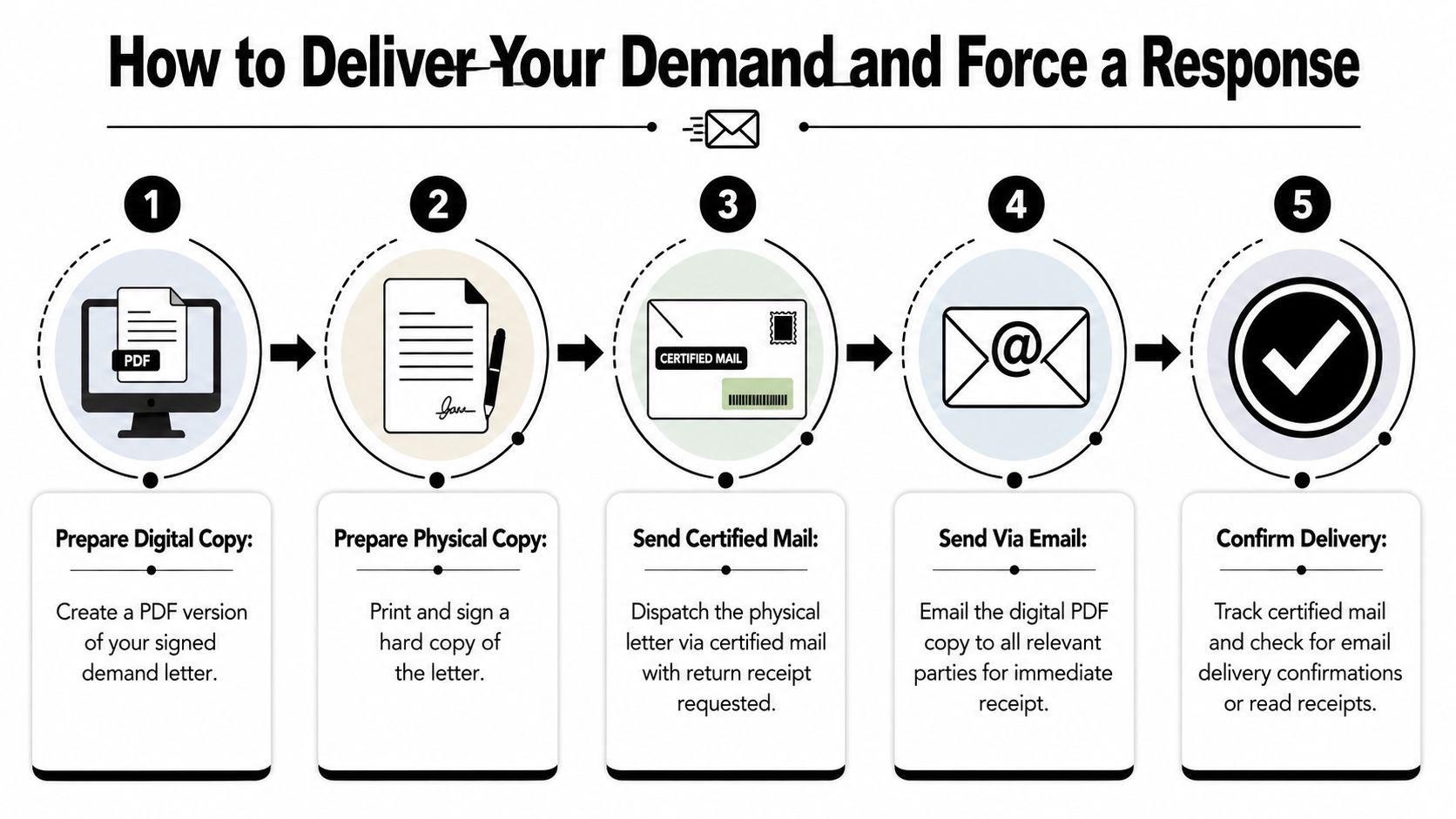

How to Deliver Your Demand and Force a Response

Writing a strong demand is only half the job. Delivery now matters almost as much as content. The old advice says to send it by certified mail and wait. That still matters, but it's no longer enough on its own.

Why certified mail still matters

A 30-day response timeline is the standard benchmark for most demand letters, and sending by certified mail is the step that documents delivery and starts that clock in a verifiable way, according to this guidance on demand letter timelines and certified mail procedure. That isn't paperwork for its own sake. It gives you proof of mailing, proof of receipt, and a clean record if the file later turns into a procedural fight.

Certified mail is the formal channel. Use it.

Why email now needs to accompany it

But don't stop there. A modern insurer often routes claims through digital systems, assigned email workflows, and scanned document queues. If your letter only arrives physically, it can sit in a mailroom or image queue while the response window drifts.

That's why I recommend a dual-channel delivery approach:

- Send the signed hard copy by certified mail

- Send the same signed letter as a PDF by email

- Email the adjuster and, if available, the claim contact or case manager

- Keep the email short, neutral, and administrative

This doesn't replace the mailed copy. It reinforces it.

Send one message the mailroom can track, and one message the claims desk can't ignore.

A workable email template

Use a subject line that matches the file exactly.

Subject: Demand Letter Submitted, Claim No. [Claim Number], [Your Name]

Then keep the body simple:

Dear [Adjuster Name],

Attached is a PDF copy of my signed demand letter regarding Claim No. [Claim Number], sent today by certified mail as well. Please confirm receipt and direct any response in writing to the contact information listed in the letter.

Thank you,

[Your Name]

Don't negotiate by email in that first message. Don't add extra commentary. The email's job is delivery confirmation and visibility.

If you want help once the response arrives, this guide on how to negotiate with an insurance adjuster is a practical next read because it deals with what to say after the letter lands.

Navigating the Insurer's Response and Next Steps

Once your demand is out, the insurer usually does one of four things. They pay. They counter. They deny. Or they stall.

The stall is more common than many people expect, especially if a claimant only uses paper delivery. A 2025 Consumer Financial Protection Bureau report found that 54% of auto insurers reject or delay physical demand letters sent without a digital follow-up, and data cited alongside it shows that 61% of claimants who used both certified mail and email received responses within 10 days, versus 31 days for mail-only, as summarized in this discussion of demand-letter delivery and insurer response patterns. That's why the delivery method matters so much now.

If they pay

Good. Review the release before signing it. Make sure the amount matches the agreement and that you understand what claims you're giving up.

If they counter

This is the most common useful response. Don't treat a counter as a final answer. Read it against your evidence.

Ask yourself:

- Did they address the appraisal directly

- Did they correct any missing options or wrong comparables

- Did they just increase the number without explaining why

A serious counteroffer usually engages your documents. A weak one just moves the number a little and hopes you're tired.

If they deny

A denial of a well-supported demand tells you something important. The problem may no longer be your explanation. It may be the carrier's valuation position.

That's often the point where appraisal becomes the smarter path, especially in vehicle value disputes. An appraisal clause can remove valuation from the insurer's internal software and put it into a structured dispute process with independent involvement.

When the carrier won't move off its number despite documentation, stop repeating yourself and change the process.

If they ignore you

Silence is a response too. If you sent the letter correctly and preserved your records, you now have an advantage. Follow up in writing, attach the original email, and reference the mailed delivery record.

If the nonresponse continues, you may need to escalate outside the claim file. One option is a regulatory complaint. If you're considering that route, this overview of the insurance commissioner complaint process helps you understand when a complaint makes sense and what documentation helps.

A demand letter is a test. It tests whether the insurer will deal fairly with a documented claim. If they won't, that doesn't mean your case is weak. It often means the informal stage is over.

If your insurer is lowballing a total loss or ignoring diminished value after a not-at-fault accident, Total Loss Northwest can help you move from argument to evidence. They specialize in independent total loss and diminished value appraisals, and they help vehicle owners use the appraisal process to challenge biased carrier valuations with real market support.